- Technology

- On-board Connectivity Market

On-board Connectivity Market Size, Share, and Growth Forecast 2026 - 2033

On-board Connectivity Market Component (Hardware, Software, Services), Technology (Satellite, Air-to-Ground, Other), Application (Entertainment, Communication, Safety & Operation, Other), Transportation (Aviation, Maritime, Rail), and Regional Analysis for 2026 - 2033

On-board Connectivity Market Size and Trend Analysis

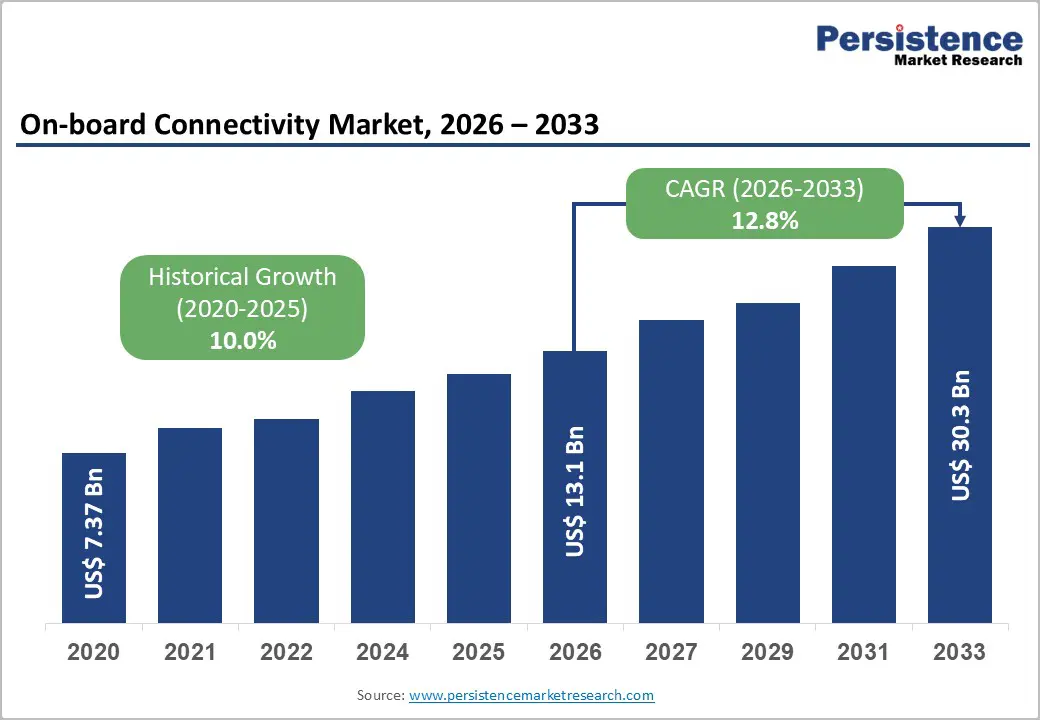

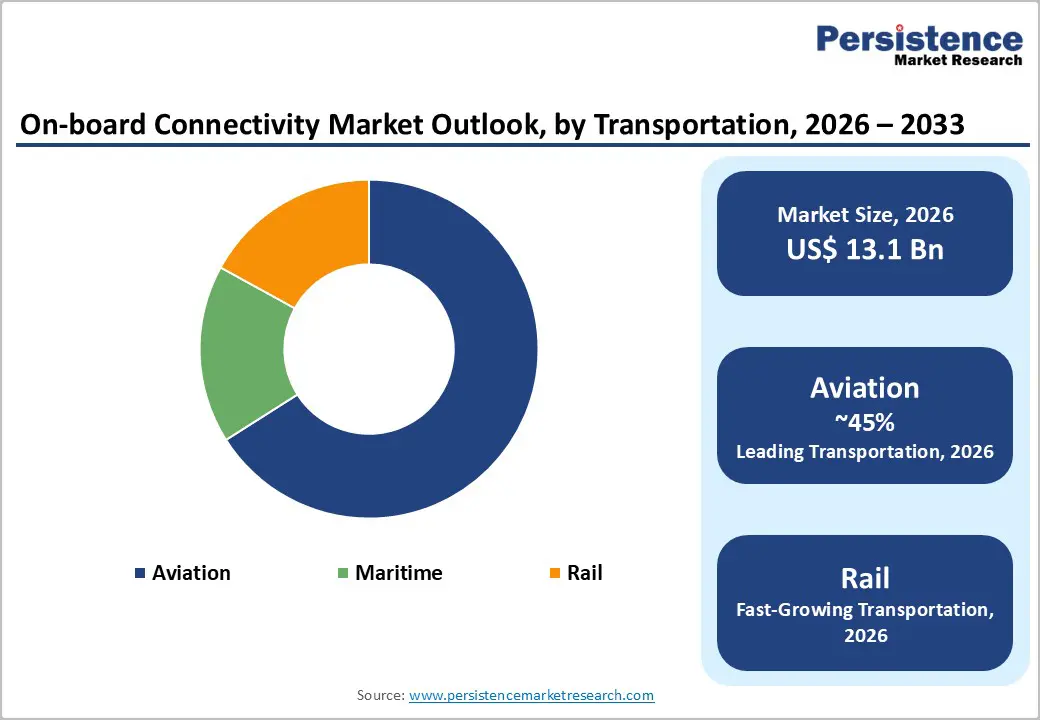

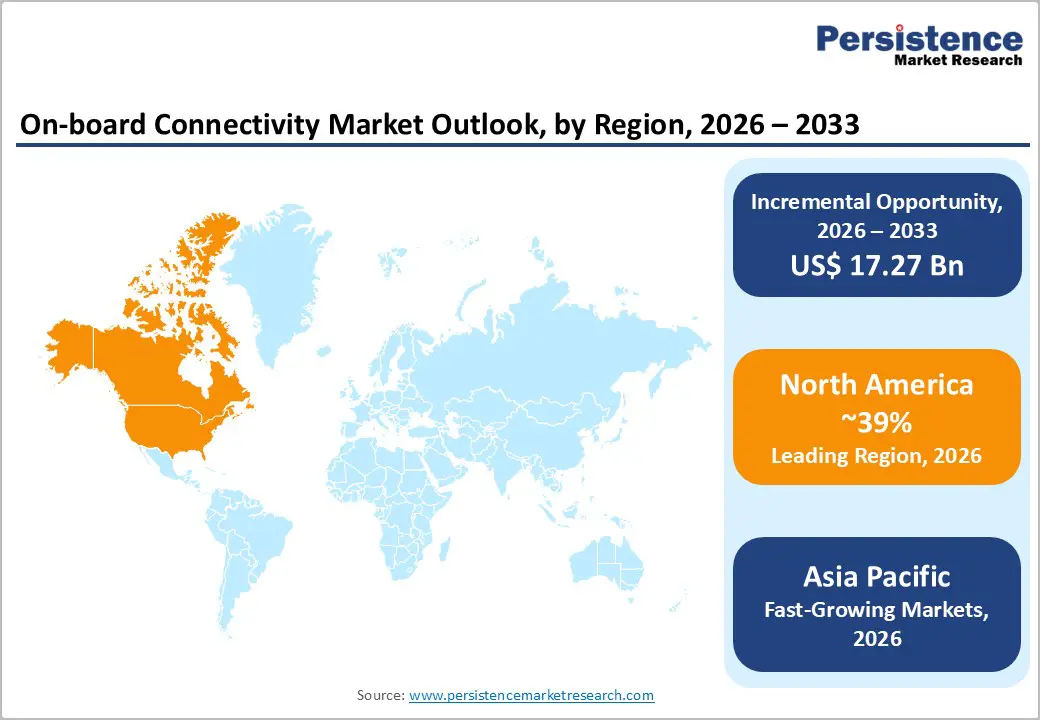

The global on-board connectivity market size is likely to be valued at US$ 13.1 billion in 2026 and is projected to reach US$ 30.3 billion by 2033, growing at a CAGR of 12.8% between 2026 and 2033. The market expansion is fundamentally driven by the accelerating global air travel recovery, the transition toward hybrid satellite architectures combining Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary (GEO) systems, and regulatory mandates for enhanced operational connectivity in aviation and maritime sectors.

Technological advancements in next-generation 5G air-to-ground (ATG) networks, integration of Internet of Things (IoT) for predictive maintenance, and rising passenger demand for seamless broadband experiences during flights are substantially amplifying market growth momentum across commercial and business aviation segments.

Key Market highlights:

- Regional Leader: North America dominates the global on-board connectivity market, commanding approximately 39% market valuation in 2026, driven by mature aviation infrastructure, high passenger connectivity demand, and established 5G ATG networks.

- Fastest Growing Region: Asia-Pacific is positioned to emerge as the fastest-growing region, fueled by explosive air passenger traffic growth exceeding 4.5 billion journeys by 2026, and rapidly expanding aviation infrastructure in China, India, Japan, and Southeast Asian nations.

- Leading Segment: The aviation transportation segment dominates with approximately 66% market share in 2026, driven by premium connectivity and productivity requirements.

- Fastest Growing Segment: Satellite technology grows fastest in Technology, fueled by LEO advancements for global coverage.

- Key Market Opportunities: IoT-enabled predictive maintenance and operational analytics offer significant market expansion opportunities. Connectivity providers and aircraft operators see value in integrating on-board connectivity with real-time health monitoring, fuel efficiency optimization, crew welfare, and passenger experience analytics, creating substantial service revenue beyond traditional subscriptions.

| Key Insights | Details |

|---|---|

|

On-board Connectivity Market Size (2026E) |

US$ 13.1 Bn |

|

Market Value Forecast (2033F) |

US$ 30.3 Bn |

|

Projected Growth CAGR (2026-2033) |

12.8% |

|

Historical Market Growth (2020-2025) |

10.0% |

Market Dynamics

Drivers - Rising Passenger Demand for In-Flight and Onboard Entertainment

The escalating demand for uninterrupted connectivity during travel significantly boosts the On-board Connectivity Market. International organizations report that Asia-Pacific air passenger traffic is expected to exceed 4.5 billion journeys by 2026, with India and China leading demand growth in the region. Airlines are accelerating fleet modernization initiatives to meet passenger expectations for ground-like connectivity experiences, driving substantial investments in Hardware, Software, and Services infrastructure.

Airlines prioritize Wi-Fi and streaming services to enhance experience, mirroring trends in the In-Flight Wi-Fi Services Market. The proliferation of low-cost carriers (LCCs) across emerging markets has intensified competitive pressures, compelling operators to deploy advanced connectivity systems as strategic differentiators. This driver increases ancillary revenues by up to 20% through premium access, as passengers use devices for work and leisure, compelling operators to upgrade systems.

Advancements in IoT and Operational Efficiency

The integration of IoT in transportation fleets is driving market growth by enabling real-time monitoring and predictive maintenance. Intelsat, in partnership with OneWeb, has developed electronically steered antennas that enable seamless switching between GEO satellite capacity and OneWeb's LEO constellation services, resulting in blended connectivity experiences. Additionally, 5G air-to-ground networks are gaining traction, particularly in North America, where Gogo Inc. has completed the pre-provisioning of 300 aircraft and deployed 170 ground towers across the U.S. and Canada in preparation for a network launch in Q4 2025.

The rail and maritime sectors, similar to those in the IoT in Intelligent Transport System market, are utilizing connectivity to improve safety and logistics, effectively reducing downtime by 15-20%. This technological advancement has led to lighter equipment, reduced antenna drag, and lower operational costs, thereby expanding the addressable market for onboard connectivity across various aircraft platforms. Furthermore, government initiatives worldwide are accelerating this adoption, positioning onboard systems as essential for efficient operations.

Restraints - Capital Intensive Infrastructure Investment and Network Deployment Costs

The significant capital investment required for developing satellite constellations, building ground station infrastructure, and retrofitting aircraft continues to hinder market entry in price-sensitive segments and the development of aviation markets. Creating Low Earth Orbit (LEO) satellite constellations requires investments that exceed USD 5 billion, while setting up dedicated 5G Air-to-Ground (ATG) network infrastructure involves deploying hundreds of ground towers equipped with advanced antenna systems.

Airlines operating regional fleets and smaller aircraft often postpone upgrades for connectivity due to low return-on-investment calculations, especially on shorter domestic routes where the demand for high-quality connectivity is limited. These financial challenges disproportionately affect operators in emerging markets, leading to a segmentation in the market where the adoption of premium connectivity is concentrated among established carriers in mature markets like North America and Western Europe.

Cybersecurity, Data Privacy Regulations, and Airspace Restrictions

Stringent regulatory frameworks, including the European GDPR compliance requirements, have created complex data protection obligations for connectivity service providers, particularly for flights originating from or operating within European Union airspace. The EU Directive on Network and Information Security (NIS) establishes baseline cybersecurity standards for telecommunications operators involved in critical aviation infrastructure. This mandates significant investments in security architecture and compliance monitoring systems.

Furthermore, geopolitical tensions and airspace restrictions in conflict-affected regions hinder optimal routing and network coverage. The complexities of regulatory burdens across multiple jurisdictions also prolong deployment timelines for next-generation connectivity technologies. These regulatory constraints significantly affect international carriers operating across various regulatory environments, increasing compliance costs and slowing down the deployment of innovative connectivity solutions.

Opportunity - Expansion of Low-Earth Orbit (LEO) Satellites

The integration of advanced IoT sensors, real-time data analytics, and predictive maintenance platforms across aviation and maritime fleets presents a significant opportunity for market expansion beyond traditional passenger connectivity services. Companies such as Honeywell International Inc., Panasonic Avionics, and Collins Aerospace (a unit of RTX Corporation) have developed sophisticated aircraft health monitoring systems that transmit data via onboard connectivity networks. These systems help reduce unscheduled maintenance events and extend fleet utilization.

Maritime operators are adopting connected systems for vessel tracking, optimizing fuel efficiency, and monitoring crew welfare. Maersk is upgrading 340 of its container ships with Inmarsat Maritime connectivity services to create "floating offices" by 2027. This convergence of connectivity and operational intelligence is expected to generate substantial service revenue opportunities, particularly among enterprise customers who prioritize predictive analytics and digital transformation initiatives.

Growth in High-Speed Rail and Maritime Connectivity

Railway operators around the world are launching extensive digitalization programs that utilize 5G standalone (SA) networks and advanced IoT connectivity for real-time train control, predictive maintenance, and improved passenger information systems. Nokia has introduced commercial 5G radio solutions specifically designed for the Future Railway Mobile Communication System (FRMCS), transitioning global rail networks from the outdated 2G GSM-R to a 5G-based architecture that offers mission-critical reliability.

Regulatory frameworks in the European Union and Asia-Pacific regions are pushing for the modernization of rail infrastructure with advanced connectivity systems, creating a multi-year opportunity for providers of on-board connectivity. For instance, Bangkok's Krung Thep Aphiwat Central Terminal Station has implemented 5G networks that support over 120 cameras, enhancing real-time security and operational efficiency for the hundreds of thousands of passengers it serves daily. The Railway Management Systems are expected to grow rapidly, positioning on-board connectivity as a vital enabling technology for next-generation smart rail operations.

Category-wise Analysis

Component Insights

The Hardware segment is projected to maintain its market dominance with approximately 52% market share by 2026. This growth is driven by the sustained demand for aircraft antennas, satellite modems, radome installations, and advanced electronically-steered antenna (ESA) systems. Hardware solutions are critical for enabling connectivity, as modern Ka-band and Ku-band antenna systems help reduce weight and drag compared to older systems.

The Software segment is expected to experience the fastest growth. This increase is fueled by the rising adoption of cloud-based network optimization platforms, cybersecurity frameworks, and edge computing solutions for real-time data processing. The expansion of these categories is supported by companies like Panasonic Avionics, Thales Group, and Honeywell, which offer diverse solutions spanning integrated hardware, software, and services ecosystems.

Technology Insights

Satellite technology is expected to hold approximately 61% of the market share by 2026, with geostationary (GEO) satellite systems continuing to lead for long-haul and international route coverage due to their established infrastructure and proven reliability. However, low Earth orbit (LEO) satellites are projected to experience the fastest growth. This growth is driven by the deployment of the Starlink constellation in maritime and aviation sectors, along with OneWeb-Intelsat hybrid services and emerging initiatives like Amazon's Project Kuiper.

Air-to-Ground (ATG) technology is anticipated to capture around 26% of the market share, primarily focused on North American markets where terrestrial 5G ATG networks are being implemented. ATG systems offer superior latency characteristics, ranging from 20 to 50 milliseconds, compared to GEO satellites, which have latencies exceeding 500 milliseconds. This makes ATG solutions more suitable for data-intensive applications that require real-time responsiveness. The remaining 13% of the market share consists of emerging hybrid solutions and alternative connectivity methods, including 5G cellular integration and experimental High Altitude Platform Station (HAPS) technologies that are currently undergoing regulatory certification.

Application Insights

Communication applications are projected to account for approximately 54% of the market share by 2026. This segment includes voice services, real-time data exchange, crew communications, and passenger messaging capabilities. The dominance of communication applications highlights their essential role in meeting operational requirements across all modes of transportation, as well as in ensuring safety compliance and adhering to regulatory reporting frameworks.

Entertainment applications are driven by the need for competitive differentiation among airlines and the increasing expectations of passengers for premium in-flight entertainment (IFE) experiences, particularly those that integrate broadband streaming capabilities. Safety and operations applications encompass real-time aircraft diagnostics, collision avoidance systems, weather radar integration, and predictive maintenance alerting. The safety and operations segment is expected to experience accelerated growth as regulatory bodies impose stricter connectivity requirements for autonomous flight systems, advanced air mobility (AAM) operations, and connected vehicle technologies in maritime and rail transportation.

Transportation Insights

Aviation is expected to lead the on-board connectivity market with approximately 66% market share by 2026. This growth is largely due to the mature commercial aviation ecosystem, high passenger traffic volumes, and a well-established infrastructure of connectivity service providers. The growth in commercial aviation is driven by large-scale fleet deployments among major global carriers and competitive advantages through premium connectivity offerings.

The maritime segment is likely to experience accelerated growth as shipping operators shift from GEO satellite services to Low Earth Orbit (LEO) constellation services to improve crew welfare, operational efficiency, and reduce costs. According to Novaspace analysis, the number of VSAT-connected maritime vessels is projected to increase from 105,000 in 2024 to 244,000 by 2034, indicating substantial market expansion. The rail transportation is emerging as the fastest-growing segment, fueled by railway digitalization initiatives, the deployment of the Future Railway Mobile Communication System (FRMCS), and government infrastructure modernization programs across Europe and the Asia Pacific.

Regional Insights

North America On-board Connectivity Market Trends

North America is recognized as the leading market, holding approximately 39% of the global market valuation in 2026. This dominance is supported by its mature aviation infrastructure, high expectations for passenger connectivity, and significant investments from U.S. and Canadian carriers. The region has well-established 5G ATG networks, with Gogo Inc. having completed the deployment of 170 ground towers across the U.S. and Canada, and transitioning legacy ATG systems to LTE technology by early 2026.

Regulatory frameworks established by the Federal Communications Commission (FCC) require network transitions and spectrum optimization, facilitating the industry's adoption of next-generation technologies. North American maritime operators are also swiftly deploying LEO satellite connectivity from Starlink and OneWeb, with shipping companies using hybrid connectivity solutions that seamlessly switch between satellite and 5G cellular networks based on geographic coverage needs.

Europe On-board Connectivity Market Trends

Europe is expected to account for about 28% of the global on-board connectivity market by 2026, driven by strict regulations, a focus on sustainability, and the integration of 5G with 4G systems. The European Aviation Network (EAN), created by Inmarsat, Deutsche Telekom, Thales Group, and Nokia, launched in 2019 and currently supports hundreds of Airbus A320 family aircraft across IAG Group airlines, showcasing an effective hybrid connectivity model.

The EU’s General Data Protection Regulation (GDPR) imposes significant data protection requirements, with penalties up to 4% of annual global turnover for non-compliance. This has prompted investments in secure data systems and cybersecurity by connectivity providers. For example, Air India chose Thales' AVANT Up in-flight entertainment system for a $400 million retrofit covering 40 Boeing 777/787 aircraft and additional Airbus/Boeing deliveries, highlighting European technology's competitive edge in Asia-Pacific.

Asia Pacific On-board Connectivity Market Trends

The Asia-Pacific region is set to become the fastest-growing market, fueled by increased air passenger traffic, expanding aviation infrastructure, and government-led digital initiatives in countries like China, India, Japan, and Southeast Asia. China Mobile and China Southern Airlines are partnering with Airbus on 5G air-to-ground connectivity pilots to enhance broadband for China’s growing aircraft fleet. In India, the aviation sector is booming, with new airports such as Noida International opening in 2025, capable of handling 90 million passengers annually.

Asian maritime operators are accelerating LEO satellite adoption, with Maersk upgrading 340 container vessels to Intelsat Maritime connectivity services, and regional shipping operators increasingly deploying Starlink terminals for crew welfare and operational communications. The Future Railway Mobile Communication System (FRMCS) is also fostering opportunities for integrated rail, air, and maritime connectivity. With smartphone penetration over 76% in the region, younger demographics are increasingly demanding seamless digital experiences during air travel, prompting airlines to invest in enhanced connectivity and entertainment options across all cabin classes.

Competitive Landscape

The on-board connectivity market features a moderately consolidated structure, with major players controlling about 65-70% of the global market value. Key companies like Panasonic Avionics, Thales Group, Honeywell International Inc., Viasat Inc., and Intelsat dominate by integrating hardware, software, and services while maintaining strong customer relationships. These market leaders are pursuing vertical integration by acquiring capabilities such as predictive maintenance, cybersecurity, and edge computing to expand into operational intelligence services. Emerging competitors like Gogo Inc., OneWeb-Eutelsat, and Starlink are disrupting the sector with lower-cost LEO satellite services and innovative 5G air-to-ground technologies.

Key Market Developments

- November 2025: Gogo has begun flight testing its next-generation 5G air-to-ground (ATG) connectivity network for North American customers. The test team is flying 5G ATG hardware installed aboard a Pilatus PC-24 and expects to complete the validation program in 40 to 50 flight hours over several weeks.

- June 2025: Thales Group and Qatar Airways signed a memorandum of agreement establishing a dedicated IFE service and maintenance centre in Doha supporting Qatar Airways' fleet expansion and FlytEDGE platform deployment across A321 NX, A350, A380, and B787 aircraft families.

- December 2024: Honeywell announced the signing of a strategic agreement with Bombardier to provide advanced technology for current and future Bombardier aircraft in avionics, propulsion, and satellite communications technologies.

Top Companies in On-board Connectivity Market

- Panasonic Avionics Corporation (Irvine, U.S.) is positioned as the leading In-Flight Entertainment and Connectivity (IFEC) specialist, operating an integrated ecosystem spanning advanced display systems, broadband connectivity services, digital solutions, and analytics platforms. Panasonic maintains 40-year market leadership in IFE innovation, with strategic partnerships with Japan Airlines, Air Arabia, EVA Air, and emerging-market carriers seeking premium passenger experience differentiation.

- Honeywell International Inc. (Charlotte, U.S.) commands substantial market influence through diversified Anthem avionics integration, a comprehensive JetWave Ka-band satellite communications ecosystem, and strategic partnerships with major aircraft manufacturers, including Bombardier and commercial aviation operators.

- Thales Group (Paris, France) is a leading aerospace and defense technology provider commanding substantial on-board connectivity market share through the AVANT IFE platform, satellite communications expertise, and extensive government and commercial aviation relationships. Thales competitive positioning is strengthened through hybrid ATG-satellite architecture leadership, demonstrated by European Aviation Network deployment, advanced antenna technologies, and strategic partnerships with major airlines, including Qatar Airways, Air India, and IAG Group carriers.

Companies Covered in On-board Connectivity Market

- Panasonic Corporation

- Honeywell International Inc.

- Huawei Technologies Co., Ltd.

- Thales Group

- RTX Corporation

- ALE International

- Bombardier Inc.

- AT&T Inc.

- Gogo Inc.

- Viasat, Inc.

- Rockwell Collins

- Intelsat

- Nokia

- Inmarsat Plc.

Frequently Asked Questions

The global on-board connectivity market is valued at US$ 13.1 billion in 2026 and is projected to reach US$ 30.3 billion by 2033, growing at a 12.8% CAGR, driven by aviation sector expansion, maritime digitalization, and railway infrastructure modernization across global markets.

Key demand drivers include the surge in global air travel, with Asia-Pacific expected to exceed 4.5 billion passenger journeys by 2026, the shift to multi-orbit satellite architectures, regulatory requirements for improved operational connectivity, and the adoption of IoT-enabled predictive maintenance, which opens up significant service revenue opportunities.

Aviation transportation currently dominates the market with approximately 66% market share in 2026, driven by mature infrastructure, high passenger volumes, and established connectivity service provider ecosystems.

North America leads the market with the U.S. maintaining dominance through the FAA's comprehensive regulatory framework, establishing 5G C-Band compatibility requirements, Gogo's launch of a purpose-built aviation 5G network with 250+ upgraded towers, and Viasat's five-fold capacity enhancement supporting generative AI applications.

IoT-enabled predictive maintenance and operational analytics integration represents the most significant opportunity, combining on-board connectivity with real-time aircraft health monitoring, fuel efficiency optimization, crew welfare systems, and passenger analytics, generating substantial service revenues.