- Pharmaceuticals

- Opioid Analgesics Market

Opioid Analgesics Market Size, Share, and Growth Forecast 2026 - 2033

Opioid Analgesics Market by Drug Type (Morphine, Oxycodone, Codeine, Fentanyl, Tramadol, Methadone, Others), by Route of Administration (Oral, Injectable, Transdermal, Others), by Application (Cancer Pain, Post-operative Pain, Chronic Pain, Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), by Regional Analysis, 2026 - 2033

Opioid Analgesics Market Share and Trends Analysis

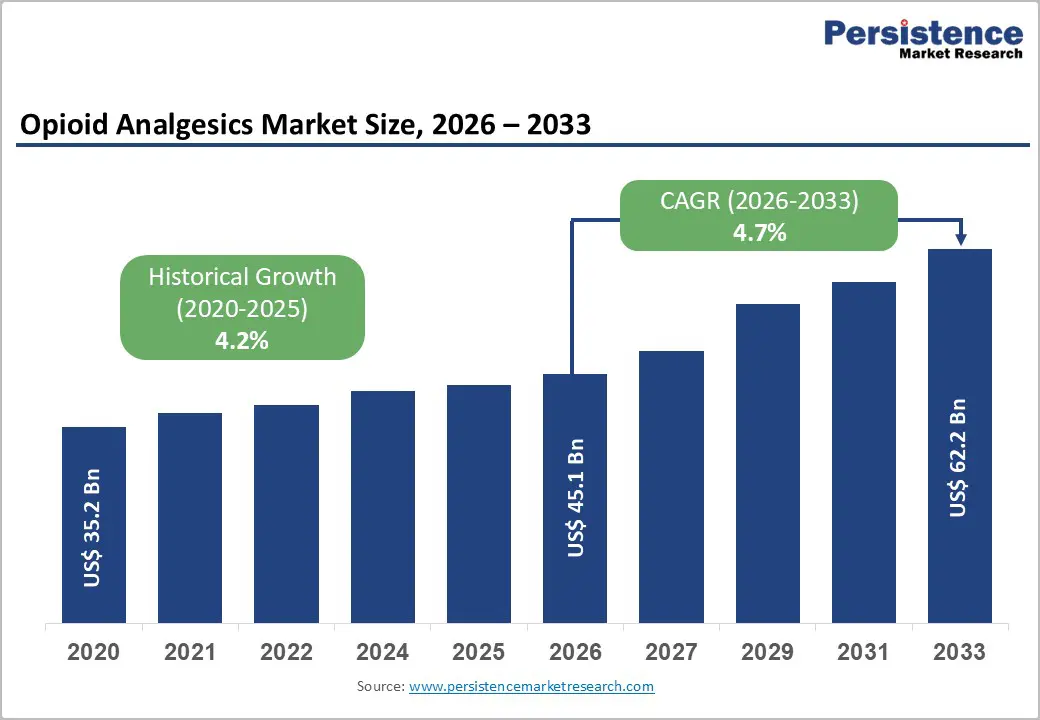

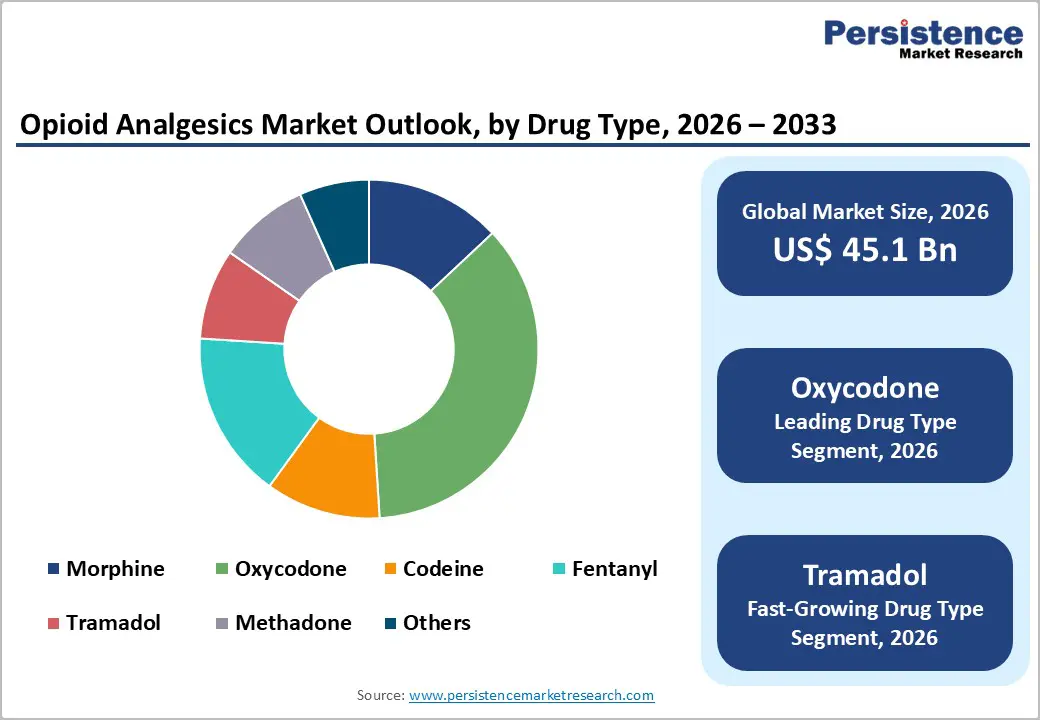

The global Opioid Analgesics market size is expected to be valued at US$ 45.1 billion in 2026 and projected to reach US$ 62.2 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033. The market’s steady expansion reflects the sustained burden of moderate-to-severe pain associated with cancer, major surgery, trauma, and chronic musculoskeletal disorders, particularly in aging populations, where non-opioid options are often insufficient.

According to the World Health Organization (WHO), around 60 million people globally use opioids, while millions live with inadequately managed pain despite growing awareness and clinical guidelines promoting balanced opioid stewardship. In parallel, updates to the Centers for Disease Control and Prevention (CDC) opioid prescribing guideline and broader adoption of multimodal pain strategies have tempered inappropriate prescribing without eliminating the critical need for opioids in carefully selected patients.

Key Industry Highlights:

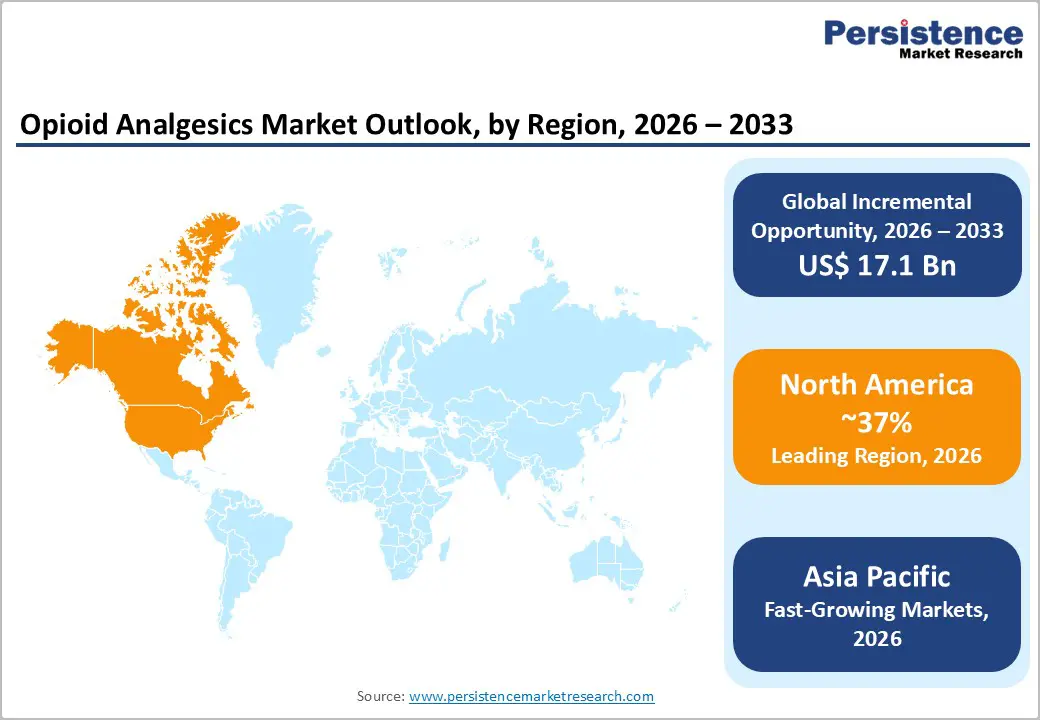

- North America remains the leading region in the opioid analgesics market with about 37% share in 2025, underpinned by high chronic pain prevalence, large cancer and surgical patient populations, and established prescribing practices, even as CDC guidelines and PDMPs have driven more than 40% reductions in dispensing rates since 2012.

- Asia Pacific is the fastest-growing region, benefiting from rapid healthcare infrastructure expansion, demographic aging in China with more than 254 million people aged 60+, and regulatory reforms in India and ASEAN that improve medical opioid availability for cancer, post-operative, and chronic pain within structured stewardship frameworks.

- Among drug types, Oxycodone dominates with an estimated 36% share in 2025, supported by flexible immediate- and extended-release oral formulations, strong evidence for moderate-to-severe pain control, and uptake of abuse-deterrent versions that mitigate tampering risks while preserving efficacy in oncology, post-operative, and chronic pain indications.

- Tramadol stands out as the fastest-growing drug segment, particularly in Europe and Asia Pacific, where its dual mechanism and relatively lower scheduling make it attractive for stepwise pain management, offering a bridge between non-opioid therapies and strong opioids in both chronic musculoskeletal and cancer-related pain.

- Key market opportunities center on abuse-deterrent formulations, advanced delivery systems such as transdermal and transmucosal products, and expansion into emerging markets where under-treatment of pain remains substantial, enabling manufacturers with robust compliance, education programs, and diversified portfolios to capture growth while aligning with evolving regulatory and public health expectations.

| Key Insights | Details |

|---|---|

|

Opioid Analgesics Market Size (2026E) |

US$ 45.1 billion |

|

Market Value Forecast (2033F) |

US$ 62.2 billion |

|

Projected Growth CAGR (2026-2033) |

4.7% |

|

Historical Market Growth (2020-2025) |

4.2% |

Market Dynamics

Drivers - Rising Chronic Pain Burden and Cancer-Related Pain Management Needs

Escalating chronic pain prevalence and growing cancer incidence are central drivers of the opioid analgesics market. The National Institute on Drug Abuse (NIDA) and CDC estimate that tens of millions of adults in the United States live with chronic pain, with more than 50 million reporting pain on most days, creating sustained demand for potent analgesics when non-opioid measures fail. In oncology, multiple studies show that over 25% of cancer patients experience moderate-to-severe pain, and persistent opioid use develops in roughly 10% of patients after cancer surgery, underscoring opioids’ continued role in palliative and supportive care. In Europe, a large multinational DARWIN EU cohort study found that approximately 1 in 10 adults aged 50+ received at least one opioid prescription in 2019, highlighting widespread clinical reliance for chronic and cancer-related pain. As populations age in North America, Europe, and the Asia Pacific, and cancer prevalence rises, clinically appropriate opioid use in oncology, palliative care, and advanced chronic pain drives stable baseline demand despite tighter controls.

High Surgical Volumes and Post-operative Pain Management Requirements

Global growth in surgical procedures provides another strong underpinning for opioid analgesics consumption. In the United States, more than 50 million inpatient surgical procedures are performed annually, and evidence shows that over 80% of surgical patients receive opioid analgesics perioperatively to manage acute pain. Research published in JAMA Network Open and other journals indicates that 6–10% of previously opioid-naïve patients continue opioid use beyond 90 days after major surgery, demonstrating the significant exposure generated by perioperative care. Similar trends are seen in large European healthcare systems, where opioids are routinely integrated into multimodal post-operative regimens for orthopedic, abdominal, and cardiovascular procedures. In Asia Pacific, rising elective surgery volumes in China and India, driven by expanding hospital infrastructure and insurance coverage, are increasing reliance on short-acting opioids such as morphine, fentanyl, and oxycodone for acute pain control. Even as guidelines from CDC, WHO, and professional societies advocate for the shortest effective duration and the lowest effective dose, the high base of surgical activity ensures ongoing demand from hospital and ambulatory surgery center settings.

Restraints - Stringent Regulatory Controls and Prescription Monitoring Programs

Intensifying regulatory oversight significantly constrains the opioid analgesics market growth, particularly in developed economies. The CDC’s original 2016 opioid prescribing guideline and its updated 2022 version, alongside state-level prescription drug monitoring programs (PDMPs), have led to substantial reductions in high-dose and long-duration prescribing in the United States. CDC dispensing data show that opioid prescribing rates have fallen by more than 40% since their peak in 2012, with more stringent thresholds for daily morphine milligram equivalents and early refill limits. In Europe, regulatory agencies and payers have tightened reimbursement criteria and monitoring, with UK primary care data indicating more than 50% reduction in new opioid prescribing episodes over the past decade, even though overall prevalence in older adults remains considerable. These interventions, while critical for curbing misuse, also reduce total prescription volume, especially in chronic non-cancer pain, thereby moderating market expansion.

Opioid Crisis Awareness and Shift Toward Non-Opioid Alternatives

Public health focus on the opioid crisis has reshaped prescriber and patient attitudes, limiting opioid growth in several indications. According to the WHO, opioids are responsible for the majority of drug-related deaths worldwide, with an estimated 128,000 deaths due to opioid overdose in 2021. In the United States, total drug overdose deaths reached roughly 114,000 in 2023, driven predominantly by synthetic opioids such as illicit fentanyl, fueling prescriber caution and regulatory scrutiny. The U.S. Drug Enforcement Administration (DEA) and state authorities have launched initiatives such as the Fentanyl Free America campaign and tightened controls on dispensing and distribution. In parallel, investment in non-opioid analgesics, including sodium channel (NaV1.8) inhibitors, anti-nerve growth factor antibodies, and neuromodulation approaches, offers alternative pain management options, particularly for chronic musculoskeletal and neuropathic pain. This clinical and societal pivot away from opioids in many chronic pain scenarios acts as a drag on market growth, especially for long-acting formulations.

Opportunities - Abuse-Deterrent Formulations (ADFs) and Advanced Delivery Systems

The development and adoption of abuse-deterrent formulations create a key opportunity segment within the opioid analgesics market. Regulatory agencies, including the U.S. Food and Drug Administration (FDA), have encouraged the transition from easily manipulated oral opioids to ADFs designed to resist crushing, dissolving, or injecting, while still delivering effective analgesia when taken as prescribed. Reformulated extended-release oxycodone products, such as abuse-deterrent versions of OxyContin, incorporate physical and chemical barriers that significantly reduce abuse via snorting or injection compared with older formulations. At the same time, transdermal systems (for example, fentanyl patches) and transmucosal formulations (sublingual or buccal tablets and films) deliver steady-state analgesia for cancer and severe chronic pain, improving adherence and reducing peak-related adverse effects. As payers and regulators increasingly favor ADF labeling and risk evaluation and mitigation strategy (REMS) programs, manufacturers capable of demonstrating real-world abuse reduction while maintaining pain control can capture premium pricing and defend market share even in a constrained prescribing environment.

Emerging Markets Expansion and Improving Access to Pain Management in the Asia Pacific

Rapidly developing healthcare systems in the Asia Pacific offer substantial growth potential, particularly where historical access to opioid analgesics has been limited. WHO and palliative care organizations have long highlighted under-treatment of moderate-to-severe pain in low- and middle-income countries, including large parts of Asia, due to regulatory, supply chain, and affordability barriers. As countries such as China, India, and members of the Association of Southeast Asian Nations (ASEAN) expand health insurance coverage and invest in oncology and surgical capacity, demand for strong opioids such as morphine, oxycodone, and fentanyl, as well as weaker opioids like tramadol, is rising. For example, China had approximately 254 million people aged 60 years or older in 2019, a figure expected to grow substantially by 2035, creating a large pool of patients with cancer, osteoarthritis, and other painful chronic diseases. In India, a large unmet need in palliative care and post-operative pain control is prompting regulatory reforms to improve medical opioid availability while maintaining controls on diversion. Manufacturers that can supply high-quality, cost-effective oral and injectable opioids, along with training and stewardship programs, are well-positioned to benefit from these structural shifts.

Category-wise Analysis

Drug Type Insights

Within the opioid analgesics market, Oxycodone is the leading drug type, accounting for approximately 36% of global market share in 2025. As a semi-synthetic mu-opioid receptor agonist, oxycodone offers flexible oral formulations in both immediate-release and extended-release forms, making it suitable for acute post-operative pain, chronic back pain, and cancer-related pain. Prescription data from the CDC and analyses of U.S. outpatient prescribing patterns consistently rank oxycodone among the top-dispensed opioids, alongside hydrocodone and morphine, particularly for moderate-to-severe pain in ambulatory settings. Abuse-deterrent formulations have helped sustain oxycodone’s role despite policy headwinds, as reformulated brands and generics reduce attractiveness for tampering and non-medical use. Clinical studies suggest that oxycodone can provide comparable or superior analgesia to morphine for some surgical and cancer pain indications, with a safety profile familiar to prescribers, further reinforcing its dominance. Tramadol is emerging as the fastest-growing opioid drug type, particularly in markets emphasizing stepwise pain management, due to its dual mechanism of action (weak mu agonism plus serotonin–norepinephrine reuptake inhibition) and relatively lower scheduling in many jurisdictions.

Route of Administration Insights

By route of administration, Oral opioids represent the leading segment, estimated to hold a market share of around 60–65% in 2025, reflecting the central role of tablets and capsules in both chronic and acute pain management. In community and primary care settings, the vast majority of opioid prescriptions are written for oral dosage forms such as immediate-release oxycodone, hydrocodone, and codeine, owing to their convenience, predictable pharmacokinetics, and suitability for outpatient use. The American Medical Association (AMA) and CDC prescribing data show that shifts in opioid use over the last decade have primarily affected oral agents, but they still constitute the bulk of dispensed opioid prescriptions. Injectable opioids, including intravenous morphine and fentanyl, dominate in emergency departments, intensive care units, and operating rooms, where rapid onset and titration are critical, making this the fastest-growing route in hospital settings as surgical procedures expand globally. Transdermal patches, especially fentanyl systems, hold a strong niche in long-term management of cancer pain and severe chronic pain in patients who cannot tolerate oral medications, supported by oncology and palliative care guidelines in Europe and North America.

Distribution Channel Insights

By distribution channel, retail pharmacies are the leading segment, estimated to account for roughly 50–55% of global opioid analgesic sales in 2025, reflecting the dominance of outpatient prescribing. In the United States, most prescriptions for oral opioids are dispensed through community pharmacy networks, which are also key touchpoints for prescription drug monitoring program (PDMP) surveillance and patient counseling. Retail channels in Europe similarly handle the majority of chronic pain and post-operative take-home prescriptions, under tight reimbursement and monitoring controls. Hospital Pharmacies hold a substantial share, particularly for injectable and transdermal opioids used in inpatient, intensive care, and oncology units, and they remain crucial in formulary decisions and stewardship initiatives. Online Pharmacies constitute the fastest-growing distribution channel, especially in North America and parts of Europe and Asia Pacific, where legitimate e-pharmacy platforms have expanded under stricter verification and e-prescribing frameworks. Regulatory bodies have simultaneously targeted illicit online sales, distinguishing licensed digital pharmacies from rogue websites as part of broader opioid crisis responses.

Regional Insights

North America Opioid Analgesics Market Trends and Insights

North America remains the leading region in the opioid analgesics market due to the high prevalence of chronic pain conditions, a well-established healthcare infrastructure, and strong access to prescription pain management therapies. The region has a large population suffering from cancer pain, post-surgical pain, arthritis, and musculoskeletal disorders, which increases the demand for effective opioid medications in hospitals and pain management clinics. In addition, the presence of major pharmaceutical manufacturers, extensive research activities, and ongoing product innovation support market growth. Regulatory agencies have also implemented stricter monitoring systems and prescription guidelines to reduce opioid misuse while ensuring availability for patients with severe pain. The increasing number of surgical procedures and the rising geriatric population further contribute to the demand for opioid-based analgesics. Moreover, improved palliative care services and better awareness of pain management practices continue to drive the adoption of opioid analgesics across healthcare facilities throughout North America.

Asia Pacific Opioid Analgesics Market Trends and Insights

Asia Pacific is the fastest-growing regional market for opioid analgesics, driven by large populations, expanding healthcare infrastructure, and increasing recognition of pain management as a human right. In China, demographic aging is dramatic, with approximately 254 million people aged 60 years or older as of 2019, expected to rise significantly by 2035, contributing to higher prevalence of cancer, osteoarthritis, and other chronic pain conditions requiring stronger analgesia. In India, the number of people living with chronic pain is estimated in the tens of millions, yet access to strong opioids remains uneven, prompting regulatory reforms to simplify medical use of morphine and other essential opioids under the amended Narcotic Drugs and Psychotropic Substances (NDPS) Act.

Manufacturing cost advantages in India and parts of China have supported a robust generics industry, supplying oral morphine, oxycodone, tramadol, and combination products to domestic and export markets. At the same time, some ASEAN countries are investing in palliative care networks and cancer centers, increasing demand for injectable and transdermal formulations suitable for hospital and hospice settings. International organizations and local professional societies are working to balance concerns about misuse with the imperative to treat severe pain, leading to gradual relaxation of overly restrictive procurement rules while retaining stringent controls on diversion. As awareness of multimodal pain management grows and insurance coverage expands, the Asia Pacific is expected to post the highest compound annual growth rate among all regions for opioid analgesics through 2033, particularly in segments such as tramadol and hospital-based injectable opioids.

Competitive Landscape

The opioid analgesics market is highly competitive, with numerous pharmaceutical manufacturers competing through product innovation, pricing strategies, and regulatory compliance. Companies focus on developing improved formulations such as extended-release and abuse-deterrent opioids to enhance safety and reduce misuse risks. Increasing investments in research and development are aimed at improving drug efficacy, delivery systems, and controlled dosing mechanisms. Strategic collaborations, mergers, and partnerships are also common as firms expand their product portfolios and geographic presence.

Key Market Developments

- In August 2025, Chemomouthpiece, LLC announced the results of a pivotal multi-center randomized controlled clinical trial evaluating its FDA-cleared Chemo Mouthpiece®, an intraoral cryotherapy device designed to reduce chemotherapy-induced oral mucositis.

- In January 2026, Vivozon Pharmaceutical launched a 20 mL small-pack version of its non-opioid injectable analgesic Onaprazoo in South Korea, aiming to expand pain management options in medical settings. The drug is designed to treat moderate to severe acute pain, particularly after surgical procedures.

Opioid Analgesics Market Research Segmentation

By Drug Type

- Morphine

- Oxycodone

- Codeine

- Fentanyl

- Tramadol

- Methadone

- Others

By Route of Administration

- Oral

- Injectable

- Transdermal

- Others

By Application

- Cancer Pain

- Post-operative Pain

- Chronic Pain

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region

- North America

- Europe

- East Asia

- South Asi/a & Oceania

- Latin America

- Middle East & Africa

Companies Covered in Opioid Analgesics Market

- Pfizer Inc.

- Johnson & Johnson

- Teva Pharmaceutical Industries Ltd.

- Purdue Pharma L.P.

- Mallinckrodt Pharmaceuticals

- Endo International plc

- AbbVie Inc.

- Sanofi S.A.

- Sun Pharmaceutical Industries Ltd.

- Hikma Pharmaceuticals PLC

- Mylan N.V.

- Bayer AG

Frequently Asked Questions

The global Opioid Analgesics market size is projected to reach approximately US$ 45.1 billion in 2026, and is expected to further expand to around US$ 62.2 billion by 2033, reflecting a forecast compound annual growth rate of about 4.7% over 2026–2033.

Key demand drivers include the high and persistent burden of chronic pain affecting more than 50 million adults in the United States, substantial cancer-related pain requiring strong opioids in over 25% of oncology patients, and growing global surgical volumes exceeding 50 million inpatient procedures annually in the U.S. alone, all of which sustain medically appropriate opioid use despite stewardship measures.

North America is the leading regional market, accounting for about 37% of global opioid analgesics revenues in 2025, underpinned by high chronic pain prevalence, large oncology and surgical caseloads, and historical prescribing patterns, even as CDC guidelines, PDMPs, and broader policy interventions have substantially reduced high-risk and long-duration prescribing.

A major growth opportunity lies in the development and uptake of abuse-deterrent formulations and advanced delivery systems, alongside expansion into under-served Asia Pacific markets where demographic aging, rising cancer incidence, and improving access to palliative and post-operative care are increasing demand for safe, well-regulated opioid therapies.

Prominent market participants include Pfizer Inc., Johnson & Johnson, Teva Pharmaceutical Industries Ltd., Purdue Pharma L.P., Mallinckrodt Pharmaceuticals, Endo International plc, AbbVie Inc., Sanofi S.A., Sun Pharmaceutical Industries Ltd., Hikma Pharmaceuticals PLC, Mylan N.V./Viatris Inc., and Bayer AG, complemented by regional generic manufacturers such as Dr. Reddy’s Laboratories Ltd. and Epic Pharma LLC.