- Industrial Goods & Service

- Passive Fire Protection Materials Market

Passive Fire Protection Materials Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Passive Fire Protection Materials by Product (Sealants, Intumescent Coatings, Foams & Boards, Mortars, Cementitious Sprays, Putties, Others), Application (Structural, Compartmentation, Opening Protection, Firestopping Materials), End-user (Building & Construction, Oil & Gas, Transportation, Others), and Regional Analysis, 2026 - 2033

Passive Fire Protection Materials Market Size and Trend Analysis

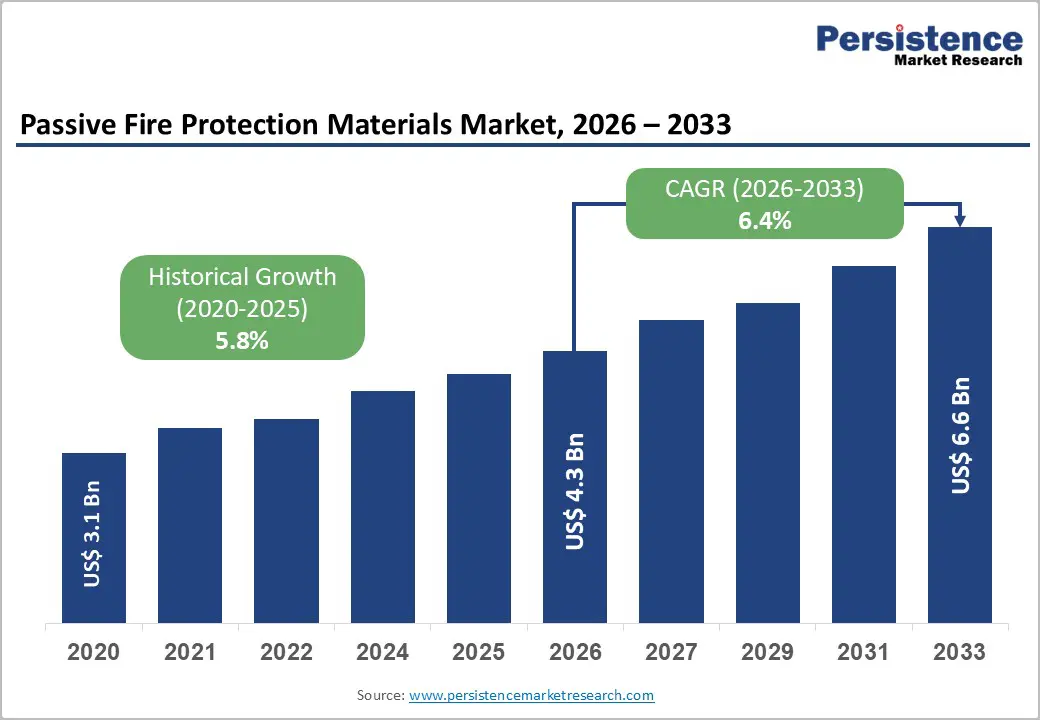

The global passive fire protection materials market size is likely to be valued at US$ 4.3 Billion in 2026 and is expected to reach US$ 6.6 Billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033.

Market growth is driven by stricter global fire safety regulations, rapid Asia-Pacific urbanization with rising high-rise construction, and expanding oil and gas infrastructure demanding specialized fire-resistant materials for high-risk environments

Key Industry Highlights:

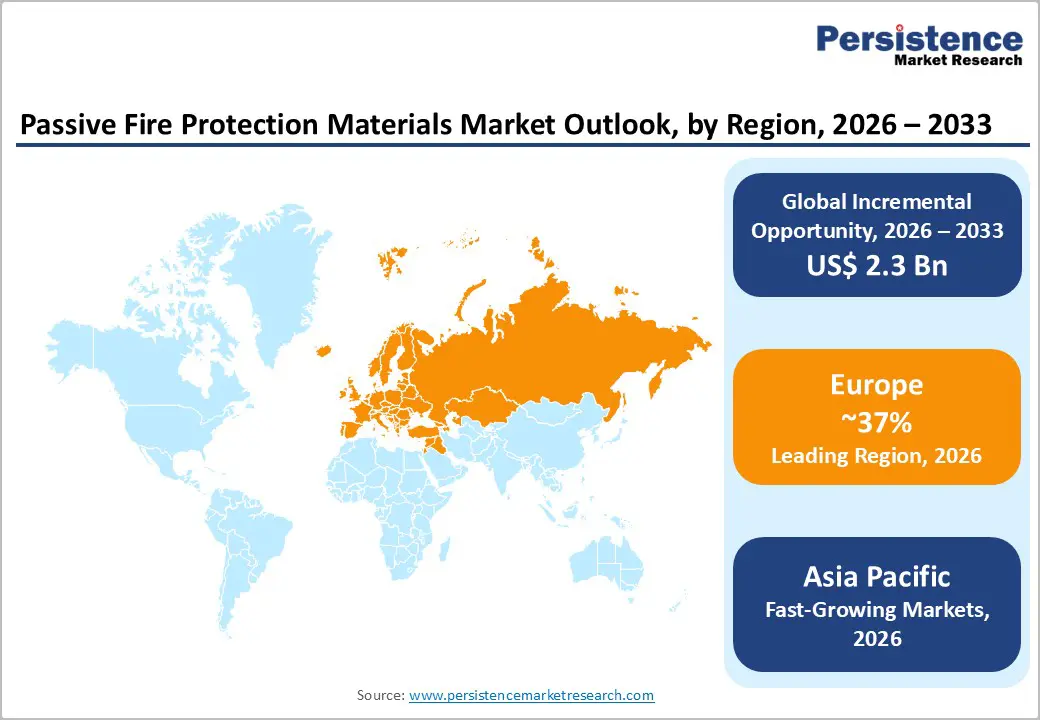

- Leading Region: Europe commands 37% global market share and leads in regulatory enforcement, premium material specifications, and green building adoption, establishing the region as the dominant market foundation with sustained innovation and sustainability-driven demand.

- Fastest Growing Region: Asia-Pacific demonstrates 8.3% CAGR driven by unprecedented urbanization, high-rise building proliferation in China and India, stringent government fire safety mandates, and oil and gas sector expansion at 9.2% CAGR, positioning the region as the primary future growth engine.

- Dominant Application: Structural fire protection applications command 40% of the passive fire protection systems market, addressing critical load-bearing element protection, achieving extended fire-resistance ratings, and meeting building code mandates for structural integrity maintenance during fire events across diverse building typologies.

- Fastest Growing Segment: Thin-film intumescent coatings exhibit 6.2% CAGR growth driven by aesthetic appeal, architectural compatibility, premium specification requirements in commercial construction, and water-based low-VOC formulation development supporting sustainability objectives.

- Key Opportunity: Oil and gas sector expansion, particularly offshore platforms and LNG terminal development in Asia-Pacific, combined with sustainable fireproofing solutions aligned with LEED, IGBC, and Green Mark certifications, represents the highest-potential growth opportunity for specialized, premium-priced passive fire protection products.

| Key Insights | Details |

|---|---|

| Passive Fire Protection Materials Market Size (2026E) | US$ 4.3 Billion |

| Market Value Forecast (2033F) | US$ 6.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.4% |

| Historical Market Growth (2020 - 2025) | 5.8% |

Market Dynamics

Drivers - Stringent Fire Safety Regulations and Mandatory Building Code Compliance

Global fire safety regulations have undergone a significant transformation, directly accelerating the adoption of passive fire protection materials across construction and industrial sectors. In the United Kingdom, regulations such as Approved Document B and the Building Safety Act 2022 mandate strict compartmentalization and fire containment measures for buildings over 11 meters, requiring all external wall materials and insulation to meet certified non-combustible standards. Across North America, jurisdictions increasingly reference NFPA standards, particularly NFPA 285 for external wall assemblies, with New York introducing stricter fireblocking requirements that influence broader regional practices.

The European Union’s EN 13501-1/2 Euroclass system, supported by country-specific codes in Germany, France, and Spain, creates harmonized yet locally tailored compliance requirements. Market analysis indicates a 7.2% annual increase in demand following new code implementations, while manufacturers report approximately 20% annual growth in thin-film intumescent coatings as architects specify premium, visually appealing fireproofing solutions for exposed structural elements in high-rise developments.

Accelerated Urbanization and Infrastructure Development Necessitating Fire-Safe High-Rise Construction

Rapid global urbanization is significantly increasing demand for fire-resistant residential and commercial infrastructure, particularly in high-density cities. According to the United Nations Department of Economic and Social Affairs, Asia-Pacific urban populations are projected to increase by an additional 1.2 billion by 2050, thereby intensifying the need for fire-safe construction solutions. China dominates regional demand, supported by massive construction activity and government mandates requiring fire-resistant materials in all public buildings under Ministry of Housing and Urban-Rural Development guidelines.

India’s Smart Cities Mission, covering more than 100 cities, along with the rise in high-rise construction in metros such as Mumbai and Delhi, further strengthens demand for integrated passive fire protection systems aligned with international standards. Southeast Asian nations, including Vietnam and Indonesia, combined with Australia’s Building Codes mandating fire-resistant materials in new constructions, sustain regional growth. With the global construction sector projected to reach US$8 trillion by 2030, passive fire protection demand rises proportionally across structural and compartmentation applications.

Restraints - Capital-Intensive Installation and Ongoing Maintenance Costs Limiting Adoption

Passive fire protection systems entail specialized installation procedures and long-term maintenance requirements that pose substantial cost challenges for developers and building owners. Intumescent coating application requires precise control over film thickness, surface preparation, and multi-layer compatibility, demanding skilled labor, certified technicians, and advanced application equipment. In addition, regulatory compliance requires periodic inspections, testing, and documentation throughout the building lifecycle, particularly for high-risk facilities subject to NFPA 80.

These standards mandate inspections at commissioning, after one year, and at four- to six-year intervals, thereby significantly increasing operational expenses. For cost-sensitive developers in emerging markets, these investments often become prohibitive, thereby limiting adoption. In many developing regions, construction budgets prioritize structural completion over integrated fire safety systems. As a result, smaller contractors and regional developers face barriers to widespread implementation, constraining market growth in price-sensitive geographies despite rising regulatory awareness and long-term safety benefits.

Regulatory Fragmentation and Complex Compliance Certification Requirements Across Jurisdictions

The lack of globally harmonized fire protection standards creates significant compliance complexity for manufacturers and project developers operating across multiple regions. In the United States, performance-based regulations emphasize system outcomes through NFPA 285 testing, whereas the United Kingdom relies on prescriptive requirements that detail cavity barrier placement and installation methods under Approved Document B. European regulations apply EN 13501-1/2 Euroclass classifications, supplemented by national codes that vary in material acceptance and construction methodologies.

Canada further complicates compliance by requiring CCMC approvals in addition to UL 263 or ASTM E119 certifications, with additional provincial amendments. This fragmented regulatory environment forces manufacturers to conduct multiple parallel testing programs, maintain region-specific product formulations, and obtain redundant certifications. These requirements significantly increase product development costs and create entry barriers for smaller manufacturers, limiting standardization, slowing innovation, and reducing competitive flexibility across international markets.

Opportunities - Expansion of Oil and Gas Industry with Specialized High-Temperature Fire Protection Requirements

The oil and gas industry represents the fastest-growing application segment for passive fire protection materials, particularly in the Asia-Pacific region, which is experiencing a 9.2% CAGR. Growth is driven by refinery expansion, offshore platform development, and LNG terminal construction. Fire incidents in Indian refineries have increased over the past decade, prompting higher investments in advanced fireproofing solutions to protect critical assets. Offshore facilities face significant fire risks due to high hydrocarbon exposure, necessitating integrated protection systems that combine intumescent coatings, fireproof cladding, and penetration sealants.

Refineries and gas processing facilities operate in high-temperature environments in which hydrocarbon fires exceed standard cellulosic fire conditions, creating a need for specialized formulations. Government enforcement of stricter safety regulations and insurance mandates requiring certified systems further drives adoption. These factors position oil and gas as a premium, high-value opportunity with long-term contracts and differentiated product requirements beyond conventional construction-grade fireproofing solutions.

Adoption of Sustainable, Low-VOC, and Eco-Friendly Fire Protection Solutions Aligned with Green Building Standards

Sustainability priorities and environmental regulations are increasing demand for environmentally friendly passive fire protection materials worldwide. Water-based, low-VOC intumescent coatings are projected to grow at a 6.2% CAGR through 2034, supported by demand from architects and developers seeking solutions that meet both fire safety and environmental objectives. Green building certifications such as LEED, IGBC, and Singapore’s Green Mark explicitly recognize fire protection materials that contribute to sustainability credits, thereby incentivizing their adoption.

Thin-film intumescent coatings, accounting for 62.4% of the intumescent market in 2025, offer effective fire resistance while preserving architectural aesthetics, making them ideal for premium commercial projects. Although bio-based fireproofing materials currently represent a small market share, increasing R&D investment is improving their performance and cost competitiveness. Manufacturers offering lightweight, recyclable, and non-toxic solutions aligned with circular economy principles are gaining premium positioning and long-term partnerships with sustainability-focused developers.

Category-wise Analysis

Product Type Insights

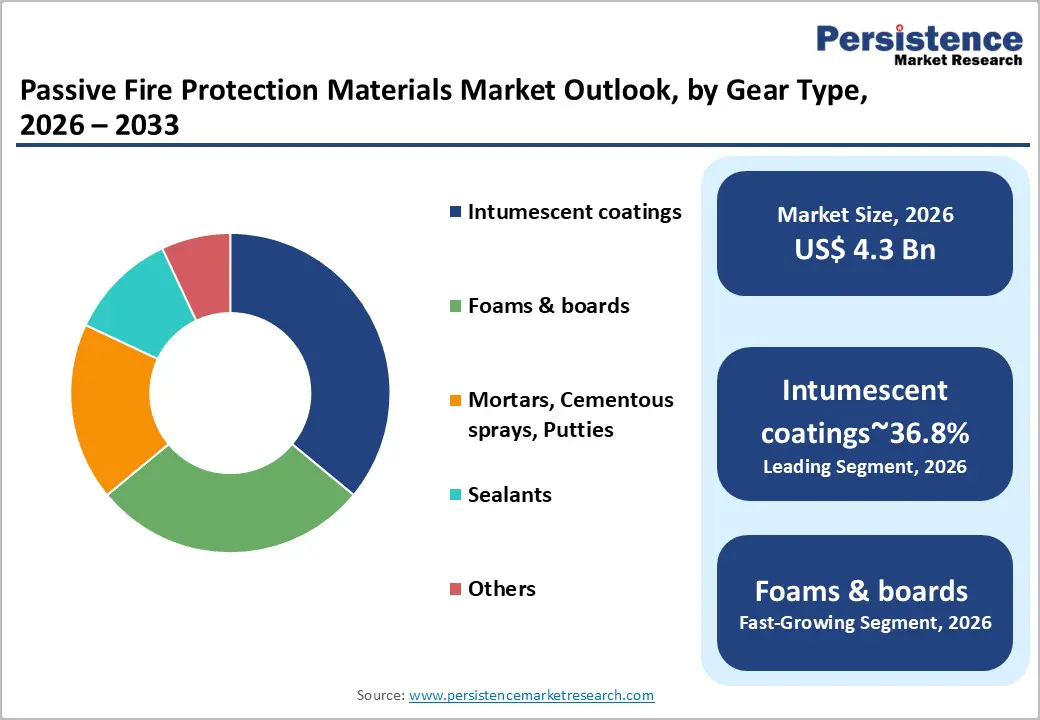

Intumescent coatings dominate the passive fire protection materials market, accounting for approximately 36.8% of total market share. Their leadership is driven by strong performance characteristics, as these coatings expand when exposed to heat, forming an insulating char layer that protects structural materials from fire and radiant heat. Intumescent coatings are highly versatile and can be applied by spray, brush, or roller to steel, concrete, timber, and composite substrates. Thin-film variants, which represent over 62% of the intumescent coatings market, are particularly popular because they preserve the visual appearance of exposed structural steel while meeting fire-resistance requirements. Water-based and low-VOC formulations are seeing accelerated adoption due to environmental regulations and installer safety benefits. Manufacturers report consistent 20% annual growth in demand for thin films, particularly in commercial construction. These combined advantages position intumescent coatings as the most preferred and fastest-growing product category within the market.

Application Type Insights

Structural fire protection is the largest application segment, accounting for approximately 40% of total passive fire protection usage. This segment focuses on protecting load-bearing components such as columns, beams, trusses, and floors, which are critical to maintaining structural stability during fire events. Building codes worldwide mandate minimum fire-resistance ratings based on building height, occupancy type, and evacuation requirements. Intumescent coatings and cementitious sprays are widely used for their ability to conform to complex geometries and to support retrofit projects.

Demand for structural protection continues to grow as regulations become stricter and insurers require higher safety standards. Aging infrastructure is also driving retrofit demand, as safety audits increasingly identify insufficient fire protection. Greater awareness of the risks of structural failure during fires has made structural fire protection a design priority, particularly in hospitals, schools, transport hubs, and high-rise commercial buildings, where extended evacuation times are required.

End-user Insights

The building and construction sector remains the largest end-user of passive fire protection materials, driven by regulatory enforcement, insurance mandates, and expanding real estate development. Demand spans new construction, renovation projects, and retrofitting of aging buildings across residential, commercial, and infrastructure segments. Commercial buildings such as offices, malls, and hotels are major growth contributors, as developers increasingly specify certified fire protection systems to ensure compliance and enhance property value.

With the global construction industry projected to reach US$8 trillion by 2030, demand for passive fire protection is rising in proportion. Residential construction, particularly in Asia-Pacific and European renovation markets, is also adopting intumescent coatings and fire-rated boards for compartmentation. Infrastructure projects, including tunnels, airports, and utility facilities, increasingly integrate passive fire protection to meet public safety requirements. Overall, the construction industry remains the backbone of market demand, supporting sustained growth across regions.

Regional Insights

North America Passive Fire Protection Materials Market Trends

The North American market demonstrates steady growth supported by stringent regulations, extensive retrofitting activity, and advanced construction standards. The United States leads regional demand through enforcement of NFPA standards, including NFPA 285 for exterior wall assemblies and NFPA 80 for fire damper maintenance. New York’s enhanced fire-blocking requirements have set a precedent that influences broader market practices. Demand for thin-film intumescent coatings is particularly strong in commercial projects requiring both fire protection and architectural appeal.

Canada’s regulatory framework, governed by the National Building Code and provincial amendments, emphasizes structural protection and compartmentation, with growing preference for low-VOC formulations. Retrofitting older commercial buildings to meet updated fire codes and insurance requirements represents a major demand source. Strong R&D investment, established manufacturers, and sustainability commitments position North America as a premium, technology-driven market segment.

Europe Passive Fire Protection Materials Market Trends

Europe accounts for approximately 37% of global market share, driven by highly stringent safety regulations and strong sustainability focus. The EN 13501-1/2 Euroclass system provides harmonized fire performance benchmarks, while national codes introduce localized requirements. Germany and the UK lead demand through strict enforcement of building safety regulations, particularly for high-rise and commercial buildings.

The UK’s Building Safety Act 2022 and amendments to Approved Document B have created significant retrofit opportunities. France and Spain show consistent demand for high-quality fireproofing in commercial and industrial projects. The market is projected to grow from US$1.5 billion in 2024 to US$1.75 billion by 2030. Manufacturers are increasingly developing lightweight, modular-friendly fire protection systems aligned with off-site construction and sustainability goals.

Asia Pacific Passive Fire Protection Materials Market Trends

Asia-Pacific is the fastest-growing region, holding 25.8% of global market share. China dominates due to extensive construction activity and mandatory requirements for fire-resistant materials in all public buildings. The country is projected to grow at an 8.9% CAGR through 2035. India follows closely, supported by rapid urbanization, Smart Cities development, and expanding high-rise construction, achieving an estimated 8.3% CAGR.

The oil and gas sector further accelerates regional growth at 9.2% CAGR. Japan maintains a stable demand driven by strict fire regulations and seismic-resilient construction standards. Emerging economies such as Vietnam, Indonesia, and Bangladesh are experiencing increasing adoption as industrialization and safety enforcement intensify. Overall, the Asia-Pacific region represents the strongest long-term growth engine for the global market.

Competitive Landscape

The global passive fire protection materials market is moderately consolidated, with leading multinational corporations holding significant market share through integrated manufacturing, extensive distribution networks, and strong R&D capabilities. Key players, including 3M, Sherwin-Williams, Saint-Gobain, BASF, and DuPont, maintain leadership through diversified product portfolios and geographic reach.

Specialized manufacturers such as Nullifire, Promat, Etex, Hempel, and Morgan Advanced Materials compete through technical expertise and customized solutions. Competitive strategies increasingly focus on sustainability, digital compliance tracking, and strategic acquisitions. Differentiation is driven by third-party certifications, proven performance across fire scenarios, technical support services, and environmentally compliant formulations. Manufacturers aligned with sustainability and regulatory excellence are securing long-term market leadership.

Key Developments:

- In November 2024: Nullifire and Tremco CPG UK unified Carboline fire protection products, creating a stronger structural protection portfolio of intumescent coatings, cementitious mortars, and acoustic absorption systems designed to deliver comprehensive, high-performance fire protection for architectural steel and concrete applications.

- In February 2023: PPG Industries introduced the PPG STEELGUARD® 951 epoxy intumescent coating with flexible epoxy technology, offering up to three hours of cellulosic fire protection and UL 1709-certified hydrocarbon resistance in a lightweight, low-film formulation for demanding oil and gas applications.

- In October 2025: Passive fire protection uptake surged in Singapore, Australia, and Europe as LEED, IGBC, and Green Mark certification incentives and investor sustainability priorities drove manufacturers to innovate low-VOC, recyclable fireproofing solutions for premium green building segments.

Companies Covered in Passive Fire Protection Materials Market

- Lloyd

- 3M

- Sherwin-Williams Company

- Hempel

- Nullifire

- Etex SA

- Saint-Gobain

- Siniat International

- Promat International

- Sharpfibre Limited

- Rudolf Hensel GmbH

- HILTI

- Carboline

- Morgan Advanced Materials plc

- Contego International Inc

- PPG Industries

- BASF SE

- Bostik

Frequently Asked Questions

The passive fire protection materials market is valued at US$ 4.3 billion in 2026 and is projected to reach US$ 6.6 billion by 2033, growing at a 6.4% CAGR.

Growth is driven by stringent fire safety regulations, rapid Asia-Pacific urbanization, and expanding oil and gas infrastructure requiring certified high-temperature fire protection solutions.

Intumescent coatings lead the market due to superior fire resistance, aesthetic flexibility, versatile application, and strong demand for thin-film, low-VOC formulations in commercial construction.

Europe leads the market, supported by strict fire safety regulations, premium material standards, extensive building renovation activity, and strong adoption of sustainable construction practices.

Key opportunities include oil and gas expansion, rising demand for sustainable fireproofing materials, and development of advanced, smart, and bio-based fire protection technologies.

Major players include Sherwin-Williams, Saint-Gobain, PPG Industries, BASF SE, Nullifire, Promat International, Etex SA, Carboline, and Morgan Advanced Materials.