- Beauty & Personal Care

- Makeup Base Market

Makeup Base Market Size, Share, and Growth Forecast 2026 - 2033

Makeup Base Market by Product Type (Foundation, Concealer, Primer, Setting Spray, Powder, Others), Formulation (Water-Based, Silicone-Based, Oil-Based, Others), Finish Type (Matte Finish, Dewy/Radiant Finish, Natural Finish, Others), Distribution Channel (Online, Offline), and Regional Analysis, 2026 - 2033

Makeup Base Market Size and Trend Analysis

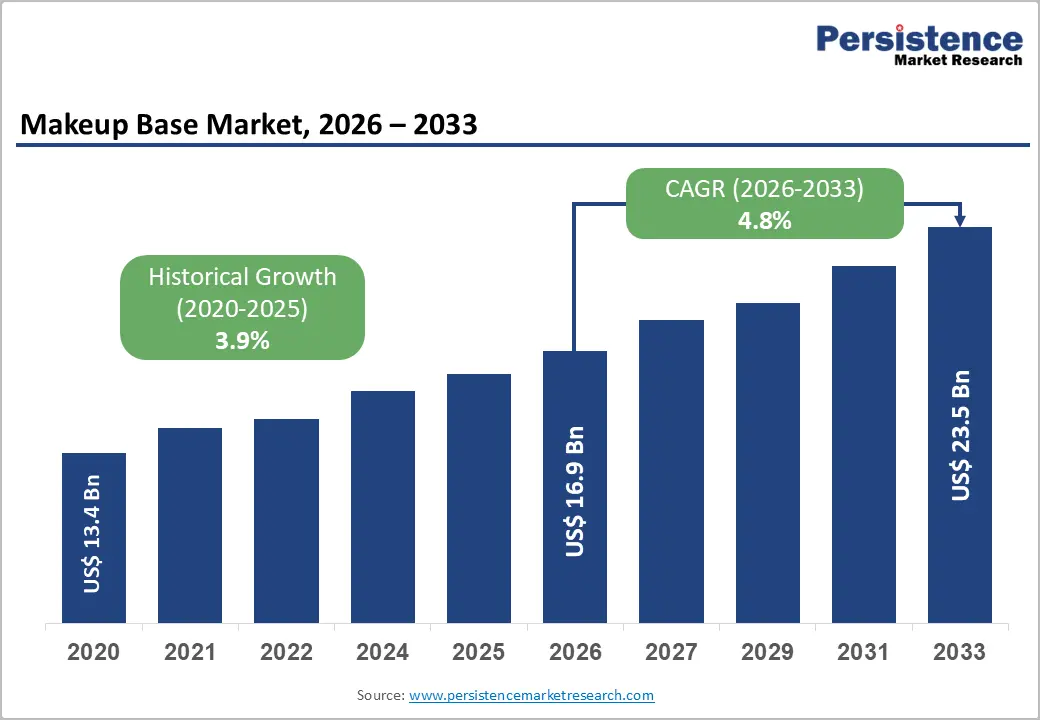

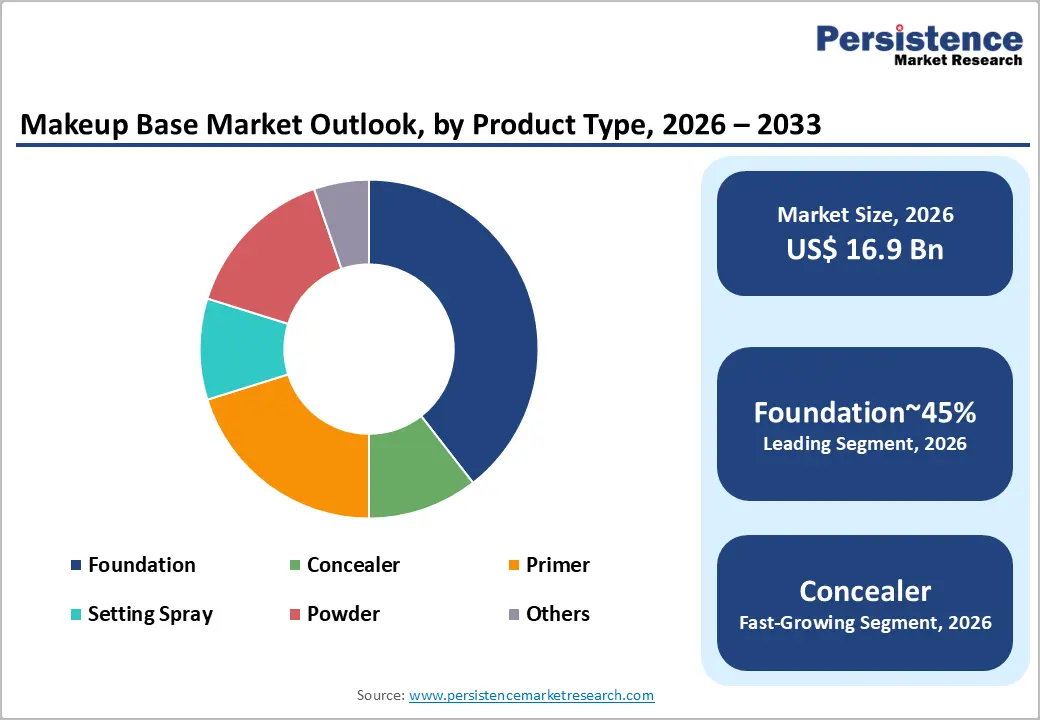

The global Makeup Base Market size is likely to be valued at US$ 16.9 billion in 2026 and is expected to reach US$ 23.5 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033.

The makeup base market is experiencing consistent above-average growth, underpinned by rising global beauty consciousness, the democratization of professional-quality cosmetics through social media, and accelerating consumer preference for multi-functional, skin-benefiting makeup base products.

Key Industry Highlights:

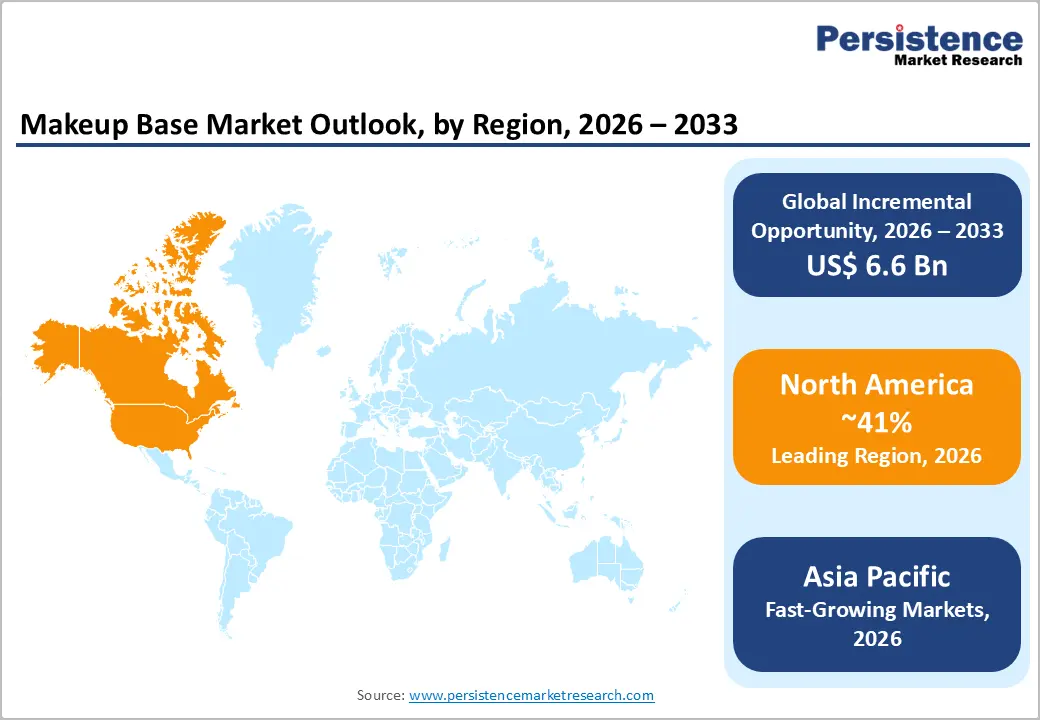

- Leading Region: North America leads the makeup base market, accounting for 41% share, driven by the U.S. beauty market's scale, MoCRA regulatory framework elevating safety standards, ULTA Beauty and Sephora as global innovation barometers, and Fenty Beauty's inclusivity disruption, permanently raising shade range expectations for all market participants.

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by China's double-digit cosmetics retail growth, South Korea's K-beauty cushion foundation and BB cream global influence, India's expanding urban middle class, and ASEAN's strong humid-climate demand for long-wear matte formulations.

- Dominant Segment: Foundation dominates the product type category with ~45% share, serving as the central makeup base franchise for all major beauty brands, with L'Oréal, Estée Lauder, and Shiseido generating their highest makeup base revenues from liquid foundation and coverage product lines.

- Fastest Growing Segment: Online distribution is the fastest growing channel, driven by social commerce on TikTok Shop, virtual try-on AI tools, influencer-led DTC brands, and subscription foundation models, with e.l.f. Cosmetics demonstrating 50M+ views in 48 hours for new launches through platform-native commerce strategies.

- Key Market Opportunity: AI-powered personalized foundation matching and clean-beauty-certified formulations represent the highest-value innovation opportunities, L'Oréal's Perso 2.0 device expanding to 18 countries, and EWG VERIFIED certifications enabling premium pricing and brand loyalty reinforcement across North America and Europe.

Market Dynamics

Drivers - Social Media and Beauty Influencer Culture Driving Makeup Consumption

The global proliferation of beauty content on social media platforms is one of the most powerful commercial drivers of makeup base product adoption worldwide. Instagram, TikTok, and YouTube collectively host hundreds of millions of beauty-related posts and videos, with makeup application tutorials driving consumer discovery and trial of foundation, primer, and setting products at an unprecedented scale.

A 2023 McKinsey & Company study on beauty consumer behavior found that social media is the primary discovery channel for new cosmetics among consumers under 35, the highest-spending beauty cohort globally. Platform-specific trends, including 'glass skin,' 'clean girl aesthetic,' and various coverage looks directly drive category-specific demand spikes for primer, foundation, and setting spray products, sustaining a continuous cycle of product discovery, purchase, and repurchase that structurally elevates makeup base consumption volumes.

Expanding Male and Gender-Inclusive Cosmetics Consumer Base

The rapid expansion of the male and gender-inclusive cosmetics market is generating meaningful incremental demand for makeup base products globally. Mintel's beauty industry consumer research reports that male cosmetics adoption has grown significantly across South Korea, Japan, the United States, and the United Kingdom, with BB creams, tinted moisturizers, and light-coverage foundations among the most purchased products.

The NPD Group noted consistent double-digit growth in male facial cosmetics in North American and European markets. Brands including LVMH's Marc Jacobs Beauty and e.l.f. Cosmetics have launched gender-neutral foundation lines targeting this emerging demographic. South Korea's established male beauty culture, where over 20% of young men regularly use base makeup according to the Korean Cosmetic Association, is providing a global blueprint for inclusive category expansion.

Restraints - Growing Consumer Shift Away from Heavy Makeup Usage

A meaningful cultural shift toward 'no-makeup makeup' and minimalist beauty aesthetics, accelerated by the COVID-19 pandemic's normalization of reduced cosmetic use during remote work, has moderated demand for full-coverage foundation and heavy base products in developed markets. Cosmetics Europe documented declining average foundation usage frequency among Western European women between 2019 and 2022.

As consumers prioritize skincare over coverage, spending shifts from traditional full-coverage foundations toward lighter-weight, skin-care-hybrid bases, disrupting established product category hierarchies and compelling brands to reformulate legacy products, creating transitional demand uncertainty.

Regulatory Complexity Around Cosmetic Ingredient Safety

Tightening global regulations on cosmetic ingredients, particularly concerning potential skin sensitizers, PFAS (per- and polyfluoroalkyl substances) in long-wear foundations, and certain preservatives, create product reformulation costs and market access complexity for makeup base manufacturers. The EU Cosmetics Regulation (EC) No 1223/2009 maintains a list of over 1,300 banned or restricted substances, and the U.S.

Modernization of Cosmetics Regulation Act (MoCRA) 2022 has introduced new safety substantiation and adverse event reporting requirements. Compliance costs for multi-market brands managing divergent regulatory frameworks in the EU, U.S., China, and ASEAN can be substantial, constraining smaller brands and slowing product launches.

Opportunities - Clean Beauty and Skin-Care-Infused Foundation Innovation

The clean beauty movement, characterized by consumer demand for formulations free from parabens, sulfates, synthetic fragrances, and potentially harmful chemicals, presents a significant premiumization opportunity for makeup base manufacturers willing to invest in ingredient transparency and certified clean formulations. The Environmental Working Group (EWG)'s EWG VERIFIED program and similar third-party certifications are increasingly used by consumers as purchase decision criteria in North America and Europe.

Brands including The Ordinary (DECIEM) and Huda Beauty LLC have gained market share through transparent, ingredient-focused positioning. The convergence of skincare and makeup, with SPF-infused, hyaluronic acid-enriched, and niacinamide-containing foundations becoming category standards, enables premium pricing and expands consumer usage occasions, particularly among the growing segment of consumers who previously avoided daily foundation use due to skin concerns.

Inclusive Shade Range Expansion and Personalized Foundation Technology

The global consumer demand for inclusive cosmetics, offering extensive shade ranges that serve all skin tones and undertones, represents a transformative, multi-year opportunity for makeup base brands willing to invest in broadened shade architectures and personalization technology. Fenty Beauty by Rihanna's 2017 launch with 40 foundation shades catalyzed an industry-wide inclusivity shift, with major brands subsequently expanding their shade ranges to remain competitive.

The increasing ethnic and racial diversity in major consumer markets, particularly the United States and Europe, expanding the commercially addressable consumer base for inclusive shade ranges. Personalized foundation matching technology, deployed by L'Oréal Group's Perso™ device and AI-powered virtual try-on tools, is enabling a new tier of bespoke product experiences that command premium pricing and strengthen brand loyalty, creating a high-value product innovation frontier for the category.

Category-wise Analysis

By Product Type Insights

Foundation is the dominant product type segment in the makeup base market, commanding approximately 45% of total category revenue. Foundation, available in liquid, powder, stick, cushion, and serum formats, is the central makeup base product that has anchored the category since its commercial introduction.

The product's dual role as both a complexion-perfecting cosmetic and an increasingly skincare-functional product (with SPF, hydrating, anti-aging, and priming properties) sustains its appeal across consumer demographics. Major brands including L'Oréal Group, Estée Lauder Companies Inc., and Shiseido Company, Limited generate their highest makeup base revenues from foundation franchises. The category's continued expansion, driven by new formats, shade range extensions, and skin-type-specific formulations, reinforces foundation's structural market leadership through 2033.

By Formulation Insights

Water-Based formulations are the dominant makeup base formulation type, representing approximately 52% of the market. Water-based foundations and primers are preferred by the majority of consumers for their lightweight texture, breathability, and suitability across most skin types, including oily, combination, and sensitive skin, without the heaviness or pore-clogging concerns associated with oil-based or silicone-heavy alternatives.

The shift toward 'second skin' and skin-care-infused foundations, where active ingredients such as hyaluronic acid, vitamin C, and peptides are incorporated, is most effectively achieved in water-based emulsion formats. Leading brands including Shiseido Company, Limited and L'Oréal Group have invested heavily in water-based foundation technology to achieve high-performance coverage with improved skin compatibility, reflecting the segment's sustained consumer preference dominance.

By Finish Type Insights

Matte Finish products represent the dominant finish type segment, accounting for approximately 42% of the makeup base market. Matte foundations and primers remain the highest-volume category globally due to their broad cross-demographic appeal, particularly among consumers with oily and combination skin types, who represent the majority of the global consumer base across tropical and subtropical climates in Asia, Latin America, and the Middle East.

The International Dermal Institute notes that oily skin is the most prevalent skin type globally, and matte-finish bases are the dermatologically preferred option for managing excess sebum and extending makeup wear. While dewy and natural finishes are gaining significant share among North American and Northern European consumers, matte remains the default for the majority of makeup base consumers globally.

By Distribution Channel Insights

Offline distribution channels remain dominant, accounting for approximately 58% of makeup base market revenue. The in-store channel, encompassing specialty beauty retailers (Sephora, ULTA Beauty), department store cosmetics counters, and drugstore/mass merchandise channels, retains a structural advantage for makeup base products specifically, as foundation shade matching and skin tone assessment are tactile, in-person experiences that online platforms cannot fully replicate.

The U.S. Census Bureau reports that health and beauty is among the retail categories with the highest in-store purchase rates versus total retail sales, reflecting the sensory and service dimensions that consumers value in cosmetics retail. However, online channels are growing significantly faster, driven by virtual try-on technology, subscription models, and influencer-driven DTC brands, and are expected to narrow the offline channel's dominance through 2033.

Regional Insights

North America Makeup Base Market Trends & Analysis

North America remains a global innovation hub for makeup base products, driven by high consumer spending, premium brand penetration, and regulatory advancements such as MoCRA 2022. The region benefits from strong omnichannel retail ecosystems and rising demand for inclusive shade ranges and clean-label formulations. AI-powered personalization and virtual try-on technologies are accelerating product adoption and consumer engagement across both mass and prestige segments.

- U.S. Makeup Base Market Size

The U.S. dominates the regional market, accounting for approximately USD 45 billion in 2026, driven by its status as the largest global beauty market. Strong DTC growth, retailer influence, and continuous product innovation in foundations, primers, and setting products sustain demand. Increasing regulatory compliance requirements are also elevating product quality and safety benchmarks.

Europe Makeup Base Market Trends, Drivers & Insights

Europe is a mature and regulation-driven market, shaped by stringent cosmetic safety laws and sustainability initiatives under the EU Green Deal. Demand is fueled by premiumization, eco-friendly formulations, and strong heritage brands. The region’s emphasis on clean beauty, biodegradable ingredients, and ethical sourcing is influencing global formulation standards and driving innovation in makeup base products.

- Germany Makeup Base Market Size

Germany leads Europe in volume consumption, with an estimated market size of USD 9.1 billion in 2026. Growth is supported by strong demand in the mass segment, widespread retail networks, and consumer preference for dermatologically tested, high-quality formulations. Drugstore chains play a crucial role in driving accessibility and product penetration.

- U.K. Makeup Base Market Size

The U.K. market is valued at approximately USD 7.8 billion in 2026, driven by high e-commerce penetration and strong consumer inclination toward premium and indie brands. Regulatory alignment with EU standards ensures product safety, while digital-first beauty trends and influencer-driven marketing continue to shape purchasing behavior.

- France Makeup Base Market Size

France represents a key prestige beauty market, estimated at USD 6.7 billion in 2026. The country’s strong luxury cosmetics heritage supports premium product demand, particularly in foundations and primers. Innovation in formulation and branding, combined with global export strength, reinforces France’s leadership in high-end makeup base products.

Asia Pacific Makeup Base Market Drivers & Analysis

Asia Pacific is the fastest-growing region, driven by rising disposable incomes, urbanization, and strong cultural emphasis on skincare and beauty. Innovations from K-beauty and J-beauty, along with increasing digital adoption, are accelerating growth. Climate-specific formulations, such as lightweight and long-wear products, further support demand across diverse markets.

- China Makeup Base Market Size

China is the largest regional market, valued at approximately USD 28.3 billion in 2026. Rapid growth is fueled by expanding middle-class consumers, strong e-commerce ecosystems, and rising domestic brand competitiveness. Demand for premium, long-lasting, and skin-enhancing base products continues to increase significantly.

- India Makeup Base Market Size

India’s market is estimated at USD 6.7 billion in 2026, with strong growth driven by increasing urbanization, rising disposable incomes, and expanding beauty awareness. Demand is particularly high for affordable, climate-suitable, and inclusive products. Both international and domestic brands are aggressively expanding their presence in this high-potential market.

- Japan Makeup Base Market Size

Japan’s makeup base market is valued at around USD 8.9 billion in 2026, characterized by advanced formulation technologies and strong consumer preference for lightweight, skin-perfecting products. Innovation in hybrid skincare-makeup solutions and high-quality standards continues to drive steady demand in this mature yet technologically advanced market.

Competitive Landscape

The global makeup base market is moderately consolidated at the prestige tier, dominated by global beauty conglomerates including L'Oréal Group, Estée Lauder Companies Inc., LVMH Moët Hennessy Louis Vuitton, and Shiseido Company, Limited, while remaining highly fragmented in the mass and indie segments. Market leaders differentiate through extensive shade architecture, proprietary pigment and skincare hybrid technology, celebrity and influencer brand partnerships, and omnichannel distribution depth.

Key strategies include acquisitions of indie and clean beauty brands, investment in virtual try-on and AI shade-matching platforms, and sustainable packaging transitions. Emerging business model trends include foundation subscription services, personalized AI-matched foundation refills, and direct-to-consumer brand ecosystems that bypass traditional retail, reflecting the market's transformation toward hyper-personalized beauty experiences.

Key Market Developments

- February, 2025: L'Oréal Group launched an AI-powered personalized foundation matching service integrated into its Perso 2.0 device, expanding to 18 countries, enabling consumers to create bespoke foundation formulas tailored to individual skin tone, type, and coverage preference at home.

- September, 2024: Estée Lauder Companies Inc. expanded its Double Wear Stay-in-Place foundation to 70 shades globally, its largest-ever shade range, responding to consumer demand for comprehensive inclusive coverage across all skin tones in the prestige foundation segment.

- April, 2024: e.l.f. Cosmetics launched its Halo Glow Liquid Filter complexion booster in partnership with TikTok Shop, achieving over 50 million views within 48 hours of launch, demonstrating the transformative impact of social commerce on makeup base product velocity.

Global Makeup Base Market- Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 13.4 Bn |

|

Current Market Value (2026) |

US$ 16.9 Bn |

|

Projected Market Value (2033) |

US$ 23.5 Bn |

|

CAGR (2026-2033) |

4.8% |

|

Leading Region |

North America, 41% share |

|

Dominant Product Type |

Foundation, 45% share |

|

Top-ranking Formulation |

Water-Based, 52% |

|

Incremental Opportunity |

US$ 6.6 Bn |

Companies Covered in Makeup Base Market

- L'Oréal Group

- Estée Lauder Companies Inc.

- Procter & Gamble (P&G)

- Shiseido Company, Limited

- Unilever

- Coty Inc.

- Amorepacific Corporation

- LVMH Moët Hennessy Louis Vuitton

- Beiersdorf AG

- Kao Corporation

- Revlon Inc.

- Mary Kay Inc.

- Huda Beauty LLC

- e.l.f. Cosmetics

- The Ordinary (DECIEM)

- Charlotte Tilbury Beauty Ltd.

- Rare Beauty

- NYX Professional Makeup

Frequently Asked Questions

The global Makeup Base Market is estimated at US$ 16.9 Billion in 2026 and is forecast to reach US$ 23.5 Billion by 2033, at a CAGR of 4.8% in the coming years.

Key drivers include social media and beauty influencer culture, with social media platforms as the primary discovery channel for beauty under-35s, and expanding gender-inclusive cosmetics adoption, with South Korea's Korean Cosmetic Association reporting over 20% of young men regularly using base makeup, providing a global blueprint for inclusive category expansion.

Foundation leads the product type category with approximately 45% market share, as it is the central makeup base franchise for all major beauty brands. Its dual role as complexion-perfecting cosmetic and skin-care-infused product, with SPF, hydrating, and anti-aging properties, sustains multi-demographic appeal across L'Oréal Group, Estée Lauder, and Shiseido's highest-revenue makeup segments.

North America leads the market, anchored by the United States' position as the world's largest beauty market, MoCRA 2022 elevating cosmetic safety standards, and retail innovation from ULTA Beauty and Sephora USA. Fenty Beauty's inclusivity disruption permanently raised shade range expectations globally, while L'Oréal's Perso AI personalization technology has been commercialized first in the North American market.

The most compelling opportunities are AI-powered personalized foundation matching and clean beauty certified formulation development aligned with EWG VERIFIED™ standards and EU Cosmetics Regulation frameworks, enabling premium pricing, increased consumer trust, and expanded distribution in safety-conscious European and North American retail channels.