- Hardware & Software IT Services

- Multi-Vendor Support Services Market

Multi-Vendor Support Services Market Size, Share, and Growth Forecast 2026 - 2033

Multi-Vendor Support Services Market by Service Type (Hardware, Software), Enterprise (Large Enterprises, Small and Medium Enterprises), Delivery Model (Onsite, Remote, Hybrid), Industry Vertical (IT & Telecom, BFSI, Healthcare, Manufacturing, Retail & E-commerce, Government & Public Sector), and Regional Analysis, 2026 - 2033

Multi-Vendor Support Services Market Size and Trend Analysis

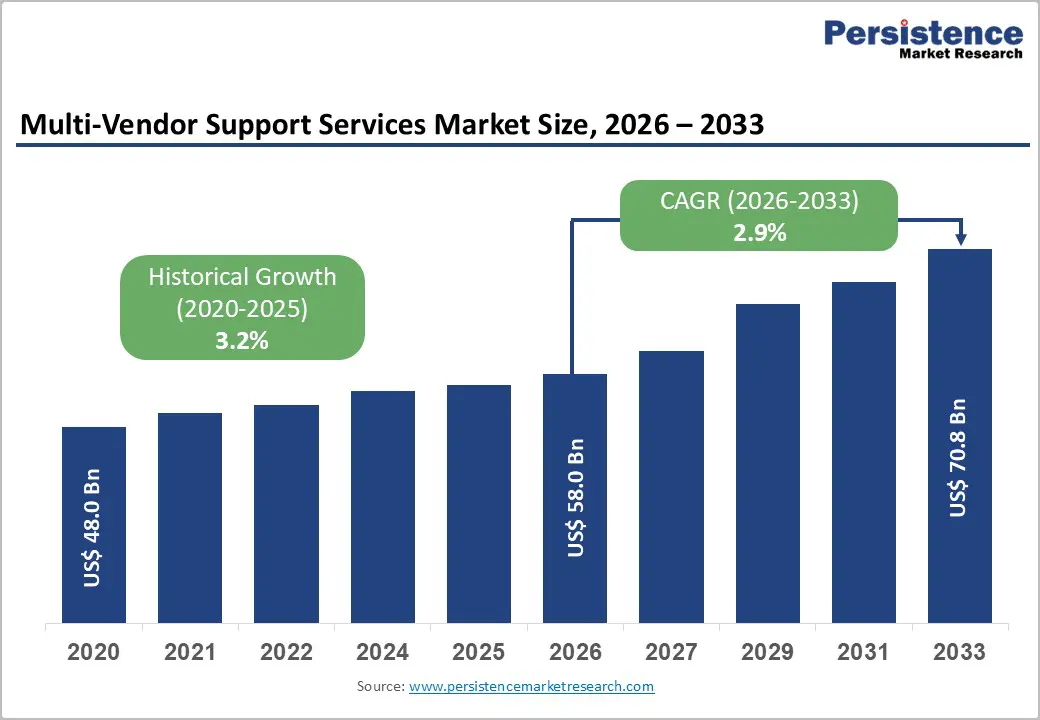

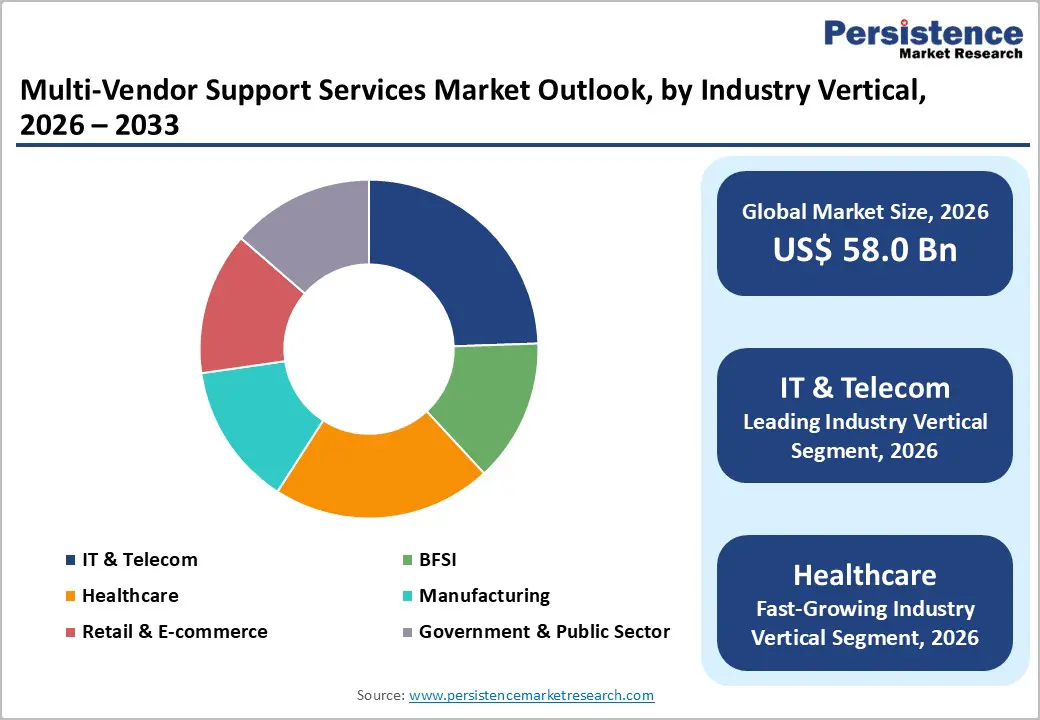

The global multi-vendor support services market size is expected to be valued at US$ 58.0 billion in 2026 and projected to reach US$ 70.8 billion by 2033, growing at a CAGR of 2.9% between 2026 and 2033.

Enterprises increasingly adopt multi-vendor strategies to integrate best-of-breed technologies across their IT environments, creating a need for centralized support services. Organizations now operate complex infrastructures that combine hardware, software, storage, and networking solutions from multiple vendors such as Cisco Systems and Hewlett Packard. Managing these heterogeneous systems requires unified maintenance, monitoring, and lifecycle services to ensure reliability. The growing shift toward hybrid cloud and distributed IT architectures further strengthens demand for vendor-agnostic support solutions that improve operational efficiency and system uptime.

Key Industry Highlights:

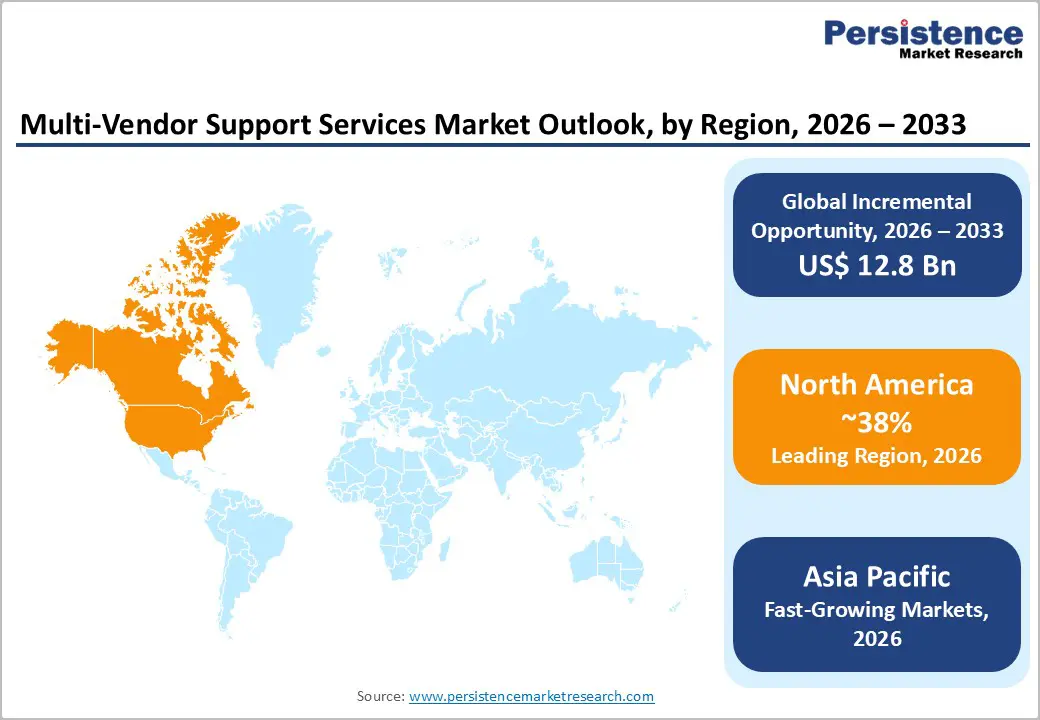

- Leading Region: North America leads the Multi-Vendor Support Services Market with 38% share in 2025, supported by the strong enterprise IT ecosystem in the United States.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rapid digital transformation and IT infrastructure expansion across China, India, and Japan.

- Leading Service Type: Hardware Support dominates with 62% share in 2025, supported by extensive maintenance needs for enterprise servers, storage, and networking infrastructure.

- Leading Enterprise: Large Enterprises hold 68% share in 2025, as organizations with complex multi-vendor IT environments rely heavily on integrated support services.

- Key Market Opportunity: Increasing adoption of AI-driven predictive maintenance is creating new opportunities by enabling proactive monitoring and improving reliability across multi-vendor IT environments.

| Global Market Attributes | Key Insights |

|---|---|

| Multi-Vendor : Services Size (2026E) | US$ 58.0 billion |

| Market Value Forecast (2033F) | US$ 70.8 billion |

| Projected Growth CAGR (2026 - 2033) | 2.9% |

| Historical Market Growth (2020 - 2025) | 3.2% |

Market Dynamics

Drivers - Rising Complexity of Multi-Vendor IT Environments is Driving Demand for Centralized and Integrated Support Services

Modern enterprises increasingly operate heterogeneous IT infrastructures composed of hardware, storage, and networking equipment from multiple vendors. For example, organizations may deploy servers from Dell Technologies, storage systems from NetApp, and networking solutions from Cisco Systems. Managing such mixed ecosystems often creates interoperability challenges, fragmented support contracts, and operational inefficiencies that strain internal IT teams.

Multi-vendor support services address these issues by providing centralized management, troubleshooting, and lifecycle maintenance across diverse technologies. A unified support framework helps enterprises streamline incident resolution, reduce downtime, and improve overall system reliability. As organizations continue integrating specialized technologies from different providers, the need for vendor-agnostic expertise and coordinated maintenance solutions continues to strengthen across enterprise IT environments.

Expansion of Cloud, Hybrid Infrastructure, and Edge Computing Increasing the Need for Vendor-Agnostic Technical Support

The rapid growth of cloud computing and hybrid IT infrastructure has significantly increased the complexity of enterprise technology environments. Businesses commonly operate workloads across public cloud platforms such as Amazon Web Services and Microsoft Azure while maintaining on-premises systems and private cloud environments. This combination creates interconnected systems that require consistent monitoring and coordinated technical support.

Edge computing deployments further intensify these requirements as organizations process data closer to devices and distributed locations. Multi-vendor support providers deliver integrated monitoring, predictive maintenance, and cross-platform troubleshooting to maintain performance across cloud, edge, and on-premises systems. As digital transformation initiatives expand globally, enterprises increasingly rely on unified support services to maintain operational continuity across complex IT ecosystems.

Restraints - Cybersecurity Regulations and Compliance Requirements Increasing Complexity of Multi-Vendor Support Management

Strict cybersecurity regulations and data protection requirements make it challenging for enterprises to manage multi-vendor IT ecosystems. Frameworks such as General Data Protection Regulation and Digital Operational Resilience Act require organizations to maintain consistent security policies, monitoring systems, and reporting standards across different vendors and technologies.

Ensuring compliance across diverse platforms often demands additional security audits, specialized expertise, and unified governance frameworks. Enterprises must coordinate multiple service providers while maintaining strict data protection standards, which can increase operational complexity and administrative workloads. These compliance pressures sometimes slow the adoption of multi-vendor support services as organizations evaluate risks, responsibilities, and regulatory obligations across interconnected IT environments.

High Initial Integration and Deployment Costs Limiting Adoption Among Budget-Constrained Organizations

Implementing multi-vendor support frameworks requires significant upfront investments in integration, system mapping, and infrastructure assessment. Organizations must align diverse hardware, software, and network components from vendors such as Dell Technologies, NetApp, and Cisco Systems to ensure seamless support coverage and service-level coordination.

These integration efforts often involve infrastructure audits, system migrations, and configuration adjustments that increase deployment costs and extend implementation timelines. Small and medium enterprises may face greater financial constraints when adopting such solutions, as limited IT budgets and resource availability can make the transition more challenging. Consequently, the financial and operational burden of initial setup can slow the pace of adoption in certain organizations.

Opportunity - Rapid Digital Transformation in Emerging Economies Creating New Growth Avenues for Multi-Vendor Support Providers

Rapid digitalization across emerging economies is generating strong demand for integrated IT support services. Countries such as India are expanding enterprise IT infrastructure through initiatives such as Make in India, encouraging investments in data centers, cloud platforms, and advanced networking systems. Businesses across industries are increasingly adopting digital technologies to enhance productivity and competitiveness.

As organizations deploy diverse hardware, software, and cloud platforms, the complexity of managing multi-vendor ecosystems continues to rise. Enterprises require unified technical support to maintain system performance and operational continuity across these environments. The growing expansion of enterprise IT infrastructure in emerging markets therefore creates substantial opportunities for service providers offering vendor-agnostic support, infrastructure maintenance, and integrated IT lifecycle management solutions.

Adoption of Artificial Intelligence and Predictive Maintenance Transforming Multi-Vendor Support Capabilities

Artificial intelligence is increasingly transforming the way multi-vendor support services are delivered by enabling predictive maintenance and automated diagnostics. Advanced analytics tools from providers such as Google Cloud allow service teams to monitor infrastructure performance in real time and identify potential failures before they disrupt operations. This proactive approach improves reliability across complex IT environments.

Predictive support systems can analyze device behavior, network activity, and application performance to detect anomalies early and trigger automated alerts. These capabilities are particularly valuable in technology-intensive sectors such as IT and telecommunications where infrastructure uptime is critical. As organizations continue integrating AI into their operations, intelligent support solutions are expected to enhance service efficiency and strengthen the value of multi-vendor maintenance strategies.

Category-wise Analysis

Service Type Insights

Hardware support dominates the Multi-Vendor Support Services Market, accounting for 62% of the market share in 2025. Enterprises operate large volumes of servers, storage devices, and networking equipment from vendors such as Hewlett Packard Enterprise and Dell Technologies within data centers and enterprise IT facilities. These diverse hardware environments require continuous maintenance, lifecycle management, and rapid troubleshooting to ensure operational stability and minimize infrastructure downtime across complex IT ecosystems.

Software support is emerging as the fastest-growing service category as enterprises increasingly deploy cloud platforms, enterprise applications, and virtualization tools. Organizations rely on integrated software environments that connect multiple platforms and vendors, making cross-vendor troubleshooting essential. As businesses expand digital platforms and adopt hybrid IT architectures, demand for coordinated software maintenance, patch management, and compatibility support continues to increase.

Enterprise Insights

Large enterprises lead the market with 68% share in 2025 due to their extensive IT infrastructure and reliance on multiple technology vendors. Organizations in sectors such as BFSI, manufacturing, and telecommunications often manage complex systems supplied by providers like Cisco Systems, NetApp, and IBM. Multi-vendor support services help these enterprises streamline maintenance, reduce operational disruptions, and manage large-scale technology environments efficiently.

Small and Medium Enterprises are emerging as the fastest-growing segment as digital transformation expands across mid-sized organizations. SMEs increasingly deploy cloud applications, managed IT infrastructure, and digital platforms to improve competitiveness. As their technology environments diversify, these businesses are adopting multi-vendor support services to gain access to specialized expertise and centralized technical assistance without maintaining large internal IT teams.

Delivery Model Insights

Remote support leads the market with 55% share in 2025 due to its ability to deliver rapid diagnostics and troubleshooting without requiring onsite visits. Advanced connectivity technologies and remote monitoring platforms enable service providers to identify technical issues, perform system checks, and deploy fixes across distributed infrastructures. Organizations using equipment from vendors such as Cisco Systems and Dell Technologies benefit from faster issue resolution and lower operational costs.

Hybrid delivery models are emerging as the fastest-growing approach as enterprises combine remote monitoring with onsite intervention when necessary. This model allows service providers to perform initial diagnostics remotely while dispatching field engineers for complex hardware repairs or infrastructure upgrades. The flexibility of hybrid support models aligns well with modern enterprise environments that integrate cloud systems, data centers, and edge infrastructure.

Industry Insights

IT and Telecom leads the Multi-Vendor Support Services Market with 35% share in 2025 due to the sector’s heavy reliance on complex networking infrastructure, data centers, and cloud platforms. Telecommunications operators and technology companies operate large-scale systems built on equipment from vendors such as Cisco Systems, IBM, and Oracle Corporation, requiring continuous monitoring and integrated maintenance to maintain service reliability.

Healthcare is emerging as the fastest-growing industry vertical as hospitals and healthcare providers expand digital health systems, medical devices, and connected infrastructure. Healthcare organizations increasingly deploy advanced IT platforms to manage patient data, diagnostics, and telemedicine services. The growing reliance on integrated technologies from multiple vendors is increasing the need for coordinated support services to ensure system reliability and regulatory compliance.

Regional Insights

North America Multi-Vendor Support Services Market Trends

North America leads the Multi-Vendor Support Services Market with a 38% share in 2025, supported by highly advanced enterprise IT infrastructure and strong adoption of third-party maintenance services. The United States plays a dominant role due to its large concentration of enterprise data centers, cloud platforms, and technology providers. Organizations operating complex infrastructures from vendors such as Cisco Systems, Dell Technologies, and IBM rely heavily on integrated support solutions to maintain performance and uptime.

The region also benefits from a mature digital ecosystem and strong regulatory emphasis on network reliability and service continuity. Technology hubs such as Silicon Valley continue to drive innovation in artificial intelligence, cloud infrastructure, and data center technologies. As enterprises expand hybrid IT architectures and large-scale data environments, demand for vendor-agnostic maintenance and unified infrastructure support remains strong across industries.

Europe Multi-Vendor Support Services Market Trends

Europe represents a steadily growing market for multi-vendor support services, supported by strong digital transformation initiatives across enterprise and industrial sectors. Countries such as Germany, United Kingdom, and France are expanding enterprise IT systems to support automation, data analytics, and connected infrastructure. Industrial modernization initiatives like Industry 4.0 have accelerated adoption of integrated IT and operational technology platforms.

The region is projected to grow at a CAGR of 4.2% during the forecast period as businesses expand cloud computing, cybersecurity systems, and digital enterprise platforms. Regulatory frameworks such as General Data Protection Regulation also encourage structured IT governance and infrastructure oversight. As European enterprises deploy technologies from multiple vendors across cloud and on-premises environments, demand for coordinated multi-vendor maintenance and lifecycle management services continues to rise.

Asia Pacific Multi-Vendor Support Services Market Trends

Asia Pacific holds a 32% share of the Multi-Vendor Support Services Market in 2025 and continues to expand as enterprises accelerate digital transformation. Countries such as China, Japan, and India are investing heavily in telecommunications infrastructure, data centers, and advanced manufacturing technologies. Rapid expansion of 5G networks and enterprise connectivity is increasing demand for reliable infrastructure maintenance and cross-vendor technical support.

The region is also witnessing strong growth in electronics manufacturing and digital services industries. Government initiatives supporting domestic technology production and smart infrastructure projects are encouraging businesses to adopt complex IT systems built on diverse platforms. As organizations deploy large-scale networking equipment, cloud infrastructure, and enterprise applications, the need for centralized support services capable of managing multi-vendor ecosystems continues to grow across the Asia Pacific.

Competitive Landscape

The multi-vendor support services market features a relatively consolidated competitive environment where major service providers compete through broad service portfolios, global delivery networks, and advanced technical capabilities. Companies focus on strengthening operational efficiency by expanding service coverage, improving response times, and integrating automation into support processes. Continuous investments in research and development help providers enhance infrastructure monitoring, predictive diagnostics, and proactive maintenance capabilities.

Competition is also shaped by strategic mergers, acquisitions, and partnerships that help providers expand geographic reach and technical expertise. Service providers increasingly adopt flexible delivery models, including subscription-based and as-a-service offerings, allowing enterprises to access scalable vendor-agnostic support solutions while improving cost efficiency and operational resilience.

Key Developments:

- In March 2025, Hewlett-Packard strengthened its service portfolio by acquiring a diagnostics technology firm focused on advanced infrastructure analytics, aiming to enhance predictive maintenance capabilities and improve multi-vendor support services for enterprise hardware and data center environments.

- In June 2024, IBM introduced Watson AIOps to enhance multi-vendor infrastructure management by using artificial intelligence to automate incident detection and root-cause analysis, significantly reducing operational alerts and helping IT teams improve system monitoring efficiency across complex enterprise environments.

- In October 2024, Cisco Systems expanded its support capabilities to edge environments through collaboration with Amazon Web Services, enabling enterprises to manage distributed infrastructure more effectively while improving remote monitoring, troubleshooting, and integrated service delivery across hybrid cloud and edge networks.

Companies Covered in Multi-Vendor Support Services Market

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies Inc.

- Cisco Systems, Inc.

- Oracle Corporation

- Microsoft Corporation

- Fujitsu Ltd.

- NEC Corporation

- Hitachi Vantara LLC

- NetApp Inc.

- Atos SE

- DXC Technology Company

- Wipro Limited

- Capgemini SE

- Tata Consultancy Services (TCS)

Frequently Asked Questions

The multi-vendor support services market is projected to reach US$ 58.0 billion in 2026, supported by growing enterprise reliance on complex multi-vendor IT infrastructures and integrated lifecycle support services.

Rising IT infrastructure complexity, hybrid cloud adoption, and multi-platform environments are increasing the need for unified support across hardware, software, and network systems.

North America leads with a 38% share in 2025, driven by strong enterprise IT ecosystems and high adoption of vendor-agnostic maintenance services.

The integration of AI-driven predictive maintenance presents a major opportunity, particularly as enterprises expand digital infrastructure across regions including Asia Pacific.

Major industry participants include IBM, Cisco Systems, Hewlett-Packard, and Dell Technologies.