- Medical Devices

- Pacemakers Market

Pacemakers Market Size, Share, and Growth Forecast, 2026 - 2033

Pacemakers Market By Product Type (External Pacemakers, Implantable Pacemakers), Application (Bradycardia, Acute Myocardial Infarction, Others), End-user (Hospitals, Outpatient Facilities), and Regional Analysis for 2026 - 2033

Pacemakers Market Size and Trends Analysis

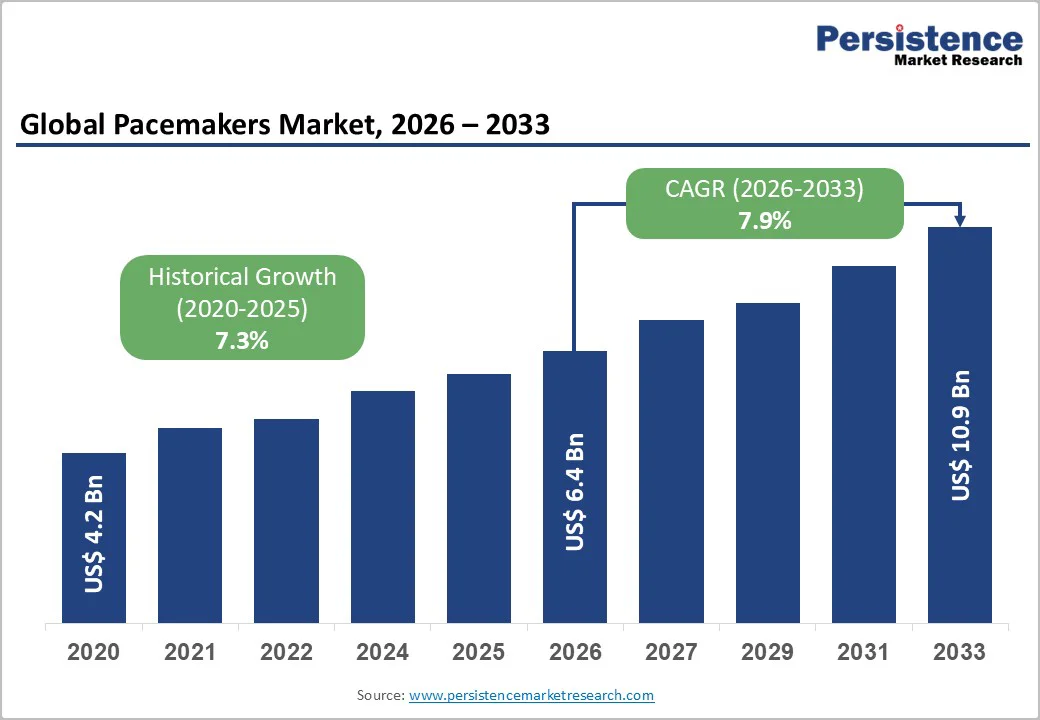

The global pacemakers market size is likely to be valued US$6.4 billion in 2026, and is expected to US$10.9 billion by 2033, growing at a CAGR of 7.9% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cardiovascular diseases, rising adoption of implantable devices for arrhythmias, and advancements in leadless technologies.

The rising need for rhythm management in bradycardia and heart failure is driving strong pacemaker adoption across diverse patient groups. Innovations in external and implantable devices, especially minimally invasive and wireless options, are further accelerating growth. Increasing recognition of pacemakers as vital for improving survival rates, particularly in hospital settings, continues to propel market demand.

Key Industry Highlights:

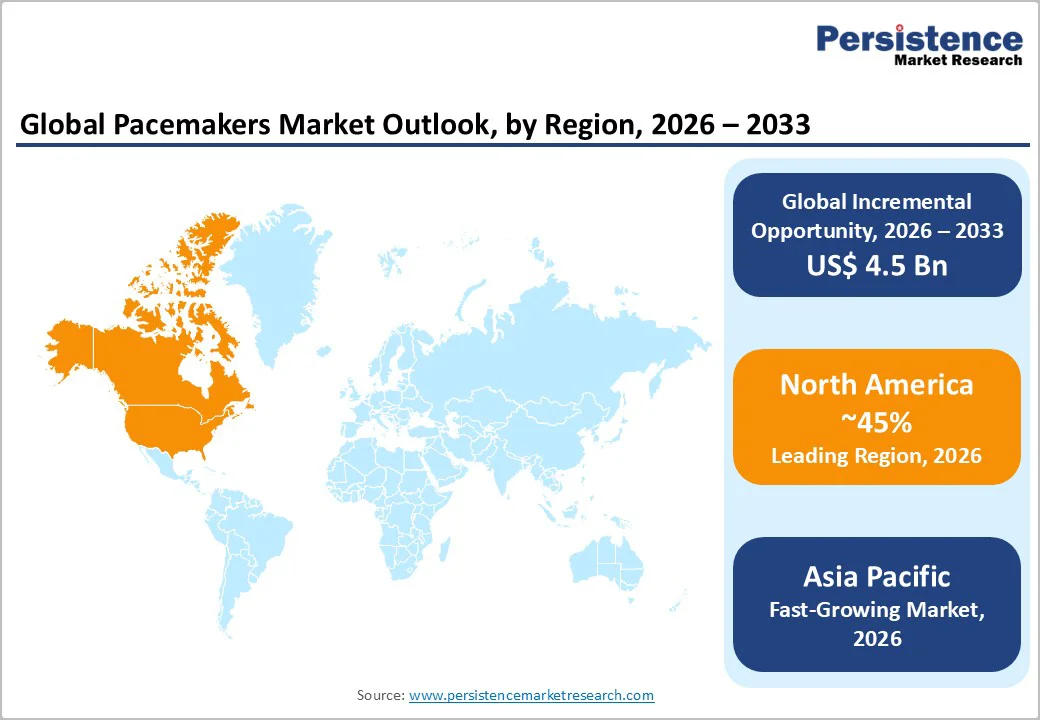

- Leading Region: North America is anticipated to command a 45% market share in 2026, driven by advanced cardiology infrastructure, high prevalence of heart conditions, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific is anticipated to be the fastest-growing region, fueled by an increasing aging population, rising awareness of cardiac care, and growing investments in healthcare in China and India.

- Dominant Product Type: Implantable pacemakers are anticipated to lead, holding 70% of the market share, due to long-term efficacy.

- Leading Application: Bradycardia is expected to account for 40% of the market revenue, driven by conduction disorders.

- Leading End-user: Hospitals are projected to contribute nearly 60% of the market revenue, due to surgical expertise.

- Key Market Driver: Rising incidence of arrhythmias and demand for wireless, leadless pacemakers is accelerating the adoption in cardiac rhythm management.

- Market Opportunity: Expansion in emerging markets and AI-integrated devices creates strong opportunities for next-generation pacemakers.

| Key Insights | Details |

|---|---|

|

Pacemakers Market Size (2026E) |

US$6.4 Bn |

|

Market Value Forecast (2033F) |

US$10.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Cardiovascular Diseases and Demand For Rhythm Management Devices

The rising prevalence of cardiovascular diseases (CVDs) is a major driver of demand for rhythm management devices, including pacemakers, across global healthcare systems. Increasing cases of bradycardia, atrial fibrillation, heart block, and age-related conduction disorders are significantly expanding the need for long-term cardiac rhythm support. Factors such as sedentary lifestyles, obesity, hypertension, diabetes, and aging populations further contribute to higher rates of CVDs worldwide. As diagnosis rates improve and more patients gain access to cardiac screening, detection of rhythm abnormalities is becoming more frequent, creating consistent demand for pacing solutions.

Pacemakers play a critical role in managing irregular heart rhythms, stabilizing heart rates, and preventing life-threatening complications. With growing patient awareness and advancements in cardiac care, rhythm management devices are being adopted earlier in treatment pathways. The shift toward minimally invasive procedures and physicians' preference for more reliable, durable devices is accelerating clinical uptake. Emerging markets, where cardiovascular disease prevalence is rising sharply, offer substantial room for adoption as healthcare infrastructure strengthens.

High Development and Implantation Costs

High development and implantation costs remain a significant restraint in the pacemakers market, limiting wider adoption, especially in low- and middle-income regions. Developing advanced pacemaker technologies such as leadless, MRI-compatible, or AI-integrated devices requires substantial investments in research, clinical trials, regulatory approvals, and precision manufacturing. These expenses are ultimately reflected in the final device price, making pacemakers one of the costlier cardiac implants. The implantation procedure itself involves specialized cardiologists, high-end surgical equipment, and post-operative monitoring, further increasing overall treatment costs. Hospitals must invest in trained staff and advanced infrastructure, adding to the financial burden.

For patients, the total cost of a pacemaker implantation, covering the device, surgery, testing, and follow-up care, can be prohibitive without comprehensive insurance or reimbursement support. In many developing countries, limited healthcare funding and inconsistent reimbursement policies restrict access, leaving a large portion of the population untreated. Even in developed markets, rising healthcare costs and premium-priced next-generation devices create financial pressure on healthcare systems.

Advancements in Leadless and AI-Integrated Pacemakers

Advancements in leadless and AI-integrated pacemakers present significant growth opportunities for the pacemakers market. Leadless pacemakers represent one of the most significant innovations, eliminating traditional leads and surgical pockets, which reduces infection risks, improves patient comfort, and enables minimally invasive implantation. Their compact size allows placement directly inside the heart via catheter-based procedures, shortening recovery time and making the therapy accessible to patients who previously faced complications with conventional systems. Ongoing improvements in battery efficiency, device positioning, and expandability, such as dual-chamber leadless pacing, are further expanding their clinical applicability.

AI-integrated pacemakers are enabling a new era of intelligent cardiac care. These devices use machine learning algorithms to analyze patient rhythms, detect abnormalities earlier, and optimize pacing parameters automatically. AI enhances remote monitoring capabilities, allowing clinicians to track patient data in real time and intervene proactively before complications arise. Predictive analytics can forecast arrhythmia episodes, battery health, or pacing irregularities, ensuring timely medical attention.

Category-wise Analysis

Product Type Insights

Implantable pacemakers are anticipated to dominate the market, accounting for 70% of the market share in 2026. Its dominance is driven by permanence, reliability, and remote monitoring, making it preferred for chronic conditions. Implantable pacemakers, such as those offered by Boston Scientific Corporation, deliver dual-chamber pacing for better heart rhythm synchronization. Their durability and advanced features make them a preferred choice among cardiologists.

External pacemakers are likely to represent the fastest-growing segment, driven by rising temporary pacing needs and increasing use in emergency and critical care settings. Their adjustability and ease of use make them ideal for acute cardiac conditions. Growing innovation in wearable and portable designs further accelerates adoption, especially in hospitals and rapidly expanding healthcare markets across the Asia Pacific region.

Application Insights

Bradycardia is anticipated to lead the market, holding 40% of the share in 2026, due to its high prevalence, especially among the elderly. Conduction blocks and age-related cardiac deterioration drive strong demand for pacing support. Pacemakers remain the primary treatment for maintaining stable heart rates, making bradycardia the most commonly addressed condition and a consistent driver of market growth.

Arrhythmias are likely to represent the fastest-growing segment, driven by the rising incidence of atrial fibrillation and growing reliance on pacemakers to support ablation procedures. Pacemakers provide effective rate control, improving outcomes for patients undergoing rhythm-management therapies. With increasing diagnosis rates, expanded treatment guidelines, and greater clinical adoption, arrhythmia-related pacemaker use is accelerating rapidly across global cardiac care settings.

End-user Insights

Hospitals are expected to dominate the market, holding approximately 60% of the share in 2026, driven by they offer advanced cardiac care infrastructure, skilled cardiologists, and full surgical facilities required for implantation and post-procedure monitoring. They handle most emergency and complex cardiovascular cases, making them the primary centers for pacemaker surgeries. Hospitals provide comprehensive diagnostics, follow-up care, and device management, strengthening their leading market share.

Outpatient facilities are projected to represent the fastest-growing segment, due to their advanced infrastructure, surgical expertise, and comprehensive cardiac care capabilities. They remain the primary centers for pacemaker implantation, diagnostics, and follow-up procedures. With specialized cardiology teams and access to emergency care, hospitals continue to be the most trusted and preferred setting for pacemaker treatments.

Regional Insights

North America Pacemaker Market Trends

North America is projected to be the leading region, accounting for 45% of the pacemakers market in 2026, supported by a highly advanced healthcare ecosystem, strong adoption of innovative cardiac technologies, and a large population affected by cardiovascular diseases. The U.S. dominates the regional market due to its robust hospital infrastructure, early availability of cutting-edge devices, and strong reimbursement policies that encourage the use of advanced pacemaker systems.

The region is also at the forefront of leadless pacemaker adoption, driven by clinicians’ preference for minimally invasive procedures and reduced complication risks. Continuous technological progress, including longer battery life, improved sensing capabilities, remote monitoring, and AI-based diagnostic alerts, is transforming patient management and driving greater trust in next-generation devices.

Major players, such as Medtronic, Boston Scientific, and Abbott, maintain strong market presence through consistent R&D investments, product launches, and extensive clinical trial programs. Partnerships between hospitals, technology firms, and research institutions are accelerating the development of digital cardiac care solutions. The rising focus on personalized medicine, home-based monitoring, and integrated cardiac care platforms is shaping the future of pacemaker usage.

Europe Pacemakers Market Trends

Europe is supported by advanced healthcare systems, strong regulatory frameworks, and a high prevalence of cardiovascular diseases among the region’s aging population. Countries such as Germany, France, the U.K., Italy, and Spain remain major contributors due to well-established cardiac care centers and strong adoption of innovative medical technologies. Europe is also witnessing a rising preference for minimally invasive procedures, which is boosting demand for leadless pacemakers and MRI-compatible devices. Continuous advancements in battery life, device miniaturization, and remote monitoring technologies further strengthen market growth across the region.

Reimbursement support in countries including Germany and France plays a crucial role in encouraging implant procedures, while growing investments in research and clinical trials help accelerate technological breakthroughs. The region also focuses heavily on patient safety, quality standards, and evidence-based medicine, prompting companies to introduce high-performance pacemakers with improved durability and diagnostic capabilities. Collaborations between hospitals, research institutions, and medtech organizations enhance innovation and training opportunities for cardiologists.

Asia Pacific Pacemakers Market Trends

Asia Pacific is likely to be the fastest-growing market for pacemakers, driven by rising cardiovascular disease prevalence, an expanding elderly population, and rapidly improving healthcare infrastructure. Countries such as China, India, Japan, and South Korea are witnessing a significant increase in cardiac disorders due to urbanization, lifestyle changes, and higher diagnosis rates, creating strong demand for pacemaker implants.

The region is also benefiting from greater healthcare investments, expansion of cardiac specialty hospitals, and government initiatives aimed at improving access to life-saving medical devices. Local manufacturers, especially in China, are strengthening their capabilities by offering affordable pacemaker solutions that cater to diverse patient needs, making advanced cardiac care more accessible.

Technological advancements such as MRI-compatible pacemakers, leadless systems, remote monitoring, and AI-powered diagnostics are steadily gaining traction across the region. International players are increasingly partnering with local distributors or forming joint ventures to tap into the growing market potential. Rising awareness campaigns, improved reimbursement structures in countries such as Japan and Australia, and growing medical tourism in India and Thailand further support market expansion.

Competitive Landscape

The global pacemakers market is highly competitive, characterized by a mix of established medtech leaders and emerging regional specialists. In developed regions such as North America and Europe, companies such as Medtronic and Boston Scientific Corporation maintain dominant positions due to their strong research and development pipelines, extensive distribution networks, and consistent product innovation. Their leadership is reinforced by early adoption of advanced technologies, broad clinical trial engagement, and strong relationships with cardiology centers.

In the Asia Pacific region, companies such as MicroPort Scientific Corporation are rapidly strengthening their presence by offering cost-effective, localized pacemaker solutions tailored to regional healthcare needs. A key competitive differentiator across the market is the growing shift toward leadless pacemakers, which provide minimally invasive implantation, greater comfort, and reduced complication risks, driving companies to accelerate innovation in this segment. Strategic partnerships, acquisitions, and integration of artificial intelligence for remote monitoring and predictive diagnostics are reshaping the market landscape.

Key Developments

- In October 2025, global healthcare company Abbott announced the launch of a dual-chamber leadless pacemaker system, which will help the heart beat properly without wires or surgical pockets used in traditional pacemakers.

- In March 2025, MicroPort® CRM announced that MicroPort® CRM Shanghai had launched the localized TEN pacemaker family in China. The six-model lineup offered single- and dual-chamber options with compact design, long battery life, and AutoMRI™ technology, enabling safe 1.5T and 3T MRI scans.

Companies Covered in Pacemakers Market

- OSYPKA MEDICAL

- Boston Scientific Corporation

- Zoll Medical Corporation

- Medtronic

- BIOTRONIK SE & Co. KG

- MicroPort Scientific Corporation

- MÉDICO S.R.L.

- Shree Pacetronix Ltd.

- Abbott

- OSCOR Inc.

- Lepu Medical Technology (Beijing) Co., Ltd.

Frequently Asked Questions

The global pacemakers market is projected to reach US$6.4 billion in 2026.

The rising prevalence of cardiovascular diseases and demand for rhythm management devices are key drivers.

The pacemakers market is poised to witness a CAGR of 7.9% from 2026 to 2033.

Advancements in leadless and AI-integrated pacemakers are the key opportunities.

OSYPKA MEDICAL, Boston Scientific Corporation, Medtronic, BIOTRONIK SE & Co. KG, and Abbott are the key players.