- Hardware & Software IT Services

- Mobile/Micro Data Center Market

Mobile/Micro Data Center Market Size, Share, and Growth Forecast, 2025 - 2032

Mobile/Micro Data Center Market by Unit (Up to 20 RU, 20 - 40 RU, Above 40 RU), Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises (SMEs)), Application (Instant/Retrofit Data Center, Edge-Computing Nodes, High-Density Networks, Remote Office and Branch Office, Mobile and Tactical Computing, Disaster Recovery and Backup), End-use, and Regional Analysis for 2025 - 2032

Mobile/Micro Data Center Market Size and Trend Analysis

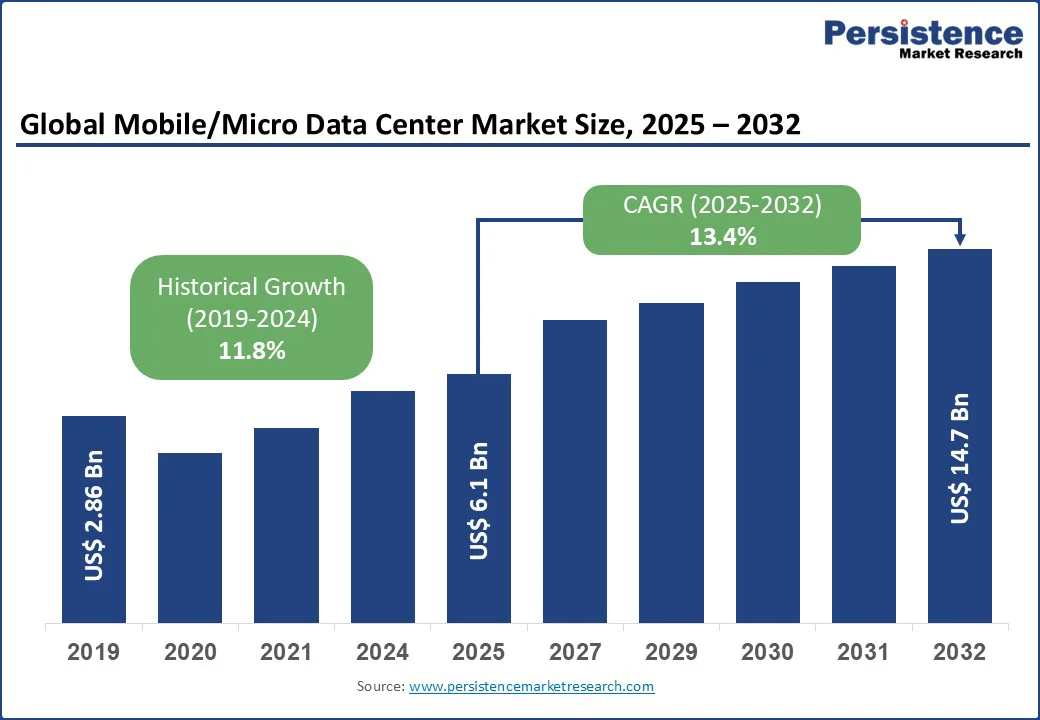

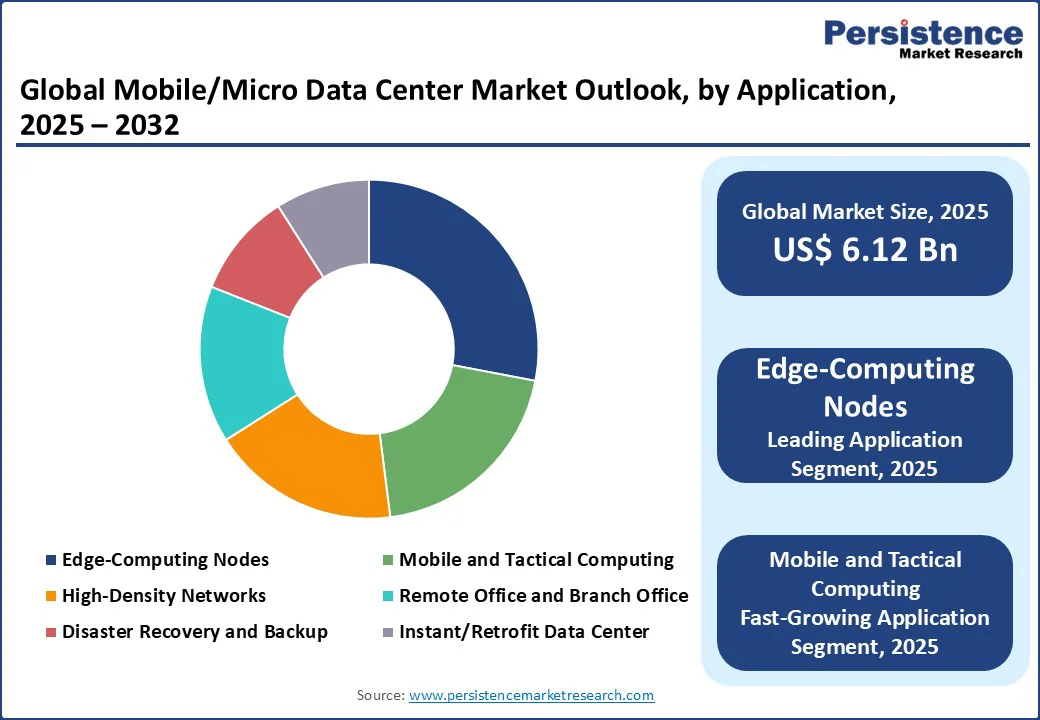

The global mobile/micro data center market size is likely to value at US$6.12 Bn in 2025 and reach US$14.72 Bn by 2032, growing at a CAGR of 13.4% during the forecast period from 2025 to 2032, fueled by the rising demand for edge computing, driven by the proliferation of IoT devices, 5G networks, and the need for low-latency data processing.

Key Industry Highlights:

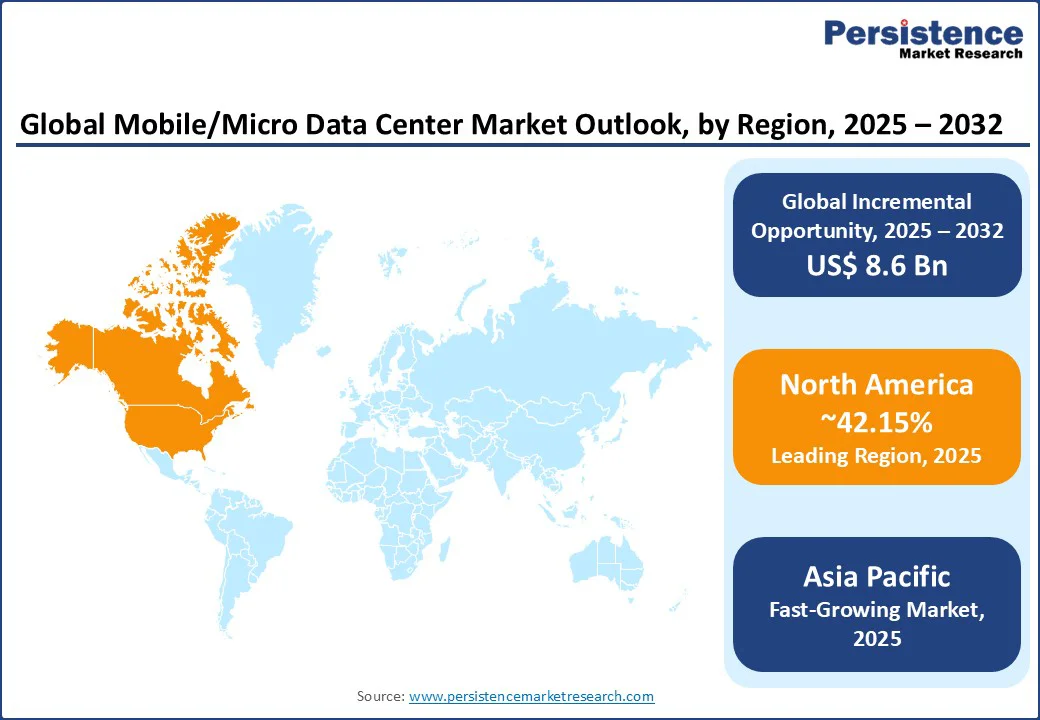

- Leading Region: North America is likely to account for 42.1% share in 2025 driven by advanced technological infrastructure, widespread 5G adoption, and high demand for edge computing in the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, propelled by rapid digitalization, smart city initiatives, and increasing IoT penetration in countries such as China and India.

- Investment Plans: China’s 14th Five-Year Plan (2021-2025) emphasizes smart infrastructure, expanding its data sector to roughly USD?821?billion by end?2024, and deploying 4.55?million 5G base stations and 226?million gigabit broadband users by mid?2025, boosting demand for mobile data centers.

- Dominant Unit Type: 20 - 40 RU units dominate, accounting for nearly 41.1% of the market share, due to their balance of scalability and compactness for edge computing.

- Leading Application: Edge-computing nodes contribute over 43.1% of market revenue, driven by the need for low-latency data processing in IoT and 5G applications.

| Key Insights | Details |

|---|---|

| Mobile/Micro Data Center Market Size (2025E) | US$ 6.12 Bn |

| Market Value Forecast (2032F) | US$ 14.72 Bn |

| Projected Growth (CAGR 2025 to 2032) | 13.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 11.8% |

Market Dynamics

Driver: Surge in Edge Computing and IoT Adoption Fuels Market Growth

The global mobile/micro data center market is experiencing significant growth due to the rapid rise in edge computing and IoT adoption across industries. Mobile/micro data centers are critical for processing data closer to its source, reducing latency and enhancing performance for applications such as autonomous vehicles, smart cities, and industrial automation.

According to the International Data Corporation (IDC), global IoT spending is expected to reach $1.1 trillion by 2026, with edge computing investments driving demand for compact data centers. According to a GSMA Intelligence report titled “5G era in the US”, the United States is expected to reach 190 million 5G connections by the end of 2025, necessitating mobile data centers for real-time data processing.

In the Asia Pacific, China’s smart city projects, such as those in Shenzhen, rely on micro data centers to support IoT ecosystems. Companies such as Schneider Electric and Vertiv Group Corp. reported increased sales of edge-ready solutions in 2024. The global push for digital transformation and low-latency computing ensures sustained demand, positioning edge computing as a key driver for market growth through 2032.

Restraint: High Initial Costs and Energy Consumption Challenges

The mobile/micro data center market faces challenges due to high initial deployment costs and significant energy consumption. These data centers require specialized infrastructure, including cooling systems and power-efficient hardware, which increases upfront costs. In 2023, the cost of deploying a single micro data center ranged from $50,000 to $200,000, per Gartner, posing a barrier for small and medium-sized enterprises (SMEs).

Additionally, energy-intensive operations, particularly in high-density applications, raise concerns about operational costs and sustainability. The competition from traditional centralized data centers, which offer economies of scale, further limits adoption in cost-sensitive markets. Limited standardization and concerns over interoperability in some regions also hinder market growth, particularly for smaller players competing with established vendors such as Dell and IBM.

Opportunity: Growing Demand in 5G and Smart City Initiatives

The increasing deployment of 5G networks and smart city initiatives presents significant opportunities for the mobile/micro data center market. These data centers are essential for supporting 5G’s ultra-low latency requirements and enabling real-time data processing for smart city applications, such as traffic management and public safety systems.

GSMA Intelligence reports that 5G connections rose to 1.6 billion by the end of 2023 and are projected to reach US$ 5.5 Bn by 2030, with the Asia Pacific leading in network rollouts.

Companies such as Huawei Technologies and Rittal GmbH are innovating with modular, energy-efficient data centers tailored for 5G and IoT applications. Government incentives, such as the U.S. Infrastructure Investment and Jobs Act, further encourage investments in smart infrastructure, creating opportunities for manufacturers to develop scalable, eco-friendly mobile data centers to meet evolving industry needs through 2032.

Category-wise Analysis

By Unit

- The 20 - 40 RU segment is likely to account for the largest share 41.1% in 2025, due to its optimal balance of scalability, compactness, and performance. These units are widely adopted in edge-computing nodes and remote office applications, offering sufficient capacity for high-density workloads while maintaining portability. Companies such as Schneider Electric and Vertiv Group Corp. lead with modular solutions catering to IT, telecom, and retail sectors, particularly in North America and the Asia Pacific, where rapid 5G deployment drives demand.

- The above 40 RU is the fastest-growing segment driven by increasing demand for high-capacity data processing in applications such as disaster recovery and high-density networks. These larger units are favored by large enterprises in the BFSI and government sectors for their ability to handle complex workloads. Players such as Dell and IBM are expanding offerings to support large-scale edge computing projects in Europe and North America.

By Enterprise Size

- Large enterprises dominate the mobile/micro data center market, accounting for approximately 62.3% of revenue in 2025, due to their extensive IT infrastructure and need for scalable, high-performance data centers. Sectors such as IT, telecom, and BFSI rely on mobile data centers for edge computing and disaster recovery. Companies such as Hewlett Packard Enterprise and Huawei Technologies cater to large enterprises with customized, high-density solutions, particularly in North America and the Asia Pacific.

- SMEs are the fastest-growing segment, driven by increasing digital transformation and the need for cost-effective, compact data center solutions. Mobile/micro data centers enable SMEs to deploy edge computing and remote office solutions without heavy infrastructure investments. Vendors such as Zella DC and Panduit Corp. are focusing on modular, plug-and-play solutions for SMEs in retail and healthcare sectors, especially in Europe and South Asia.

By Application

- Edge-computing nodes account for over 43.1% of market revenue in 2025, driven by the need for low-latency data processing in IoT, 5G, and smart city applications. These nodes are critical for real-time analytics in industries such as retail and telecom. Major players, such as Schneider Electric and Vertiv, supply edge-ready solutions for projects in the U.S. and China, where 5G infrastructure investments fuel demand.

- The mobile and tactical computing segment is the fastest-growing in mobile/micro data center market, propelled by rising demand in government, defense, and disaster recovery applications. These portable data centers support mission-critical operations in remote or temporary environments. Companies such as Eaton and Rittal GmbH are innovating with rugged, mobile solutions for defense sectors in North America and the Middle East, driven by increasing security and resilience needs.

By End-use

- The IT and telecommunication sector holds the largest share of micro/mobile date center market, contributing approximately 38.4% of market revenue in 2025, driven by the global rollout of 5G networks and IoT ecosystems. Mobile data centers are critical for supporting high-density networks and edge computing. Companies such as Huawei and IBM lead with solutions tailored for telecom giants in the Asia Pacific and North America.

- Healthcare and life sciences are the fastest-growing end-use segments, driven by the adoption of IoT-enabled medical devices and real-time data analytics. Mobile data centers support remote diagnostics and telehealth applications, with vendors such as Dell and Schneider Electric expanding offerings in Europe and North America, where healthcare digitization is accelerating.

Regional Insights

North America Mobile/Micro Data Center Market Trends

North America dominates the global industry, likely to account for 42.1% share, fueled by strong demand from the IT, telecommunications, and BFSI sectors in the U.S. and Canada. The U.S. IT industry increasingly depends on mobile data centers to support edge computing and disaster recovery, ensuring low latency and business continuity.

Meanwhile, Canada’s telecom sector drives growth through the expansion of high-density networks, as highlighted by the Canadian Radio-television and Telecommunications Commission (CRTC). Leading companies such as Dell and Vertiv dominate this landscape with extensive distribution channels, actively supporting smart city initiatives and 5G infrastructure projects.

Additionally, growing consumer preference for scalable and energy-efficient solutions further bolsters North America’s market leadership, positioning the region for sustained innovation and robust infrastructure development.

Asia Pacific Mobile/Micro Data Center Market Trends

The Asia Pacific stands out as the fastest-growing region fueled by rapid digitalization, smart city initiatives, and high IoT penetration in countries such as China and India. China’s 14th Five-Year Plan emphasizes smart infrastructure, expanding its data sector to roughly USD?821?billion by end?2024, and deploying 4.55?million 5G base stations and 226?million gigabit broadband users by mid?2025, boosting demand for mobile data centers.

India’s Digital India initiative drives demand for edge-computing nodes in urban centers. The region’s telecom and retail sectors also contribute, with companies such as Huawei Technologies and Zella DC expanding their presence. Rising industrial automation and government-led projects ensure the Asia Pacific’s rapid market growth through 2032.

Europe Mobile/Micro Data Center Market Trends

Europe ranks as the second fastest-growing region in the mobile/micro data center market, propelled by strict data privacy regulations and increasing demand from telecom and healthcare sectors. Smart city initiatives in countries such as Germany and France further stimulate growth.

In 2023, the European Commission allocated €1.3 billion through the Digital Europe Programme to accelerate digital transformation and cybersecurity, bolstering demand for mobile data centers in edge computing and high-density network applications.

Germany’s robust telecom sector benefits from key players such as Rittal GmbH and Schneider Electric, driving innovation and infrastructure development. Additionally, the EU’s Smart Cities Marketplace fosters IoT-driven projects, boosting the need for compact, energy-efficient data centers. Europe’s strong emphasis on sustainability and regulatory compliance continues to shape market dynamics and inspire cutting-edge solutions.

Competitive Landscape

The global mobile/micro data center market is highly competitive, characterized by a fragmented landscape with a mix of global giants and regional players. Leading companies, including Dell, Inc., Hewlett-Packard Enterprise, and Schneider Electric, dominate through extensive product portfolios and global distribution networks.

Regional players such as Zella DC focus on localized offerings in the Asia Pacific and Europe. Companies are investing in energy-efficient, modular designs and AI-integrated solutions to enhance market share, driven by demand for edge computing and 5G applications.

Key Industry Developments

- February 2025: Google Cloud announced that it has deployed over 100 million lithium-ion (Li-ion) cells across its global data center fleet. This milestone reflects a significant shift from traditional lead-acid batteries to Li-ion battery backup units (BBUs), which are integral components of micro mobile data centers. These compact, modular data centers are designed for edge computing applications, offering scalability, rapid deployment, and energy efficiency.

- October 2024: Zella DC introduced the Zella Outback outdoor micro data center. This advanced solution is designed for edge computing applications, particularly in harsh environments such as remote locations, mining sites, farms, and urban rooftops. The Zella Outback offers enhanced insulation, modular panels for easy maintenance, upgraded access control with multi-factor authentication, and optional fireproofing measures.

Companies Covered in Mobile/Micro Data Center Market

- Dell, Inc.

- Eaton

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Panduit Corp.

- Rittal GmbH & Co.

- Schneider Electric

- Vertiv Group Corp.

- Zella DC

- Others

Frequently Asked Questions

The mobile/micro data center market is projected to reach US$6.12 Bn in 2025.

The surge in edge computing, IoT adoption, and 5G network rollouts is the key market driver.

The mobile/micro data center market is poised to witness a CAGR of 13.4% from 2025 to 2032.

The rising demand in 5G networks and smart city initiatives is the key market opportunity.

Dell, Inc., Hewlett-Packard Enterprise, Schneider Electric, and Huawei Technologies are key market players.