- Healthcare Services

- Nap Pod Market

Nap Pod Market Size, Trends, Share, and Growth Forecast, 2026 – 2033

Nap Pod Market by Product Type (Single Nap Pods, Double Nap Pods, Multiple Nap Pods, Compact Nap Pods), Application (Corporate Offices, Airports & Transit Hubs, Hospital Facilities, Education Institutions, Others), End-User (Commercial Users, Residential, Others), and Regional Analysis for 2026-2033

Nap Pod Market Share and Trends Analysis

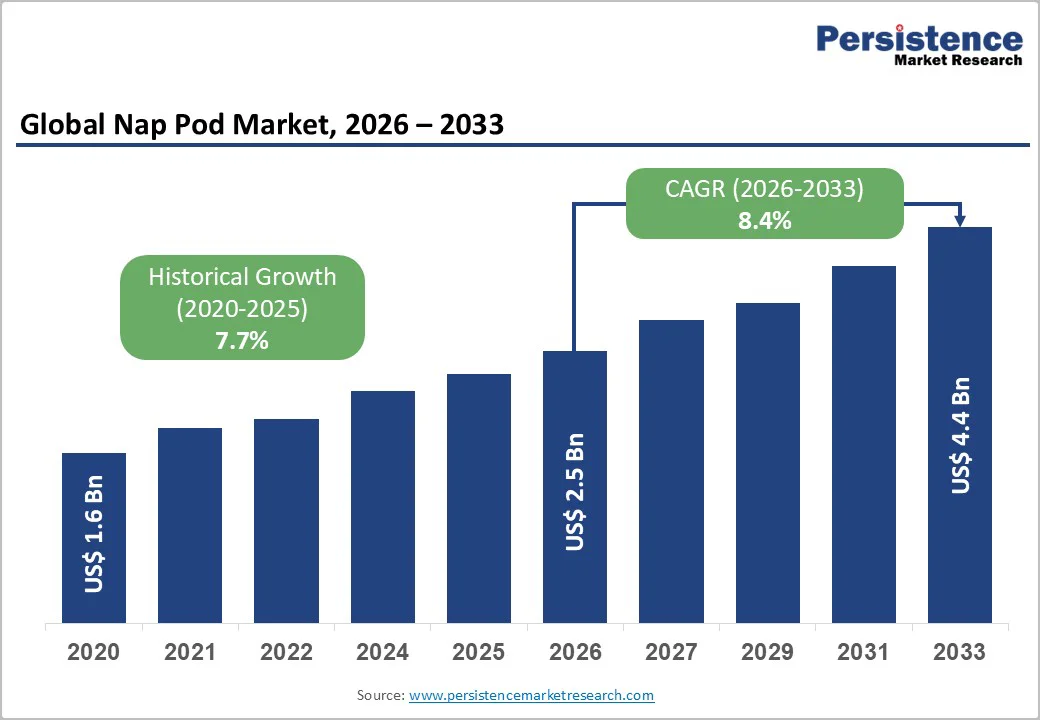

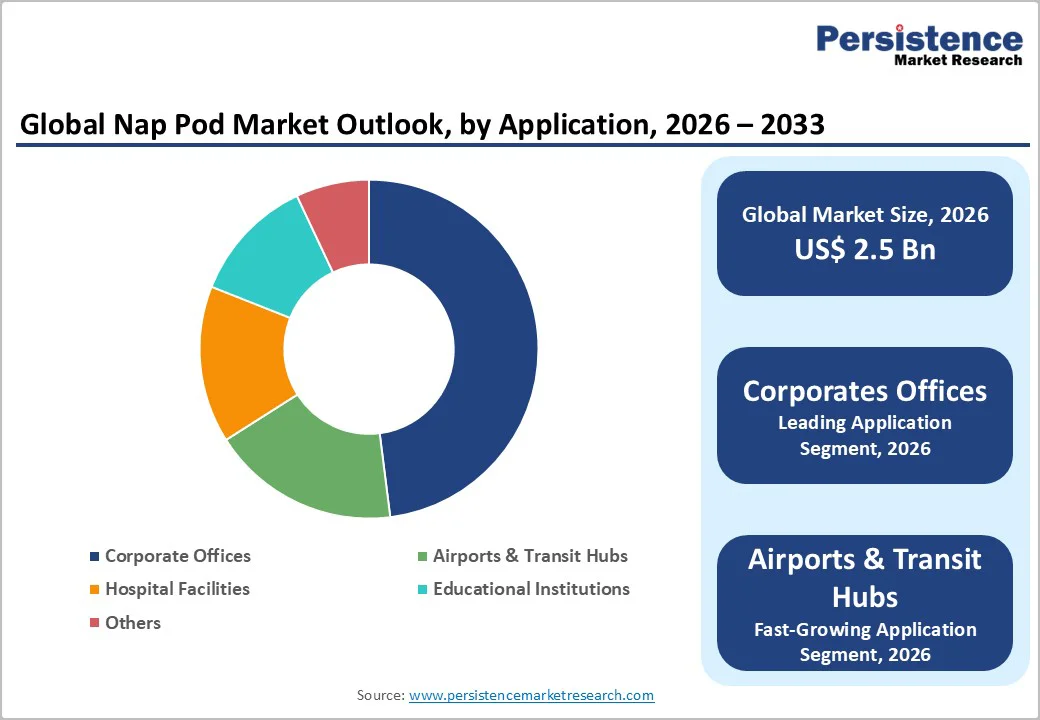

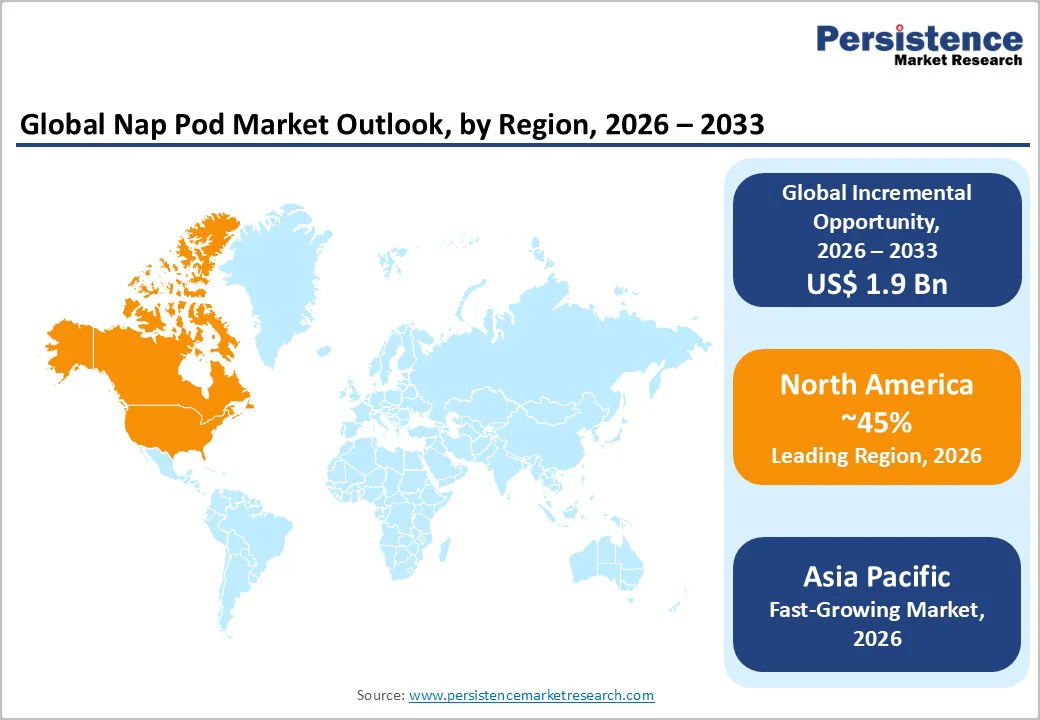

The global nap pod market size is likely to be valued at US$ 2.5 billion in 2026 and is estimated to reach US$ 4.4 billion by 2033, growing at a CAGR of 8.4% during the forecast period 2026−2033. This trajectory indicates that nap pods are evolving from niche wellness amenities into more mainstream infrastructure for corporate offices, airports, universities, and healthcare facilities. Demand is further supported by the rapid expansion of workplace wellness programs, growing use of fatigue-management solutions in transportation hubs, and rising hospital investments in patient-recovery and staff-rest infrastructure. These trends align with a broader institutional focus on reducing burnout, improving safety, and quantifying the return on investment from well-rested employees and patients. Market growth is further reinforced by urban workforce expansion and management’s emphasis on productivity enhancement, encouraging organizations to treat nap pods as part of a wider human capital strategy rather than as discretionary perks.

Key Industry Highlights

- Dominant Region: North America is projected to lead in 2026 with an estimated 45% market share, driven by corporate wellness culture, high workforce density, and advanced office infrastructure.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing market through 2033, fueled by high-speed urbanization, corporate expansion, and growing wellness awareness.

- Leading Application: Corporate offices are projected to hold a 48% market revenue share in 2026, owing to employee wellness initiatives and deep productivity focus.

- Fastest-growing Application: Airports and transit hubs are expected to grow the fastest from 2026 to 2033, driven by rising international travel and strong passenger demand for rest solutions.

- August 2025: Visakhapatnam Railway Station launched the East Coast Railway zone's first sleeping pod facility, featuring 73 single pods, 15 double pods, and 18 women-only pods with Wi-Fi, hot water, and snacks.

| Report Attribute | Details |

|---|---|

|

Nap Pod Market Size (2026E) |

US$ 2.5 Bn |

|

Market Value Forecast (2033F) |

US$ 4.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Workplace Wellness Mandates to Fuel Nap Pod Market Growth

Workplace wellness mandates are strengthening demand for nap pods as enterprises formalize employee-wellbeing requirements. Regulations and organizational policies increasingly emphasize fatigue risk management, mental recovery, and measurable productivity outcomes. Short rest cycles improve cognitive clarity, decision-making quality, and employee engagement, prompting companies to integrate structured rest infrastructure into their wellness frameworks. Nap pods provide controlled, hygienic, private micro-rest environments that align with compliance standards and support workforce performance targets. One organizational study reported a 13% productivity loss linked to employee fatigue, reinforcing the financial rationale for structured rest solutions.

Mandates are also influencing long-term workplace design strategies. Modern offices are shifting toward holistic wellbeing zones that embed rest, focus, and recovery spaces as strategic productivity enhancers. Nap pods fit these design priorities by offering scalable, tech-enabled units that reduce downtime during high-pressure work cycles. Companies aiming for talent retention, environmental, social, & governance (ESG) alignment, and employer-branding differentiation view nap pods as tangible evidence of welfare commitments. As wellness compliance moves from optional to expected, nap pods transition from a discretionary amenity to a functional requirement in forward-looking corporate environments.

Prohibitive Costs to Stall Market Expansion

High initial costs remain a core restraint due to the capital-intensive nature of pod construction, technology integration, and space preparation. Each unit typically requires durable materials, ergonomic engineering, noise-control insulation, ventilation systems, and optional smart capabilities such as occupancy sensors or ambient environment controls. These elements elevate the manufacturing expense per unit, leading to premium price points that challenge budget-sensitive buyers. Installation adds further financial weight, as organizations must allocate dedicated floor space, electrical fittings, safety compliance, and sometimes structural modifications, all contributing to higher upfront investment thresholds.

Affordability also becomes a limiting factor for small enterprises, public institutions, and emerging markets where expenditure on employee wellness infrastructure faces strict prioritization. Buyers often evaluate the return on investment over long periods, making the adoption cycle slower. The procurement decision involves cost justification, internal approvals, and ongoing maintenance planning, which lengthens deployment timelines. High entry prices ultimately restrict broader market outreach, especially in sectors testing new workplace wellness models or operating within constrained funding environments.

Technological Innovations and Smart Integrations to Unlock New Opportunities

Technological innovations and smart integrations represent a significant opportunity due to the evolving expectations of modern users who prioritize efficiency, comfort, and personalized experiences. Advanced features such as climate control, noise cancellation, biometric sleep tracking, and connectivity with mobile applications transform traditional resting spaces into intelligent wellness hubs. These enhancements allow users to optimize their rest based on real-time data, improving productivity and overall well-being. The integration of smart sensors and AI-driven adjustments enables pods to adapt automatically to user preferences, creating a highly tailored and seamless experience. This shift aligns with the growing demand for solutions that support both physical and mental rejuvenation within professional and high-traffic environments.

Smart capabilities also open avenues for businesses to differentiate their offerings and capture high-value clientele. Enterprises can leverage data-driven insights from pod usage to optimize space allocation, enhance service quality, and design targeted wellness programs. Interactive features and app-based controls elevate user engagement and satisfaction, encouraging repeat utilization and brand loyalty. Investments in cutting-edge technology establish a competitive advantage, allowing organizations to position themselves as innovators in workplace wellness and public comfort solutions, while driving operational efficiency and long-term growth potential.

Category-wise Analysis

Product Type Insights

Single nap pods are projected to hold the largest share of the market, estimated at around 42% in 2026, driven by extensive use across corporate offices, airports, and healthcare facilities. Their cost efficiency, compact footprint, and customizable features make them ideal for high-traffic environments. Organizations favor single pods due to simplified installation, easier compliance management, and consistent user experience. The balance of functionality, affordability, and operational convenience positions them as a preferred choice, sustaining strong demand and reinforcing their status as the leading segment.

Compact nap pods are expected to experience the fastest growth over the 2026-2033 period due to the increasing demand for space optimization in co-working spaces, universities, and small offices. Their lower installation cost, modular design, and flexibility appeal to cost-sensitive buyers and emerging markets. These pods allow efficient utilization of limited space while providing comfortable and private resting solutions. Growing awareness of employee wellness and productivity benefits further supports adoption, positioning compact nap pods as a rapidly expanding segment with significant potential across diverse sectors.

Application Insights

Corporate offices are projected to account for approximately 48% of the nap pod market revenue share in 2026, due to the deepening focus on employee wellness and productivity. Organizations are investing in rest infrastructure to reduce burnout, improve mental health, and enhance overall performance. Technology and finance sectors, characterized by high work intensity and extended operating hours, are leading adopters. The implementation of nap pods enables firms to attract and retain talent while fostering a supportive work environment, establishing corporate offices as the dominant end-use segment in the market.

Airports and transit hubs are anticipated to experience the fastest growth through 2033, driven by rising international travel and increasing passenger expectations for convenient rest options. Integration of nap pods with digital booking and scheduling systems enhances accessibility and utilization, particularly in major airports across Europe, North America, and Asia. These facilities offer travelers privacy, comfort, and short-term rest opportunities during layovers or delays. Growing demand from airlines and transit operators for premium passenger experiences further accelerates adoption, positioning airports and transit hubs as a rapidly expanding segment with high growth potential.

End-User Insights

Commercial users are projected to hold approximately 60% market share in 2026, establishing them as the leading segment. Businesses, hospitals, and corporate offices drive demand through business-to-business (B2B) sales, leveraging economies of scale to deploy multiple units efficiently. The segment benefits from structured procurement processes, standardized installations, and higher utilization rates across workplaces. Commercial adoption is fueled by organizational focus on employee wellness, productivity enhancement, and operational efficiency, positioning this segment as the dominant contributor to market revenue.

The residential segment is expected to experience the fastest growth, driven by the increasing focus on home wellness and remote work trends. Investments in compact nap pods for personal spaces are creating substantial opportunities. Rising consumer spending on health and well-being, with a significant portion of home wellness budgets allocated toward rest solutions, supports adoption. Flexibility, affordability, and ease of installation make residential pods appealing to individuals seeking comfort and productivity enhancements, positioning this segment for rapid expansion across emerging and mature markets.

Regional Insights

North America Nap Pod Market Trends

North America is projected to dominate with an estimated 45% of the nap pod market share in 2026. The region’s leadership is underpinned by a convergence of corporate wellness culture, high workforce density in urban centers, and significant investments in employee productivity solutions. Large-scale enterprises in technology, finance, and healthcare sectors are early adopters of nap pods, leveraging them as strategic tools to reduce burnout, increase retention, and enhance operational efficiency. The prevalence of sophisticated office infrastructures allows seamless integration of nap pods without disrupting workflow, while advanced real estate solutions in metropolitan areas facilitate optimal space utilization. This structured adoption, combined with a high emphasis on ergonomic design, digital integration, and user-centered customization, positions North America as the most mature and lucrative market for nap pod deployment.

A key driver of dominance lies in the alignment of wellness initiatives with measurable business outcomes across the U.S. and Canada. Companies track employee engagement, productivity metrics, and absenteeism reductions linked to rest facilities, reinforcing the strategic value of nap pods beyond comfort. High consumer and organizational awareness of sleep science, coupled with supportive regulatory frameworks and standards for workplace health, creates a favorable ecosystem for sustained growth. In addition, strong purchasing power and access to cutting-edge manufacturing technologies ensure that North America maintains a competitive advantage in both commercial and emerging residential segments, solidifying its position as the leading market.

Europe Nap Pod Market Trends

Europe represents a significant and steadily growing market for nap pods, characterized by high adoption in corporate offices, airports, and public institutions. The region benefits from a strong focus on employee well-being, progressive workplace policies, and widespread awareness of productivity and mental health initiatives. Organizations prioritize creating restorative environments to support work-life balance, reduce stress, and enhance performance, driving the deployment of nap pods across diverse industries such as finance, technology, healthcare, and education.

Key drivers for the Europe market include advanced infrastructure, high urban workforce density, and supportive regulatory frameworks that encourage wellness-oriented workplace investments. Airports and transit hubs in major European cities are integrating nap pods to improve passenger experience, while universities and coworking spaces adopt them to enhance focus and efficiency. Sustainability and ergonomic design trends also influence product selection, with organizations favoring energy-efficient and compact solutions. These factors, combined with rising demand for smart and digitally integrated pods, ensure Europe remains a strategically important market for nap pods, with consistent growth potential and increasing adoption across both commercial and emerging residential applications.

Asia Pacific Nap Pod Market Trends

Asia Pacific is anticipated to be the fastest-growing regional nap pod market between 2026 and 2033, driven by rapid urbanization, increasing corporate expansion, and evolving workplace culture. The region is experiencing a surge in co-working spaces, airports, educational institutions, and healthcare facilities, creating significant demand for rest infrastructure. Companies are increasingly recognizing the impact of employee wellness on productivity, leading to the adoption of innovative solutions such as nap pods. Rising awareness of mental health, coupled with competitive work environments, encourages businesses to implement rest-focused amenities to attract and retain talent.

Key factors supporting growth include increasing disposable income, expanding urban office infrastructure, and government initiatives promoting workplace well-being. The flexibility of compact and modular nap pods aligns with space constraints in densely populated cities, making them highly practical for both commercial and educational settings. Some of the region’s largest economies present untapped opportunities for residential adoption, as remote work trends and home wellness awareness gain traction. Technological integration, affordability, and rising investment in employee-centric facilities position Asia Pacific as a high-growth market with considerable potential for expansion across multiple sectors.

Competitive Landscape

The global nap pod market structure exhibits moderate fragmentation, comprising specialized manufacturers, wellness-tech companies, and contract furniture suppliers. Leading players are estimated to hold 35% of the market, leveraging brand recognition, distribution networks, and advanced design capabilities. Emerging regional firms capture specialized segments, targeting specific industries or localized needs. Market dynamics are shaped by innovation, with companies emphasizing ergonomics, comfort, and intelligent features to differentiate their offerings and enhance user experience.

Competition also revolves around pricing strategies, product customization, and design flexibility. Manufacturers are increasingly developing compact, modular pods suitable for constrained spaces and integrating digital technologies such as app control, smart sensors, and environmental adjustments. These strategies support adoption across commercial, residential, and institutional segments, fostering growth and diversification in the market.

Key Industry Developments

- In November 2025, Guernsey's Caritas homeless charity received planning permission to install two emergency sleeping pods at its St Peter Port site to provide immediate shelter for rough sleepers during winter. The pods, each accommodating two people with heating and power, address rising homelessness amid housing shortages and aim to support recovery without replacing long-term solutions.

- In May 2025, the University of New Mexico introduced nap pods at Zimmerman Library, providing students with convenient spaces to rest and recharge. The initiative aims to support student well-being and improve focus during study sessions.

- In March 2025, a new pod hotel opened in New Delhi, offering travelers compact and comfortable resting spaces within the airport. The facility is designed to provide privacy and convenience for passengers during layovers and delays, enhancing the overall travel experience.

Companies Covered in Nap Pod Market

- MetroNaps

- Sleepbox

- GoSleep

- NapCabs GmbH

- SnoozeCube

- MinuteSuites

- 9 Hours

- Pod Time

- Nap Pods Ltd

- Restworks

- Dream Pods

- LoungePods

- Energypods

Frequently Asked Questions

The global nap pod market is projected to reach US$ 2.5 billion in 2026.

Rising demand for employee wellness, productivity enhancement, space-efficient rest solutions, and growing adoption of sleeping pods in corporate, healthcare, and travel sectors are driving the market.

The market is poised to witness a CAGR of 8.4% from 2026 to 2033.

Key market opportunities lie in innovations in the form of smart-technology integrations, compact and modular designs, and expanding adoption of nap pods in residential, commercial, and travel sectors.

Some of the key market players include MetroNaps, Sleepbox, GoSleep, NapCabs GmbH, SnoozeCube, MinuteSuites, and 9 Hours.