- Food Ingredients & Additives

- Lupin Protein Market

Lupin Protein Market Size, Share, and Growth Forecast, 2025 - 2032

Lupin Protein Market by Product Type (Isolates, Concentrates, Flours, Textured Protein), Application (Sports Nutrition, Weight Management, Meal Replacements, Functional Foods), End-use (Food and Beverages, Dietary Supplements, Animal Feed, Pharmaceuticals, Cosmetics and Personal Care), and Regional Analysis for 2025 - 2032

Lupin Protein Market Size and Trends Analysis

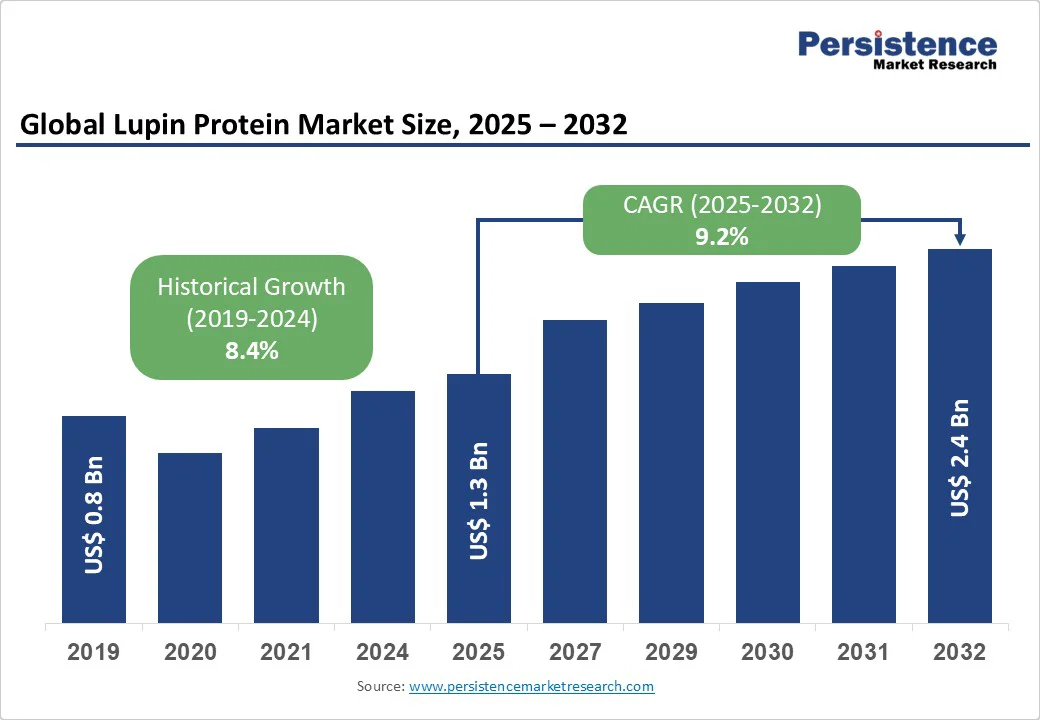

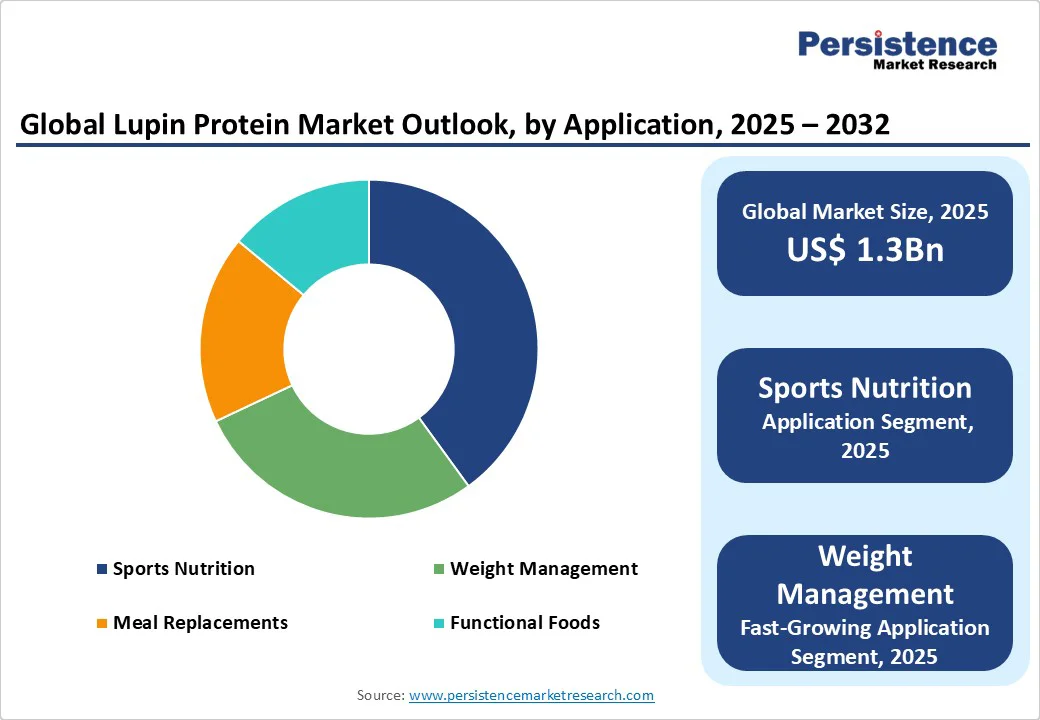

The global lupin protein market size is likely to be valued at US$ 1.3 Bn in 2025 and is expected to reach US$ 2.4 Bn by 2032, growing at a CAGR of 9.2% during the forecast period from 2025 to 2032.

The lupin protein market has experienced significant growth, driven by the increasing demand for plant-based proteins amid rising health consciousness, veganism, and sustainability concerns in the food industry.

The adoption of lupin protein as a versatile, allergen-free alternative to soy and dairy proteins has boosted its use in various applications, from nutrition supplements to functional foods.

Key Industry Highlights:

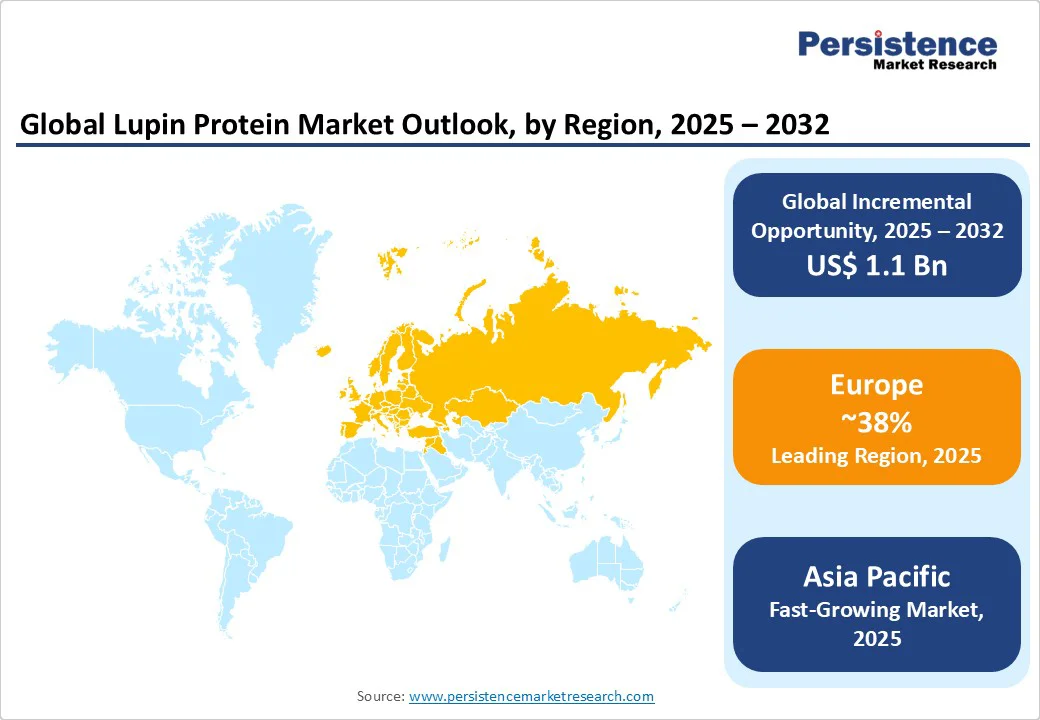

- Leading Region: Europe, holding a 38% market share in 2025, driven by established cultivation, rising plant-based protein demand, supportive regulations, and innovative food applications.

- Fastest-growing Region: Asia Pacific is emerging as the fastest-growing market, fueled by rapid urbanization, increasing government investments in agriculture and nutrition programs, and growing demand for affordable protein sources in countries such as China and India.

- Dominant Product Type: Concentrates, commanding nearly 42% market share, due to their cost-effectiveness, ease of incorporation into foods, and widespread adoption in food and beverages for enhancing nutritional profiles.

- Leading Application: Sports Nutrition, accounting for over 40% of market revenue, driven by the need for high-protein, low-carb options in fitness and wellness products.

| Key Insights | Details |

|---|---|

| Lupin Protein Market Size (2025E) | US$1.3 Bn |

| Market Value Forecast (2032F) | US$2.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.4% |

Market Dynamics

Driver - Increasing Deployment of Plant-Based Proteins in Consumer Diets

The growing global emphasis on health, sustainability, and ethical consumption is fueling the adoption of plant-based proteins in consumer diets, and lupin protein is emerging as a key beneficiary of this trend. As consumers increasingly shift away from animal-derived proteins due to concerns around cholesterol, lactose intolerance, and environmental footprint, lupin protein offers a nutrient-rich alternative with high protein content, dietary fiber, and essential amino acids. Moreover, it aligns with the surging demand for clean-label, allergen-friendly, and non-GMO products, particularly among flexitarians, vegans, and health-conscious individuals.

Food and beverage manufacturers are responding by incorporating lupin protein into a wide range of products, from baked goods and dairy alternatives to protein bars and ready-to-drink shakes. For instance, in 2023, Wide Open Agriculture acquired Prolupin’s assets, giving it production capacity in Europe and access to the European plant-based dairy market. This growing deployment not only supports nutritional diversity but also strengthens lupin protein’s position as a sustainable and competitive ingredient in the global plant-protein market.

Restraint - High development and regulatory costs

The high costs associated with developing and regulating lupin protein products hamper market growth. Developing lupin-based ingredients and finished products requires extensive investments in research, formulation, and processing technologies to ensure that the final output meets safety, nutritional, and sensory expectations.

Unlike more established plant proteins such as soy or pea, lupin is relatively new in the mainstream food industry, which means additional resources must be allocated to optimize taste, texture, and consumer acceptance. Beyond R&D, companies face strict regulatory hurdles when bringing lupin-based products to global markets.

Regulatory agencies such as the European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) mandate comprehensive allergen labeling and safety assessments, which further add to development timelines and costs.

For instance, EU law, the European Commission mandates that lupin is listed among 14 major allergens, requiring clear labeling on food products to ensure consumer safety and transparency regarding allergenic ingredients. Consequently, high costs and compliance burdens limit the pace of innovation and adoption in the lupin protein sector.

Opportunity - Advancements in modular and AI-integrated processing technologies

Advancements in modular and AI-integrated processing technologies present a significant opportunity for the lupin protein market. Traditional protein extraction methods often face challenges such as high energy use, lower yields, and inconsistent product quality. However, the adoption of modular processing systems allows manufacturers to scale operations more flexibly, reducing upfront capital investments while ensuring efficient throughput.

AI integration is revolutionizing process optimization by enabling real-time monitoring, predictive maintenance, and automated adjustments to enhance protein purity, texture, and nutritional value. These innovations not only improve cost-effectiveness but also help producers tailor lupin protein for diverse applications, ranging from plant-based dairy to sports nutrition. For instance, Bühler Group and Microsoft partnered in 2023 to integrate AI into food processing equipment, enabling predictive quality control and reducing resource wastage in plant-based protein production.

Category-wise Analysis

Product Type Insights

Concentrates dominate, expected to account for approximately 42% share in 2025. Its dominance stems from its cost-effectiveness, rapid processing cycles, and ease of integration into everyday foods for applications such as sports nutrition and meal replacements.

Lupin protein concentrates, such as those offered by Aminola and Barentz International B.V., enable nutritional enhancement, scalability, and seamless incorporation across products, making them a preferred choice for industries such as food and beverages and dietary supplements. Their modular forms also reduce upfront costs, driving adoption among startups and SMEs.

The isolates segment is the fastest-growing, driven by industries with high-purity requirements, such as pharmaceuticals and cosmetics. Lupin protein isolates offer greater concentration and customization, appealing to premium brands with complex formulations.

The growing focus on hypoallergenic and high-bioavailability proteins, such as in weight management supplements, is accelerating the adoption of isolates in regions such as North America and Europe, with significant growth potential in high-value applications.

Application Insights

Sports nutrition leads the lupin protein market, holding a 40% share in 2025. The segment’s dominance is driven by the need for efficient muscle recovery and performance enhancement in expanding fitness networks, particularly in protein shakes and bars. Protein forms streamline the integration of lupin into active lifestyles, reduce digestive issues, and improve efficacy, making them critical for providers such as The Protein Bread Company and FRANK Food Products.

The weight management segment is the fastest-growing, fueled by the rapid growth of wellness trends and the need for low-calorie, high-satiety options. The rise in obesity awareness and the increasing demand for natural appetite suppressants have spurred the adoption of lupin protein in this sector. The Asia Pacific region, with its booming health consciousness, is driving rapid adoption in this segment.

End-use Insights

Food and beverages hold the largest market share, accounting for approximately 50% of revenue in 2025. Food and beverage end-use allows vendors such as Coorow Seeds and Lupingredients to maintain close relationships with customers, offer tailored proteins, and provide dedicated support. This end-use is particularly dominant in applications with complex requirements, such as functional foods and meal replacements, where customized lupin solutions are critical.

The dietary supplements are the fastest-growing, driven by the increasing adoption of advanced nutrition technologies and the rise of personalized wellness products for immunity and vitality. These platforms offer seamless access to lupin proteins, enabling faster development and integration with other nutraceuticals. The growing popularity of supplement-focused lupin among consumers and health brands is accelerating the adoption of protein solutions through this end-use, particularly in North America and the Asia Pacific.

Regional Insights

North America Lupin Protein Market Trends

The North American lupin protein market is experiencing significant growth, driven by multiple socio-economic, health, and industry trends. Increasing consumer awareness of health and wellness has created a strong demand for plant-based proteins, which are perceived as healthier, sustainable, and environmentally friendly alternatives to animal-derived proteins.

Lupin protein, in particular, has gained attention due to its high protein content, rich essential amino acids, dietary fiber, and low allergenicity, making it suitable for a wide range of dietary needs, including weight management, muscle recovery, and functional nutrition.

Food manufacturers in North America are increasingly incorporating lupin protein into diverse product categories, including meat substitutes, dairy alternatives, bakery items, snacks, and beverages. This innovation is fueled by growing consumer interest in protein-enriched foods and the desire for convenient, nutritious options that align with active and health-conscious lifestyles.

The regulatory environment in North America supports the adoption of alternative proteins. Government initiatives promoting sustainable agriculture, plant-based diets, and nutritional education encourage research, development, and commercialization of lupin protein products. Asia Pacific Lupin Protein Market Trends

Asia Pacific is emerging as the fastest-growing market for lupin protein, driven by several dynamic factors. Rapid urbanization in countries such as China, India, and Japan is transforming consumer lifestyles, leading to increased demand for convenient, nutritious, and protein-rich food products. Rising disposable incomes and a growing middle-class population are further boosting consumption of plant-based proteins as affordable and healthy alternatives to animal-derived proteins.

Government initiatives and investments in agriculture and nutrition programs are also playing a critical role. Policies supporting sustainable agriculture, food security, and dietary diversification encourage the production and adoption of protein-rich crops such as lupin.

These initiatives include subsidies for farmers, research funding for high-yield lupin varieties, and public health campaigns promoting protein consumption. Additionally, the increasing awareness of health, fitness, and wellness among urban consumers has fueled demand for protein-enriched foods, snacks, and beverages.

Europe Lupin Protein Market Trends

Europe accounts for a 38% share of the global lupin protein market, making it the dominant region in terms of revenue and consumption. This strong market position is driven by a combination of agricultural, consumer, regulatory, and industrial factors.

Europe has a long-standing tradition of cultivating lupin, particularly in countries such as Germany, France, Poland, and Italy. The favorable climatic conditions, coupled with advanced farming techniques, ensure a steady and high-quality supply of lupin seeds, which is essential for large-scale protein extraction and processing.

Consumer demand is another major driver. Increasing awareness of health, nutrition, and sustainability has led to a rising preference for plant-based protein sources. Lupin protein, being naturally rich in essential amino acids, allergen-friendly, and low in fat, fits well within European consumers’ dietary trends.

Additionally, the regulatory environment in Europe is supportive of plant-based protein adoption. Initiatives such as the European Green Deal and policies promoting sustainable agriculture encourage the production and consumption of alternative proteins.

Finally, food manufacturers are innovating by incorporating lupin protein into various applications, including meat alternatives, dairy substitutes, bakery products, and snacks. These factors collectively solidify Europe’s dominance in the lupin protein market.

Competitive Landscape

The global lupin protein market is characterized by intense competition, regional strengths, and a mix of global and niche players. In developed regions such as North America and Europe, large firms such as Barentz International B.V., Prolupin GmbH, and Aminola dominate through scale, advanced R&D capabilities, and established partnerships with food agencies. In the Asia Pacific, rapid agricultural developments and increasing demand for plant-based proteins are attracting significant investments from both international players, such as Coorow Seeds and Lupingredients, and regional vendors.

Key Developments

- In May 2024, Aminola expanded its lupin protein concentrate production capacity to meet the growing demand in the pet nutrition and livestock feed sectors.

- In April 2024, Prolupin GmbH partnered with European vegan food startups to incorporate lupin protein into innovative dairy-alternative products, enhancing plant-based offerings and meeting rising consumer demand for nutritious, sustainable options.

Companies Covered in Lupin Protein Market

- Aminola

- Prolupin GmbH

- A. Costantino & C. SpA

- The Protein Bread Company

- Coorow Seeds

- Lupingredients

- FRANK Food Products

- Barentz International B.V

- Others

Frequently Asked Questions

The global lupin protein market is projected to reach US$ 1.3 Bn in 2025.

The increasing deployment of plant-based proteins in consumer diets is a key driver.

The lupin protein market is poised to witness a CAGR of 9.2% from 2025 to 2032.

Advancements in modular and AI-integrated processing technologies are a key opportunity.

Aminola, Prolupin GmbH, A. Costantino & C. SpA, The Protein Bread Company, and Barentz International B.V. are key players.