- Nutraceuticals & Functional Foods

- Pancreatin Market

Pancreatin Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Pancreatin Market by Form (Tablets, Capsules, Powder), by Source (Porcine, Bovine), by Application, by Distribution Channel, and Regional Analysis from 2026 - 2033

Pancreatin Market Share and Trends Analysis

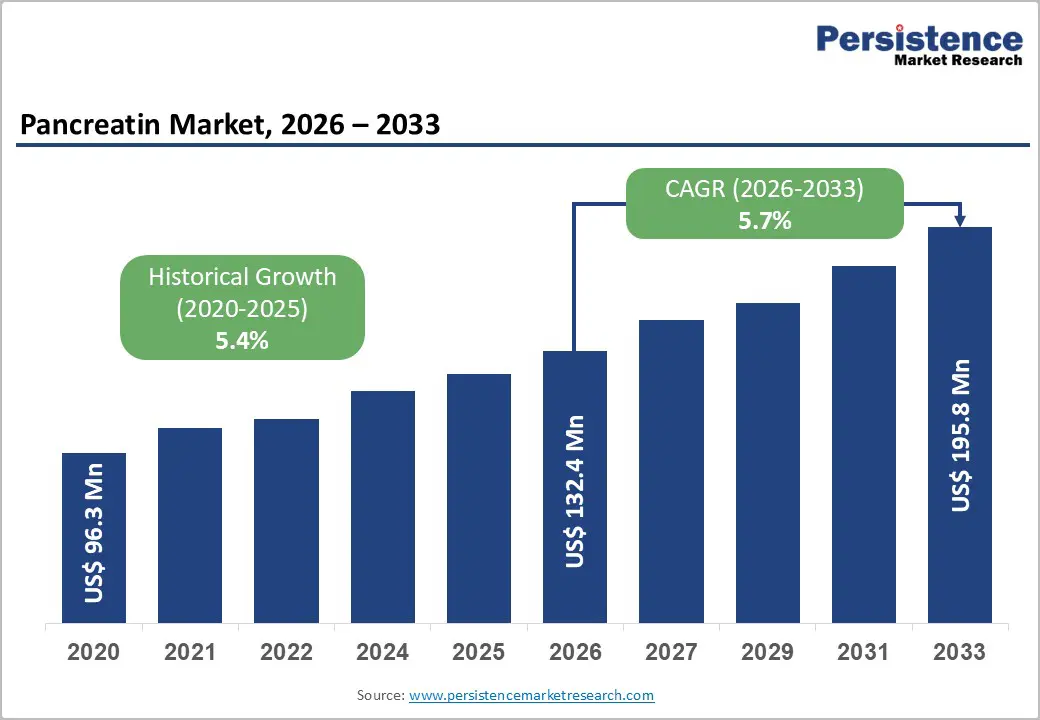

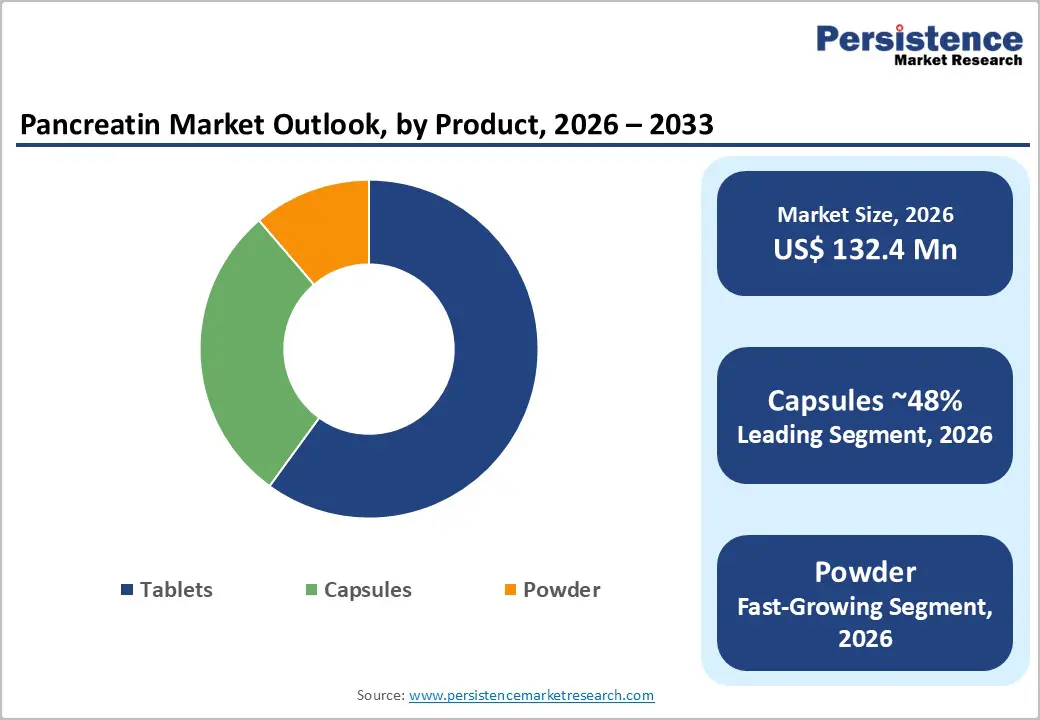

The global pancreatin market size is likely to be valued at US$132.4 million in 2026 and US$195.8 million by 2033. The market is projected to grow at a CAGR of 5.7% from 2026 to 2033. The market focuses on enzyme-based therapies used to support digestion in patients with pancreatic enzyme deficiency. Pancreatin formulations combine lipase, amylase, and protease to aid fat, carbohydrate, and protein absorption.

Market demand is primarily driven by the rising incidence of exocrine pancreatic insufficiency, chronic pancreatitis, cystic fibrosis, and post-surgical digestive complications. Growth is supported by increasing diagnosis rates, improved awareness of digestive health, and wider availability of prescription and OTC enzyme supplements. Technological advancements in enteric coating and dosage standardization enhance treatment efficacy, while expanding access in emerging economies continues to strengthen overall market adoption.

Key Industry Highlights

- The growing prevalence of exocrine pancreatic insufficiency, chronic pancreatitis, and cystic fibrosis is significantly increasing long-term demand for pancreatin-based enzyme replacement therapies worldwide.

- Pancreatin remains largely prescription-driven due to dosage sensitivity, disease severity, and the need for physician supervision, supporting steady demand through hospital and specialty pharmacy channels.

- Capsule formulations dominate the market owing to better enzyme protection, controlled release, higher patient compliance, and improved therapeutic outcomes compared to conventional tablet formulations.

- Hospital pharmacies account for the largest share as pancreatin is commonly initiated during inpatient care following pancreatic surgery or a severe digestive insufficiency diagnosis.

| Key Insights | Details |

|---|---|

|

Pancreatin Market Size (2026E) |

US$132.4 Mn |

|

Market Value Forecast (2033F) |

US$195.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Dynamics

Driver - Improved Enteric-Coated Formulations

Improved enteric-coated formulations have emerged as a critical growth driver in the pancreatin market by directly addressing one of the therapy’s long-standing clinical challenges—enzyme degradation in the highly acidic gastric environment. Traditional pancreatin products often suffered from reduced activity before reaching the small intestine, limiting therapeutic effectiveness and creating variability in patient outcomes. Modern enteric-coating technologies now enable enzymes to remain protected in the stomach and release precisely in the duodenum, where digestion occurs, significantly improving bioavailability and consistency of action. These technological advancements have translated into more predictable fat absorption, better symptom control, and reduced gastrointestinal side effects such as bloating and steatorrhea. For physicians, improved reliability has increased confidence in prescribing pancreatin as a frontline therapy rather than a last-resort intervention. Enhanced formulations also support more accurate dose titration based on lipase units, allowing clinicians to tailor treatment to disease severity, dietary patterns, and patient response.

From a patient perspective, enteric-coated microspheres and mini-tablets improve ease of administration, compliance, and quality of life, especially for pediatric and geriatric populations requiring long-term therapy. For manufacturers, formulation innovation enables product differentiation, premium pricing, and stronger brand loyalty in an otherwise mature enzyme market. Additionally, regulatory agencies increasingly favor standardized, acid-resistant formulations due to their superior safety and efficacy profiles. Collectively, these improvements are reshaping treatment expectations, expanding prescribing volumes, and reinforcing pancreatin’s role as an essential therapy in managing pancreatic enzyme insufficiency.

Restraints - Lack of Plant-Based Alternatives

The lack of plant-based or synthetic alternatives remains a critical structural restraint for the pancreatin market. Pancreatin is a complex blend of lipase, amylase, and protease enzymes that must closely replicate human pancreatic secretions to ensure effective digestion and nutrient absorption. Currently, animal-derived sources primarily porcine pancreas are the only clinically proven option capable of delivering the required enzyme composition, activity levels, and stability. Plant-based or microbial enzymes, while available as dietary supplements, fail to match the potency, acid resistance, and therapeutic reliability needed for treating serious conditions such as exocrine pancreatic insufficiency, cystic fibrosis, and post-pancreatectomy malabsorption.

This absence of clinically equivalent alternatives restricts innovation across the market. Manufacturers remain heavily dependent on traditional extraction and purification processes rather than advancing toward next-generation synthetic or recombinant solutions. As a result, product differentiation is largely limited to dosage strengths, delivery formats, and coating technologies, rather than true therapeutic breakthroughs. Long-term reliance on animal-derived enzymes also exposes the market to supply chain vulnerabilities, ethical concerns, and cultural or religious resistance in certain patient populations.

Furthermore, regulatory approval for novel non-animal enzymes is complex and time-consuming, as demonstrating bioequivalence to pancreatin requires extensive clinical validation. This creates high entry barriers for innovation-driven biotech companies and discourages R&D investment in alternative enzyme platforms. Until a plant-based or synthetic substitute can demonstrate equivalent clinical efficacy and safety, the pancreatin market will continue to face limited innovation pathways and sustained dependence on animal-origin enzyme sources.

Opportunity - Fixed-Dose Combination Therapies

Fixed-dose combination therapies represent a high-value innovation opportunity within the pancreatin market by addressing multiple digestive challenges through a single, integrated formulation. While pancreatin effectively replaces missing pancreatic enzymes, many patients continue to experience incomplete digestion due to impaired bile secretion, altered gut microbiota, or gastric acid–mediated enzyme degradation. Combining pancreatin with bile salts can significantly improve fat emulsification and absorption, particularly in post-cholecystectomy patients or those with hepatic or biliary dysfunction. The addition of probiotics helps restore gut microbial balance, supports intestinal health, and may reduce common gastrointestinal side effects such as bloating, diarrhea, and abdominal discomfort associated with enzyme therapy. Incorporating acid suppressants or buffering agents further enhances enzyme stability by protecting pancreatin from gastric acid destruction, ensuring optimal activity in the small intestine.

From a commercial perspective, fixed-dose combinations offer strong product differentiation, improved patient convenience, and higher treatment adherence by reducing pill burden. These formulations also create opportunities for premium pricing and brand loyalty, especially in chronic conditions such as exocrine pancreatic insufficiency and chronic pancreatitis. Moreover, combination therapies can expand pancreatin use beyond severe indications into moderate and functional digestive disorders. As regulatory pathways for combination products become clearer and clinical evidence strengthens, fixed-dose pancreatin combinations are positioned to become an important growth driver in both prescription and select OTC digestive care markets.

Category-wise Analysis

By Form Insights

Capsules account for the highest share in the pancreatin market due to their superior therapeutic performance, patient convenience, and clinical preference. Pancreatin enzymes are highly sensitive to gastric acid, and capsule formulations, particularly enteric-coated capsules, provide effective protection by preventing premature enzyme degradation in the stomach. This allows the enzymes to be released in the small intestine, where digestion and nutrient absorption occur, resulting in improved clinical outcomes compared to tablets and powders. Capsules also enable precise and consistent dosing, which is critical in managing chronic conditions such as exocrine pancreatic insufficiency, cystic fibrosis, and chronic pancreatitis.

From a patient perspective, capsules are easier to swallow, cause less gastrointestinal irritation, and offer better treatment adherence, especially during long-term therapy. Clinicians favor capsule formulations because they align with established treatment guidelines and allow flexible dose titration based on meal size and fat content. Additionally, pharmaceutical advancements such as micro-pellet and delayed-release capsule technologies have further enhanced enzyme stability and absorption efficiency. These combined advantages—higher efficacy, better compliance, and strong physician acceptance—have positioned capsules as the dominant dosage form in the global pancreatin market.

By Distribution Channel Insights

Hospital pharmacies hold the highest share in the pancreatin market due to their central role in initiating, monitoring, and managing enzyme replacement therapy. Pancreatin is primarily prescribed for serious conditions such as exocrine pancreatic insufficiency, chronic pancreatitis, cystic fibrosis, and post-pancreatectomy malabsorption, which often require clinical diagnosis, physician supervision, and careful dose titration. Hospitals serve as the first point of contact for these patients, ensuring that pancreatin therapy is correctly prescribed and tailored to individual needs, including enzyme strength, meal timing, and dietary fat content.

Additionally, hospital pharmacies offer direct access to a broad range of formulation strengths and enteric-coated capsules, which are critical for treatment efficacy. They also facilitate patient education on proper administration, adherence, and monitoring for potential side effects. In many emerging markets, hospital pharmacies are more reliable and trusted than retail or online channels, particularly for chronic and specialized treatments, which enhances their market share. Furthermore, repeat prescriptions are often managed through hospital outpatient departments, reinforcing consistent demand. Collectively, the combination of clinical supervision, product availability, patient support, and trust positions hospital pharmacies as the dominant distribution channel for pancreatin globally.

Region-wise Insights

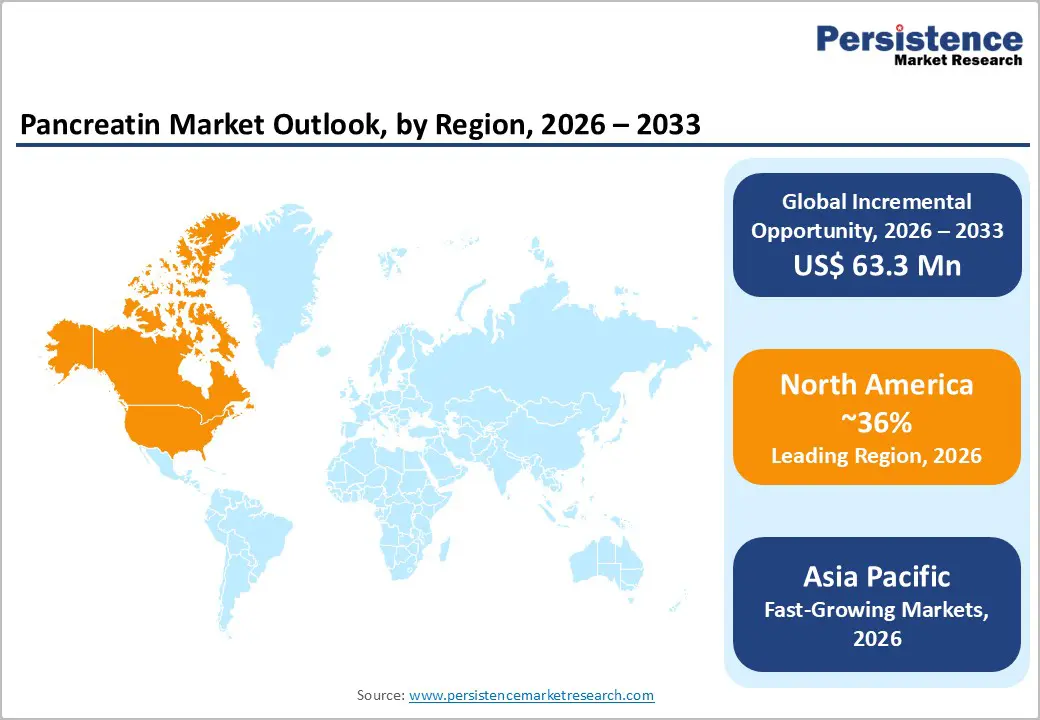

North America Pancreatin Market Trends

North America leads the global pancreatin market, driven by high awareness of digestive health, well-established healthcare infrastructure, and a growing prevalence of exocrine pancreatic insufficiency, chronic pancreatitis, and cystic fibrosis. The region benefits from advanced diagnostic capabilities, which enable early detection and prompt initiation of enzyme replacement therapy. Physicians in the U.S. and Canada increasingly prefer enteric-coated capsules, supporting higher efficacy and patient compliance.

In the U.S., the market is further strengthened by robust insurance coverage, prescription support programs, and strong clinical adoption in hospital and specialty pharmacy settings. The rising geriatric population and increasing survival rates for pancreatic cancer patients are expanding long-term pancreatin usage. Additionally, ongoing research, regulatory approvals for improved formulations, and patient education initiatives are enhancing market penetration. Premium pricing strategies and consistent demand from chronic therapy patients reinforce North America’s leadership position, making it the largest and most mature market globally for pancreatin products.

Asia Pacific Pancreatin Market Trends

Asia Pacific is emerging as the fastest-growing market for pancreatin, driven by rising healthcare awareness, improving diagnostic infrastructure, and increasing prevalence of digestive disorders. Rapid urbanization, changing dietary patterns, and a growing middle-class population are contributing to higher incidences of exocrine pancreatic insufficiency, chronic pancreatitis, and post-surgical digestive complications, fueling demand for enzyme replacement therapy.

Countries such as China, India, Japan, and South Korea are witnessing expanding hospital networks, specialty clinics, and retail pharmacy availability, which improves patient access to pancreatin products. Rising adoption of enteric-coated capsules and patient education initiatives further support market growth. Additionally, local manufacturing capabilities and regulatory support for pharmaceutical imports are reducing costs and increasing affordability in emerging economies. Telemedicine and online pharmacy platforms are also enhancing distribution reach, particularly in rural areas. Collectively, these factors position the Asia Pacific as a high-potential growth market, with significant opportunities for new product launches, fixed-dose combinations, and long-term therapy adoption.

Competitive Landscape

The pancreatin market is highly competitive, characterized by numerous global and regional players focusing on product innovation, formulation improvements, and geographic expansion. Companies compete on factors such as enzyme potency, enteric coating technology, dosage convenience, and patient compliance. Market players are increasingly investing in research and development to introduce advanced delivery systems, fixed-dose combinations, and pediatric-friendly formulations. Strategic partnerships, collaborations with hospitals, and expansion into emerging markets strengthen market presence.

Key Industry Developments:

- In August 2025, Enzybel Pharma 2, part of European distributor Natix, allied with Chinese enzyme manufacturer Deebio to help address the global shortage of high-activity pancrelipase (pancreatin). The partnership focused on producing a highly purified, standardized form of the active pharmaceutical ingredient (API), used in the treatment of pancreatic insufficiency.

Companies Covered in Pancreatin Market

- Antozyme Biotech Pvt Ltd

- Umang Pharmaceuticals

- Enzyme Bioscience Pvt. Ltd

- Biovencer Healthcare Private Limited

- Nordmark

- Fengchen Group Co., Ltd.

- Biozyme

- Sichuan Biosyn Pharmaceutical Co., Ltd.

- Bioseutica

- Wellona Pharma

- Shreeji Pharma International

- Hetero Healthcare Limited

- Creative Enzymes

- Baoding Faithful Industry Co. Ltd.

- SG Pharma Pvt. Ltd.

- Provita Nutrition and Health Inc.

- Hepalink Group

- NOW® Foods

- Bio Basic Inc.

- Sichuan Deebio Pharmaceutical Co., Ltd.

- Others

Frequently Asked Questions

The global pancreatin market is projected to be valued at US$132.4 Mn in 2026.

The increasing prevalence of exocrine pancreatic insufficiency, chronic pancreatitis, cystic fibrosis, and post-surgical malabsorption is boosting demand for enzyme replacement therapy.

The global market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Developing child-friendly, easy-to-swallow capsules or powders for cystic fibrosis and congenital pancreatic disorders.

Antozyme Biotech Pvt Ltd, Umang Pharmaceuticals, Enzyme Bioscience Pvt. Ltd, Biovencer Healthcare Private Limited, and others.