- Nutraceuticals & Functional Foods

- Parenteral Formula Market

Parenteral Formula Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Parenteral Formula Market by Nutrient (Carbohydrates, Amino Acids, Lipids, Electrolytes, Vitamins and Minerals, and Specialty Formulas), by Indications (Neurological Diseases, GI Disorders, Malnutrition, Alzheimer’s, Cancer Care, Chronic Kidney Diseases, Dysphagia, and Others) by Sale Channel (Modern Trade, Hospital Pharmacies, Retail Pharmacies, Drug Stores, and Online Pharmacies), and Regional Analysis from 2026 to 2033

Parenteral Formula Market Share and Trend Analysis

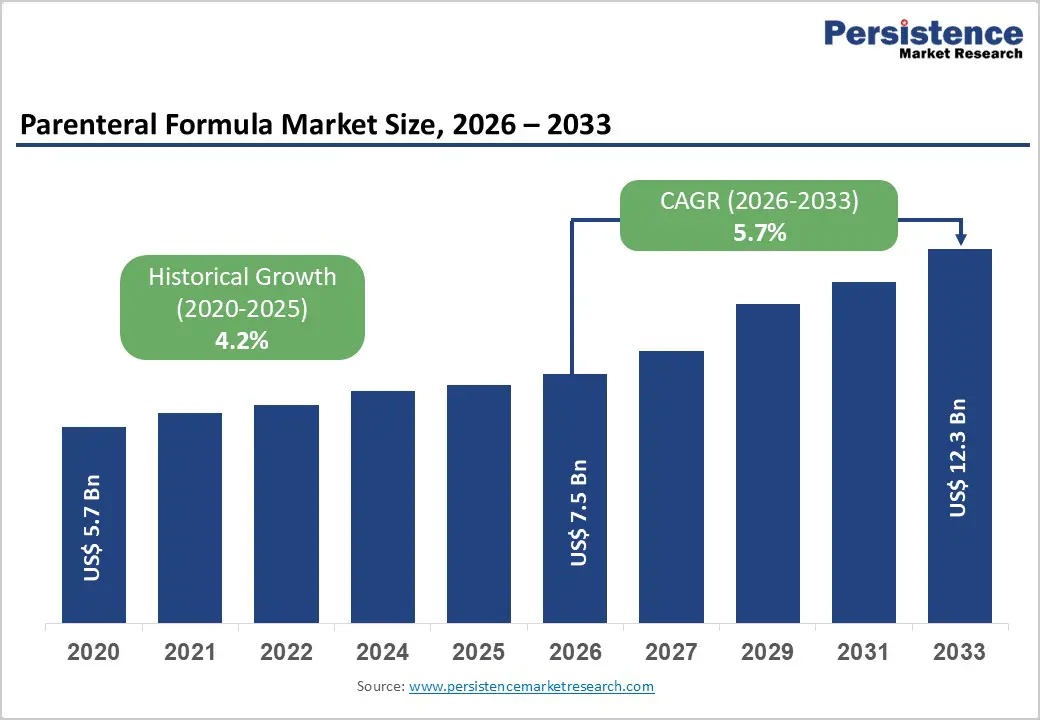

The global parenteral formula market size is estimated to grow from US$ 7.5 billion in 2026 to US$ 12.3 billion by 2033, growing at a CAGR of 5.7% from 2026 to 2033. Global demand for parenteral formulas is rising steadily, driven by the increasing prevalence of chronic and acute medical conditions, the growing incidence of hospital-acquired malnutrition, and the expanding emphasis on early clinical nutrition intervention. Healthcare providers are increasingly integrating parenteral nutrition into standard treatment protocols for patients unable to meet nutritional needs through oral or enteral routes, particularly in oncology, critical care, gastrointestinal disorders, and post-surgical recovery.

Rising ICU admissions, longer hospital stays, and aging populations are reinforcing sustained demand. Expanded use of parenteral formulas across hospitals, specialty clinics, and home-care settings is supporting consistent market growth. Improved diagnostic practices for malnutrition, higher clinician awareness of nutrition’s role in patient outcomes, and preference for precise, controlled nutrient delivery are further accelerating adoption. In addition, rising healthcare expenditure and improved access to advanced hospital infrastructure are enabling wider uptake across both developed and emerging markets.

Continuous innovation in formulation stability, multi-chamber packaging, lipid emulsions, and amino acid optimization is enhancing safety, flexibility, and therapeutic outcomes. The growing focus on outcome-based care, personalized nutrition, and home parenteral nutrition programs is further propelling global demand.

Key Industry Highlights

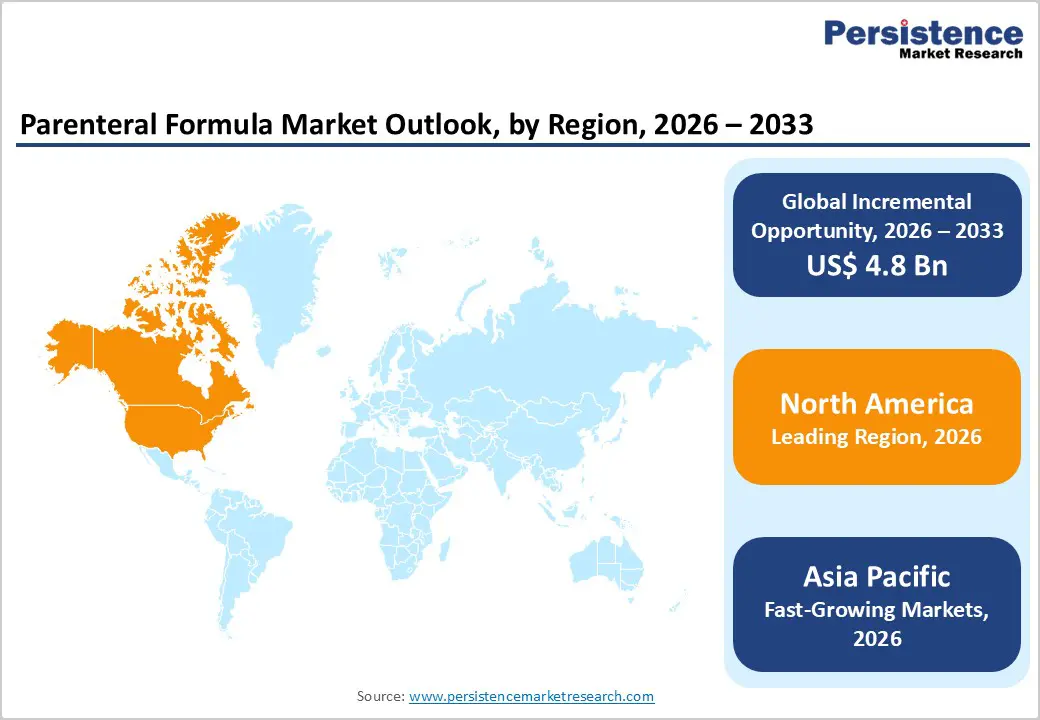

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, high chronic disease burden, strong adoption of clinical nutrition protocols, favorable reimbursement environments, and the presence of major parenteral nutrition manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid healthcare infrastructure development, rising hospital admissions, increasing chronic disease prevalence, and improving access to advanced clinical nutrition services.

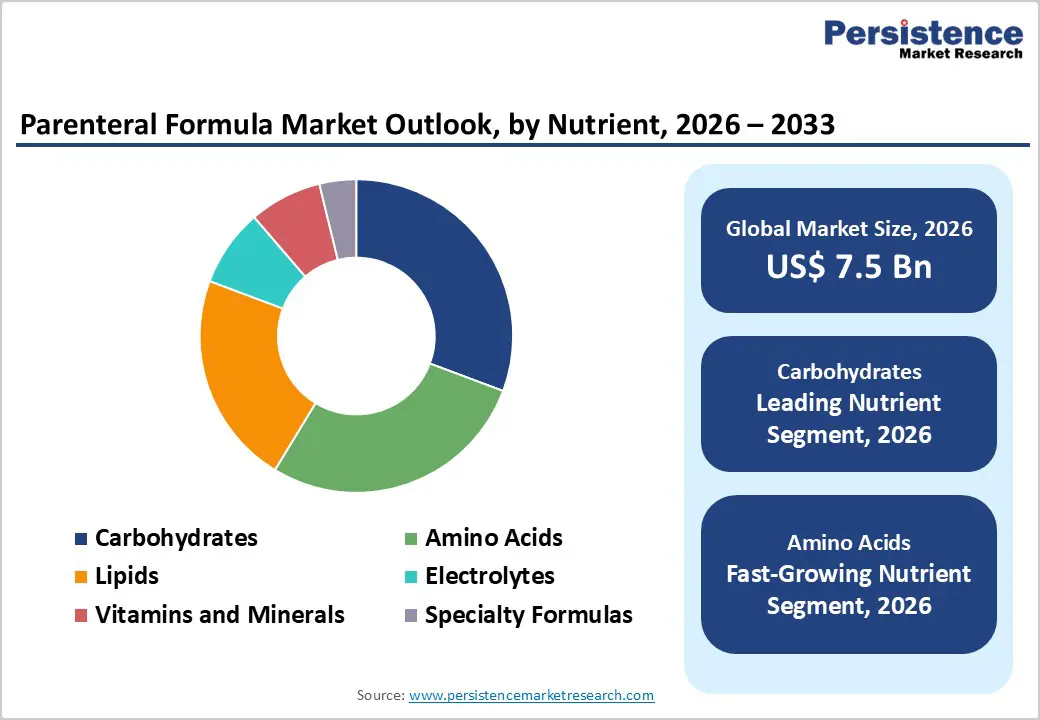

- Leading Nutrient Segment: Carbohydrates dominate the market due to reliable energy delivery, metabolic efficiency, precise dosing control, and broad compatibility across parenteral nutrition regimens.

- Fastest-Growing Nutrient Segment: Amino acids are expanding rapidly as demand increases for protein preservation, muscle maintenance, and tailored formulations for oncology, renal, and critically ill patients.

- Leading Indication Segment: Cancer care remains the top application, driven by high rates of cancer-related malnutrition, gastrointestinal complications, and prolonged reliance on parenteral nutrition during treatment.

- Fastest-Growing Indication Segment: Malnutrition management is scaling quickly due to heightened awareness of early nutritional intervention, aging populations, and increasing use of nutrition therapy to improve recovery and reduce complications.

| Key Insights | Details |

|---|---|

| Parenteral Formula Market Size (2026E) | US$ 7.5 Bn |

| Market Value Forecast (2033F) | US$ 12.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7 % |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2 % |

Market Dynamics

Driver - Rising Burden of Chronic Illnesses and Increasing Dependence on Clinical Nutrition Support

Escalating prevalence of chronic and acute medical conditions is a primary force accelerating demand for parenteral formulas worldwide. Diseases such as cancer, gastrointestinal disorders, chronic kidney disease, neurological impairments, and severe infections often limit a patient’s ability to meet nutritional requirements through oral or enteral routes. In such cases, parenteral nutrition becomes a critical component of clinical management. Growth in the global geriatric population further amplifies demand, as older adults are more susceptible to malnutrition, impaired absorption, and prolonged hospital stays. Increasing ICU admissions, complex surgical procedures, and trauma cases also contribute to sustained utilization of parenteral formulas.

Healthcare providers are placing greater emphasis on early nutritional intervention to reduce complications, shorten recovery time, and improve treatment outcomes. Advances in formulation science, including improved lipid emulsions, balanced amino acid profiles, and multi-chamber delivery systems, are making parenteral nutrition safer and more adaptable across patient groups. In parallel, stronger clinical guidelines and hospital protocols around nutrition therapy are reinforcing routine use. As hospitals continue to prioritize outcome-based care, parenteral formulas are increasingly viewed as an essential therapeutic support rather than an adjunct intervention.

Restraints - High Treatment Costs, Compounding Complexity, and Risk of Clinical Complications

Despite strong clinical relevance, several factors continue to restrain broader expansion. Parenteral nutrition therapy is inherently cost-intensive, requiring sterile manufacturing, controlled storage, and specialized administration infrastructure. These costs can strain hospital budgets, particularly in low- and middle-income regions where healthcare spending is constrained. Clinical risks associated with parenteral nutrition, including catheter-related infections, metabolic imbalances, and liver complications, further limit indiscriminate use and necessitate close monitoring. Preparation and compounding processes demand skilled pharmacy personnel and adherence to stringent safety standards, creating operational challenges for smaller healthcare facilities. Inconsistent access to trained clinical nutrition teams can also lead to underutilization or inappropriate administration.

Additionally, reimbursement limitations and variability in insurance coverage restrict adoption in certain markets. Regulatory compliance requirements, while essential for safety, increase development timelines and manufacturing costs for suppliers. Supply chain disruptions and raw material price volatility further impact product availability and pricing stability. These combined factors create barriers to wider penetration, especially outside advanced hospital settings, and can slow adoption despite rising clinical need.

Opportunity - Personalized Nutrition, Home Parenteral Care, and Emerging Healthcare Markets

Evolving healthcare delivery models are opening new avenues for growth and differentiation. Increasing focus on personalized medicine is driving demand for customized parenteral formulas tailored to individual metabolic needs, disease states, and organ function. Advances in digital health and clinical decision-support tools are enabling more precise nutritional planning and monitoring. Expansion of home parenteral nutrition programs represents a significant opportunity, particularly for stable chronic patients requiring long-term support, as it reduces hospital burden and improves quality of life. Emerging markets present strong growth potential due to rapid healthcare infrastructure development, rising chronic disease incidence, and expanding access to tertiary care facilities.

Governments and private providers are investing in hospital capacity, ICU expansion, and oncology services, all of which support parenteral nutrition adoption. Innovation in packaging, extended shelf-life formulations, and safer infusion technologies is improving ease of use and reducing complication risks. Strategic partnerships between manufacturers, hospitals, and homecare providers further enhance market reach. As nutrition therapy becomes increasingly integrated into comprehensive disease management, parenteral formulas are positioned to benefit from both volume expansion and higher-value, specialized solutions.

Category-wise Analysis

By Nutrient, Carbohydrates Lead Due to Immediate Energy Provision, Metabolic Efficiency, and Clinical Compatibility

The carbohydrates segment is projected to dominate the global parenteral formula market in 2026, capturing a revenue share of 30.7%. This leadership is primarily driven by carbohydrates being the most reliable and rapidly metabolized energy source in parenteral nutrition therapy, particularly for critically ill, post-surgical, and metabolically stressed patients. Glucose-based formulations are widely used due to their predictable metabolic response, precise dosing control, and compatibility with most parenteral regimens. Clinicians prefer carbohydrate solutions for maintaining caloric balance, preventing protein catabolism, and supporting organ function during acute care. Compared to complex lipid or amino acid regimens, carbohydrate formulations allow easier titration and monitoring, reducing metabolic complications. Their stability, ease of integration into multi-chamber bags, and suitability across adult, pediatric, and neonatal populations further support widespread adoption. Continuous improvements in formulation purity, osmolarity control, and infusion safety, combined with rising hospital admissions and ICU utilization, continue to reinforce the dominance of carbohydrate-based parenteral formulas globally.

By Indication, Cancer Care Leads Due to High Malnutrition Risk and Intensive Nutritional Support Requirements

The cancer care segment is expected to lead the global parenteral formula market in 2026, accounting for a 17.6% revenue share. This dominance is driven by the high prevalence of cancer-associated malnutrition, cachexia, and gastrointestinal complications that limit oral or enteral feeding. Oncology patients frequently require parenteral nutrition during chemotherapy, radiation therapy, surgical recovery, and advanced disease stages to maintain energy balance and treatment tolerance. Parenteral formulas play a critical role in improving clinical outcomes by supporting immune function, preserving lean body mass, and reducing infection risks. Increasing cancer incidence globally, longer treatment durations, and improved survival rates have expanded the eligible patient pool for long-term nutritional support. Hospitals and oncology centers increasingly adopt individualized parenteral regimens tailored to metabolic demands and organ function. Growing clinical awareness of early nutritional intervention in cancer care, along with standardized oncology nutrition protocols, continues to sustain this segment’s leadership.

By Sale Channel, Hospital Pharmacies Lead Due to Centralized Administration, Clinical Control, and Safety Compliance

Hospital pharmacies are projected to dominate the global parenteral formula market in 2026, capturing a 48.1% revenue share. This leadership is driven by the clinical nature of parenteral nutrition, which requires sterile preparation, precise compounding, and close medical supervision. Hospital pharmacies serve as the primary point of dispensing and preparation for parenteral formulas used in ICUs, oncology wards, neonatal units, and surgical departments. Centralized pharmacy compounding ensures dosing accuracy, minimizes contamination risks, and complies with stringent regulatory and safety standards. Hospitals also benefit from long-term supply contracts with manufacturers, ensuring consistent availability of standardized and customized formulations. Increasing hospital admissions, growth in critical care capacity, and rising prevalence of chronic and acute conditions further strengthen this channel’s dominance. Additionally, the expansion of hospital-based home parenteral nutrition programs continues to route procurement through institutional pharmacy systems, reinforcing their leading market position.

Regional Insights

North America Parenteral Formula Market Trends

North America is expected to dominate the global Parenteral Formula Market in 2026, accounting for a 46.7% value share, largely driven by the United States. The region benefits from a high prevalence of chronic diseases such as cancer, gastrointestinal disorders, renal failure, and neurological conditions, all of which increase reliance on parenteral nutrition. Advanced healthcare infrastructure, widespread ICU availability, and strong adoption of evidence-based clinical nutrition protocols support consistent demand. Hospitals in North America routinely integrate parenteral formulas into oncology care, surgical recovery, and long-term critical care pathways.

The presence of leading manufacturers and well-established supply chains ensures access to advanced formulations, including multi-chamber bags and lipid emulsions. Favorable reimbursement frameworks and strong clinical guidelines further encourage usage. Regulatory oversight by the U.S. FDA ensures high product quality and safety standards. Additionally, growing adoption of home parenteral nutrition for stable chronic patients supports sustained market leadership across the region.

Europe Parenteral Formula Market Trends

Europe’s parenteral formula market is expected to grow steadily in 2026, supported by aging demographics, rising chronic disease burden, and strong emphasis on clinical nutrition management. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate consistent demand due to well-developed public healthcare systems and high hospital utilization rates. European clinicians place strong focus on preventing hospital-associated malnutrition, driving routine use of parenteral formulas in surgical, oncology, and intensive care settings. Stringent regulatory frameworks emphasize formulation safety, traceability, and ingredient quality, supporting adoption of standardized, high-purity products.

The region also benefits from growing awareness of early nutritional intervention to reduce hospital stays and complications. Hospital pharmacies and centralized compounding units dominate distribution, while home parenteral nutrition programs are gradually expanding. Sustainability initiatives and optimized packaging solutions further influence procurement decisions, contributing to stable long-term growth across Europe.

Asia Pacific Parenteral Formula Market Trends

The Asia Pacific parenteral formula market is projected to register a higher CAGR of around 7.7% between 2026 and 2033, driven by rapid healthcare infrastructure expansion, rising chronic disease prevalence, and improving access to advanced clinical nutrition. Countries such as China, India, Japan, and South Korea are witnessing increased hospital admissions due to cancer, renal disorders, and gastrointestinal diseases. Growing investments in tertiary care hospitals, ICUs, and oncology centers are significantly expanding the addressable market. Awareness of clinical nutrition is improving among healthcare professionals, particularly in urban hospitals.

Governments across the region are strengthening domestic pharmaceutical manufacturing and encouraging local production of parenteral nutrition products, improving affordability and supply stability. Global manufacturers are entering through partnerships, technology transfers, and regional production facilities. Expansion of home healthcare services and gradual adoption of home parenteral nutrition further support demand. These factors position Asia Pacific as the fastest-growing regional market globally.

Competitive Landscape

The global parenteral formula market is highly competitive, with strong participation from Baxter, B. Braun SE, Fresenius Kabi AG, Pfizer Inc., Sichuan Kelun-Biotech Biopharmaceutical Co., Ltd., and Otsuka Pharmaceutical Co., Ltd. These players leverage extensive global manufacturing and distribution networks, strong hospital relationships, and continuous innovation in formulation stability, multi-chamber bag systems, lipid emulsions, amino acid profiles, micronutrient optimization, and sterility assurance to address diverse clinical nutrition requirements across critical care, oncology, renal, and surgical settings.

Rising prevalence of chronic diseases, increasing hospitalizations, growth in the geriatric population, and higher incidence of malnutrition and gastrointestinal disorders are driving innovation in the market. Manufacturers are focusing on ready-to-use formulations, personalized and indication-specific parenteral nutrition solutions, improved safety and compatibility, and ease of administration, while strengthening hospital partnerships, expanding presence in emerging markets, and sustaining R&D investments to deliver clinically effective, safe, and high-compliance parenteral formulas.

Key Industry Developments:

- In June 2025, Elgan Pharma Ltd. and Chiesi Farmaceutici S.p.A. announced the dosing of the first infants in FIT-PIV, a Phase 3 clinical trial evaluating the safety and efficacy of ELGN-2112, an investigational therapy being developed to treat intestinal malabsorption in preterm infants a common condition linked to severe and potentially life-threatening complications.

- In November 2024, Otsuka Pharmaceutical Factory launched “KIDPAREN Injection,” a high-calorie parenteral nutrition formulation combining amino acids, glucose, electrolytes, lipids, and multivitamins, specifically designed to support the nutritional needs of patients with chronic kidney disease.

- In November 2022, WuXi STA, a subsidiary of WuXi AppTec, commenced operations at a new parenteral formulation manufacturing line at its drug product facility in Wuxi, China. This marked the company’s second parenteral line launched that year for both clinical and commercial injectable production, with an annual capacity of 10 million units, underscoring WuXi STA’s ongoing commitment to expanding and strengthening its injectable drug product manufacturing platform.

Companies Covered in Parenteral Formula Market

- Baxter

- B. Braun SE

- Fresenius Kabi AG

- Pfizer Inc.

- Sichuan Kelun-Biotech Biopharmaceutical Co., Ltd.

- Otsuka Pharmaceutical Co., Ltd.

- Grifols, S.A.

- Aculife Healthcare Private Limited

- CSL

- Terumo Corporation

- Nutricia

- ICU Medical, Inc.

- Others

Frequently Asked Questions

The global parenteral formula market is projected to be valued at US$ 7.5 Bn in 2026.

Rising prevalence of chronic diseases, cancer-related malnutrition, and an aging population is increasing dependence on parenteral nutrition when oral or enteral feeding is not viable.

The global parenteral formula market is poised to witness a CAGR of 5.7%between 2026 and 2033.

Expansion of home-based parenteral nutrition and demand for personalized, ready-to-use formulations present strong growth potential globally.

Baxter, B. Braun SE, Fresenius Kabi AG, Pfizer Inc., Sichuan Kelun-Biotech Biopharmaceutical Co., Ltd., and Otsuka Pharmaceutical Co., Ltd. are some key players in the parenteral formula market.