- Automation & Robotics

- Pavement Tester Market

Pavement Tester Market Size, Share, and Growth Forecast, 2026 – 2033

Pavement Tester Market by Product Type (Instruments, Kits & Accessories, Others), Testing Type (Asphalt Content Testing, Soil Density Testing, Others), End-user (Roadway Construction Industries, Government Agencies, Others), and Regional Analysis 2026 – 2033

Pavement Tester Market Size and Trends Analysis

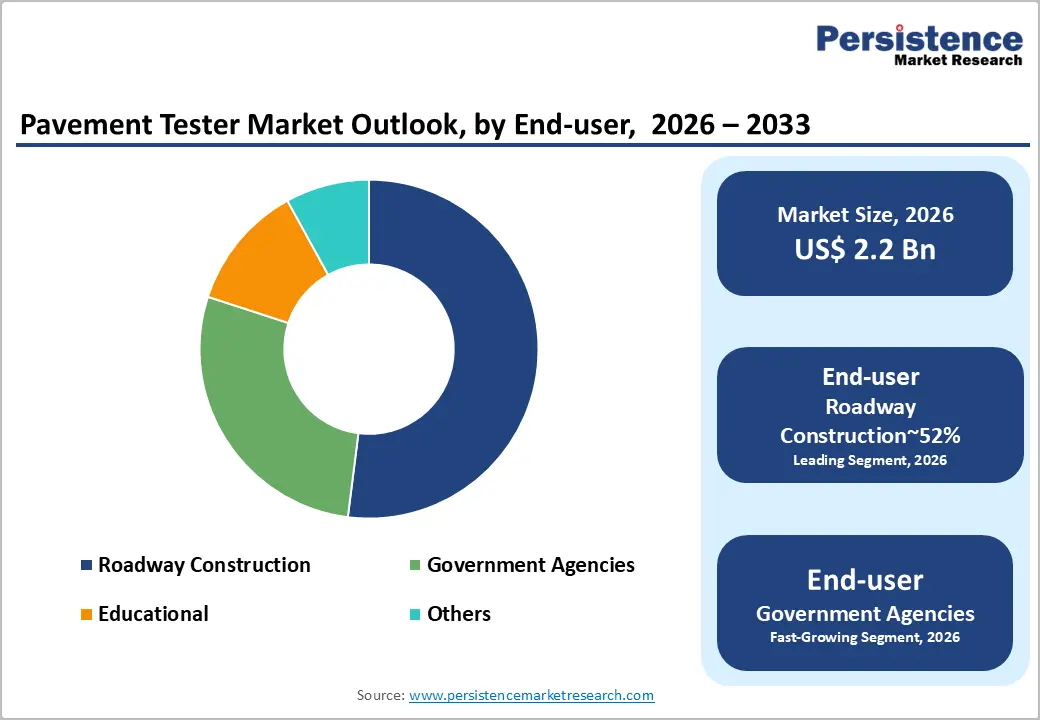

The global pavement tester market size is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by expanding public infrastructure investment initiatives, increasing adoption of non-destructive pavement testing technologies, and stronger regulatory requirements related to pavement quality assessment and certification. These factors are anticipated to sustain steady demand for pavement testing equipment over the forecast period. Rising road construction activities in the Asia Pacific region, along with ongoing highway maintenance and rehabilitation programs across North America and Europe, are expected to strengthen demand across multiple regions. The market is also likely to benefit from greater government procurement of testing equipment, higher testing frequency associated with the growing use of recycled asphalt materials, and the emergence of smart city initiatives that incorporate advanced pavement monitoring systems.

Key Industry Highlights:

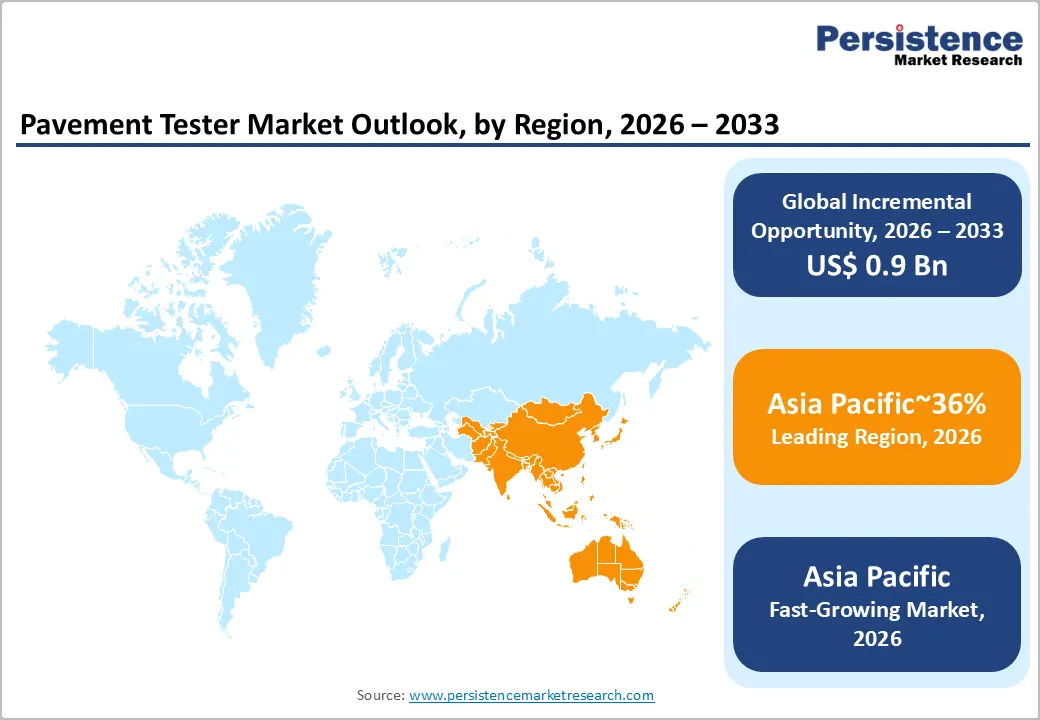

- Leading Region: Asia Pacific is projected to lead, accounting for approximately 36% share in 2026, supported by large-scale highway construction programs under China’s Belt and Road Initiative, India’s Bharatmala Pariyojana multi-year highway development agenda, and aggressive government infrastructure funding pipelines across Southeast Asian economies.

- Fastest Growing Region: Asia Pacific is also anticipated to grow the fastest, driven by rapidly expanding urban pavement networks in China and India, accelerating smart city pavement monitoring requirements, and significant public capital allocations toward transportation corridor modernization.

- Leading Product Type: Instruments are expected to lead, accounting for approximately 55% share in 2026, anchored by regulatory compliance workflows requiring traceable measurement, the technical depth of falling weight deflectometers and asphalt content analyzers, and their broad deployment across highway quality assurance operations.

- Leading End-user: Roadway construction is projected to dominate, holding approximately 52% share in 2026, driven by sustained public infrastructure investment, multi-stage testing requirements per construction project, and EPC contractor quality compliance programs.

| Key Insights | Details |

|---|---|

| Pavement Tester Market Size (2026E) | US$2.2 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Infrastructure Modernization Programs Expanding Pavement Testing Procurement Globally

National infrastructure modernization mandates are generating sustained procurement demand across pavement testing equipment categories. Governments in North America, Asia Pacific, and Europe are committing multi-year capital allocations toward highway rehabilitation, new road construction, and urban transit corridors. These commitments create direct purchasing requirements for field-deployable and laboratory testing instruments capable of validating pavement performance across asphalt content, soil density, and load-bearing parameters. The causal chain from infrastructure appropriation to equipment procurement is shortening as transportation agencies standardize testing protocols, driving consistent volume demand across market segments. U.S. Infrastructure Investment and Jobs Act, and Europe’s Trans-European Transport Network framework are collectively reinforcing multi-jurisdictional demand streams.

Product innovation from Dynatest with DynaWare, a modernized hardware and software upgrade platform for the Falling Weight Deflectometer series, illustrates how established manufacturers are aligning portfolios with increased frequency and scale of government testing workflows. GSSI with the RealTime Density Scan GPR sensor, developed through an April 2025 collaboration with Hamm AG via the Smart Compact system, is positioned to accelerate real-time compaction verification across major highway projects globally. These innovations are expected to elevate instrument utilization rates per project site, expanding the addressable market for both hardware and associated service contracts. As public infrastructure funding cycles deepen, demand for durable, high-precision pavement testing instruments is likely to sustain across both greenfield and rehabilitation construction corridors.

AI and Sensor Integration Elevating Non-Destructive Instrument Adoption

The integration of artificial intelligence and advanced sensor arrays into pavement testing instruments is transforming operational efficiency across field and laboratory environments. AI-powered diagnostic systems enable automated pattern recognition, real-time anomaly flagging, and predictive maintenance scheduling, reducing manual labor requirements per testing cycle significantly. These capabilities are particularly compelling for large-scale highway agencies managing thousands of lane-kilometers annually, where automated data interpretation accelerates condition assessments without proportional increases in skilled personnel. The return-on-investment proposition is expected to accelerate instrument adoption among government agencies and engineering firms pursuing lifecycle cost optimization strategies.

Controls Group, with its AI-driven automated pavement testing platform, demonstrates how Tier 1 manufacturers are embedding machine-learning analytics into hardware for real-time field monitoring. Troxler Electronic Laboratories, with the Model 3430 nuclear density gauge, is anticipated to incorporate enhanced connectivity capabilities, enabling cloud-based data aggregation across dispersed testing sites. The convergence of IoT architecture, high-resolution sensors, and predictive analytics is expected to support premium pricing for advanced instrument platforms while expanding the installed base across mid-tier procurement tiers. Manufacturers investing in unified hardware-software ecosystems are positioned to capture recurring service revenues alongside initial equipment sales, creating durable commercial relationships with institutional buyers.

Barrier Analysis – Calibration Traceability Requirements Increasing Operational Overhead in Public Procurement

Regulatory traceability requirements for pavement testing instruments, particularly within public infrastructure procurement, mandate formal calibration certification, documented chain of custody, and periodic third-party verification across instrument lifecycles. These compliance obligations add significant operational overhead to testing programs, particularly for organizations managing distributed instrument fleets across multiple construction sites simultaneously. The administrative burden of maintaining calibration traceability slows rapid fleet expansion, moderating new instrument acquisition among high-volume contractors who prioritize operational agility. Compliance complexity is further amplified in multi-jurisdictional projects where differing national standards impose layered certification requirements on participating vendors.

Commercial implications include extended procurement timelines for government tenders, as instrument shortlisting processes incorporate traceability audits alongside technical performance evaluation. PaveTesting Ltd., with the TRRL Beam Fatigue Apparatus, is positioned to leverage its certified calibration service network as a differentiated procurement credential within European public works frameworks. Forney LP, with its automated compression testing systems, is expected to align product documentation capabilities with evolving ASTM and ISO traceability standards to maintain procurement eligibility in North American government contracts. Manufacturers investing in embedded calibration management software are anticipated to reduce customer compliance overhead, improving instrument retention rates and service contract renewal cycles.

Skilled Operator Shortage Constraining Field Deployment Efficiency in High-Growth Regions

The operational complexity of advanced pavement testing instruments requires trained technicians capable of configuring equipment, interpreting sensor outputs, and maintaining calibration standards under field conditions. A structural shortage of qualified testing professionals, particularly in fast-growing markets across Southeast Asia and parts of Latin America, is expected to constrain the deployment efficiency of high-capability instrument systems. Infrastructure project timelines are extending where testing bottlenecks arise from operator unavailability, creating friction in procurement cycles and reducing perceived operational ROI for premium equipment platforms. This challenge is expected to moderate adoption velocity in precisely the markets where commercial growth potential is greatest.

The skills gap creates indirect competitive pressure for manufacturers whose instruments require extensive training protocols, potentially favoring simpler field-deployable alternatives in operator-constrained environments. Zorn Instruments, with the ZFG Dynamic Plate Load Tester, is positioned to benefit from growing demand for user-friendly, low-complexity testing equipment in markets with nascent operator capability. Matest S.p.A., with its Automatic Marshall Apparatus, is expected to invest in training ecosystem partnerships to reduce operator dependency barriers for its laboratory-grade product line. Long-term resolution of this restraint is likely to depend on vocational training infrastructure development and digital interface simplification embedded within next-generation instrument platforms.

Opportunity Analysis – Smart City Pavement Monitoring Programs Creating Recurring IoT-Enabled Demand

The global proliferation of smart city infrastructure programs is creating sustained institutional demand for IoT-enabled pavement condition monitoring platforms across municipal and metropolitan transportation networks. Urban governments and transit authorities are embedding continuous monitoring systems into road networks to enable proactive maintenance interventions and extend pavement service life beyond traditional scheduled cycles. This demand pattern differs structurally from project-based procurement, as smart city frameworks require perpetual sensor deployment, data streaming infrastructure, and periodic instrument upgrades tied to platform evolution. The addressable opportunity encompasses both initial instrument supply and long-term maintenance service contracts, offering manufacturers a recurring revenue structure with strong institutional retention dynamics.

GSSI with the RealTime Density Scan platform and Trimble with its advanced pavement inspection systems are anticipated to be early beneficiaries of smart city procurement programs across North America and Europe. The integration of LiDAR, GPR, and ultrasonic pulse-echo technologies into unified monitoring platforms is expected to differentiate premium vendors in competitive tender processes. Manufacturers capable of offering cloud-connected dashboards alongside physical instruments are positioned to capture significantly higher contract values per municipality. As smart city frameworks expand across Asia Pacific under China’s urbanization agenda and India’s Smart Cities Mission, the IoT-enabled pavement monitoring segment is projected to emerge as a structurally distinct high-growth revenue stream.

Airport Runway Pavement Testing Expansion Unlocking High-Precision Procurement Channels

Civil aviation infrastructure expansion across Asia Pacific, the Middle East, and Africa is creating specialized demand for high-precision runway pavement testing systems operating beyond standard highway specifications. Airport runway assessments impose the most stringent performance tolerances of any pavement application, requiring deflection measurement accuracy, friction coefficient analysis, and subsurface structural integrity evaluation within civil aviation certification frameworks. The premium pricing commanded by aviation-grade testing instruments, combined with mandatory testing cycles tied to aircraft weight classification and runway recertification schedules, creates a structurally attractive demand niche. This segment is expected to expand significantly as new terminals and airport expansion projects advance across high-growth developing regions.

Dynatest with DynaWare and the Falling Weight Deflectometer platform is positioned to lead airport runway pavement assessment procurement, given its established international certification pedigree and multi-decade institutional relationships with civil aviation authorities. ARA (Applied Research Associates), with its RoadSoft pavement management system, is expected to deepen integration between structural testing data and runway lifecycle planning, creating a compelling data-led procurement proposition for airport operators. Operators seeking to reduce runway rehabilitation costs through predictive maintenance strategies are likely to prioritize advanced non-destructive testing platforms, enabling manufacturers to command premium price points across this specialized high-value application channel.

Category–wise Analysis

Product Insights

Instruments are forecasted to dominate the product segment, accounting for approximately 55% share in 2026, underpinned by the sector’s demand for high-precision, regulatory-grade measurement tools across both field and laboratory applications. Instruments such as falling weight deflectometers, asphalt content analyzers, nuclear density gauges, and friction testers are widely used in pavement evaluation and testing. These tools play a fundamental role in supporting pavement performance assessment. Dynatest with DynaWare, a modernized FWD hardware and software platform, and Troxler Electronic Laboratories with the Model 3430 nuclear density gauge exemplify the technology leadership driving sustained instrument procurement across institutional buyers globally. The integration of AI-driven diagnostics and IoT connectivity into flagship instrument platforms is anticipated to accelerate replacement cycles among agencies seeking enhanced data management capabilities.

Kits & Accessories are expected to be the fastest-growing segment, driven by rising test frequency across multi-site construction projects and the growing standardization of consumable-dependent testing methodologies. Sample preparation tools, calibration standards, molds, probes, and field-ready consumable assemblies are witnessing rising demand across the pavement testing ecosystem. Gilson Company is well-positioned to benefit from this demand growth. The company’s HM-5000 Asphalt Content Tester accessory ecosystem supports ongoing testing operations through compatible consumables and calibration components. Similarly, Matest S.p.A. offers a modular laboratory accessory portfolio. This product line enables laboratories to scale testing capacity while maintaining consistent calibration standards. Large highway development programs are currently active across numerous construction corridors in the region. As project-level testing protocols intensify, the need for repeatable accessories and consumables is expected to grow significantly.

End-user Insights

Roadway construction is expected to lead the market, accounting for approximately 52% share in 2026, driven by sustained public infrastructure investment, EPC contractor quality compliance requirements, and the technical complexity of large-scale paving operations necessitating continuous field testing across multiple construction stages. Highway construction projects require pavement testing at workflow stages spanning subgrade preparation through asphalt laying, compaction, and surface finishing, generating exceptional instrument utilization intensity per project kilometer. Controls Group, with its automated pavement testing platform, and Forney LP, with its compression testing systems, are central to the procurement frameworks of major highway contractors operating at a national scale. National infrastructure programs, including India’s Bharatmala, the U.S. Infrastructure Investment and Jobs Act, and Europe’s TEN-T network, are expected to sustain multi-year procurement tailwinds for highway construction-grade testing equipment.

Government agencies are expected to be the fastest-growing, driven by the structural shift toward independent infrastructure quality validation, expanding regulatory compliance mandates, and increased public accountability requirements for construction quality outcomes. Transportation ministries and highway authorities across Asia Pacific and North America are institutionalizing direct testing capabilities, procuring instruments independently rather than relying exclusively on contractor reporting to ensure unbiased pavement performance data. Dynatest with DynaWare and Humboldt Mfg. Co., with its field pavement testing range, is positioned as a preferred vendor across government agency procurement frameworks, given established institutional relationships and compliance-aligned product documentation. The growing emphasis on lifecycle cost management in public infrastructure budgeting is expected to propel government agencies toward proactive testing investment, accelerating their emergence as a structurally distinct high-value demand segment.

Regional Insights

Asia Pacific Pavement Tester Market Trends

Asia Pacific is projected to remain the largest regional market in the Pavement Tester Market. The region is also expected to record the fastest growth trajectory. It is estimated to hold around 36% of the global market share in 2026. This leadership is driven by both strong demand volumes and rapid growth momentum. These trends are supported by the region’s exceptionally high level of infrastructure investment. Major national highway programs are playing a central role in driving this demand. Examples include China’s Belt and Road Initiative. India’s Bharatmala Pariyojana is also contributing significantly to road infrastructure expansion. In addition, regional connectivity strategies across the Association of Southeast Asian Nations are strengthening transport corridors. Dynatest is expected to strengthen its presence in the Asia Pacific market. The company’s DynaWare supports advanced pavement analysis and monitoring functions. Similarly, Geophysical Survey Systems, Inc. is likely to expand regional adoption of its RealTime Density Scan.

The rapid development of smart city ecosystems across major metropolitan corridors is also influencing the market. This expansion is particularly visible in China, India, and Southeast Asia. As a result, there is an increasing demand for IoT-enabled infrastructure monitoring platforms. China is projected to act as the main anchor for market momentum in the Asia Pacific region. This expectation is largely driven by the country’s massive expansion of its highway network. It is also supported by strong expressway quality assurance programs. China’s Ministry of Transport has allocated significant capital to transportation infrastructure development. This investment covers the construction of thousands of kilometers of new highways. It also includes programs designed to ensure strict quality compliance in road construction. The company offers AI-driven automated pavement testing systems that align with the country’s infrastructure monitoring initiatives. Similarly, Matest S.p.A. is also likely to expand its distribution network via China-based partners. Its Automatic Marshall Apparatus supports pavement quality evaluation in large-scale road construction projects.

North America Pavement Tester Market Trends

North America is expected to remain a mature and structurally stable regional market. Demand is largely supported by infrastructure rehabilitation cycles, compliance-driven upgrades of testing instruments, and the growing institutional use of non-destructive testing methods among federal and state transportation agencies. Highway rehabilitation programs are increasingly prioritizing data-driven lifecycle management instead of traditional reactive maintenance practices. Troxler Electronic Laboratories, with the Model 3430 nuclear density gauge, and Forney LP, with its automated materials testing systems, are strongly embedded in North American government procurement frameworks. Agencies are increasingly seeking improved data capture capabilities that align with evolving federal infrastructure management standards.

The U.S. is projected to anchor North American market momentum because of its large-scale federal and state highway infrastructure investments. It also benefits from a mature procurement ecosystem for pavement testing instruments and a regulatory framework that requires traceable quality verification in public construction programs. Humboldt Mfg. Co., with its field pavement testing portfolio and a recently secured partnership with a U.S. state transportation department, is positioned to deepen its institutional presence. As federal funding cycles accelerate repair and reconstruction workflows, demand for pavement condition assessment instruments is expected to remain elevated to support systematic field testing across diverse pavement types.

Europe Pavement Tester Market Trends

Europe is expected to remain a mature and structurally stable regional market. This outlook is supported by sustainability-driven infrastructure upgrades and stringent compliance frameworks aligned with Trans-European Transport Network quality standards. The European Union’s infrastructure digitalization initiatives include hundreds of funded projects focused on pavement assessment and road condition monitoring across member states. These programs are expected to sustain procurement of testing instruments at steady, measured volumes throughout the forecast period. PaveTesting Ltd., with the TRRL Beam Fatigue Apparatus, and Matest S.p.A., with its automated laboratory testing systems, are well-positioned within European procurement ecosystems. The growing adoption of recycled asphalt pavement materials under EU sustainability mandates is expected to increase testing intensity for each infrastructure project.

Germany is expected to serve as the primary anchor for European market dynamics because it is the region’s largest road infrastructure economy and hosts a strong ecosystem for advanced materials testing certification. It also has a high concentration of engineering and construction firms that are leading investments in pavement quality assurance. German transportation authorities operating under the Bundesfernstraßen federal highway program are expected to continue procuring precision testing instruments. Cooper Research Technology, through its CRT Asphalt Testing Systems, is well-positioned to remain relevant in Germany’s public infrastructure procurement environment. This is because tenders in the country’s technically demanding market evaluate measurement performance, documentation, and certification depth alongside product pricing.

Competitive Landscape

The global pavement tester market is moderately fragmented, with leadership concentrated among established engineering instrument manufacturers such as Dynatest, GSSI, Humboldt Mfg. Co., Cooper Research Technology, and Controls Group. These companies exert structural influence over the market through their engineering heritage, certification depth, and long-standing procurement relationships with transportation authorities and major engineering, procurement, and construction (EPC) contractors. Competition among leading manufacturers is primarily defined by technological differentiation across sensor precision, software integration, AI-enabled diagnostics, and calibration traceability frameworks. Dynatest, through its DynaWare ecosystem, and GSSI, with the RealTime Density Scan platform, emphasize advanced field diagnostics and real-time measurement capabilities. Humboldt Mfg. Co. and Cooper Research Technology maintain strong positions within laboratory and field testing instrumentation portfolios, while Controls Group is expanding its presence through automated testing platforms that integrate intelligent data processing and workflow automation. Regional distributor partnerships and white-label instrument supply arrangements are also expanding, particularly in emerging markets, allowing mid-tier manufacturers to broaden geographic reach without proportionally increasing direct sales infrastructure.

Key Industry Developments:

- In October 2025, India’s Infrastructure Sector began broad implementation of Drones and LiDAR for precision surveying and road surface defect detection. The shift toward "smart roads" integrates AI-based planning with physical pavement testing, moving the industry from reactive repairs to predictive maintenance.

- In May 2025, Shimadzu Corporation launched the Autograph AGS-V Series, a high-precision universal testing machine for construction materials. This development introduces enhanced precision in measuring the mechanical properties of asphalt and concrete, allowing manufacturers to meet increasingly stringent structural safety standards.

Companies Covered in Pavement Tester Market

- Dynatest International

- Humboldt Mfg. Co.

- Controls Group

- Cooper Research Technology Ltd.

- Geophysical Survey Systems Inc. (GSSI)

- Matest S.p.A.

- Troxler Electronic Laboratories, Inc.

- Gilson Company, Inc.

- PaveTesting Ltd.

- Forney LP

- GDS Instruments

- Zorn Instruments GmbH & Co. KG

Frequently Asked Questions

The global pavement tester market is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$3.1 billion by 2033. This growth trajectory reflects sustained global infrastructure investment, expanding government testing mandates, and progressive adoption of AI-enabled pavement diagnostic platforms across institutional buyer segments.

The primary growth driver is the acceleration of global infrastructure modernization programs, particularly large-scale highway construction and rehabilitation initiatives in Asia Pacific, North America, and Europe. Regulatory mandates requiring traceable pavement quality verification, combined with the transition toward non-destructive testing technologies and AI-integrated instrument platforms, are reinforcing sustained commercial momentum across the forecast period.

The pavement tester market is projected to grow at a CAGR of 5.3% from 2026 to 2033, representing an acceleration from the historical CAGR of 4.8% recorded during the pre-2026 period. This acceleration is expected to be driven by rising testing frequency requirements, smart city procurement programs, and the expansion of government agency direct procurement channels.

Asia Pacific is projected to lead the pavement tester market, accounting for approximately 36% of the global market share in 2026. The region’s leadership is supported by China’s Belt and Road Initiative, India’s Bharatmala highway program, and the rapid expansion of smart city infrastructure frameworks requiring advanced pavement condition monitoring technologies.

Key players include Dynatest International with DynaWare, Humboldt Mfg. Co. with its field testing portfolio, Controls Group with automated AI-driven testing systems, Cooper Research Technology with CRT Asphalt Testing Systems, GSSI with the RealTime Density Scan, Gilson Company with the HM-5000, Matest S.p.A. with its laboratory testing equipment, Troxler Electronic Laboratories with the Model 3430, and Zorn Instruments with the ZFG Dynamic Plate Load Tester.