- Specialty & Fine Chemicals

- Methanesulphonic Acid (MSA) Market

Methanesulphonic Acid (MSA) Market Size, Share, and Growth Forecast, 2026 - 2033

Methanesulphonic Acid (MSA) Market by Grade (Technical Grade, Others), Form (Liquid, Solid/Flakes), End-user (Metal Finishing and Electro-plating, Others), and Regional Analysis for 2026 - 2033

Methanesulphonic Acid (MSA) Market Size and Trends Analysis

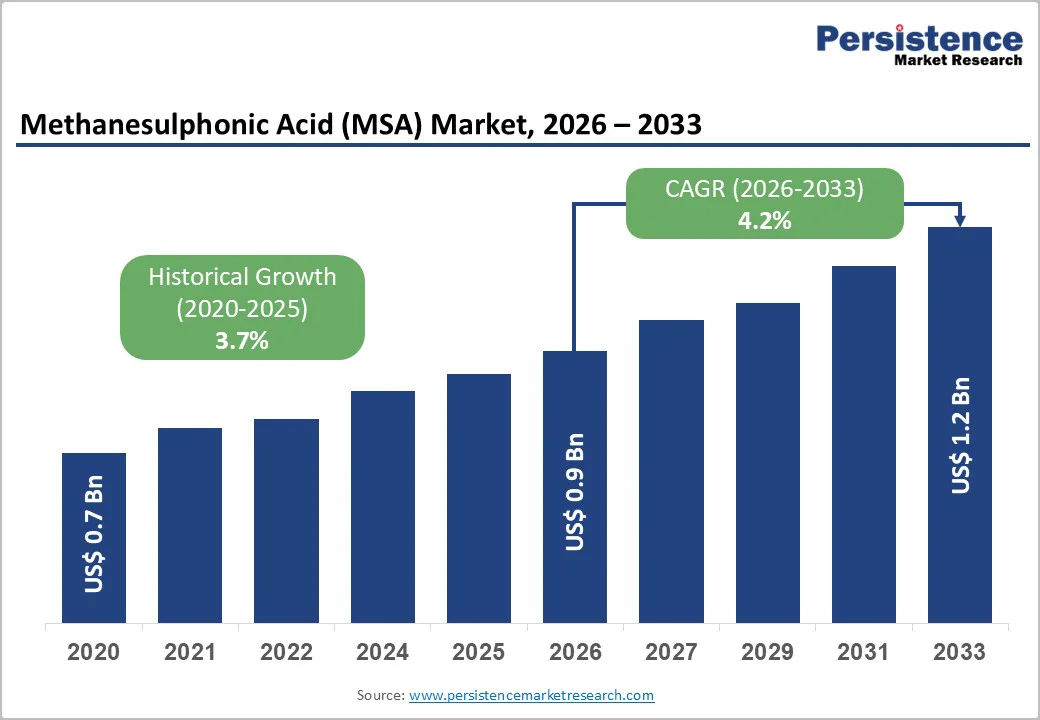

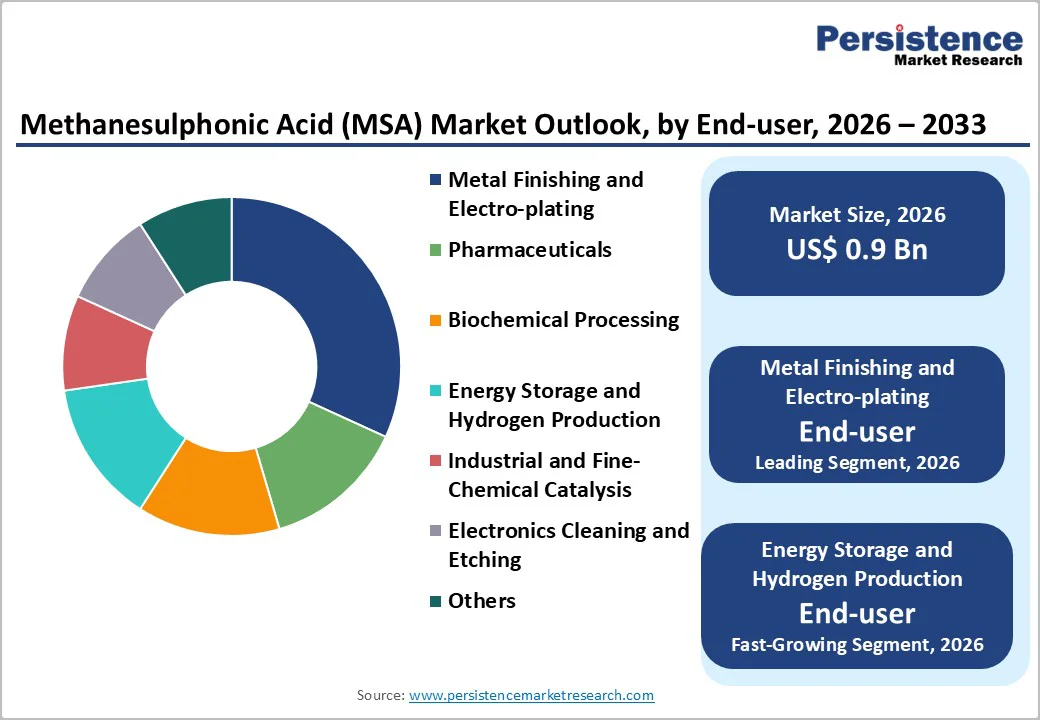

The global methanesulphonic acid (MSA) market size is likely to be valued at US$0.9 billion in 2026. It is expected to reach US$1.2 billion by 2033, growing at a CAGR of 4.2% from 2026 to 2033, driven by the increasing prevalence of eco-friendly alternatives to traditional acids, rising demand for high-purity catalysts in electroplating and electronics, and advancements in biodegradable formulations.

Surging demand for versatile, low-corrosion methanesulfonic acid (MSA), particularly in pharmaceuticals and energy storage, is driving adoption across industries. Advances in liquid and ultra-high-purity grades are further supporting uptake by delivering greater stability and efficiency. Growing recognition of MSA’s role in enabling sustainable processes in emerging regions continues to fuel market growth.

Key Industry Highlights:

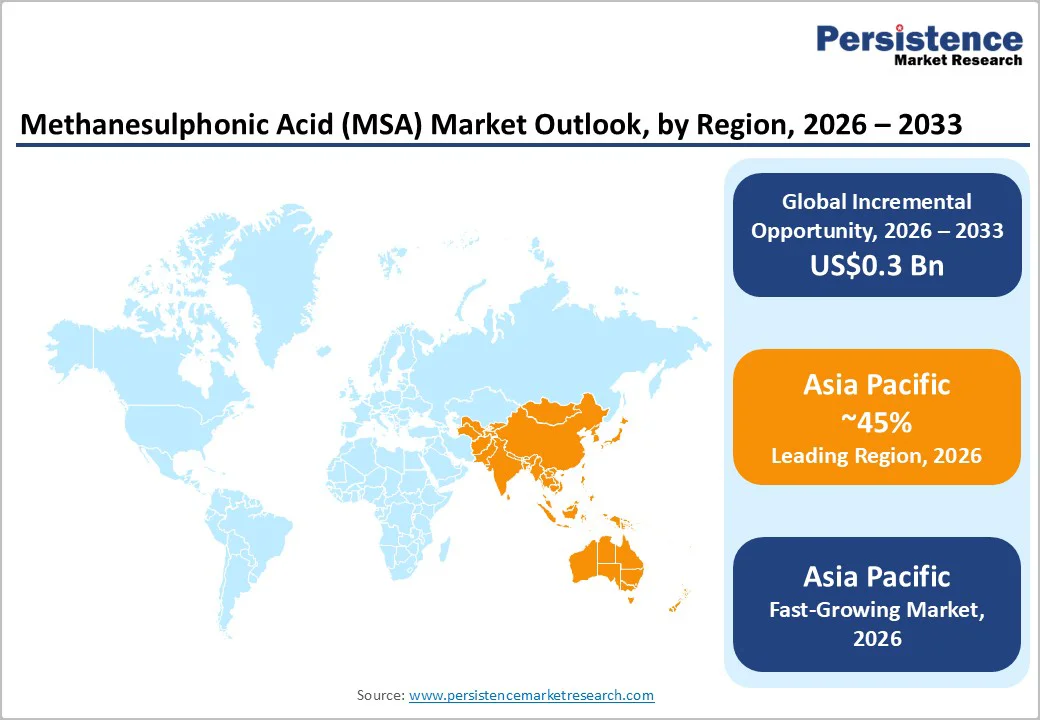

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by robust electronics manufacturing, expanding electroplating, and strong chemical production in China and India.

- Fastest-growing Region: Asia Pacific, fueled by industrialization, rising awareness of green chemistry, and growing investments in hydrogen production.

- Dominant Grade: Technical grade, to hold approximately 40% of the market share, as it provides cost-effective performance for industrial catalysis.

- Leading Form: Liquid accounts for over 70% of market revenue due to its ease of handling and precise dosing in plating baths.

- Leading End-user: Metal finishing and electroplating, contributing nearly 35% of the market revenue, due to superior conductivity and low toxicity.

| Key Insights | Details |

|---|---|

|

Methanesulphonic Acid (MSA) Market Size (2026E) |

US$0.9 Bn |

|

Market Value Forecast (2033F) |

US$1.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Eco-Friendly Alternatives and Demand for High-Purity Catalysts

The growing shift toward eco-friendly alternatives is creating a major opportunity for MSA producers, driven by stricter regulations favoring low-toxicity acids and reduced environmental impact. Conventional mineral acids often cause corrosion and waste challenges, particularly in electroplating and catalysis, resulting in higher disposal costs and compliance risks. Advanced MSA solutions, including liquid forms, solid flakes, ultra-high-purity grades, electronic etchants, and pharma-compliant variants, address these issues by providing a biodegradable, non-oxidizing alternative. These formats streamline processes, reduce reliance on neutralizers, and perform effectively in precision plating and hydrogen production where clean reactions are essential.

Methanesulfonic acid (MSA) also reduces the risk of metal contamination, effluent toxicity, and equipment damage, key concerns in industrial operations. Its recyclability and ease of handling, especially in liquid form, make it well-suited for high-volume and sensitive facilities. As sustainability initiatives and the adoption of green chemistry expand globally, demand for MSA continues to grow across metal finishing, pharmaceuticals, and energy storage applications.

Cost-Intensive Development and Purification Processes

High development and purification costs pose a major challenge for companies advancing next-generation methanesulfonic acid (MSA) and novel application systems. Producing specialized grades, such as ultra-high-purity liquids, pharmaceutical-grade solids, or low-impurity flakes, requires extensive R&D, specialized distillation, and advanced ion-exchange technologies, which are significantly more expensive than those used for conventional acids. Achieving and maintaining high purity is particularly demanding, as many refined variants, trace metals, reduced batches, and stabilizer-enhanced products are sensitive to moisture, temperature, and oxidation, necessitating rigorous optimization to ensure stability during storage and use.

Meeting long-term compliance standards often requires costly impurity trials, advanced HPLC testing, and high-grade membranes, substantially increasing R&D spending. Strict regulatory requirements related to heavy metal limits, biodegradability, and batch-to-batch consistency also require extensive validation studies under multiple conditions and in various production runs, adding time and cost to development. Scaling up production further requires controlled reactors, specialized drying systems, and robust quality assurance, which drive overall costs higher. For smaller producers, these barriers can restrict product diversification or delay commercialization.

Advancements in Biodegradable and Ultra-Pure Delivery Platforms

Advances in biodegradable and ultra-pure methanesulfonic acid (MSA) delivery platforms are reshaping the global chemical landscape by addressing two key challenges: toxicity concerns and impurity limitations. Biodegradable MSA, engineered to achieve up to 95% OECD biodegradability, reduces dependence on persistent mineral acids and supports green labeling in applications such as metal plating. Innovations, including ionic stabilization, solvent-free synthesis, crystal engineering, and hybrid formulations, improve environmental performance and lower effluent generation, helping industries reduce compliance costs.

Progress in ultra-pure MSA platforms, such as electronic-grade liquids, pharmaceutical-buffered solids, catalyst intermediates, and precision etching solutions, also enables more controlled reactions by ensuring high ion purity, a critical safeguard against defects and unwanted by-products. These advanced formats minimize contamination, improve yields, and support automated dosing without the need for highly skilled operators, making them well-suited for large-scale precision applications. Emerging technologies such as nano-filtration, bio-derived stabilizers, and VLP-based purification systems further enhance purity and performance.

Category-wise Analysis

Grade Insights

Technical-grade MSA is expected to lead the market, capturing around 40% of the market share in 2026. Its dominance is driven by cost-effectiveness, versatility, and reliability, making it the preferred choice for industrial catalysis. Technical-grade MSA delivers strong acidity, stable performance, and operational efficiency, making it ideal for large-scale plating and catalytic applications. For instance, it offers an optimal cost-to-performance balance for processes such as electroplating and industrial catalysis, supporting widespread adoption.

Ultra-high-purity MSA, on the other hand, is the fastest-growing segment due to its precision and rising use in electronics etching. Its ultra-low impurity profile makes it ideal for semiconductor cleaning, minimizing defects and ensuring process reliability. Ongoing advancements in purification technologies are enhancing quality and accelerating adoption, particularly in North America and Europe, where demand for high-specification, contaminant-free acids is increasing. In electronics, even trace impurities can disrupt sensitive processes in advanced semiconductor and printed circuit board (PCB) production, making ultra-high-purity MSA essential.

Form Insights

Liquid MSA is expected to dominate the market, accounting for approximately 70% of the market in 2026. Its leadership is driven by excellent solubility, ease of dosing, and convenient handling, making it the preferred choice for plating baths. Liquid MSA ensures uniform mixing, consistent performance, and operational safety, making it ideal for large-scale industrial applications. For instance, it is widely used as the electrolyte in commercial electroplating baths for metals such as tin, tin-lead, and nickel in high-value industries, including electronics and connectors. Being liquid at room temperature and highly soluble with metal methanesulfonates, it supports stable electrolyte solutions with high ionic conductivity, enabling efficient and uniform metal deposition in large-scale plating operations.

Solid or flake MSA represents the fastest-growing segment, driven by its compact form and increasing use in pharmaceutical formulations. The shift toward dry, stable products with longer shelf life is boosting adoption. Innovations in flake crystallization and the development of solid stabilizers are further fueling growth. For example, pharmaceutical APIs are often isolated as mesylate salts, solid crystalline forms that offer enhanced stability and easier manufacturability compared to liquids or amorphous compounds.

End-user Insights

Metal finishing and electroplating are expected to dominate the MSA market, capturing around 35% of the market in 2026, driven by the high volume of plating operations and a global focus on corrosion protection. Consistent bath maintenance, conductivity requirements, and the widespread use of tin-lead alternatives sustain steady demand. The increasing emphasis on electronics etching and energy storage further reinforces metal finishing’s market leadership. For instance, MSA-based electrolytes are widely used in electronics manufacturing to plate tin and tin-lead solder coatings on components and connectors, enhancing solderability and corrosion resistance, which are key for high-reliability applications in automotive, consumer electronics, and industrial equipment.

Energy storage and hydrogen production are the fastest-growing segments, fueled by rising demand for clean fuels, sensitivity to impurities, and the expanding use of electrolytic catalysts. Optimized concentrations, improved efficiency, and higher proton conductivity in electrolyzers are accelerating adoption. The increasing application of MSA in pharmaceuticals, biochemical processing, and other green energy sectors supports growth. For example, MSA solutions are used in both the positive and negative electrolytes of zinc-cerium hybrid redox flow batteries, achieving open-circuit potentials above +2.4 V at full charge, thereby enhancing energy density and efficiency for large-scale storage systems.

Regional Insights

North America Methanesulphonic Acid (MSA) Market Trends

North America’s MSA market is driven by the region’s advanced electronics infrastructure, strong R&D capabilities, and high awareness of the benefits of green chemistry. Well-established processing systems in the U.S. and Canada support broad application programs, ensuring easy access to MSA across plating, pharmaceutical, and energy sectors. Rising demand for ultra-high-purity, convenient, and easy-to-dose forms is further accelerating adoption, enhancing performance while lowering reliance on traditional alternatives.

Technological advancements in MSA, including stable purities, optimized catalytic delivery, and targeted biodegradability, are attracting substantial public and private investment. Government initiatives and sustainability campaigns continue to encourage its use as a safer alternative to conventional acids, reducing plating emissions and supporting emerging hydrogen applications. The increasing adoption of electronic-grade and industrial MSA, particularly in electronics and catalysis, is expanding the compound’s end-use potential.

Europe Methanesulphonic Acid (MSA) Market Trends

Europe’s MSA market in 2026 is driven by rising awareness of sustainability, robust chemical infrastructure, and government-led green initiatives. Countries, including Germany, France, and the U.K., have established industrial frameworks that support routine catalysis and encourage the adoption of advanced MSA delivery systems. These eco-friendly formulations are particularly attractive to plating operations, regulatory-conscious industries, and pharmaceutical users, enhancing compliance and coverage.

Advances in MSA technology, such as higher purity, application-specific delivery, and improved biodegradable grades, are further expanding market potential. European authorities are actively backing research and pilot programs for both standard and specialized acid applications, reinforcing market confidence. The growing focus on convenient, low-emission solutions aligns with the region’s preventive chemistry and waste-reduction goals. Public awareness campaigns and sustainability drives are expanding reach across urban and rural areas, while suppliers continue to invest in advanced distillation and high-purity formulations to boost efficacy.

Asia Pacific Methanesulphonic Acid (MSA) Market Trends

Asia Pacific is projected to be both the largest and fastest-growing MSA market in 2026, fueled by increasing industrial awareness, supportive government initiatives, and expanding application programs. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting chemical strategies to support electronics manufacturing and emerging hydrogen technologies. MSA is particularly favored in these regions for its versatility, scalability, and suitability for large-scale plating operations across urban and rural areas.

Advances in technology are enabling the production of stable, efficient, and easy-to-handle methanesulfonic acid that can withstand demanding manufacturing conditions while minimizing dependence on impurities. These innovations are crucial for servicing remote facilities and enhancing overall process efficiency. Rising demand from electronics, energy storage, and pharmaceutical sectors is driving market growth, while public-private partnerships, higher chemical investments, and increased spending on purification research and manufacturing capacity are accelerating adoption. The ease of MSA delivery, combined with improved performance and reduced corrosion risk, reinforces its position as a preferred choice.

Competitive Landscape

The global methanesulphonic acid (MSA) market is highly competitive, with established chemical giants and emerging specialty producers vying for market share. In North America and Europe, Arkema and BASF lead through strong R&D capabilities, extensive distribution networks, and deep industry connections, supported by innovative grades and targeted application programs.

In the Asia Pacific, Varsal drives growth with localized solutions that improve accessibility. High-purity MSA delivery enhances performance, reduces corrosion risks, and facilitates large-scale adoption across regions. Strategic partnerships, collaborations, and acquisitions are helping companies combine expertise, expand product portfolios, and accelerate commercialization. Eco-friendly formulations address toxicity concerns, supporting penetration in regulated sectors.

Key Industry Developments

- In February 2024, Alfa Aesar announced the development of a novel MSA-based catalyst for organic synthesis, designed to offer improved efficiency in pharmaceutical and fine chemical manufacturing.

Companies Covered in Methanesulphonic Acid (MSA) Market

- Sipcam Oxon Spa

- Arkema

- Avantor, Inc.

- Hydrite Chemical

- VARSAL

- Tokyo Chemical Industry (India) Pvt. Ltd.

- Thermo Fisher Scientific Inc.

Frequently Asked Questions

The global methanesulphonic acid (MSA) market is projected to reach US$0.9 billion in 2026.

The rising prevalence of eco-friendly alternatives and demand for high-purity catalysts are key drivers.

The methanesulphonic acid (MSA) market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Advancements in biodegradable and ultra-pure delivery platforms are the key opportunities.

Arkema, BASF, Varsal, Hydrite Chemical, and Avantor, Inc. are the key players.