- Specialty & Fine Chemicals

- Microencapsulation Market

Microencapsulation Market Size, Share, and Growth Forecast, 2026 - 2033

Microencapsulation Market by Technology Type (Coating, Emulsion, Spray Technologies, Dripping, Others), Coating Material (Carbohydrate, Gums & Resins, Others), Application (Pharmaceutical & Healthcare Products, Others), and Regional Analysis for 2026 - 2033

Microencapsulation Market Size and Trends Analysis

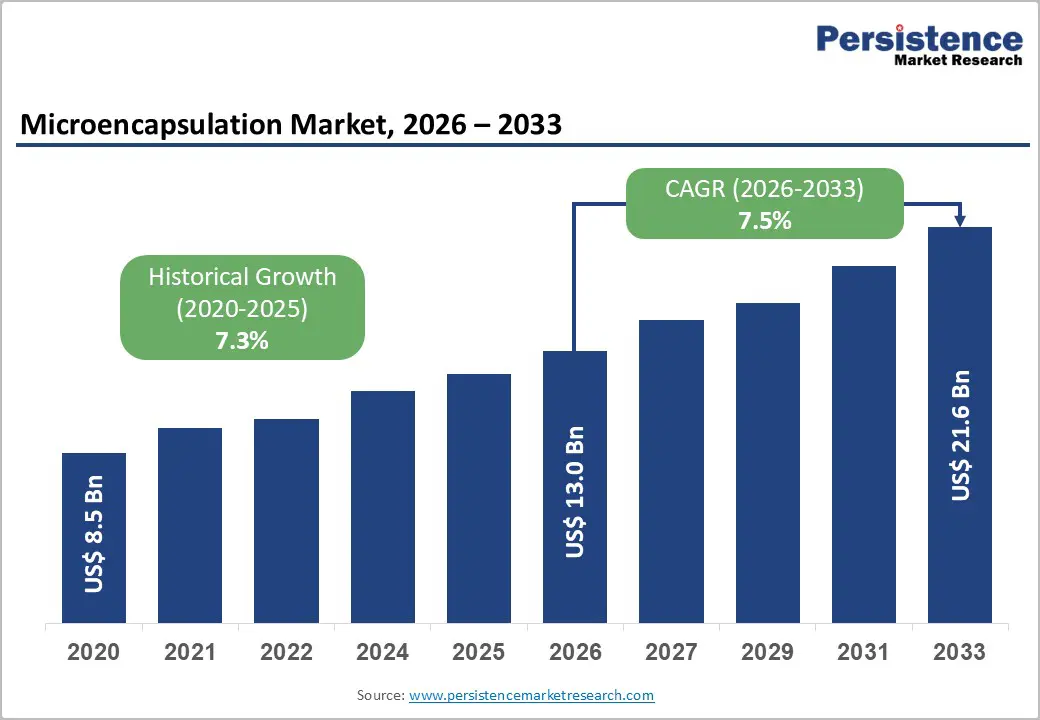

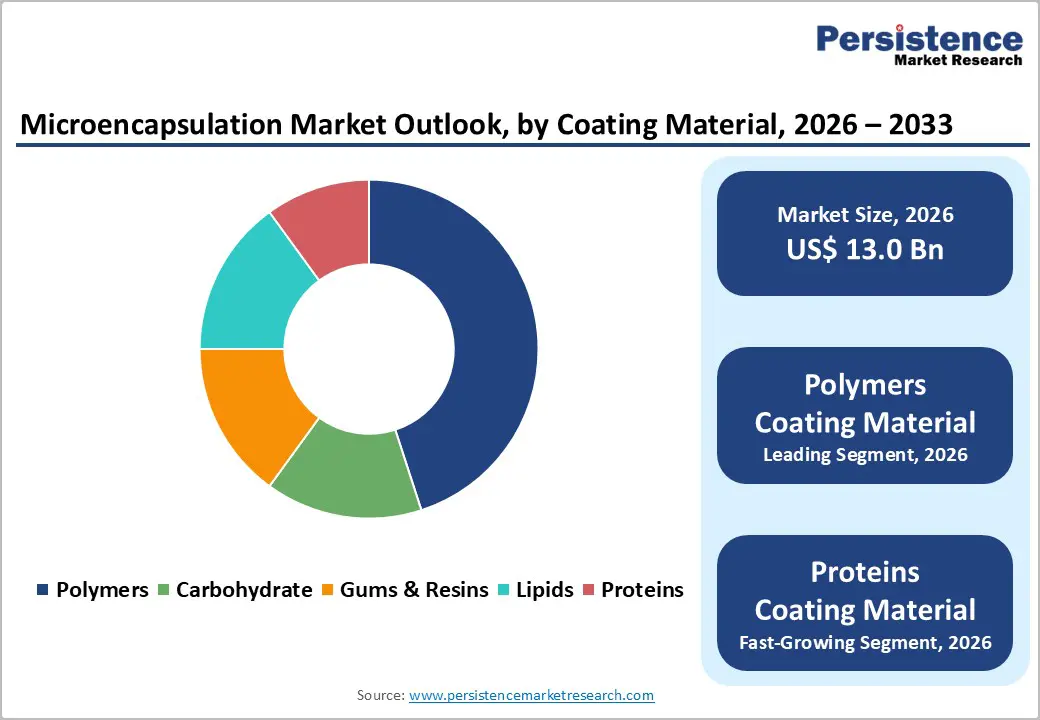

The global microencapsulation market size is likely to be valued at US$13.0 billion in 2026, and is expected to reach US$21.6 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of controlled-release technologies in pharmaceuticals, rising demand for stable ingredients in food preservation, and advancements in spray and emulsion encapsulation methods.

Rising demand for targeted microencapsulation in pharmaceuticals, healthcare, and food applications is driving market adoption. Advances in polymer and lipid coatings are enhancing durability and biocompatibility, while growing awareness of microencapsulation’s role in ingredient protection and efficacy is supporting growth, particularly in emerging markets.

Key Industry Highlights:

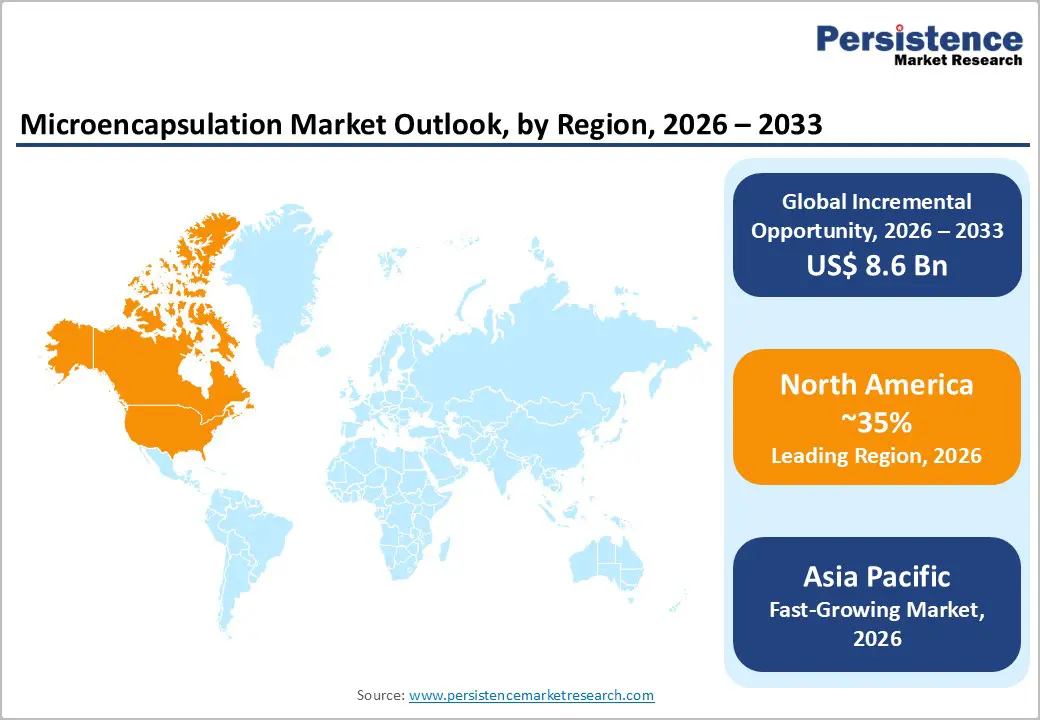

- Leading Region: North America, anticipated to account for a 35% market share in 2026, driven by advanced pharmaceutical R&D, high demand for functional foods, and strong innovation in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid industrialization, rising agrochemical needs, and growing investments in food processing in China and India.

- Dominant Technology Type: Spray Technologies, to hold approximately 40% of the market share, as they provide high throughput and uniform coating for powders.

- Leading Coating Material: Polymers account for over 35% of market revenue, owing to their versatility, biocompatibility, and widespread use in controlled-release.

- Leading Application: Pharmaceutical & healthcare products, to contribute nearly 40% of the market revenue, due to drug delivery precision and stability enhancement.

| Key Insights | Details |

|---|---|

| Microencapsulation Market Size (2026E) | US$13.0 Bn |

| Market Value Forecast (2033F) | US$21.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Controlled-Release Technologies and Demand for Stable Ingredients

The rising demand for controlled-release technologies is quickly becoming a major opportunity for microencapsulation suppliers, driven by the growing industry demand for prolonged efficacy, targeted delivery, and reduced side effects. Traditional formulations often create instability, especially in pharmaceuticals and agrochemicals, leading to degradation and lower performance. Stable technologies, including spray encapsulation, emulsion methods, polymer coatings, lipid shells, and protein matrices, address these concerns by offering a protective, timed-release alternative. These formats simplify application, reduce the need for frequent dosing, and are particularly effective during precision medicine or sustainable farming trends where controlled action is critical.

Microencapsulation significantly lowers the risk of active loss, environmental exposure, and waste, which remain major concerns in processing settings. They also support improved bioavailability and easier scalability, especially for spray and emulsion grades, making them ideal for high-volume or premium products. As global innovation organizations push for wider controlled coverage and user-friendly materials, demand continues to expand across food & beverages, home & personal care, and construction.

High Development and Scalability Costs

High development and scalability costs present a significant barrier for companies advancing next-generation microencapsulation and novel delivery systems. Developing innovative methods such as High-NA spray, multi-core emulsions, or bio-based polymers requires extensive research, specialized reactors, and advanced drying technologies, all of which are far more expensive than basic blending. Stability is an even greater challenge as many premium capsules, pH-sensitive shells, and temperature-stable variants are sensitive to shear, moisture, and aggregation, requiring rigorous optimization to ensure they remain intact throughout production and use. Achieving long-term performance often requires costly stability trials, sophisticated particle testing, and high-grade excipients, significantly increasing R&D expenditures.

Meeting stringent regulatory expectations for release profiles, toxicity, and batch uniformity requires multiple validation studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled spray towers, specialized fluid beds, and quality-assurance systems, further driving up overall costs. For smaller formulators, these challenges can limit innovation or delay commercialization.

Developments in Bio-Based and Multi-Core Delivery Platforms

Developments in bio-based and multi-core microencapsulation delivery platforms are transforming the global ingredient landscape by addressing two major challenges: dependence on synthetic materials and release-control barriers. Bio-based platforms are engineered to achieve high renewable content, reducing reliance on petrochemicals and enabling green labeling in personal care. Innovations, such as alginate shells, chitosan coatings, starch encapsulation, and hybrid biopolymers, significantly improve sustainability and reduce toxicity, lowering compliance costs for brands and eco-campaigns.

Progress in multi-core platforms, including nested emulsions, coacervate capsules, layer-by-layer shells, and triggered-release systems, supports more precise delivery by stimulating sequential actives, the formulation’s first line of defense against degradation and inefficiency. These formats eliminate burst release, enhance protection, and allow versatile use without additional stabilizers, making them highly suitable for mass pharmaceutical programs. New technologies such as 3D-printed capsules, bio-adhesive polymers, and VLP-based carriers further enhance targeting and response.

Category-wise Analysis

Technology Type Insights

Spray technologies are anticipated to dominate the market, accounting for approximately 40% of the revenue share in 2026. Its dominance is driven by high throughput, uniform coating, and cost-effectiveness, making it preferred for powders. Spray technologies provide scalability, ensure precision, and contribute to yield, making them suitable for large-scale food campaigns. GEA Group Aktiengesellschaft is a global leader in spray-drying technology and supplies NIRO® spray-drying plants used extensively in the food and dairy industries. Their spray dryers are engineered to convert liquid products into uniform, free-flowing powders, such as milk powder, whey protein powder, and other food ingredient powders, by atomizing the liquid into fine droplets and rapidly drying them with hot air.

Emulsion is likely to be the fastest-growing segment, due to its versatility and expanding use in liquid actives. Its droplet profile makes them ideal for targeted release, reducing leakage. Continuous innovations in double emulsions are further strengthening their control, driving rapid adoption across North America and Europe, where demand for advanced, multi-phase encapsulation is accelerating. Secoya Technologies (based in Europe) develops the RayDrop® microfluidic emulsification platform, which enables precise production of single and double emulsions (e.g., water in oil in water) for encapsulation applications. This technology is used to generate monodispersed droplets and core-shell particles that improve encapsulation efficiency, stability, and controlled release of active ingredients such as APIs, bioactive.

Coating Material Insights

Polymers are expected to lead the market, holding approximately 35% of the market share in 2026, driven by biocompatibility, large-scale controlled-release programs, and strong global demand for versatile shells. Their dominance continues as formulators expand pharma applications. Rising adoption of lipid hybrids and expanded protein campaigns highlight the growing focus on natural alternatives. Evonik’s EUDRAGIT® polymer series is widely used for controlled-release and targeted drug delivery in pharmaceuticals. These polymers are engineered to encapsulate active pharmaceutical ingredients (APIs) within a polymeric shell that controls how and where the drug is released in the body, improving therapeutic efficacy and patient compliance. The EUDRAGIT® range is widely used in oral controlled-release tablet coatings and microcapsules that protect the API throughout the digestive tract and release it at the desired pH.

Proteins are likely to be the fastest-growing segment, due to strong momentum in natural encapsulation and expanding inclusion of edible shells in food. The growing shift toward bio-friendly, allergen-managed platforms, along with improved film formation, is accelerating adoption. Advancements in whey and gelatin hybrids and continued progress of plant proteins entering trials drive market growth. Balchem offers protein-based microencapsulation technologies (often using whey protein or dairy proteins) to protect and stabilize sensitive nutrients, probiotics, and bioactives in functional foods, beverages, and supplements. Their controlled-release systems help ensure that sensitive ingredients remain viable during processing and storage and are delivered effectively in the final product.

Application Insights

Pharmaceutical & healthcare products are expected to dominate the market, contributing nearly 40% of revenue in 2026, due to remaining the primary hub for controlled-release, large drug programs, and management of diverse actives requiring targeted delivery. Their strong integration, trained formulators, and ability to handle high-volume or sensitive blends drive higher consumption. The pharmaceutical sector is leading polymer rollouts and administering emerging lipid trials. Doxil® is a liposomal formulation of the chemotherapy drug doxorubicin. This product uses liposome-based microencapsulation to encapsulate the active drug within a protective lipid shell, which enables controlled release, enhanced bioavailability, reduced toxicity, and improved targeting to tumor tissues.

Food & beverages are likely to be the fastest-growing segment, driven by their strong flavor presence and expanding role in protected ingredients. They offer convenient, quick, and accessible masking, attracting producers who prefer stable, low-bitterness settings. Increased outreach programs, freshness focus, and wider availability of routine and premium capsules further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. Balchem Corporation is strengthening its position in the food & beverage microencapsulation market by announcing a new high-capacity manufacturing facility in Orange County, New York, scheduled to open in 2027. The 12-acre facility will significantly expand production of Balchem’s microencapsulated food ingredient solutions, including BakeShure®, ConfecShure®, and MeatShure®. These technologies are widely used in bakery, confectionery, and meat products to improve shelf life, texture, and processing efficiency.

Regional Insights

North America Microencapsulation Market Trends

North America is projected to lead, accounting for 35% of the market share in 2026, driven by the region’s advanced pharmaceutical infrastructure, strong research and development capabilities, and high public awareness of functional benefits. Processing systems in the U.S. and Canada provide extensive support for encapsulation programs, ensuring wide accessibility of microencapsulation across pharma, food, and personal care populations. Increasing demand for spray, convenient, and easy-to-incorporate forms is further accelerating adoption, as these formats improve efficacy and reduce barriers associated with unstable actives.

Innovation in microencapsulation technology, including stable multi-core, improved lipid delivery, and targeted bio-based enhancement, is attracting significant investment from both public and private sectors. Government initiatives and clean label campaigns continue to promote the use of ingredients against degradation, waste reduction, and emerging green threats, creating sustained market demand. The growing focus on protein grades and specialty uses, particularly for nutraceuticals and others, is expanding the target applications for microencapsulation.

Europe Microencapsulation Market Trends

The Europe microencapsulation market is growing due to increasing awareness of functional benefits, strong processing systems, and government-led sustainability programs. Countries such as Germany, France, and the U.K. have well-established frameworks that support routine encapsulation and encourage the adoption of innovative delivery methods, including microencapsulation. These stable formulations are particularly appealing for pharma populations, eco-conscious consumers, and food users, improving compliance and coverage rates.

Technological advancements in microencapsulation development, such as enhanced spray drying, application-targeted delivery, and improved bio-based grades, are further boosting market potential. European authorities are increasingly supporting research and trials for encapsulation against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, clean-label options aligns with the region’s focus on preventive health and waste reduction. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in polymers and novel variants to increase efficacy.

Asia Pacific Microencapsulation Market Trends

The Asia Pacific market is expected to grow the fastest in 2026, driven by rising industrial awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting encapsulation campaigns to address food preservation and emerging pharma needs. Microencapsulation is particularly attractive in these regions due to its scalable administration, ease of integration, and suitability for large-scale production drives in both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-deploy microencapsulation that can withstand challenging climatic conditions and minimize dependence loss. These innovations are critical for reaching remote facilities and improving overall efficacy coverage. Growing demand for food & beverages, agrochemicals, and pharmaceuticals applications is contributing to market expansion. Public-private partnerships, increased industrial expenditure, and rising investment in research and manufacturing capacity are further accelerating growth. The convenience of microencapsulation delivery, combined with improved protection and reduced risk of degradation, positions microencapsulation as a preferred choice.

Competitive Landscape

The global microencapsulation market features competition between established chemical leaders and emerging specialty encapsulators. In North America and Europe, BASF and DSM-Firmenich lead through strong R&D, distribution networks, and industry ties, bolstered by innovative polymers and delivery programs. In Asia Pacific, Roquette Frères advances with localized solutions, enhancing accessibility. Multi-core delivery boosts stability, cuts degradation risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Bio-based formulations solve sustainability issues, aiding penetration in green-focused areas.

Key Industry Developments

- In December 2025, Balchem Corporation announced plans to build a high-capacity facility in Orange County, New York, dedicated to advanced microencapsulated food ingredients. Scheduled to open in 2027, the 12-acre plant will expand production of BakeShure®, ConfecShure®, and MeatShure® solutions to meet growing global demand and support innovation, supply reliability, and customer service.

Companies Covered in Microencapsulation Market

- BASF

- DSM-Firmenich

- Givaudan

- Symrise

- Cargill, Incorporated

- FrieslandCampina

- DuPont

- AVEKA Group

- Encapsys, LLC

- TasteTech

- Balchem Corp.

- Others

Frequently Asked Questions

The global microencapsulation market is projected to reach US$13.0 billion in 2026.

The rising prevalence of controlled-release technologies and demand for stable ingredients are key drivers.

The microencapsulation market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Advancements in bio-based and multi-core delivery platforms are key opportunities.

BASF, DSM-Firmenich, Givaudan, Cargill Incorporated, and DuPont are the key players.