- Advanced Materials

- Nanocatalysts Market

Nanocatalysts Market Size, Share, and Growth Forecast 2026 - 2033

Nanocatalysts Market by Product Type (Metal Oxides, Non-Metal Oxides, Carbon Nanotubes (CNTs), Carbon Black, Nanoparticles, Nanoclays, Nanofibers, Nanocomposites), Power Type (Carbon-Based, Metal-Based, Metal & Non-metal Oxides, Polymeric Nanomaterials, Composite / Hybrid Nanomaterials, Ceramic-Based Nanomaterials), Industry, and Regional Analysis, 2026 - 2033

Nanocatalysts Market Size and Trend Analysis

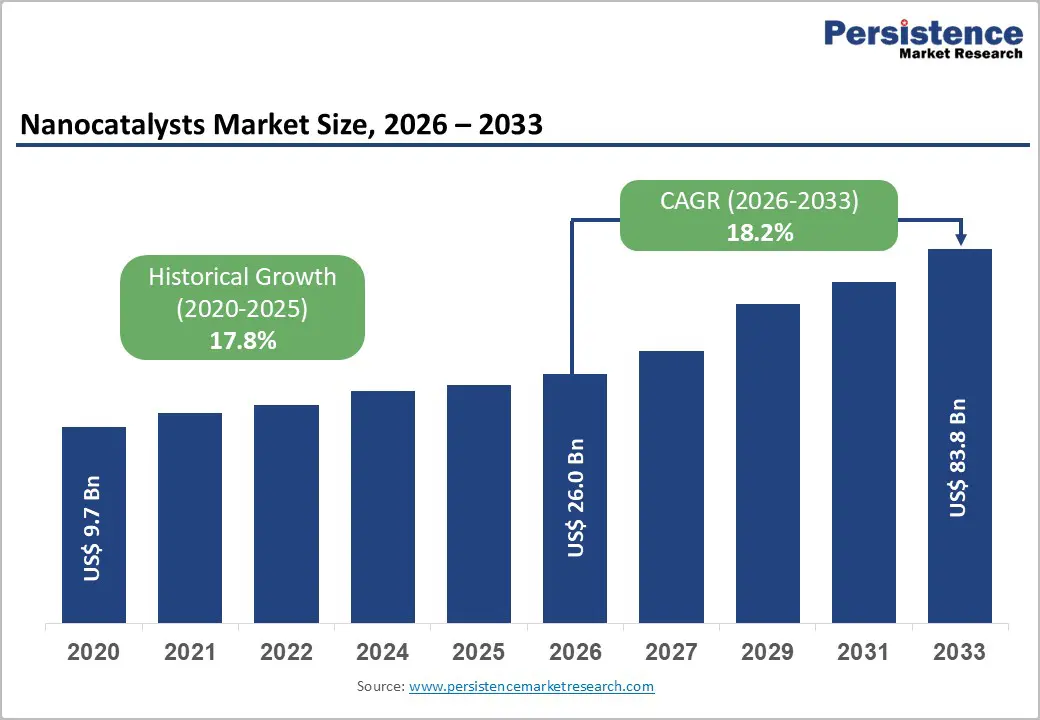

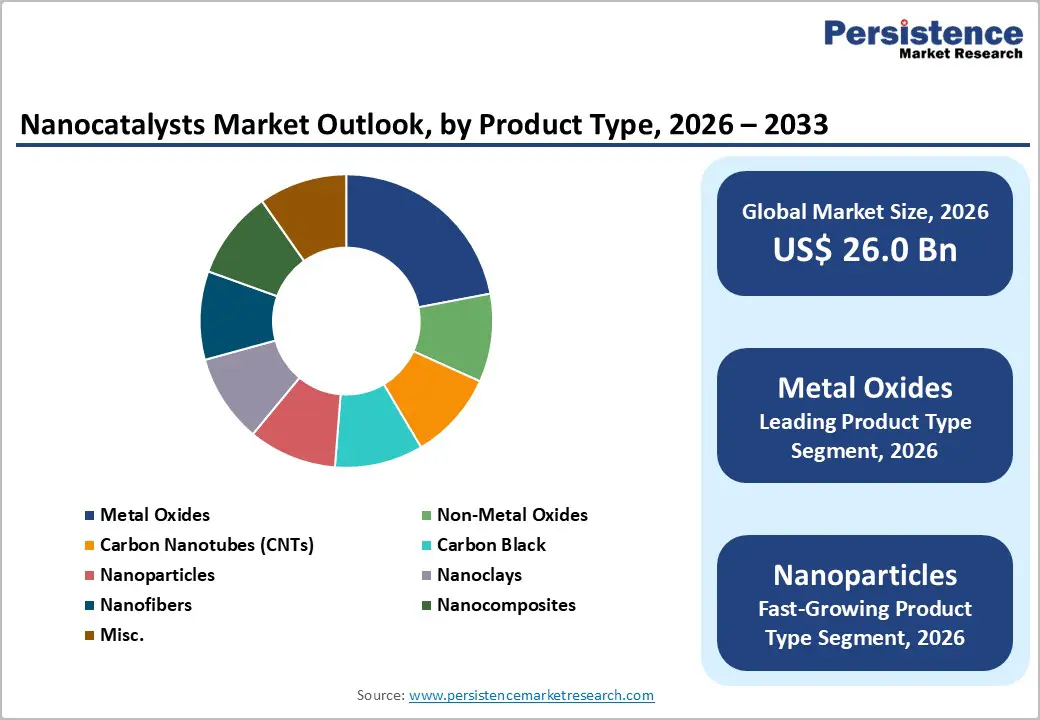

The global nanocatalysts market size is expected to be valued at US$ 26.0 billion in 2026 and projected to reach US$ 83.8 billion by 2033, growing at a CAGR of 18.2% between 2026 and 2033.

Accelerated demand for sustainable catalysis in energy and chemical fuels this expansion. Nanocatalysts provide superior surface area (up to 1000 m²/g), enhanced reactivity, and high selectivity, enabling up to 30% energy savings in chemical reactions.

Growing adoption in hydrogen production, emission control, and advanced chemical synthesis further supports growth. Global net-zero initiatives, along with stringent environmental regulations, are accelerating the shift toward cleaner and more efficient catalytic technologies across industries.

Key Industry Highlights:

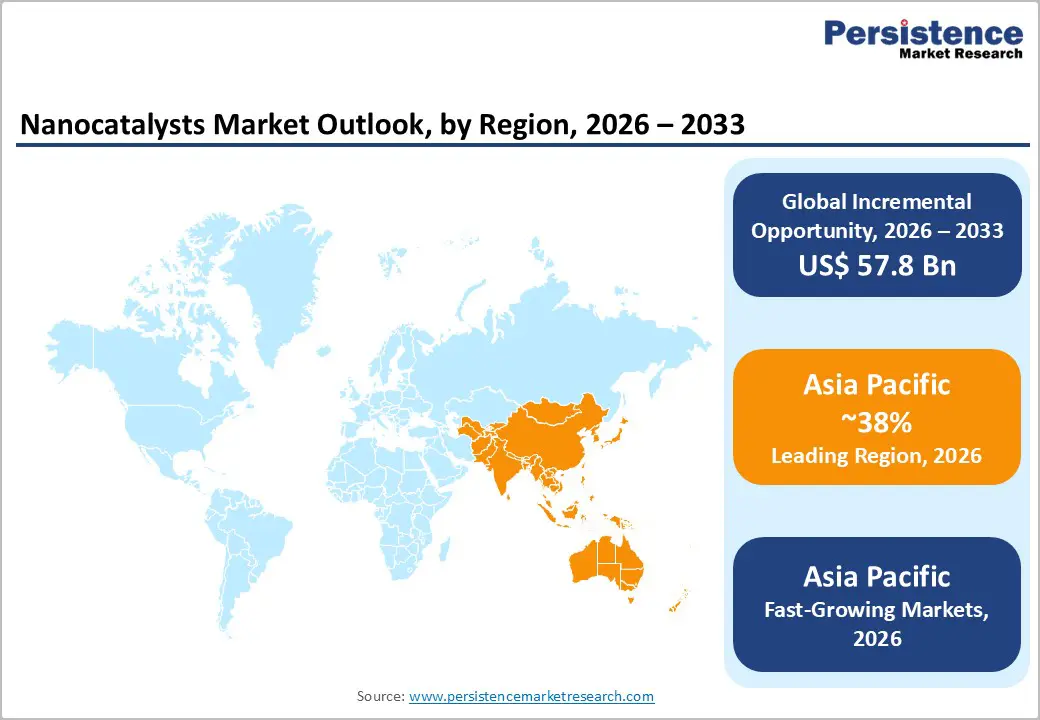

- Leading Region: Asia Pacific leads the market with a 38% share in 2025, driven by strong manufacturing growth and supportive government policies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a 20.1% CAGR (2025 - 2032), fueled by China and India’s energy and industrial expansion.

- Leading Product Category: Metal Oxides dominate with a 35% share in 2025, due to their high stability and use in refining and fuel cells.

- Fastest Growing End-Use Category: The Energy & Power segment is the fastest-growing, driven by hydrogen adoption and clean energy demand.

- Key Market Opportunity: Green hydrogen expansion, supported by large-scale electrolyzer deployments, is creating strong demand for advanced nanocatalysts.

| Key Insights | Details |

|---|---|

| Nanocatalysts Size (2026E) | US$ 26.0 billion |

| Market Value Forecast (2033F) | US$ 83.8 billion |

| Projected Growth CAGR (2026 - 2033) | 18.2% |

| Historical Market Growth (2020 - 2025) | 17.8% |

Market Dynamics

Drivers - Rapid Adoption of Nanocatalysts in Renewable Energy Applications

Nanocatalysts are accelerating advancements in renewable energy technologies by significantly improving reaction efficiency in fuel cells and water electrolysis. According to IEA projections, global electrolyzer capacity is expected to reach 80 GW by 2030, where nanocatalysts such as metal oxides can reduce platinum usage by up to 80%, lowering overall costs. Their high surface area and enhanced catalytic activity improve hydrogen generation efficiency and support scalable clean energy solutions.

Additionally, nanocatalysts enhance refining processes by increasing output yields by 10-15% while reducing carbon emissions. This aligns with global net-zero commitments and stricter environmental regulations. Their ability to optimize energy conversion and reduce reliance on scarce metals makes them crucial for hydrogen economy development and electric mobility, positioning the market for strong long-term growth across renewable energy and industrial sectors.

Superior Efficiency Driving Adoption in Chemical Manufacturing

Nanocatalysts are transforming chemical synthesis by enabling higher reactivity, selectivity, and process efficiency across industries. In pharmaceutical manufacturing, they achieve up to 99% reaction selectivity, minimizing waste and improving product purity while reducing energy consumption by nearly 30%. Their ability to facilitate precise reactions is driving adoption in complex synthesis processes and high-value chemical production.

Furthermore, nanocatalysts enhance operational efficiency in petrochemical and industrial applications. Materials like carbon nanotubes extend catalyst lifespan and reduce downtime, improving productivity and lowering maintenance costs. As industries aim to increase throughput and optimize energy use, nanocatalysts are becoming essential in high-performance manufacturing systems, supporting sustainable production and encouraging continuous investment in advanced catalytic technologies across global chemical sectors.

Restraints - High Production Costs and Limited Industrial Scalability Challenges

Nanocatalysts face significant restraints due to their high manufacturing costs, which can be 5-10 times greater than conventional catalysts. The complex synthesis methods, requiring precise control over particle size, morphology, and composition, increase production expenses and limit large-scale commercialization. Additionally, fluctuations in raw material prices, often ranging between 15-20%, further add to cost uncertainty and affect profitability for manufacturers.

Despite strong research advancements, only about 20% of lab-scale nanocatalyst innovations successfully transition to industrial applications. This gap highlights challenges in scaling up production while maintaining performance consistency. The high capital investment required for specialized equipment and controlled environments also restricts adoption, particularly in emerging markets, thereby slowing the overall growth potential of the nanocatalysts industry.

Stringent Regulations and Health Concerns Limiting Adoption

Regulatory frameworks and safety concerns present major barriers to the widespread adoption of nanocatalysts. Agencies such as ECHA and OSHA enforce strict testing and certification requirements to evaluate environmental and human health impacts, often extending approval timelines by 12-18 months. These regulatory processes also increase compliance costs by approximately 25%, adding financial pressure on manufacturers.

Concerns over nanoparticle toxicity and potential environmental risks have led to tighter usage restrictions, with exposure limits being significantly more stringent than conventional materials. These uncertainties slow down commercialization and limit application scope, particularly in sensitive industries such as healthcare and consumer goods. As a result, companies must invest heavily in safety validation and compliance, delaying product launches and restraining market expansion.

Opportunities - Expanding Role of Nanocatalysts in Hydrogen Economy Growth

The rapid scale-up of hydrogen production presents a significant opportunity for the nanocatalysts market. Global investments in electrolyzer infrastructure, including large-scale hydrogen hubs, are driving demand for advanced catalytic materials that enhance efficiency and reduce reliance on precious metals. Non-PGM nanocatalysts are gaining traction due to their ability to deliver high efficiency levels, reaching up to 80% in electrochemical reactions, while significantly lowering costs.

Government initiatives and funding programs are further accelerating adoption, particularly in the energy and power sector. China’s aggressive hydrogen development plans and similar policies worldwide are expanding the application scope of nanocatalysts. As hydrogen emerges as a key pillar in clean energy transition, nanocatalysts will play a critical role in improving performance, scalability, and sustainability of electrolyzer technologies, creating long-term growth opportunities.

Growing Pharmaceutical Innovation Driving Biocatalysis Adoption

The expanding pharmaceutical industry is creating substantial opportunities for nanocatalysts, particularly in biocatalysis and advanced synthesis processes. With global pharmaceutical output projected to reach multi-trillion-dollar levels, there is increasing demand for efficient, high-precision catalytic solutions. Nanocatalysts enable over 99% selectivity in chiral synthesis, improving drug purity while reducing waste generation by up to 40%, making them highly valuable in drug manufacturing.

Regulatory support, including fast-track approvals for efficient and sustainable processes, is further encouraging adoption. In Europe, the rise of Pharma 4.0 is driving the use of advanced materials such as polymeric and hybrid nanocatalysts in continuous manufacturing systems. These advancements are improving productivity, reducing environmental impact, and enabling innovation in complex drug formulations, thereby strengthening the long-term growth prospects of nanocatalysts in the pharmaceutical sector.

Category-wise Analysis

Product Type Insights

Metal oxides dominate the nanocatalysts market, accounting for approximately 35% share in 2025, driven by their exceptional stability, durability, and wide applicability in industrial and energy processes. These materials are extensively used in fuel cells, where they demonstrate operational lifespans exceeding 5,000 hours, supported by data from leading energy research initiatives. Titanium dioxide (TiO2) further enhances this segment, offering 20-30% higher photocatalytic activity, making it highly effective in environmental and chemical applications.

Nanoparticles and nanocomposites are among the fastest-growing product categories, supported by their superior tunability and high surface area. Their ability to be engineered for specific reactions enables greater efficiency and selectivity across pharmaceuticals, energy storage, and environmental applications. Continuous advancements in nanofabrication techniques and increasing demand for multifunctional catalysts are accelerating adoption across diverse industries, driving long-term growth in this segment.

Power Type Insights

Carbon-based nanomaterials lead the nanocatalysts market, capturing around 28% share in 2025, primarily due to their high electrical conductivity, large surface area (up to 1000 m²/g), and excellent chemical stability. These properties make them highly suitable for energy storage, fuel cells, and catalytic reactions. Their integration into battery systems has been shown to improve efficiency by up to 15%, aligning with the rapid expansion of electric vehicle adoption and renewable energy systems.

Composite and hybrid nanomaterials are emerging as the fastest-growing category, driven by their ability to combine multiple material advantages into a single system. These advanced materials offer enhanced catalytic activity, improved durability, and better resistance to harsh operating conditions. Their growing use in hydrogen production, advanced manufacturing, and environmental catalysis is fueling strong adoption, as industries seek high-performance and cost-efficient catalytic solutions.

Industry Insights

The energy and power sector holds the largest share of around 32% in 2025, driven by increasing demand for clean energy solutions and efficient catalytic processes. Nanocatalysts are widely used in hydrogen production, fuel cells, and energy conversion systems, where they can achieve efficiency levels of up to 60% in hydrogen-related applications. The strong push toward decarbonization and renewable energy adoption continues to support the dominance of this segment.

The chemical and materials industry is emerging as the fastest-growing end-use segment, driven by rising demand for high-efficiency synthesis processes and specialty chemicals. Nanocatalysts enable improved reaction control, reduced waste, and lower energy consumption, making them highly valuable in advanced manufacturing. Increasing investment in sustainable chemical production and process optimization is accelerating their adoption, positioning this segment for significant long-term expansion across global markets.

Regional Insights

North America Nanocatalysts Market Trends and Insights

North America holds a significant position in the nanocatalysts market, accounting for around 30% share in 2025, supported by strong research infrastructure and advanced industrial applications. The United States leads the region with substantial investments such as US$1.2 billion in DOE funding (2024), focusing on hydrogen technologies and clean energy innovations. National labs like PNNL are driving breakthroughs in nanocatalyst design and performance.

Additionally, robust regulatory frameworks from agencies like the EPA and FDA ensure safe and efficient deployment across industries. The region also contributes nearly 25% of global patents, reflecting its leadership in innovation. Strong demand from pharmaceuticals, automotive, and energy sectors continues to drive growth, making North America a critical hub for high-value nanocatalyst applications and technological advancements.

Europe Nanocatalysts Market Trends and Insights

Europe plays a vital role in the nanocatalysts market, driven by stringent environmental regulations and strong policy support for sustainable technologies. The region is witnessing steady expansion, with a projected CAGR of approximately 8.1% through the forecast period. Frameworks such as REACH ensure strict chemical safety standards, while Horizon Europe provides over €1 billion in funding for advanced materials and nanotechnology research.

Countries like Germany are leading in automotive applications, where nanocatalysts help achieve up to 90% NOx emission reductions. The European Green Deal aims to cut emissions by 50% by 2030, further boosting demand for clean catalytic technologies. Increasing adoption in hydrogen, automotive, and industrial sectors is positioning Europe as a key market for sustainable nanocatalyst innovations.

Asia Pacific Nanocatalysts Market Trends and Insights

Asia Pacific dominates the nanocatalysts market, accounting for approximately 38% share in 2025, driven by rapid industrialization, strong manufacturing ecosystems, and large-scale investments in energy and chemical sectors. China leads with initiatives like Made in China 2025, focusing on advanced materials and solar efficiency improvements of up to 22%. Japan’s METI-backed programs and India’s national missions further strengthen R&D and commercialization.

The region is also the fastest-growing market, supported by a ~20.1% CAGR during 2025 - 2032. Expanding applications in renewable energy, electronics, and automotive sectors are fueling demand. Increasing government support, coupled with rising focus on hydrogen production and clean technologies, is accelerating adoption of nanocatalysts across Asia Pacific, positioning it as the global growth hub for advanced catalytic solutions.

Competitive Landscape

The nanocatalysts market is moderately consolidated, with leading players focusing heavily on research and development to maintain technological leadership. A significant number of patents have been filed globally, reflecting intense innovation in catalyst design, material engineering, and performance optimization. Companies are increasingly investing in advanced nanostructuring techniques to enhance efficiency, durability, and selectivity across applications such as energy, chemicals, and environmental remediation.

Strategic collaborations and joint ventures, particularly in Asia, are shaping the competitive dynamics of the market. Manufacturers are also leveraging artificial intelligence and computational modeling to accelerate catalyst discovery and reduce development time. Continuous innovation, coupled with partnerships and technological integration, is becoming a key strategy for gaining competitive advantage in this rapidly evolving and highly innovation-driven market.

Key Developments:

- In September 2024, Heraeus acquired Arora Matthey to strengthen its catalyst portfolio and expand its capabilities in advanced materials. The acquisition enhances Heraeus’ position in nanocatalyst development, supporting applications across chemical processing, energy, and industrial catalysis while improving its global footprint and innovation capacity.

- In March 2025, BASF launched a new high-efficiency metal oxide catalyst designed for ammonia production. The innovation focuses on improving reaction efficiency and reducing energy consumption, supporting sustainable chemical manufacturing and aligning with growing demand for low-emission industrial processes worldwide.

- In July 2024, Johnson Matthey announced a US$50 million hydrogen-focused project supported by the U.S. Department of Energy. The initiative aims to advance nanocatalyst technologies for hydrogen production, strengthening clean energy development and accelerating the transition toward low-carbon fuel solutions.

Companies Covered in Nanocatalysts Market

- Strem Chemicals, Inc.

- American Elements

- Cabot Corporation

- LG Chem

- OCSiAl

- Evonik Industries

- Arkema

- US Research Nanomaterials, Inc.

- Nanocomposix, Inc.

- Nanoshel LLC

- SkySpring Nanomaterials, Inc.

- Nanophase Technologies Corporation

- Cytodiagnostics, Inc.

- Quantum Materials Corp.

- Inframat Advanced Materials

Frequently Asked Questions

The nanocatalysts market size is valued at US$ 26.0 billion in 2026, supported by strong demand from the energy and chemical sectors.

Demand is driven by clean energy transition and improved reaction efficiency, offering up to 30% energy savings in industrial processes.

Asia Pacific leads with a 38% share in 2025, increasing from 37.2% in 2024, driven by strong industrial and policy support.

The key opportunity lies in hydrogen expansion, supported by 80 GW electrolyzer capacity, boosting advanced catalyst demand.

Major players include BASF, Johnson Matthey, Umicore, and Heraeus, focusing on innovation and advanced material development.