- Pharmaceuticals

- Neurodegenerative Diseases Drugs Market

Neurodegenerative Diseases Drugs Market Size, Share, and Growth Forecast 2026 - 2033

Neurodegenerative Diseases Drugs Market by Drug Class (Immunomodulators, Dopamine Agonists, Cholinesterase Inhibitors, N-Methyl-D-Aspartate (NMDA) Receptor Antagonists, Others), Disease Indication (Alzheimer’s Disease, Parkinson’s Disease, Multiple Sclerosis, Amyotrophic Lateral Sclerosis (ALS), Others), Route of Administration (Oral, Injectable, Transdermal, Intrathecal, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Pharmacies, Others), by Regional Analysis, 2026–2033

Neurodegenerative Diseases Drugs Market Size and Trend Analysis

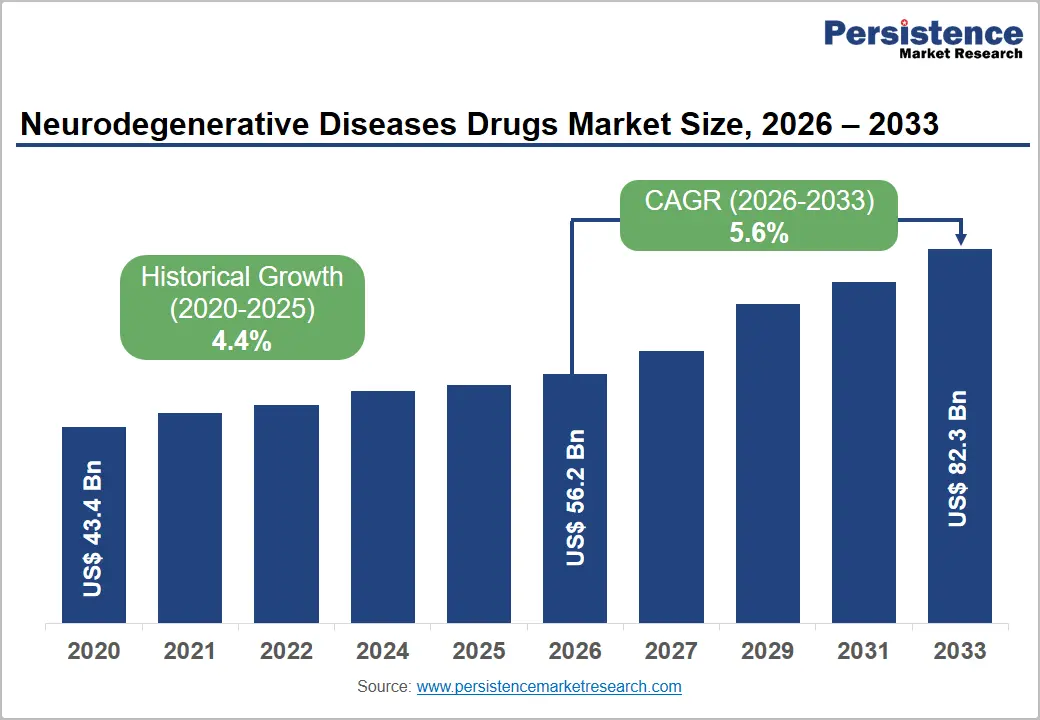

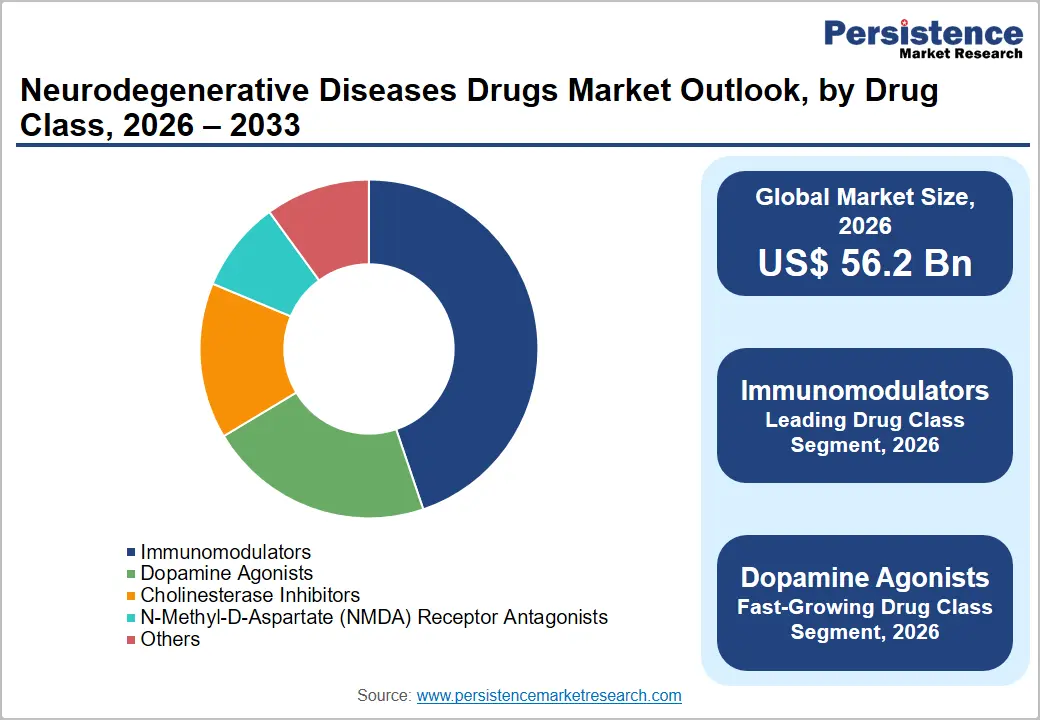

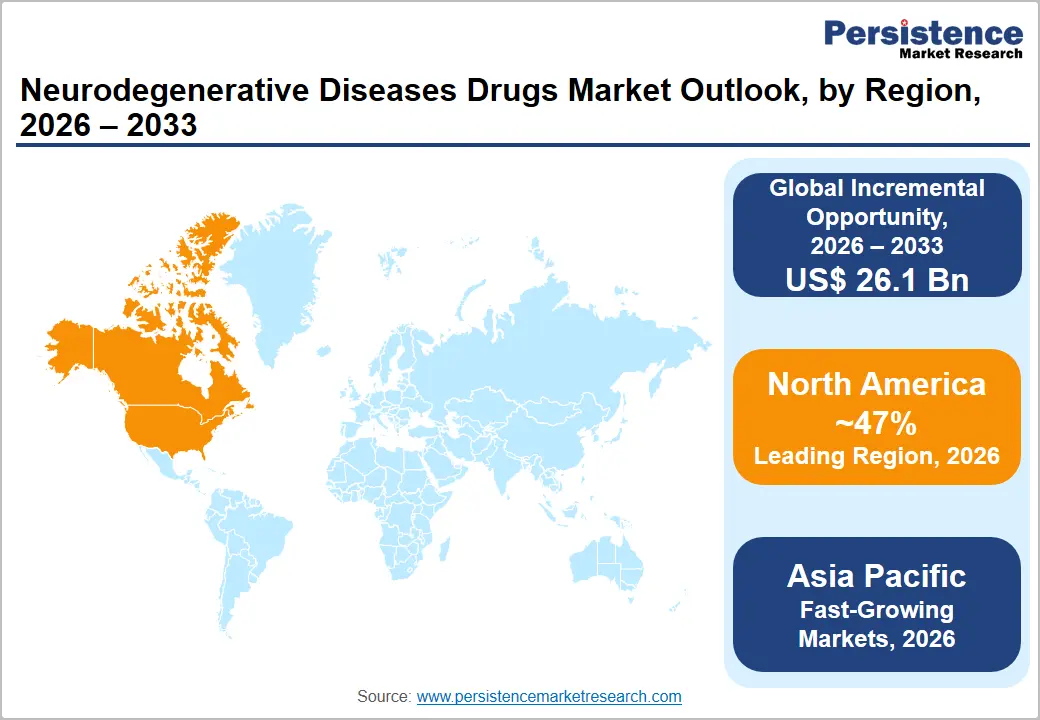

The global neurodegenerative diseases drugs market size is expected to be valued at US$ 56.2 billion in 2026 and projected to reach US$ 82.3 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. This trajectory is driven by the converging forces of rapidly aging global demographics generating structurally expanding neurodegenerative patient populations, breakthrough FDA approvals of disease-modifying therapies for Alzheimer’s disease after decades without approvals, and robust pipeline investment across Parkinson’s, ALS, and multiple sclerosis.

According to the World Health Organization (WHO), neurological disorders are the leading cause of disability-adjusted life years (DALYs) globally, affecting an estimated 3 billion people. The Alzheimer’s Association’s 2024 Alzheimer’s Disease Facts & Figures reports approximately 6.9 million Americans living with Alzheimer’s dementia in 2024 a figure projected to nearly double by 2060 while the FDA’s approval of lecanemab (Leqembi®) and donanemab (Kisunla™) as the first disease-modifying anti-amyloid therapies for early Alzheimer’s has transformed the commercial landscape.

Key Market Highlights

- Leading Region: North America leads the global neurodegenerative diseases drugs market with 47% market share in 2025, anchored by FDA approvals of Leqembi® and Kisunla™ as disease-modifying Alzheimer’s therapies, NIH NIA’s US$ 3.5B+ annual neurodegeneration R&D investment, and the highest density of MS neurology centers globally.

- Fastest Growing Region: Asia Pacific is projected to register the highest CAGR during 2026–2033, driven by China’s NMPA approval of lecanemab (January 2024), Japan’s PMDA early Alzheimer’s approval (September 2023), and rapidly expanding dementia diagnostic infrastructure enabling anti-amyloid therapy eligibility assessment.

- Dominant Segment: Immunomodulators lead the drug class category with 45% market share in 2025, driven by Roche’s Ocrevus® generating ~CHF 4.9B annually and 20+ approved MS DMTs serving a 2.9 million global MS patient population per MSIF data.

- Fastest Growing Segment: Dopamine Agonists represent the fastest growing drug class over 2026–2033, driven by Parkinson’s Foundation’s projection of 1 million U.S. Parkinson’s patients by 2030, AbbVie’s Produodopa™ subcutaneous infusion approval, and pipeline alpha-synuclein immunotherapy programs in advanced clinical development.

- Key Opportunity: Anti-amyloid disease-modifying Alzheimer’s therapies Leqembi® and Kisunla™ address an estimated 6.9 million current U.S. Alzheimer’s patients and 55 million global dementia patients per WHO, representing a multi-decade revenue expansion opportunity worth tens of billions as diagnosis infrastructure and payer coverage scale.

Market Dynamics

Drivers - FDA Approval of Disease-Modifying Alzheimer’s Therapies Transforming Commercial Landscape

The approval of anti-amyloid disease-modifying therapies (DMTs) for Alzheimer’s disease represents the most commercially significant regulatory development in the neurodegenerative diseases drugs market in decades. The U.S. FDA granted traditional approval to Eisai/Biogen’s lecanemab (Leqembi®) in July 2023 and Eli Lilly’s donanemab (Kisunla™) in July 2024 for early symptomatic Alzheimer’s disease, representing the first drugs proven to meaningfully slow cognitive decline by clearing amyloid plaques. The Alzheimer’s Association estimates approximately 6.9 million Americans currently live with Alzheimer’s dementia, projecting this will reach 13.8 million by 2060 absent medical breakthroughs. These approvals have mobilized substantial commercial infrastructure investment including specialized infusion center networks, amyloid PET diagnostic capacity, and ARIA monitoring protocols creating new high-value drug administration channels and diagnostic device demand throughout the ecosystem.

Rapidly Aging Global Population Expanding Neurodegenerative Patient Pool

The accelerating global demographic aging trend is the most fundamental structural driver of neurodegenerative disease drug demand. The United Nations projects the global population aged 60 years and above will reach 2.1 billion by 2050, double the 2020 level, while those aged 80+ will triple to 426 million. Age is the single most significant risk factor for all major neurodegenerative conditions: Alzheimer’s Disease International (ADI) reports that dementia prevalence doubles every 5 years after age 65, while Parkinson’s Foundation data indicates that nearly 90% of Parkinson’s disease cases occur in individuals over 60 years. The Multiple Sclerosis International Federation (MSIF) estimates over 2.9 million people live with MS globally, with diagnosis rates stable but prevalence increasing as improved treatments extend patient survival and quality of life, sustaining long-term drug utilization.

Restraints - Exceptionally High Drug Development Failure Rates and R&D Cost Burden

Neurodegenerative diseases have historically presented the highest clinical trial failure rates across all therapeutic areas. According to research published in Science Translational Medicine, Alzheimer’s drug development experienced a 99.6% clinical trial failure rate between 1998 and 2017 before the recent DMT successes. The cost of bringing a neurodegenerative disease drug to market is estimated by the Tufts Center for the Study of Drug Development at over US$ 2 billion per approved drug on average across all therapeutic areas, and substantially higher for CNS drugs, creating enormous financial risk that constrains small and mid-size company participation and concentrates R&D investment among large pharmaceutical companies with diversified portfolio risk management capabilities.

Drug Pricing Controversy and Reimbursement Barriers for Disease-Modifying Therapies

The high list prices of newly approved disease-modifying Alzheimer’s therapies have generated significant payer and policy scrutiny that is constraining real-world adoption. Leqembi® (lecanemab) was initially priced at US$ 26,500 per year, while Kisunla™ (donanemab) was launched at US$ 32,000 annually. Medicare’s Centers for Medicare & Medicaid Services (CMS) initially imposed restrictive Coverage with Evidence Development (CED) requirements that limited patient access to clinical trial settings, before expanding coverage following traditional FDA approvals. These pricing and coverage tensions moderate near-term patient adoption rates below the epidemiological demand potential.

Opportunities - Dopamine Agonists: Fastest Growing Drug Class Through Parkinson’s Pipeline Expansion

Dopamine agonists represent the fastest growing drug class in the neurodegenerative diseases drugs market, driven by an expanding Parkinson’s disease patient population, pipeline innovation in extended-release and device-aided dopamine delivery platforms, and growing adoption of non-ergot dopamine agonists including pramipexole (Mirapex®), ropinirole (Requip®), and rotigotine (Neupro®) transdermal patch. The Parkinson’s Foundation reports nearly 1 million Americans will be living with Parkinson’s disease by 2030, with global prevalence estimated at 10 million currently per WHO data. Novel dopamine delivery innovations including Abbvie’s Produodopa™ (foslevodopa/foscarbidopa) subcutaneous infusion, Bial’s opicapone (Ongentys®), and pipeline alpha-synuclein-targeting immunotherapy programs are extending treatment options across early, mid-stage, and advanced Parkinson’s disease populations generating sustained high-growth revenue opportunities for companies with established or emerging dopaminergic therapy portfolios.

Category-wise Analysis

Drug Class Insights

Immunomodulators lead the neurodegenerative diseases drugs market by drug class, accounting for approximately 45% share in 2026, driven predominantly by their dominant role in the treatment of Multiple Sclerosis (MS) one of the highest-revenue neurodegenerative indications. MS disease-modifying therapies (DMTs) including natalizumab (Tysabri®), ocrelizumab (Ocrevus®), ofatumumab (Kesimpta®), cladribine (Mavenclad®), and siponimod (Mayzent®) collectively generate multi-billion dollar annual revenues. Roche’s Ocrevus® (ocrelizumab) alone generated approximately CHF 4.9 billion in 2022 globally, making it one of the highest-revenue MS drugs. The Multiple Sclerosis International Federation (MSIF) estimates over 2.9 million people live with MS globally, with the number of approved DMTs exceeding 20 in the U.S. and Europe a dense competitive landscape generating high-volume immunomodulator procurement that anchors the drug class’s dominant revenue position.

Disease Indication Analysis

Alzheimer’s disease is likely to represent the leading disease indication segment in the neurodegenerative diseases drugs market in 2026, commanding the largest share of revenues driven by both the massive global patient population and the transformative commercial implications of the first approved disease-modifying therapies. The Alzheimer’s Association’s 2024 Facts & Figures report estimates approximately 6.9 million Americans age 65 and older are living with Alzheimer’s dementia, with total U.S. healthcare and long-term care costs for dementia patients estimated at US$ 360 billion in 2024. The WHO estimates over 55 million people globally have dementia, with Alzheimer’s disease accounting for 60–70% of cases. The commercial potential of Leqembi® and Kisunla™ to address the disease-modifying treatment gap historically limited to symptomatic agents like cholinesterase inhibitors and memantine positions Alzheimer’s as the highest near-term revenue growth catalyst across all neurodegenerative indications.

Distribution Channel Analysis

Specialty pharmacies is likely to represent the leading distribution channel for neurodegenerative diseases drugs in 2026, particularly for high-cost disease-modifying therapies for MS, Alzheimer’s, and Parkinson’s disease that require specialized dispensing, patient support programs, and cold chain logistics. MS DMTs including Ocrevus®, Tysabri®, Kesimpta®, and the newly approved anti-amyloid Alzheimer’s therapies are exclusively distributed through FDA-designated Risk Evaluation and Mitigation Strategies (REMS) programs or specialty pharmacy networks that provide mandatory patient monitoring support. CVS Specialty, Walgreens Specialty Pharmacy, and Accredo (Evernorth) are the dominant specialty pharmacy networks managing neurodegenerative drug dispensing in the U.S. The channel’s growth is further reinforced by payer mandates directing high-cost specialty drugs to preferred specialty pharmacy networks as a condition of reimbursement.

Regional Insights

North America Neurodegenerative Diseases Drugs Market Trends and Insights

North America is likely to account for approximately 47.2% of the global neurodegenerative diseases drugs market in 2026, supported by rapid commercialization of anti-amyloid Alzheimer’s therapies, strong Medicare reimbursement mechanisms, and substantial public research investment through the National Institutes of Health. The region benefits from advanced neurology specialty centers, widespread biomarker-based diagnostics, and a high concentration of leading drug developers. The U.S. Food and Drug Administration approval of Leqembi and Kisunla has significantly expanded the commercial outlook for disease-modifying Alzheimer’s therapies. Multiple sclerosis and Parkinson’s disease continue to generate strong prescription volumes across specialty neurology networks, infusion centers, and integrated academic health systems throughout the region.

U.S. Neurodegenerative Diseases Drugs Market Trends and Insights

The United States is poised for nearly 88.4% of the North American market in 2026, driven by FDA regulatory acceleration pathways, extensive Medicare Part B and Part D coverage, and the world’s largest Alzheimer’s and multiple sclerosis treatment infrastructure. NIH allocates more than US$ 3.6 billion annually to Alzheimer’s research, supporting continued innovation in neuroinflammation, tau, and genetic-targeted therapeutics. More than 6.9 million Americans are living with Alzheimer’s disease, creating substantial long-term demand for both symptomatic and disease-modifying drugs.

Canada Neurodegenerative Diseases Drugs Market Trends and Insights

Canada is likely to contribute around 9.1% of the regional market in 2026 and is projected to reach a CAGR of 7.8%. Provincial reimbursement systems, increasing dementia prevalence, and expanded access to biologics through academic neurology centers in Toronto, Montreal, and Vancouver contributes to growth. National dementia strategies and public drug funding programs are improving diagnosis rates and accelerating uptake of innovative neurological therapies.

Europe Neurodegenerative Diseases Drugs Market Trends and Insights

Europe is likely to capture approximately 28.6% of the global market in 2026, supported by mature reimbursement systems, strong multiple sclerosis treatment adoption, and centralized approvals through the European Medicines Agency. Market expansion is driven by high treatment penetration in Western Europe and increasing use of monoclonal antibodies for Alzheimer’s disease. National health technology assessment bodies such as NICE, G-BA, and HAS play a critical role in determining commercial uptake and pricing. Continued growth is expected as countries broaden access to innovative neurology therapies and invest in dementia diagnostics, digital monitoring, and specialty memory clinic networks.

Germany Neurodegenerative Diseases Drugs Market Trends and Insights

Germany is poised for 24.8% of the European market in 2026. Strong statutory health insurance coverage, a robust neurology specialist base, and early adoption of premium biologics such as Ocrevus and Kesimpta sustain the country’s leadership in multiple sclerosis and Alzheimer’s therapeutics. University hospitals and certified MS centers continue to drive rapid integration of newly approved neurodegenerative therapies.

UK Neurodegenerative Diseases Drugs Market Trends and Insights

UK is likely to represent 18.5% of the regional market in 2026 and is expected to expand at a CAGR of 7.4%. Initiatives by the National Institute for Health and Care Excellence, reimbursement scenarios and NHS-led expansion of memory clinics and neurological care pathways contribute to awareness. Government dementia strategies are also increasing investment in early diagnosis and access to advanced biologic therapies.

Asia Pacific Neurodegenerative Diseases Drugs Market Trends and Insights

Asia Pacific held approximately 18.9% of the global neurodegenerative diseases drugs market in 2025 and is projected to register the fastest CAGR of 9.8% in the coming years. Growth is fueled by large aging populations, rising dementia and Parkinson’s prevalence, and broader reimbursement of innovative therapies. Regulatory approvals by China’s NMPA and Japan’s PMDA have accelerated access to anti-amyloid treatments. Investments in neurology specialty centers, amyloid PET imaging, and cognitive screening infrastructure are substantially improving treatment uptake across the region.

China Neurodegenerative Diseases Drugs Market Trends and Insights

China accounted for nearly 41.7% of the Asia Pacific in 2026, supported by more than 15 million Alzheimer’s patients and early approval of Leqembi. Ongoing National Reimbursement Drug List negotiations are expected to improve affordability and significantly broaden adoption of advanced neurodegenerative therapies. Domestic biotechnology firms are also accelerating the development of locally manufactured monoclonal antibodies and neuroprotective drugs.

Japan Neurodegenerative Diseases Drugs Market Trends and Insights

Japan represented around 27.6% of the regional market in 2025. Rapid population aging, PMDA approvals, and national dementia initiatives under the New Orange Plan continue to strengthen demand for Alzheimer’s and Parkinson’s disease drugs, with forecast growth of 8.6% CAGR through 2033. Universal healthcare reimbursement and advanced diagnostic infrastructure support early and sustained treatment adoption across the country.

Competitive Landscape

The global neurodegenerative diseases drugs market is moderately consolidated in established therapy segments, with Biogen, Eisai Co., Eli Lilly, Roche/Genentech, Novartis, AbbVie, and AstraZeneca commanding dominant combined revenues across MS, Alzheimer’s, and Parkinson’s indication categories. Key competitive differentiators include disease-modifying versus symptomatic mechanism positioning, oral versus injectable formulation preference, REMS program management capability, and real-world evidence generation for HTA submissions. Emerging strategies include combination therapy development, tau-targeting antibody programs, and gene therapy platforms for ALS and rare neurodegenerative disorders targeting precision medicine patient subpopulations.

Key Developments:

- In May 2026, Oligomerix announced the successful completion of its Phase 1a clinical trial evaluating OLX-07010, the company’s lead small-molecule candidate designed to inhibit tau aggregation for the treatment of rare neurodegenerative disorders and Alzheimer’s disease.

- In May 2026, Shanghai Fosun Pharmaceutical and AriBio entered into an exclusive global option agreement covering the development, regulatory approval, manufacturing, and commercialization of AR1001, an investigational therapy for the treatment of Alzheimer’s disease.

- In January 2026, Insilico Medicine received U.S. Food and Drug Administration Investigational New Drug (IND) clearance for ISM8969, an AI-enabled NLRP3 inhibitor being developed as a potential best-in-class therapy for neuroinflammatory and neurodegenerative disorders.

- In July 2025, Klotho Neurosciences bagged the FDA Orphan Drug Designation for KLTO-202, it unique secreted-Klotho promoter gene therapy for treating Amyotrophic Lateral Sclerosis (ALS). The designation provides key benefits, including 7 years of market exclusivity, GDUFA User Fee waivers, and tax credits for clinical trials.

Global Neurodegenerative Diseases Drugs Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 43.4 Bn |

|

Current Market Value (2026) |

US$ 56.2 Bn |

|

Projected Market Value (2033) |

US$ 82.3 Bn |

|

CAGR (2026-2033) |

5.6% |

|

Leading Region |

North America, 47% share |

|

Dominant Disease Indication |

Multiple Sclerosis, 41.3% share |

|

Top-ranking Drug Class |

Immunomodulators, 44.8% |

|

Incremental Opportunity |

US$ 26.1Bn |

Companies Covered in Neurodegenerative Diseases Drugs Market

- MIMEDX Group, Inc.

- BioTissue, Inc.

- Organogenesis Holdings Inc.

- Integra LifeSciences Holdings Corporation

- MTF Biologics

- Amnio Technology, LLC

- Applied Biologics, LLC

- Tides Medical

- NuVision Biotherapies, LLC

- Amniox Medical, Inc.

- Skye Biologics Holdings, LLC

- Human Regenerative Technologies, LLC

- Celularity Inc.

- Axogen Corporation

- Sanara MedTech Inc.

- Others

Frequently Asked Questions

The global neurodegenerative diseases drugs market is projected to be valued at US$ 56.2 billion in 2026, driven by FDA approvals of Leqembi® (lecanemab) and Kisunla™ (donanemab) as first disease-modifying Alzheimer’s therapies, the Alzheimer’s Association’s documented 6.9 million U.S. Alzheimer’s patients, WHO’s 55 million global dementia estimates, and the expanding MS immunomodulator market with 20+ approved DMTs globally.

Rising global prevalence of Alzheimer’s, Parkinson’s, and multiple sclerosis, expanding approvals of disease-modifying therapies, and increasing healthcare spending on aging populations are the primary demand drivers for the neurodegenerative diseases drugs market.

North America leads with approximately 47% market share in 2025, anchored by FDA approvals of Leqembi® and Kisunla™ for early Alzheimer’s disease, NIH NIA’s US$ 3.5B+ annual neurodegeneration research investment, CMS Medicare Part B/D reimbursement for infused and oral neurodegenerative therapies, and commercial leadership of Biogen, Eisai, Eli Lilly, Roche/Genentech, and Novartis.

The key growth opportunity lies in the development and commercialization of disease-modifying therapies targeting amyloid, tau, alpha-synuclein, and neuroinflammation, particularly in emerging markets with improving diagnostic and reimbursement infrastructure.

Key players include Biogen Inc., Eisai Co. Ltd. (Leqembi®), Eli Lilly and Company (Kisunla™), Roche/Genentech (Ocrevus®), Novartis AG (Kesimpta®), AbbVie Inc. (Produodopa™), AstraZeneca plc, Bristol Myers Squibb, Sanofi SA, UCB S.A., Merck KGaA, Bial Portela (Ongentys®), Lundbeck A/S, Acadia Pharmaceuticals Inc., and Cerevel Therapeutics (acquired by AbbVie), among others.