- Non-food Packaging

- MDO-PE Film Market

MDO-PE Film Market Size, Share, and Growth Forecast, 2026 - 2033

MDO-PE Film Market by Material Type (High-density Polyethylene (HDPE), Others), Packaging Formats (Pouches, Others), End-user (Food, Hygiene, Beverages, Others), and Regional Analysis for 2026 - 2033

MDO-PE Film Market Size and Trends Analysis

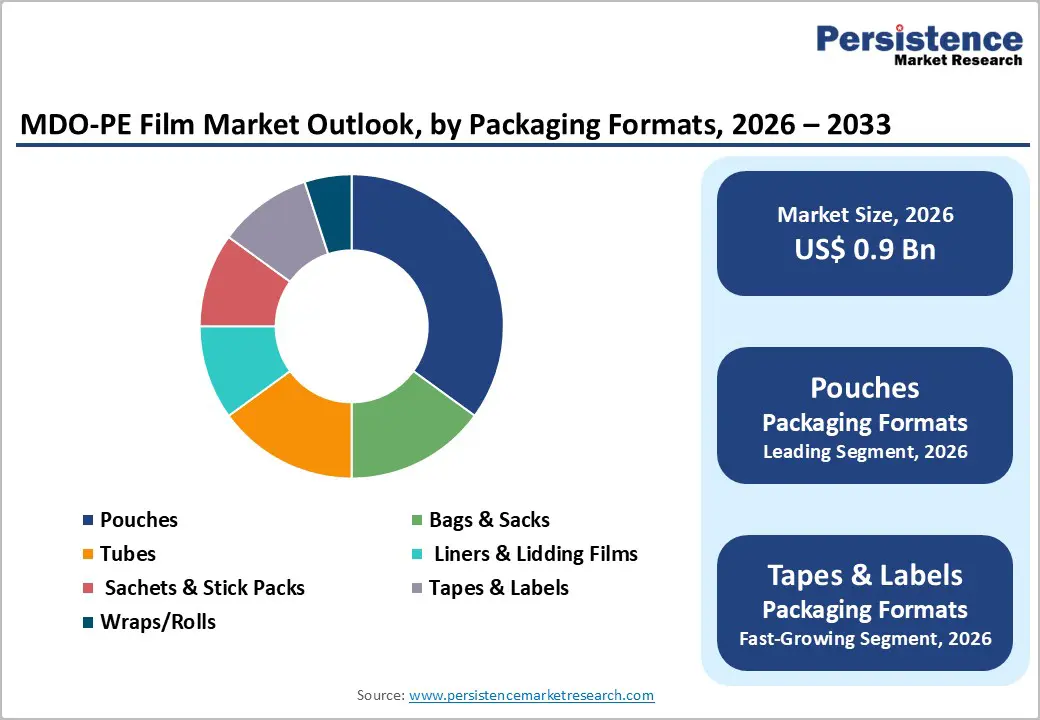

The global MDO-PE film market size is likely to be valued at US$0.9 billion in 2026, and is expected to reach US$1.2 billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of sustainable flexible packaging requirements, rising demand for high-stiffness mono-material polyethylene films in food and hygiene applications, and advancements in machine-direction orientation (MDO) processing technologies.

Growing demand for recyclable, high-performance MDO-PE films, particularly HDPE and LLDPE grades for pouches and labels, is accelerating adoption among end users. Advances in downgauging and enhanced barrier properties are further boosting uptake by offering material savings and recyclability compliance. Increasing recognition of MDO-PE film as critical for lightweight, circular-economy packaging in emerging FMCG and e-commerce markets remains a major driver of market growth.

Key Industry Highlights:

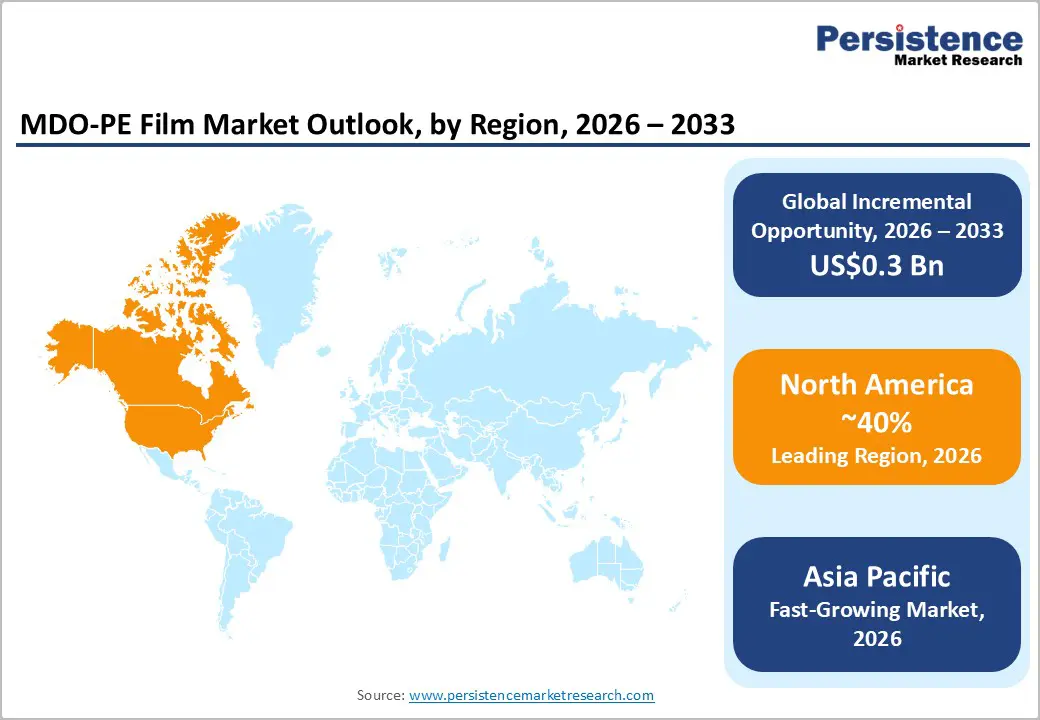

- Leading Region: North America is projected to lead the market, accounting for 40% of revenue in 2026, driven by its advanced flexible packaging ecosystem, strong R&D, and high recyclability awareness. HDPE and easy-to-convert formats are accelerating MDO-PE adoption across food, hygiene, and homecare.

- Fastest-growing Region: Asia Pacific, fueled by rapid FMCG growth, expanding e-commerce packaging volumes, and growing investments in MDO-PE capacity in China and India.

- Dominant Material Type: High-density polyethylene (HDPE), to hold approximately 45% of the market share, as it provides the highest stiffness and yield.

- Leading Packaging Formats: Pouches, accounting for over 40% of market revenue, due to their dominance in food and home care flexible packaging.

- Leading End-user: Food, contributing nearly 38% of market revenue due to the large volume of stand-up pouches and flow-wrap applications.

| Key Insights | Details |

|---|---|

| MDO-PE Film Market Size (2026E) | US$0.9 Bn |

| Market Value Forecast (2033F) | US$1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Sustainable Flexible Packaging and High-Stiffness Mono-Material Solutions

The demand for sustainable flexible packaging is accelerating as brand owners, retailers, and regulators push for packaging formats that reduce environmental impact while maintaining performance. Flexible packaging already offers advantages such as lightweight structures, lower transportation-related emissions, and reduced material use compared with rigid alternatives. The next phase of demand is driven by the shift toward high-stiffness monomaterial solutions, designed to improve recyclability without compromising functionality.

Traditionally, flexible packaging relied on multilayer laminates to provide stiffness, barrier protection, and shelf appeal; however, these structures are difficult to recycle. Mono-material packaging, typically based on polyethylene or polypropylene, addresses this challenge by using a single polymer family, making mechanical recycling more efficient and scalable. Advances in resin formulation, film orientation, and coating technologies have enabled mono-material films to deliver higher stiffness, improved heat resistance, and enhanced barrier properties, allowing them to replace complex laminates in applications such as food pouches, sachets, and stand-up packs.

High Capital Intensity and Technical Complexity of MDO Lines

Machine Direction Orientation (MDO) lines are increasingly used to produce high-performance mono-material films, but their adoption is constrained by high capital intensity and significant technical complexity. Installing an MDO line requires substantial upfront investment in specialized stretching units, precision rollers, advanced temperature control systems, and high-speed automation. In addition to the core equipment, manufacturers must invest in plant modifications, energy-efficient utilities, and downstream-conversion compatibility, thereby increasing the total project cost. For small and mid-sized film producers, these costs can create financial risk and long payback periods, especially in markets with price-sensitive customers.

Beyond capital requirements, operating MDO lines demands advanced technical expertise. Achieving consistent orientation without film breakage requires precise control of draw ratios, heat profiles, and line speeds. Minor deviations can lead to defects such as uneven thickness, curl, or loss of mechanical strength, directly impacting yield and production efficiency. The complexity increases further when processing recycled or downgauged materials, which often have variable melt properties and narrower processing windows.

Developments in Mono-Material Structures and High-Barrier MDO-PE Platforms

Ongoing innovation in mono-material packaging and high-barrier MDO-PE (Machine-Direction-Oriented Polyethylene) platforms is transforming flexible packaging by overcoming traditional limitations in performance and recyclability. High barrier and stiffness requirements were met using multilayer, multipolymer laminates, which limited recyclability. Advances in MDO-PE technology now allow polyethylene-based films to deliver enhanced mechanical strength, improved stiffness, and downgauged structures while remaining within a single polymer family.

Material innovations have played a critical role in this shift. New PE resin blends, combined with optimized orientation ratios, yield films with higher tensile strength and controllable shrinkage properties. These improvements support the replacement of PET-PE or PET-CPP laminates in applications such as stand-up pouches, flow wraps, and sachets. In parallel, developments in thin, PE-compatible barrier coatings and EVOH-based interlayers have significantly improved oxygen and moisture barrier performance without compromising mono-material recyclability. Process-level enhancements are also accelerating adoption. Better temperature management, inline coating capabilities, and advanced surface treatments have improved printability, seal integrity, and machinability on high-speed packaging lines.

Category-wise Analysis

Material Type Insights

High-density Polyethylene (HDPE) is expected to lead the market, holding approximately 45% of the share in 2026, propelled by its strong balance of performance, cost efficiency, and sustainability benefits. HDPE offers high stiffness, excellent tensile strength, and good chemical resistance, making it suitable for both rigid and flexible packaging applications. Its lightweight nature supports material reduction and lower transportation emissions. HDPE is widely accepted within the existing recycling streams, aligning well with mono-material packaging strategies. Berry Global Group, Inc. produces high-density polyethylene (HDPE) bottles that incorporate post-consumer recycled HDPE for personal care and home product packaging. These containers are designed to be fully recyclable in regions with existing local recycling systems, demonstrating how HDPE’s recyclability and versatility support sustainable packaging strategies while meeting performance requirements.

Linear low-density polyethylene (LLDPE) is expected to be the fastest-growing material, thanks to its unique combination of flexibility, strength, and excellent film-forming properties. This makes it increasingly favored over traditional LDPE in various applications. LLDPE’s superior tensile strength and puncture resistance enable manufacturers to produce thinner, lighter films without compromising durability, thereby reducing material usage and costs while enhancing performance. LLDPE films are particularly dominant in packaging, especially in flexible food wraps, pouches, and stretch films, and their use is expanding as e-commerce and convenience packaging continue to grow. Ergis S.A., a leading European plastics company, produces LLDPE-based stretch films widely used in industrial packaging, including pallet wraps and load containment films. These products leverage LLDPE’s higher tensile strength and puncture resistance, offering improved performance compared to traditional LDPE films and helping companies better protect goods during transit.

Packaging Formats Insights

Pouches are projected to lead the market, accounting for 40% of the market in 2026, owing to their combination of functionality, cost efficiency, and consumer convenience. They offer excellent shelf presence, easy-to-open features, and a lightweight structure, which reduces material use and transportation costs. Pouches can be engineered for resealability, portion control, and extended shelf life, making them ideal for food, pet care, and personal-care products. Their flexibility supports a range of filling and sealing technologies, and they are compatible with emerging sustainable materials, such as monolithic polymer films. Amcor plc is a major producer of flexible pouch packaging used widely across the food and consumer goods sectors. In 2024, Amcor partnered with Stonyfield Organic to develop a fully polyethylene-based spouted pouch for refrigerated yogurt that eliminates metalized layers while maintaining performance, highlighting how pouch formats are being engineered for convenience and sustainability.

The tapes and labels segment is expected to be the fastest-growing packaging format, as it serves a critical function across virtually all industries while adapting to evolving supply chain and branding requirements. Growth is being fueled by the rise of e-commerce and automated logistics, where sturdy tapes ensure secure carton sealing and labels provide essential tracking, branding, and regulatory information. Innovations in adhesive technology and printable materials have further expanded functionality. Features such as water-resistant labels, tamper-evident tapes, and smart tracking codes enhance both protection and data capture. Avery Dennison Corporation, a global leader in pressure-sensitive materials, has experienced increased demand for its labeling and packaging solutions, including self-adhesive labels and specialty tapes, as clients restock inventories and expand product rollouts. In 2024, the company reported stronger-than-expected earnings growth, driven in part by higher label volumes sold to brand owners in the retail and logistics sectors, highlighting the growing reliance on labels for branding, compliance, and supply chain management.

End-user Insights

The food sector is projected to dominate the market, accounting for nearly 38% of revenue by 2026. This is due to its continued role as the primary end user of flexible pouches and large FMCG programs, and to the management of a wide range of products that require lightweight, recyclable packaging. Strong integration, skilled converters, and the ability to handle both high-volume and premium blends are driving higher consumption in this segment. The food industry is also at the forefront of HDPE rollouts and the adoption of emerging LLDPE technologies. Tetra Pak International S.A., a global leader in food packaging solutions, provides cartons and processing systems for dairy, juices, soups, and other perishable foods worldwide. Through its advanced material science, aseptic technology, and integrated filling machines, Tetra Pak helps food brands extend shelf life while ensuring safety and convenience for consumers.

The hygiene segment is expected to be the fastest-growing end-user category, driven by the increasing consumer focus on cleanliness, health, and personal care. This growing awareness is boosting demand for products such as baby wipes, sanitary napkins, diapers, and disinfectant wipes, which require specialized packaging to maintain product integrity, prevent contamination, and enhance convenience. Flexible pouches, resealable packs, and flow wraps are becoming more popular for supporting on-the-go use while maintaining hygiene standards. The expansion of healthcare and improvements in living standards in emerging markets are further fueling demand for hygiene-related products. Kimberly-Clark Corporation, a leading provider of hygiene products, has seen sustained strong demand for key items such as Huggies diapers and Kleenex tissues. This reflects the broader trend of hygiene products driving packaging growth, as consumers increasingly prioritize cleanliness and health in their daily essentials.

Regional Insights

North America MDO-PE Film Market Trends

North America is projected to lead the market, accounting for 40% of revenue in 2026, driven by the region’s advanced flexible packaging ecosystem, strong research and development capabilities, and high public awareness of recyclability benefits. Converting systems in the U.S. and Canada provide extensive support for MDO-PE programs, ensuring broad accessibility across food, hygiene, and home care populations. The increasing demand for HDPE, convenient, and easy-to-convert forms further accelerates adoption, as these formats improve yield and reduce barriers associated with multi-material structures.

Innovation in MDO-PE film technology, including stable downgauging, improved printability and delivery, and targeted mono-material enhancement, is attracting significant investment from both the public and private sectors. Government initiatives and EPA campaigns continue to promote the use of waste risks, landfill constraints, and emerging circular-economy threats, creating sustained market demand. The growing focus on hygiene grades and specialty uses, particularly for e-commerce and others, is expanding the target applications for MDO-PE film.

Europe MDO-PE Film Market Trends

Europe's market growth is expected to be driven by increasing awareness of the benefits of mono-materials, robust regulatory frameworks, and government-led initiatives promoting circular packaging. Countries, including Germany, France, Italy, and the U.K., have well-established conversion infrastructure that facilitates the regular use of MDO-PE and encourages the adoption of innovative film-delivery solutions, including MDO-PE film. These recyclable formulations are particularly attractive to the food sector, regulation-conscious brands, and hygiene product manufacturers, as they enhance sortability and improve recycling rates.

Technological advancements in MDO-PE film, such as improved orientation, targeted application delivery, and higher stiffness grades, are further expanding market potential. European authorities are increasingly supporting research and trials for both standard and specialized film applications, boosting market confidence. The growing focus on convenient, low-waste solutions aligns with the region’s push for packaging transitions to reduce plastic pollution. Public awareness campaigns are extending their reach in both urban and rural areas, while suppliers are investing in resins and innovative variants to enhance effectiveness.

Asia Pacific MDO-PE Film Market Trends

Asia-Pacific is likely to be the fastest-growing market for MDO-PE film in 2026, driven by rising packaging awareness, expanding government initiatives, and growing application programs across the region. Countries such as China, India, Japan, and Indonesia are actively promoting film campaigns to address FMCG growth and emerging e-commerce needs. MDO-PE film is particularly attractive in these regions due to its cost-effective manufacturing, ease of conversion, and suitability for large-scale flexible packaging applications among both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and readily convertible MDO-PE films that withstand challenging climatic conditions and minimize gauge dependence. These innovations are critical for reaching domestic converters and improving overall packaging coverage. Growing demand for food, hygiene, and beverage applications is contributing to market expansion. Public-private partnerships, increased FMCG expenditure, and rising investment in MDO-PE research and manufacturing capacity are further accelerating growth. The convenience of film delivery, combined with improved stiffness and reduced risk of failure, positions MDO-PE film as a preferred choice.

Competitive Landscape

The global MDO-PE film market features competition between established flexible packaging leaders and emerging mono-material specialists. In North America and Europe, Coveris Holdings Inc. and Avery Dennison Corporation lead through strong R&D, distribution networks, and brand partnerships, bolstered by innovative high-stiffness and recyclable programs. In Asia Pacific, Plasbel Plásticos S.A.U. advances with localized solutions, enhancing accessibility. Mono-material delivery boosts recyclability, cuts sorting risks, and enables mass integrations across converters. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. High-stiffness formulations solve performance issues, aiding penetration in downgauging areas.

Key Industry Developments

- In July 2025, COLINES® was recognized for its pioneering work in Cast MDO-PE film production, a key innovation in flexible packaging. This milestone followed the launch of fully mono-material, PE-based stand-up pouches at the 2022 K Show in Düsseldorf. These pouches featured an innovative lamination of Cast MDO-PE and Cast PE films. COLINES® then advanced further with mono-film solutions, optimizing the benefits of Cast MDO-PE by providing an efficient sealing side and a high-quality print side with exceptional optical properties, including low haze and superior gloss.

- In June 2025, RKW Group introduced the next generation of sustainable PE plastic films, RKW Horizon®, utilizing the latest MDO technology. Paired with RKW ProTec sealing films, the solution offered recyclable, sustainable packaging for various formats and industries. The company set new standards in sustainability and functionality for flexible packaging with its expanded RKW Horizon® MDO-PE product line, which now includes films with an integrated EVOH barrier, enhancing performance while maintaining recyclability.

Companies Covered in MDO-PE Film Market

- Coveris Holdings Inc.

- Avery Dennison Corporation

- Saes Coated Films S.p.A.

- Lenzing Plastics GmbH & Co. KG

- RKW Group

- Nowofol

- Klöckner Pentaplast Group

- Camvac Limited

- Plasbel Plásticos S.A.U.

- Novel Packaging Inc.

- Polysack Flexible Packaging Ltd.

- Polythene UK Ltd.

Frequently Asked Questions

The global MDO-PE film market is projected to reach US$0.9 billion in 2026.

Rising demand for sustainable flexible packaging and high-stiffness mono-material solutions are the key drivers.

The MDO-PE film market is poised to witness a CAGR of 4.6% from 2026 to 2033.

Mono-material structures and high-barrier MDO-PE platforms are the key opportunities.

Coveris Holdings Inc., Avery Dennison Corporation, RKW Group, Lenzing Plastics GmbH & Co. KG, and Plasbel Plásticos S.A.U. are the key players.