- Medical Devices

- Ozone Therapy Units Market

Ozone Therapy Units Market Size, Share, and Growth Forecast, 2026 - 2033

Ozone Therapy Units Market by Product Type (Trolley-Mounted Ozone Therapy Units, Table-top Ozone Therapy Units), Application (Oncological Treatment, Dermatological Treatment, Others), End-user (Hospitals & Clinics, Others), and Regional Analysis for 2026 - 2033

Ozone Therapy Units Market Size and Trends Analysis

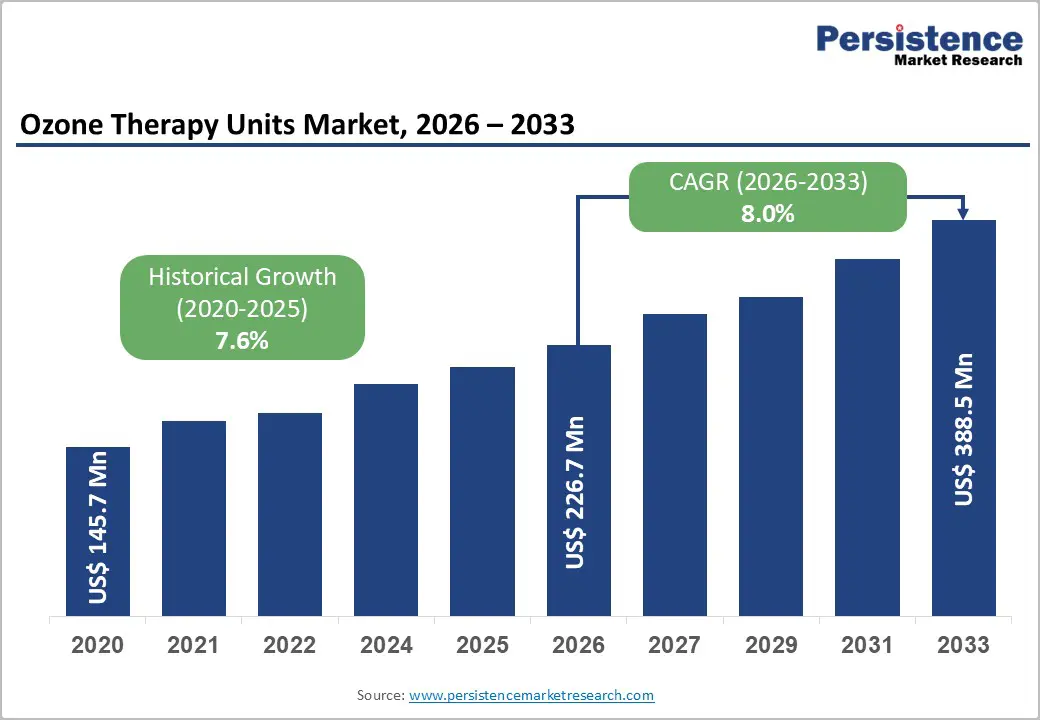

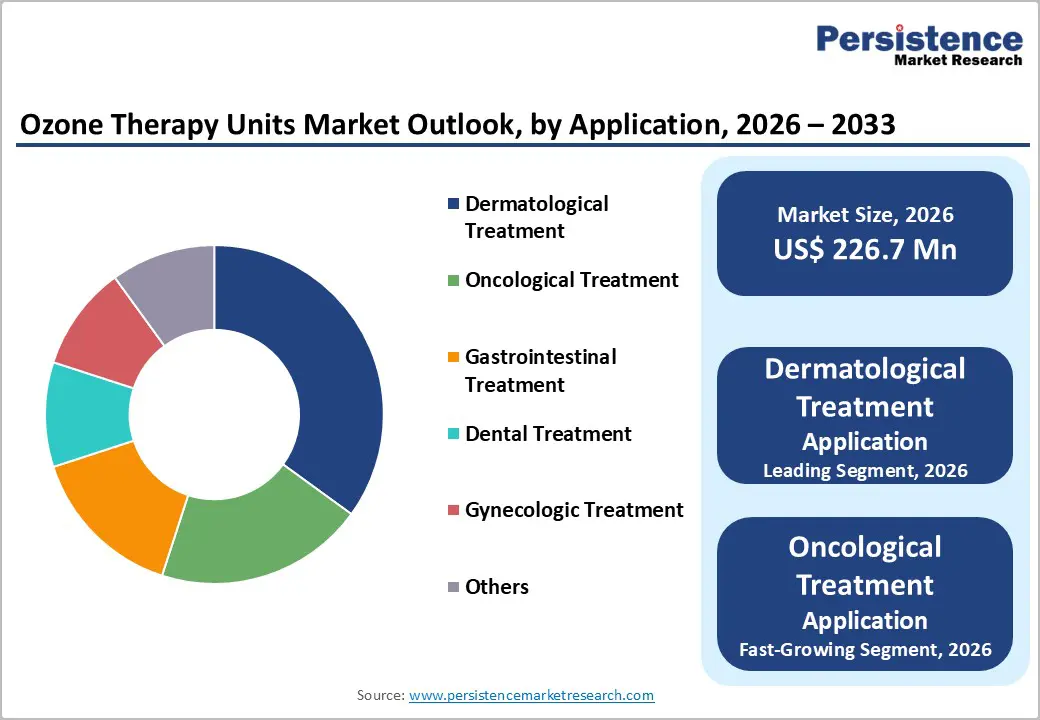

The global ozone therapy units market size is likely to be valued at US$226.7 million in 2026, and is expected to reach US$388.5 million by 2033, growing at a CAGR of 8.0% during the forecast period from 2026 to 2033, driven by the increasing prevalence of alternative medical treatments, rising demand for non-invasive therapies in dermatology and oncology, and advancements in portable ozone generation technologies.

Growing demand for compact, user-friendly ozone therapy units, especially trolley-mounted and table-top models, is accelerating adoption among end-users. Advances in high-purity ozone delivery are further boosting uptake by offering safer, more effective options. Increasing recognition of ozone therapy units as critical for wound healing and immune support in emerging healthcare markets remains a major driver of market growth.

Key Industry Highlights:

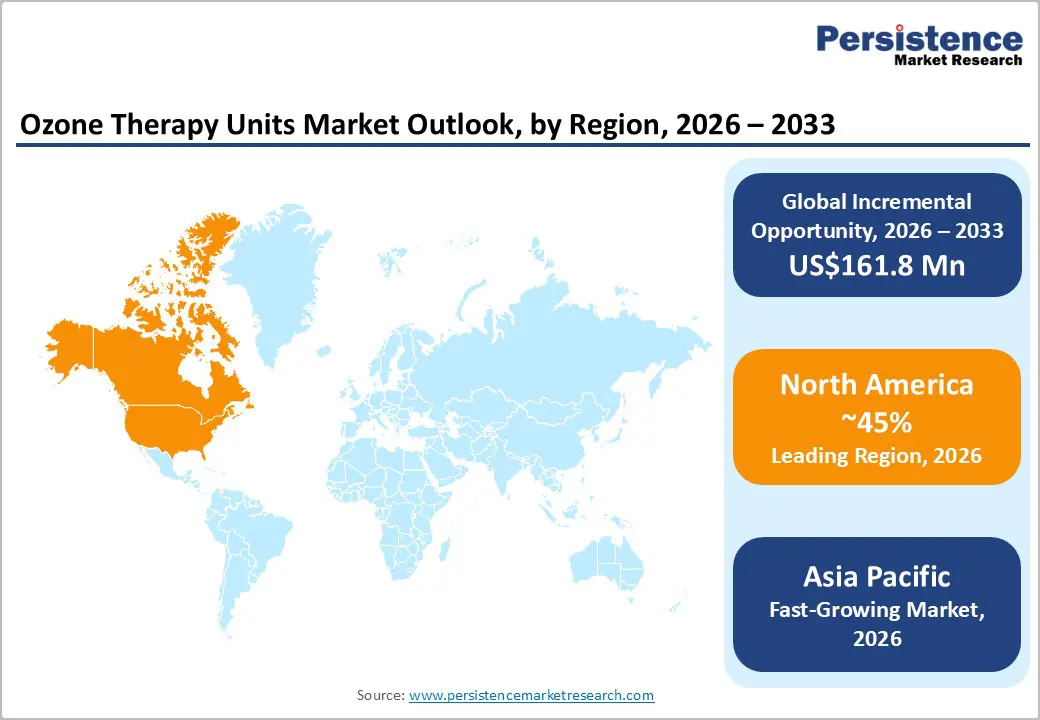

- Leading Region: North America, anticipated to account for a 45% market share in 2026, driven by the region’s advanced alternative healthcare infrastructure, strong research and development capabilities, and high public awareness of non-invasive benefits

- Fastest-growing Region: Asia Pacific, fueled by rising chronic disease burden, growing wellness tourism, and increasing investments in alternative therapies in China and India.

- Dominant Product Type: Trolley-mounted ozone therapy units, to hold approximately 60% of the market share, as they provide mobility and versatility for clinical use.

- Leading Application: Dermatological treatment, to account for over 35% of the market revenue in 2026, due to ozone's efficacy in skin rejuvenation and wound care.

- Leading End-user: Hospitals & clinics, to contribute nearly 50% of the market revenue in 2026, due to integrated treatment protocols and high patient volume.

| Key Insights | Details |

|---|---|

|

Ozone Therapy Units Market Size (2026E) |

US$226.7 Mn |

|

Market Value Forecast (2033F) |

US$388.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

8.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Alternative Medical Treatments and Non-Invasive Therapies

The growing interest in alternative medical treatments is creating a significant opportunity for manufacturers of ozone therapy units. This trend is fueled by rising consumer preference for natural, low-risk therapies and a reduced dependence on pharmaceuticals. Conventional treatments, particularly in dermatology and oncology, often come with side effects that can lower patient adherence. Non-invasive solutions, such as trolley-mounted units, table-top devices, autohemotherapy systems, and ozone generators, offer a gentler, oxygen-based approach. These devices streamline procedures, minimize the need for invasive methods, and are especially effective in wellness programs or chronic disease management where immune support is important.

Ozone therapy units also help lower risks of infection and inflammation, and shorten recovery periods, which remain key concerns in healthcare. They promote better oxygenation and are easier to integrate into care settings, with trolley-mounted and table-top models being particularly suitable for high-volume clinics or home use. As global health authorities encourage broader access to alternative and patient-friendly therapies, demand for ozone therapy continues to grow across gastrointestinal, dental, and gynecologic applications.

High Development and Regulatory Approval Costs

High development and regulatory approval costs pose major challenges for companies developing next-generation ozone therapy units and innovative systems. Creating advanced models, such as high-purity trolley-mounted units, compact table-top devices, or automated systems, requires extensive research, specialized generators, and sophisticated safety technologies, making them far more expensive than standard models. Ensuring efficacy is an even greater challenge: many advanced units, precision-controlled products, and ozone-stable formulations are highly sensitive to dosage, oxidation, and sterility, demanding careful optimization to maintain safety throughout use. Achieving reliable long-term performance often involves costly clinical trials, advanced testing, and high-quality materials, substantially increasing R&D expenditures.

Meeting strict regulatory requirements for medical device certification, safety, and batch consistency further adds to the burden. Multiple validation studies under varied conditions and across numerous production batches are necessary, extending development timelines and costs. Scaling up manufacturing also requires controlled cleanrooms, specialized ozone chambers, and robust quality-assurance systems, driving expenses even higher. For smaller manufacturers, these hurdles can limit innovation and delay commercialization.

Innovations in Portable and High-Purity Delivery Platforms

Innovations in portable and high-purity ozone therapy delivery platforms are reshaping the global healthcare landscape by tackling two key challenges: mobility and dosage precision. Portable systems are designed for compactness, reducing dependence on fixed units and enabling effective home-based treatments. Advancements such as battery-powered trolley-mounted devices, lightweight table-top units, auto-dosing systems, and app-controlled generators enhance accessibility, minimize hospital visits, and lower costs for both providers and patients.

High-purity platforms, including medical-grade ozone filters, precision mixers, sterile bags, and UV-protected tubing, promote safer applications by ensuring controlled oxidation, the therapy’s primary safeguard against side effects. These systems eliminate impurities, improve efficacy, and support versatile use without requiring highly skilled operators, making them ideal for large-scale clinical programs. Cutting-edge technologies such as nano-bubbling, bio-adhesive applicators, and VLP-based monitoring further enhance safety and therapeutic response.

Category-wise Analysis

Product Type Insights

Trolley-mounted ozone therapy units are anticipated to dominate the market, accounting for approximately 60% of the market share in 2026. Its dominance is driven by mobility, high capacity, and versatility, making it preferred for clinics. Trolley-mounted ozone therapy units provide multi-application support, ensure safety, and contribute to efficiency, making them suitable for large-scale healthcare campaigns. The OZONOSAN boardcase is built in a portable trolley format, allowing it to be easily moved between treatment rooms, used in home visits, or integrated into multi-room clinical workflows, which directly supports the idea that mobility enhances versatility and large-scale use in clinics.

Table-top ozone therapy units represent the fastest-growing segment, due to their compactness and expanding use in home care. Its portable profile makes it ideal for targeted personal use, reducing clinic visits. Continuous innovations in miniaturization are further strengthening accessibility, driving rapid adoption across North America and Europe, where demand for convenient, home-based therapies is accelerating. The OZOMED smartline is explicitly designed as a table-top unit, making it suitable for small clinics and practices where space is limited and for users who want a smaller, accessible unit for personal or near-home use.

Application Insights

Dermatological applications are projected to lead, accounting for approximately 35% of the market share by 2026. This growth is driven by increasing demand for skin regeneration, large-scale aesthetic programs, and global interest in anti-inflammatory therapies. Clinics are expanding their wound care services, further reinforcing the dominance of dermatology in the market. The rising adoption of ozone therapy for oncological support and expanded dental programs reflects the growing focus on multi-therapeutic applications. MEDOZONS Ltd. (Russia) is a prominent player in the global dermatology-focused ozone therapy market. Its MEDOZONS® PRO-01 Ozone Therapy Device is a professional medical ozone generator designed for both local and systemic use, supporting dermatological treatments such as wound healing, inflammatory skin conditions, acne, alopecia, and other skin regeneration protocols.

Oncological treatment is likely to be the fastest-growing segment, due to strong momentum in adjunct therapy and expanding inclusion in cancer support. The growing shift toward immune-boosting platforms, along with better tolerance, accelerates the adoption. Advancements in ozone protocols and continued progress of clinical trials drive market growth. Brio-Medical explicitly includes advanced ozone therapy (specifically EBOO-Extracorporeal Blood Oxygenation and Ozonation) as part of its integrative oncology program to support patients with various types and stages of cancer. This reflects real-world adoption of ozone protocols as a complement to standard cancer care rather than a replacement therapy.

End-user Insights

Hospitals and clinics are projected to dominate, accounting for nearly 50% of the revenue share by 2026. They remain the primary centers for treatment, managing large patient programs and diverse therapies that require controlled ozone administration. Their strong infrastructure, trained personnel, and capacity for high-volume or specialized sessions drive higher usage. Hospitals are at the forefront of deploying trolley-mounted units and conducting emerging table-top trials. For example, Arka Anugraha Hospital, an NABH-accredited integrative and functional medicine facility, actively incorporates medical ozone therapy into its treatment protocols, highlighting the role of large clinical settings in leading adoption.

Homecare settings are expected to be the fastest-growing segment, fueled by convenience and the increasing popularity of self-administered therapies. Homecare offers quick, accessible treatments, appealing to users who prefer low-effort, at-home options. Expanded outreach programs, a growing wellness focus, and wider availability of routine and premium units are accelerating adoption, particularly in urban and semi-urban areas. The Airthereal AH1000 Portable Ozone Machine, for instance, is commonly used for personal wellness, air treatment, and small-scale ozone procedures at home.

Regional Insights

North America Ozone Therapy Units Market Trends

North America is expected to lead, accounting for roughly 45% of the market share by 2026. This growth is driven by the region’s advanced alternative healthcare infrastructure, strong R&D capabilities, and high public awareness of the benefits of non-invasive treatments. Robust distribution networks in the U.S. and Canada ensure widespread availability of ozone therapy units across dermatology, oncology, and dental applications. Rising demand for table-top, user-friendly, and convenient formats is further accelerating adoption, as these designs improve accessibility and lower barriers compared with traditional methods.

Technological innovations, including stable high-purity delivery, enhanced portability, and targeted therapeutic integration, are attracting significant investment from both public and private sectors. Government initiatives and wellness campaigns continue to encourage use for chronic inflammation, wound healing, and emerging immune challenges, sustaining market demand. The growing emphasis on homecare devices and specialty applications, particularly in gastrointestinal treatments, is broadening the scope of ozone therapy unit use.

Europe Ozone Therapy Units Market Trends

Europe is experiencing significant growth in the ozone therapy units market, driven by rising awareness of therapeutic benefits, robust healthcare systems, and government-led wellness initiatives. Countries such as Germany, France, and the U.K. have well-established medical frameworks that support routine ozone therapy and encourage the adoption of innovative delivery methods. These effective treatments are particularly appealing to dermatology patients, health-conscious consumers, and oncology populations, improving compliance and coverage rates.

Technological advancements, such as enhanced purity, targeted delivery systems, and improved portable units, are further expanding market potential. European authorities are increasingly backing research and clinical trials for both routine and specialized applications, boosting confidence in the sector. Growing emphasis on convenient, home-use options aligns with the region’s preventive healthcare focus and efforts to reduce hospital visits. Public awareness campaigns and promotional initiatives are extending reach in urban and rural areas, while suppliers are investing in next-generation units to enhance efficacy and versatility.

Asia Pacific Ozone Therapy Units Market Trends

The Asia Pacific region is expected to be the fastest-growing market for ozone therapy units, driven by rising health awareness, expanding government initiatives, and increasing application programs. Countries including India, China, Japan, and various Southeast Asian nations are actively promoting therapy campaigns to address chronic disease prevalence and emerging wellness needs. Ozone therapy units are particularly appealing in these markets due to their non-invasive nature, scalability, and suitability for large-scale clinical programs in both urban and rural areas.

Technological advancements are enabling the development of stable, effective, and user-friendly ozone therapy units capable of withstanding challenging climatic conditions and reducing infection risks. These innovations are essential for extending access to remote facilities and enhancing overall therapeutic coverage. Growing demand across dermatology, oncology, and dental applications is further driving market expansion. Public-private partnerships, increasing healthcare spending, and rising investment in ozone research and manufacturing are also accelerating growth. The convenience, improved efficacy, and lower risk of side effects make ozone therapy units an increasingly preferred option in the region.

Competitive Landscape

The global ozone therapy units market is characterized by competition between established medical leaders and emerging specialized players. In North America and Europe, companies like W&H Dentalwerk Burmoos GmbH and APOZA Enterprise Co., Ltd. maintain leadership through strong R&D, extensive distribution networks, and industry partnerships, supported by innovative product lines and treatment programs. In the Asia Pacific region, Aquolab is advancing the market with localized solutions that improve accessibility. High-purity delivery systems enhance safety, reduce risks, and facilitate large-scale integration across regions. Strategic partnerships, collaborations, and acquisitions are helping companies combine expertise, expand portfolios, and accelerate commercialization. Portable units address mobility challenges, supporting growth in homecare and decentralized treatment settings.

Key Industry Developments

- In June 2025, Ozone Medical launched the O3Go, a portable ozone therapy device designed to broaden ozone therapy use in both homecare and clinics, reflecting the trend toward compact, accessible devices.

- In May 2025, Nippon Ozone acquired the medical device unit of MediOzone to expand its ozone therapy portfolio and accelerate access to advanced ozone delivery systems.

Companies Covered in Ozone Therapy Units Market

- W&H dentalwerk burmoos GMBH

- APOZA Enterprise Co., Ltd.

- Aquolab

- J.Hänsler GmbH

- Evozone GmbH

- Herrmann Apparatebau GmbH

- MIO International Ozonytron GmbH

- Sedecal

- CLEM Prevention

Frequently Asked Questions

The global ozone therapy units market is projected to reach US$226.7 million in 2026.

The rising prevalence of alternative medical treatments and demand for non-invasive therapies are key drivers.

The ozone therapy units market is poised to witness a CAGR of 8.0% from 2026 to 2033.

Advancements in portable and high-purity delivery platforms are key opportunities.

W&H dentalwerk Burmoos GmbH, APOZA Enterprise Co., Ltd., Aquolab, J.Hänsler GmbH, and Evozone GmbH are the key players.