- Processed Food

- Millet Cereals Market

Millet Cereals Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Millet Cereals Market by Product Type (Ready to Eat RTE Millet Cereals, Hot Millet Cereals), by Nature (Organic, Conventional), Sales Channel (Supermarkets & Hypermarkets, Specialty Stores, Convenience Stores, Online retail, Others), and Regional Analysis, 2026 - 2033

Millet Cereals Market Share and Trends Analysis

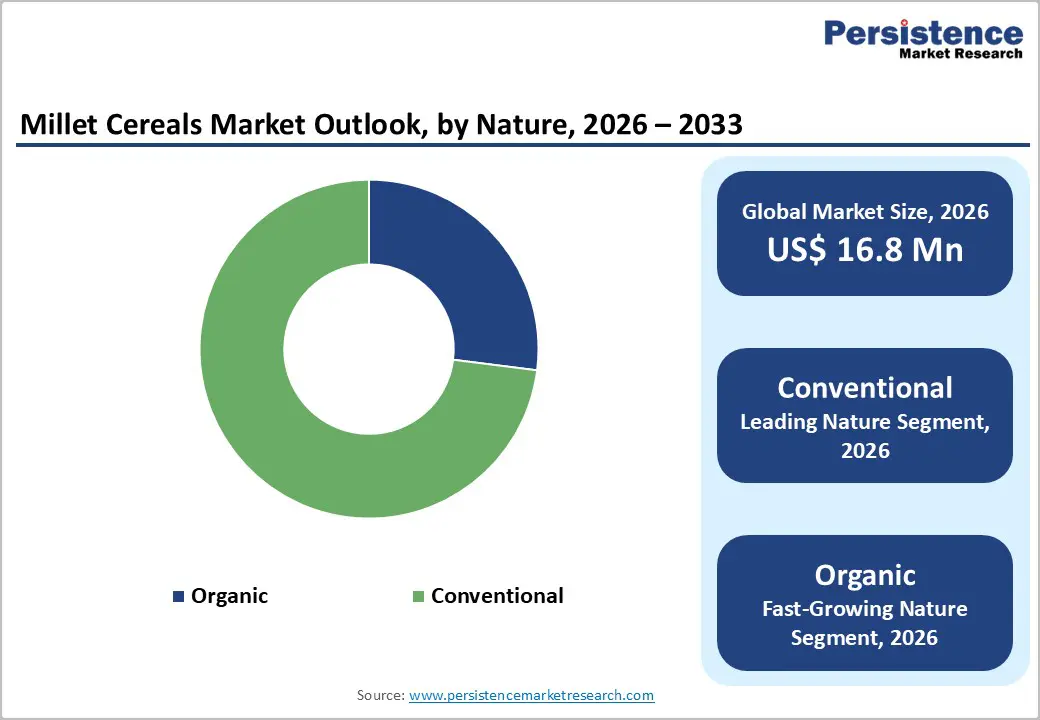

The global millet cereals market size is expected to be valued at US$ 16.8 million in 2026 and projected to reach US$ 38.6 million by 2033, growing at a CAGR of 12.6% between 2026 and 2033.

The market is predominantly driven by the surging global demand for gluten-free, high-protein breakfast alternatives and the structural pivot toward climate-resilient ancient grains. Rising health literacy regarding the prevention of non-communicable diseases like diabetes and obesity has positioned millets as a primary nutri cereal. Furthermore, the significant momentum generated by the International Year of Millets 2023 has led to widespread institutional support and the integration of millet-based cereals into global retail supply chains, while innovations in processing technologies by companies such as Nestlé and Tata Consumer Products Limited have successfully bridged the gap between traditional nutrition and modern convenience.

Key Industry Highlights:

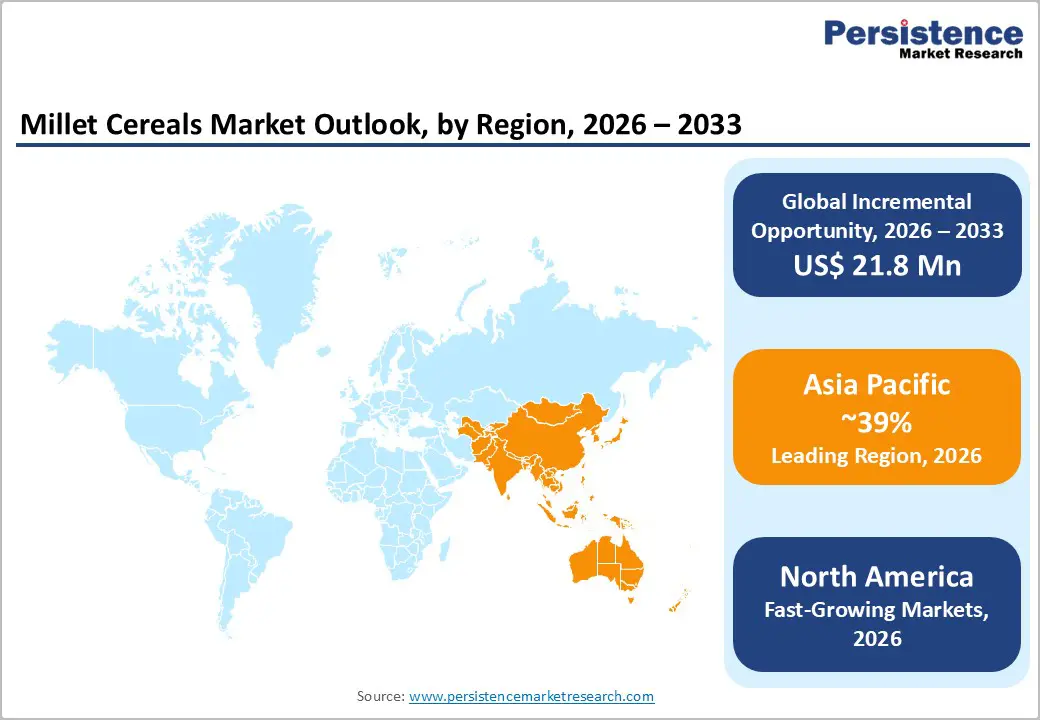

- Leading Region: Asia Pacific held a 39% market share in 2025, driven by deep cultural roots and strong government support for millet missions in India.

- Fastest Growing Region: North America is the fastest growing region through 2033, fueled by the gluten-free movement and the rising demand for ancient grain superfoods.

- Dominant Segment: Conventional nature products held 73% of the market in 2025, benefiting from mass market accessibility and large-scale production.

- Fastest Growing Segment: Organic millet cereals are growing at the highest rate, as health-conscious consumers in developed economies prioritize pesticide-free and non-GMO credentials.

- Key Opportunity: The integration of millets into Personalized Nutrition and subscription-based e commerce models offers a high margin avenue for artisanal brands.

| Key Insights | Details |

|---|---|

| Global Millet Cereals Market Size (2026E) | US$ 16.8 Mn |

| Market Value Forecast (2033F) | US$ 38.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 12.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.4% |

Market Dynamics

Driver - Growing Health Awareness and Demand for Functional Nutri Cereals

A powerful growth engine for the millet cereals market is the accelerating consumer pivot toward preventive healthcare and functionally dense diets. Millets are widely acknowledged for their strong nutritional credentials, offering around 12% protein along with meaningful levels of calcium, magnesium, and dietary fiber. Clinical meta-analyses indicate that consistent millet intake can lower fasting blood glucose by nearly 11-12%, reinforcing their relevance for the expanding global diabetic and prediabetic population. As metabolic disorders rise, consumers are actively replacing refined grains with low-glycemic, whole-grain alternatives.

This health-led shift is particularly visible in urban markets across Asia Pacific and North America, where shoppers increasingly scrutinize ingredient lists and glycemic impact. Millet cereals align well with the clean-label movement, being perceived as natural, non-GMO, and minimally processed. In addition, growing awareness of gluten intolerance, weight management goals, and gut health is broadening millet’s appeal beyond traditional consumers, encouraging manufacturers to expand fortified, ready-to-eat, and convenience-focused millet cereal portfolios.

Restraints - Supply Chain Inefficiencies and Limited Mechanization

Despite robust demand, the market is restrained by structural bottlenecks in production and post-harvest handling. Mechanized harvesting reaches barely 15% of millet acreage in Sub Saharan Africa compared to over 80% for wheat in high income markets. The tiny size of millet seeds often clogs conventional agricultural machinery, leading to high labor intensity and lower price competitiveness. According to reports from the Food and Agriculture Organization (FAO), post-harvest losses can hover between 25% and 30% in regions where hermetic storage and modern dehulling plants remain scarce. These inefficiencies lock many producers into subsistence cycles, forfeiting significant revenue potential. For large scale manufacturers, the lack of standardized, high quality grain supply complicates the production of uniform cereal flakes and puffs, often leading to volatile pricing in the retail segment.

Opportunity - Personalized Nutrition and the Rise of Organic Superfoods

The surging interest in personalized wellness offers a lucrative opportunity for companies to launch hyper targeted millet based solutions. The Organic segment is identified as the fastest growing nature category, as affluent consumers increasingly link pesticide free farming with long term longevity. In 2026, the integration of millet cereals into AI driven dietary apps and subscription models provides a pathway for brands like Slurrp Farm and Soulfull to reach health conscious parents seeking nutrient dense, low sugar options for children. There is a massive revenue pocket in formulating cereals that address specific life stages, such as high calcium finger millet (Ragi) cereals for bone health in the aging population or iron fortified pearl millet cereals for maternal nutrition. Brands that leverage verified sustainability credentials and organic certifications can command price premiums of 40% to 60% over commodity grains.

Category-wise Analysis

Product Type Analysis

Ready to Eat RTE Millet Cereals segment dominated the market, driven by the convenience seeking habits of the global urban workforce. These products, including millet flakes, puffs, and granolas, offer a quick breakfast solution that fits into high paced lifestyles. However, the Hot Millet Cereals segment, comprising porridges and traditional mixes like Upma, is witnessing a resurgence in the health and wellness sector. This growth is supported by the comfort food trend and the perception of hot cereals as being more wholesome and less processed. Brands like Nestlé India have successfully launched masala millet porridges that cater to local taste habits while providing high fiber and mineral density, bridging the gap between traditional recipes and modern retail formats.

Sales Channel Analysis

Supermarkets & Hypermarkets remain the leading distribution channel, providing the high visibility and bulk purchasing options that drive the majority of volume sales. These large-format stores often feature dedicated health food or ancient grain aisles that make it easier for consumers to discover new millet-based brands. Meanwhile, Online retail is emerging as a critical growth engine. The expansion of e-commerce platforms allows niche brands such as Millet Bank and Danodia Foods to offer detailed product descriptions and unique subscription models that physical stores may lack. In 2026, the ease of home delivery and competitive online pricing are attracting a tech-savvy demographic, making the digital channel essential for the rapid scaling of the Millet Cereals Market.

Region-wise Insights

North America Millet Cereals Market Trends and Insights

North America is identified as the fastest-growing regional market for the forecast period. This growth is underpinned by an aggressive shift toward gluten-free and low glycemic diets among the U.S. and Canadian populations. In 2025, millets began appearing in the premium health aisles of major retailers as a superior alternative to quinoa and brown rice. The region’s mature innovation ecosystem has fostered the rise of startups that integrate millets into baked goods and sophisticated breakfast mixes.

Regulatory frameworks in the U.S., supported by the FDA’s nutritional labeling guidelines, have empowered consumers to seek out nutrient-dense ancient grains. The vegan and plant-based movements in the region further contribute to millet’s appeal as a flexible plant protein source. Additionally, Western millers are increasingly preferring millet’s native mineral profile and longer shelf life compared to rice-based flours. The presence of high-income demographics that value sustainability and environmental stewardship ensures that North America remains a primary engine for high-value market growth through 2033.

Asia Pacific Millet Cereals Market Trends and Insights

Asia Pacific remains the dominant regional market, holding a 39% share in 2025. This leadership is rooted in centuries of cultural tradition and the region’s status as a primary production hub. India and China are the global engines of millet consumption and production, with India rebranding millets as nutri cereals to boost domestic and international demand. Government minimum support prices and the integration of millets into public distribution systems have underpinned the region’s entrenched market position.

Manufacturing advantages in Asia Pacific, including lower labor costs and proximity to raw materials, allow local companies like Tata Consumer Products and Marico to produce cost effective Ready to Eat RTE Millet Cereals. In 2024, the region witnessed a surge in specialized startups focusing on millet-based baby foods and ethnic breakfast mixes. While China remains a vital consumption base, its urbanizing dietary shift is nudging the regional market toward a more mature phase. The high penetration of mobile payments and social commerce in urban centers is further accelerating the retail accessibility of premium millet cereal products.

Market Competitive Landscape

The Millet Cereals Market is currently characterized by a fragmented structure, featuring a mix of large multinational food conglomerates and a vibrant ecosystem of specialized startups. Market leaders like Nestlé and Kellanova leverage their extensive global distribution networks and marketing budgets to introduce millet based variants of their flagship cereal brands. Conversely, firms like Slurrp Farm, Tata Consumer Products Limited, and Soulfull focus on the nutri cereal niche, emphasizing natural ingredients and clean labels to build brand loyalty among health conscious parents.

Key differentiators in the industry include processing expertise to improve palatability, organic certifications, and strategic partnerships with farmer producer organizations. Emerging business models are increasingly moving toward the Direct to Consumer (DTC) space, where brands engage with users via social media and wellness platforms. Research and development efforts are currently concentrated on using AI for trend forecasting and optimizing the extrusion process to create millet puffs with textures indistinguishable from traditional corn based cereals. As the market matures, a wave of consolidation is expected, with larger players acquiring successful niche brands to bolster their better for you portfolios.

Key Developments:

- In February 2026, Bakeit Food launched a US$4 million granola production facility in the UK, expanding domestic capacity for premium breakfast cereal products.

- In February 2026, Slurrp Farm has raised Rs 30 crore (around $3.3 million) in its extended Series C round from Scarlet Ventures.

- In October 2025, Institute of Hotel Management Ranchi hosted ‘Millet Fest 2025’ in collaboration with Milli Life Naturals Ltd and Startup Jharkhand to promote millet-based nutrition awareness.

- In August 2023, Tata Consumer Products GB entered the UK breakfast cereals category with Joyfull Millets, marking a strategic diversification beyond its traditional beverage-focused portfolio.

Companies Covered in Millet Cereals Market

- Nestlé

- Slurrp Farm

- Tata Consumer Products Limited

- Kellanova

- Marico

- Bagrrys

- Millet'n'Minutes

- Millet Bank

- Danodia Foods

- Navaloka

- Hometown Food Company

- Others

Frequently Asked Questions

The global Millet Cereals market is projected to be valued at US$ 16.8 Mn in 2026.

Growing Health Awareness and Demand for Functional Nutri Cereals is driving demand for Millet Cereals market.

The Global Millet Cereals market is poised to witness a CAGR of 12.6% between 2026 and 2033.

Personalized Nutrition and the Rise of Organic Superfoods is creating opportunity for key players in the Millet Cereals market.

Key industry leaders include Nestlé, Slurrp Farm, Tata Consumer Products Limited, Kellanova, Marico, Bagrrys, and Others