- Hardware & Software IT Services

- Master Data Management Market

Master Data Management Market Size, Share, and Growth Forecast 2026 – 2033

Master Data Management Market by Component Type (Solution and Services), by Deployment Mode (Cloud and On-premise), and End- user (BFSI, Government, Retail, IT & Telecommunication, Healthcare and Others) and Regional Analysis for 2026 – 2033

Market Overview

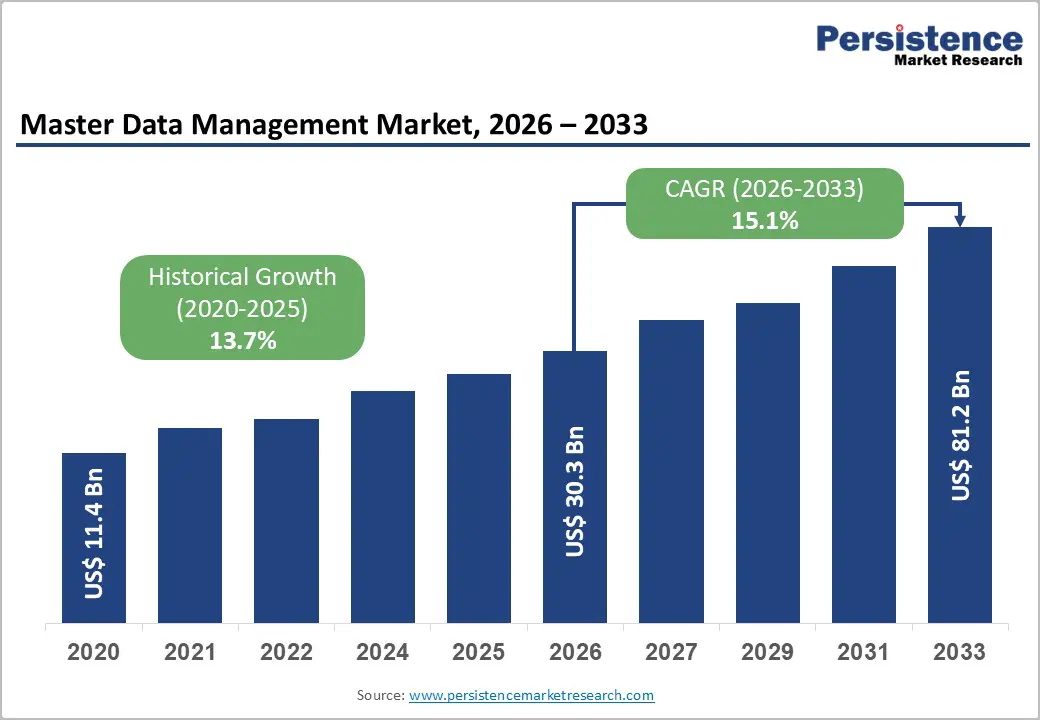

The global Master Data Management (MDM) market size was valued at US$30.3 billion in 2026 and is projected to reach US$81.2 billion by 2033, growing at a CAGR of 15.1% between 2026 and 2033. The fundamental driver of this growth is enterprises' critical need to consolidate fragmented data from multiple operational systems and establish unified, authoritative sources of truth for strategic decision-making. Organizations increasingly recognize that master data governance directly impacts operational efficiency, regulatory compliance, and competitive advantage in data-driven markets.

Key Market Highlights

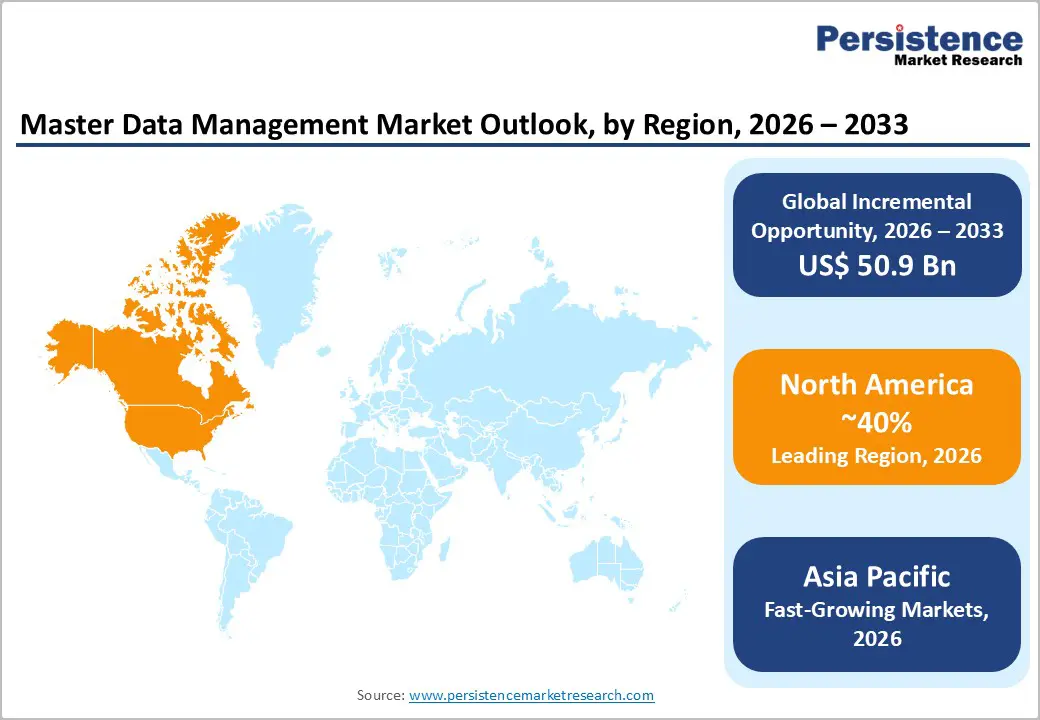

- Leading Region: North America dominates the Master Data Management market with approximately 40% market share, reflecting early digital transformation adoption, advanced cloud migration maturity, substantial enterprise IT investments in modern data governance infrastructure, and concentrated innovation across Informatica, Oracle, IBM, SAP, and specialized MDM vendors serving BFSI, healthcare, retail, and technology sectors with comprehensive governance solutions.

- Fastest Growing Region: Asia-Pacific demonstrates the fastest growth trajectory at 18.4 % CAGR, reflecting rapid industrialization, manufacturing-centric digital transformation, enterprise cloud adoption across China, India, Japan, and ASEAN, and emerging demand for governance frameworks supporting complex supply chain data management and operational excellence initiatives.

- Dominant Segment: Cloud-based MDM deployment architectures maintain market dominance with approximately 58 % market share, reflecting enterprise preference for scalable, cost-efficient SaaS consumption models that eliminate expensive on-premises infrastructure investments while enabling real-time analytics and seamless cloud data warehouse integration for advanced analytics and AI initiatives.

- Fastest Growing Segment: Services including consulting, implementation, training, managed services, and ongoing governance support represent the fastest-growing component category, expanding at 19.63 % CAGR as organizations require specialized expertise, comprehensive change management, and sustained governance support to maximize MDM investment value and drive organizational adoption.

- Key Market Opportunity: AI-driven automation and intelligent data management represent the most significant future growth opportunity, with organizations implementing AI-enhanced MDM solutions achieving substantial improvements in data quality metrics, dramatic reductions in manual stewardship effort, accelerated time-to-value for analytics and AI initiatives, and measurable competitive advantage through superior data-driven decision-making capabilities

| Global Market Attributes | Key Insights |

|---|---|

| Master Data Management Market Size (2026E) | US$ 30.3 Bn |

| Market Value Forecast (2033F) | US$ 81.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.1% |

| Historical Market Growth (CAGR 2020 to 2024) | 13.7% |

Market Dynamics

Market Growth Drivers

Accelerating Cloud Enterprise Resource Planning Migrations and Multi-Cloud Architecture Adoption

Organizations are migrating enterprise resource planning systems to cloud environments at unprecedented velocity, with approximately 66 % of ERP implementations selecting cloud delivery models in 2024. Cloud-based ERP migrations necessitate comprehensive master data reconciliation, cleansing, and consolidation across legacy and modern systems to eliminate data inconsistencies that compromise reporting accuracy and operational efficiency. Mid-market manufacturing, distribution, and retail organizations are particularly aggressive in adopting cloud ERP platforms, projected to grow at 21.3 % CAGR, creating immediate demand for scalable MDM solutions that integrate seamlessly with cloud data platforms including Snowflake, Databricks, and Microsoft Fabric. Cloud-native MDM architectures provide flexible, elastic governance capabilities supporting multi-region deployments and reducing infrastructure capital expenditure while enabling real-time data synchronization and analytics-ready master data delivery for emerging use cases, including artificial intelligence model development and personalization initiatives.

Regulatory Mandates and Compliance Framework Expansion Across Geographic Regions

Financial services, healthcare, and government organizations face escalating regulatory requirements that mandate sophisticated data governance frameworks and transparent data lineage capabilities. The General Data Protection Regulation (GDPR) enforced across European Union member states since 2018 establishes strict requirements for personal data protection, consent management, and breach notification procedures that necessitate centralized master data management. Concurrently, financial services organizations must maintain compliance with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations, which require accurate customer identity data, consolidated transactional history, and comprehensive audit trails. Healthcare organizations across North America are responding to interoperability mandates and quality improvement programs by implementing MDM platforms to unify patient records, provider credentials, and clinical reference data, with regulatory penalties ranging from millions to tens of millions of dollars, depending on violation severity and data breach scope.

Market Restraints

Complex Legacy System Integration Requirements and Implementation Timeline Extensions

Organizations attempting MDM implementations encounter substantial integration complexity due to heterogeneous technology landscapes that combine decades-old mainframe systems, mid-range platforms, cloud applications, and newer SaaS solutions, requiring careful data mapping and validation protocols. Approximately 67% of enterprises report experiencing data quality degradation during cloud migration, with inconsistent data definitions across source systems complicating automated matching and reconciliation logic. The typical large enterprise manages data across 15 to 23 distinct business applications, generating customer, product, supplier, and financial master data in multiple formats, requiring specialized integration expertise and extended implementation timelines spanning 12 to 24 months, depending on organizational complexity and data domain scope.

Severe Talent Shortage in Specialized Data Governance and MDM Architecture Roles

Global shortage of qualified data architects, data stewards, master data management specialists, and data governance professionals creates significant barriers to MDM program execution, particularly for mid-market organizations lacking dedicated data management functions. Cloud transformation initiatives are simultaneously competing for scarce data engineering talent, intensifying recruitment challenges and driving compensation escalation that strains organizational budgets. Organizations struggle to allocate experienced resources to governance model definition, data quality assessment, change management, and ongoing stewardship workflows, resulting in suboptimal MDM implementations that fail to deliver anticipated business value or organizational adoption.

Market Opportunities

Generative Artificial Intelligence Integration Driving Data Quality as Competitive Differentiator

Integration of generative AI and large language models into MDM platforms creates transformative opportunities for automating data quality improvements, entity resolution, data enrichment, and policy enforcement at unprecedented scale and accuracy. Healthcare and financial services organizations are achieving 80% data-matching accuracy by combining ChatGPT-style enrichment capabilities with MDM platforms, dramatically reducing manual data stewardship effort and accelerating time-to-insight for analytics teams. Informatica's Fall 2025 release, introducing CLAIRE Copilot for MDM with natural language query capabilities and AI Agent Hub, demonstrates vendor momentum in delivering conversational interfaces that democratize data governance for non-technical business users.

Industry-Specific SaaS Solutions and Vertical Domain Specialization Creating Rapid Deployment Opportunities

Specialized MDM vendors are capturing market share by delivering pre-configured, industry-specific solutions optimized for unique business requirements in retail, healthcare, manufacturing, life sciences, and automotive sectors. Retail organizations increasingly require integrated Product Information Management (PIM) capabilities embedded within MDM platforms to synchronize product master data across omnichannel distribution networks, e-commerce platforms, and supply chain partners, with Syndigo recognized as the industry leader in this domain. Healthcare organizations deploying cloud-based MDM platforms for patient identity management, provide directory consolidation, and clinical reference data governance can eliminate duplicate patient records, improve clinical interoperability compliance, and accelerate Healthcare Effectiveness Data and Information Set (HEDIS) quality metric achievement, generating 15 to 20 % administrative cost savings through reduced reconciliation effort and improved billing accuracy.

Category-wise Insights

Component Analysis

Software solutions maintain dominant market positioning with approximately 63 % market share, reflecting enterprise reliance on MDM software platforms as foundational infrastructure for enterprise data governance. MDM software solutions deliver critical capabilities including automated data matching, duplicate detection, entity resolution, data quality validation, and survivorship rules that establish authoritative golden records for customer, product, and supplier master data domains. Continuous vendor innovation in AI-powered data matching, real-time data synchronization, and low-code governance workflow configuration strengthens the solutions segment's strategic importance as organizations prioritize rapid implementation and measurable business value realization. Software dominance reflects a fundamental market structure where technology platforms enable organizations to establish centralized governance capabilities spanning customer 360-degree views, supplier master management, product catalog standardization, and financial reference data consolidation.

Deployment Mode Analysis

Cloud-based MDM deployment captured approximately 58 % market share in 2026, reflecting a comprehensive enterprise shift toward SaaS consumption models offering superior scalability, flexibility, and economic efficiency compared to on-premises deployments. Cloud MDM platforms eliminate substantial capital infrastructure investments, support elastic scaling for growing data volumes, enable rapid feature deployment through continuous software updates, and provide seamless integration with modern cloud data warehouses and analytics platforms. Product innovations including subscription-based pricing models, pre-built industry accelerators, and managed professional services have substantially reduced implementation complexity and total cost of ownership, accelerating adoption among mid-market organizations previously constrained by expensive on-premises deployments. Cloud platforms support data residency requirements through regional deployment configurations, security-hardened access controls, and encryption standards that meet GDPR, HIPAA, and sector-specific compliance mandates essential to regulated industries.

End-User Analysis

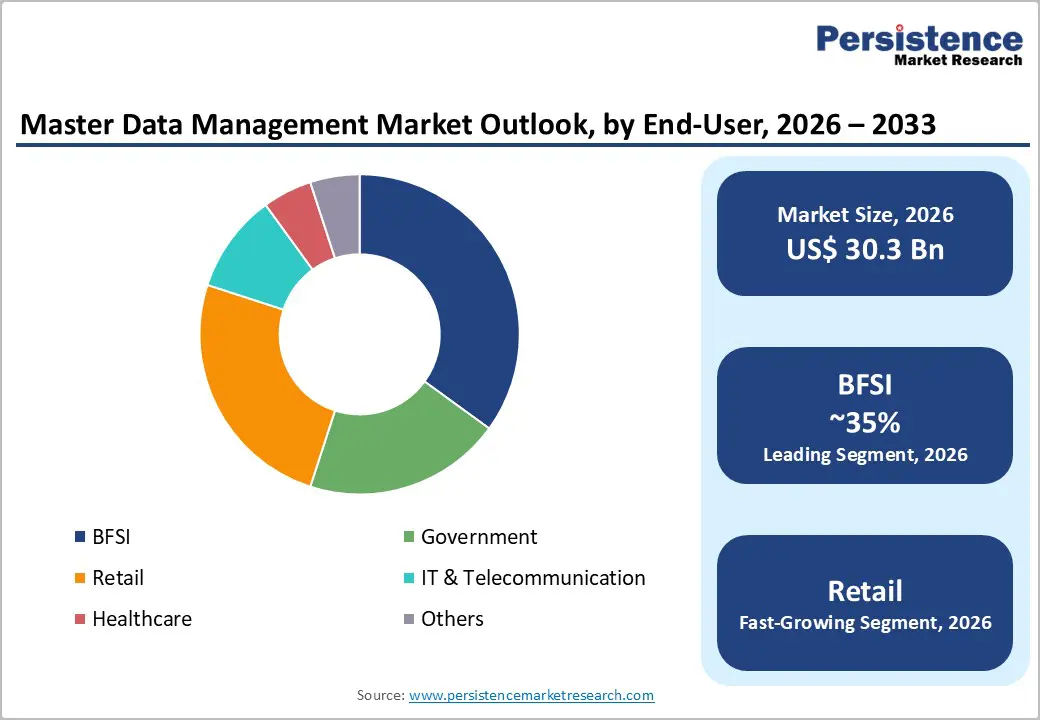

Banking, Financial Services, and Insurance (BFSI) sector maintains market leadership among end-user segments, driven by foundational reliance on accurate, consistently governing customer and account data for regulatory compliance, risk management, and customer experience optimization. Financial institutions manage vast volumes of customer, account, product, and transactional data subject to stringent regulatory oversight including KYC/AML compliance, regulatory capital requirements, open banking regulations, and anti-fraud requirements that necessitate enterprise-grade MDM governance. Robust MDM implementations within financial services organizations enable consolidated customer 360-degree views supporting cross-sell and upsell opportunities, improved lending decision accuracy through better customer financial history visibility, enhanced fraud detection through consolidated transaction analysis across accounts and products and accelerated statutory reporting compliance through unified reference data and financial data governance.

Regional Insights

North America

North America maintains market leadership position with approximately 42 % market share, driven by exceptionally mature digital transformation adoption, advanced cloud migration programs, and substantial organizational investments in modern data governance infrastructure. The region benefits from early implementation of cloud-based enterprise applications including Salesforce, SAP S/4HANA, and Oracle Cloud Infrastructure, creating dependent demand for comprehensive MDM platforms to consolidate data across cloud and hybrid environments. Regulatory frameworks including HIPAA (healthcare), GLBA (financial services), and CCPA (consumer privacy) establish strict data governance requirements driving enterprise MDM investments as foundational compliance infrastructure. Informatica's announcement of Fall 2025 release featuring agentic AI capabilities and seamless integration with Salesforce Agentforce demonstrates vendor innovation concentrated in North America addressing customer demands for AI-ready data governance.

Europe Master Data Management Trends

Europe's MDM market expansion is fundamentally shaped by stringent data protection regulations including General Data Protection Regulation (GDPR) and emerging frameworks including European Health Data Space (EHDS) enabling cross-border healthcare information exchange with enhanced governance safeguards. Organizations across Germany, United Kingdom, France, and Spain have prioritized MDM implementation as strategic compliance infrastructure enabling GDPR-compliant consent management, data subject rights fulfillment, automated breach notification, and cross-border data transfer governance. Healthcare providers across European Union member states face pressure to standardize patient data management and clinical data governance to support interoperability initiatives, with approximately 96 % of General Practitioners in Europe utilizing Electronic Health Records (EHRs) that require consistent master data governance. Financial institutions in European markets are investing heavily in MDM platforms to support GDPR compliance, implement robust consent management, and maintain transparent data processing records demonstrating lawful basis for personal data handling across customer relationship and risk management systems.

Asia Pacific Master Data Management Trends

Asia-Pacific represents the fastest-growing regional market segment, with MDM adoption accelerating at 18.4 % CAGR driven by rapid industrial digitalization, manufacturing sector transformation, and enterprise cloud adoption across China, Japan, India, and ASEAN nations. The region's manufacturing sector encompassing electronics, automotive, pharmaceuticals, and consumer goods generating exponential data volumes throughout production processes, creating urgent demand for centralized master data governance supporting supply chain optimization, quality control, and regulatory compliance. India's manufacturing sector is experiencing growth momentum, with industrial machinery and smart factory initiatives driving demand for MDM solutions that consolidate supplier master data, material hierarchies, and production asset records across global supply chains. China's digital transformation initiatives including Industry 4.0 programs are creating market expansion opportunities for MDM vendors offering cloud-based platforms supporting distributed manufacturing operations and real-time supply chain visibility.

Competitive Landscape

The Master Data Management market demonstrates moderate-to-highly competitive intensity characterized by significant vendor consolidation, extensive product differentiation, and sustained innovation focused on cloud-native architectures and AI integration. Oracle, Informatica, IBM, and SAP maintain commanding market positions through comprehensive enterprise software portfolios, extensive customer relationships spanning decades, and substantial research and development investments in enhancing MDM platforms. Specialized MDM vendors, including Reltio, Semarchy, Profisee, TIBCO Software, Ataccama, Stibo Systems, and Pimcore, differentiate through cloud-native architectures, rapid deployment methodologies, transparent pricing models, and industry-specific accelerators appealing particularly to mid-market organizations and domain-specialized use cases.

Key Market Developments

- In May 2025, Salesforce agreed to acquire Informatica for USD 8 billion, fusing CRM with end-to-end data governance capabilities.

- In April 2025, Semarchy launched its MDM platform on Snowflake AI Data Cloud, unifying warehousing and governance functions.

- In February 2024, Semarchy, a provider of master data management (MDM) and data integration solutions, announced the launch of its new Acceleration Toolkit. This toolkit is designed to assist businesses in creating a compelling rationale for MDM adoption, enhancing user uptake and trust, and expediting the realization of value.

Companies Covered in Master Data Management Market

- IBM Corporation

- Oracle

- SAP

- TIBCO Software Inc

- Semarchy

- Informatica Inc.

- Reltio

- SAS Institute Inc.

- Stibo Systems

- Syndigo LLC

- Pimcore

- Other Key Players

Frequently Asked Questions

The global Master Data Management market was valued at US$ 30.3 Billion in 2026 and is projected to reach US$ 81.2 Billion by 2033.

Digital transformation initiatives requiring cloud migration, cloud-based enterprise resource planning deployments, and multi-cloud data consolidation drive critical MDM demand. Stringent regulatory frameworks including GDPR, HIPAA, KYC/AML compliance mandates and heightened focus on data governance as strategic capability propel enterprise MDM investment as foundational governance infrastructure essential for competitive advantage.

Cloud-based MDM deployment architectures represent the dominant and fastest-growing segment, expanding at approximately 20 % or greater CAGR, driven by enterprise preference for scalable, cost-efficient SaaS consumption models, reduced infrastructure investment requirements, and seamless integration with modern cloud data platforms including Snowflake, Databricks, and Microsoft Fabric supporting advanced analytics and AI initiatives.

North America maintains market leadership with approximately 42 % market share, reflecting exceptional digital transformation maturity, advanced cloud adoption, substantial enterprise IT investments in modern data governance infrastructure, concentrated vendor innovation across Informatica, Oracle, IBM, SAP and specialized MDM vendors serving BFSI, healthcare, and technology sectors with comprehensive solutions.

Leading vendors include Informatica (market leader), Oracle, IBM, SAP, and SAS Institute.