- Medical Devices

- Low-dose Radiotherapy Market

Low-dose Radiotherapy Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Low-dose Radiotherapy Market by Component (Equipment, Software & Services), Technology (External Beam Radiotherapy (EBRT), Brachytherapy), Application (Cancer Treatment, Non-Cancer / Inflammatory Conditions, Others), End-user, and Regional Analysis from 2025 to 2032

Low-dose Radiotherapy Market Share and Trends Analysis

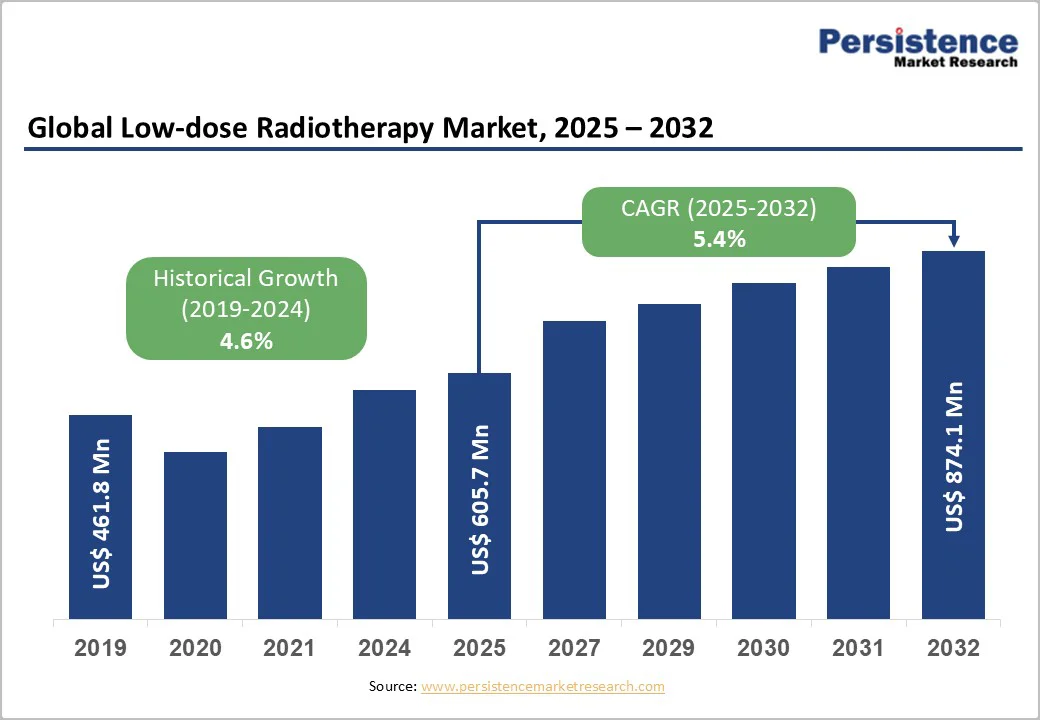

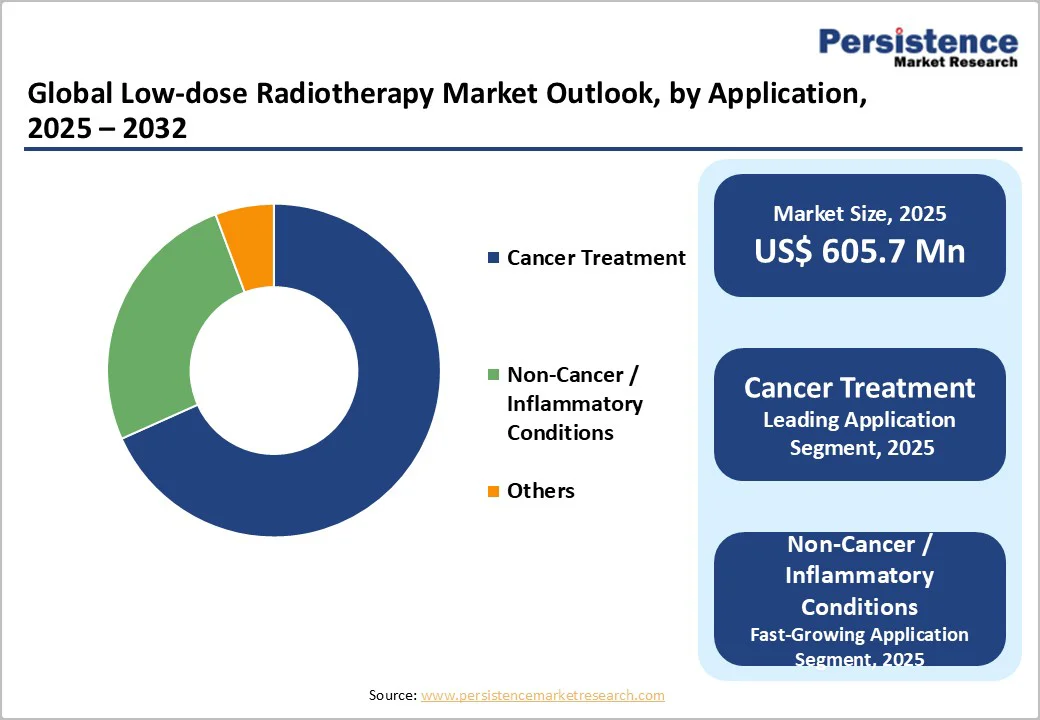

The global low-dose radiotherapy market size is valued at US$605.7 million in 2025 and is projected to reach US$874.1 million by 2032, growing at a CAGR of 5.4% between 2025 and 2032.

Radiation therapy remains a fundamental modality in cancer care, but the growing interest in low-dose radiation therapy (LDRT) is reshaping how clinicians approach both malignant and non-malignant conditions. Unlike conventional high-dose treatments, LDRT delivers carefully calibrated, minimal radiation levels designed to modulate inflammation, relieve pain, and support tissue healing with significantly reduced toxicity.

This targeted, lower-intensity approach allows effective treatment of select cancers, degenerative joint disorders, and inflammatory diseases while preserving healthy tissue. Its distinct purpose, dosage strategy, and gentler treatment frequency position LDRT as a versatile and increasingly valuable complement to traditional radiation therapy.

Key Industry Highlights:

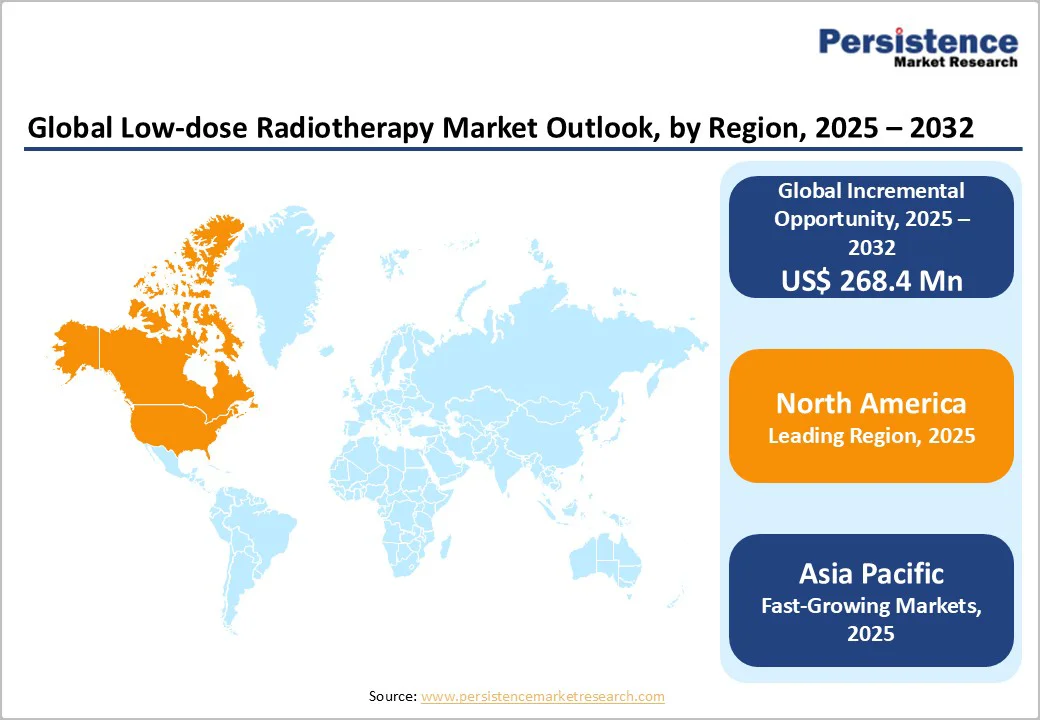

- Leading Region: North America dominates the global market with 36.1%, driven by High adoption of advanced modalities, strong oncology workforce, high cancer screening rates and favorable regulatory pathways.

- Fastest-Growing Region: Asia Pacific is expected to grow at a 6.7% CAGR, fueled by rising cancer prevalence, expanding healthcare investments, and increasing access to modern radiotherapy systems.

- Leading Component: Equipment leads with 74.1% share, supported by continuous upgrades in linear accelerators, imaging modules, and treatment delivery platforms essential for high-volume radiotherapy centers.

- Leading Technology: External Beam Radiotherapy (EBRT) dominates with over 84% value share, driven by widespread clinical adoption, technological precision, and its suitability for most solid tumor treatments.

- Leading Application: Cancer treatment remains the dominant category with 72.4%, due to high global cancer burden and growing preference for non-invasive, targeted radiotherapy approaches.

- Leading End-user: Hospitals lead with a 64.8% share, owing to their comprehensive oncology departments, availability of advanced equipment, and higher patient intake for both routine and complex radiotherapy procedures.

- Developed markets strengthen reimbursement for advanced radiotherapy modalities, accelerating hospital adoption and reducing out-of-pocket burden for patients.

- Oncology centers increasingly invest in AI-driven planning systems, driven by improved workflow efficiency, treatment accuracy, and reduced clinician workload.

| Key Insights | Details |

|---|---|

| Low-dose Radiotherapy Market Size (2025E) | US$605.7 Million |

| Market Value Forecast (2032F) | US$874.1 Million |

| Projected Growth (CAGR 2025 to 2032) | 5.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.6% |

Market Dynamics

Driver - Growing Clinical Validation and Expanding Use of LDRT Across Malignant and Benign Conditions

Global demand for low-dose radiotherapy (LDRT) is accelerating as healthcare systems increasingly recognize its unique ability to deliver therapeutic benefit with minimal toxicity. LDRT, typically defined as radiation doses below 1 Gray (Gy) per fraction, offers anti-inflammatory, analgesic, and immunomodulatory effects, making it valuable beyond oncology.

Clinically, it is gaining renewed acceptance for benign inflammatory and degenerative musculoskeletal disorders such as osteoarthritis, plantar fasciitis, and tendinitis, especially when conventional therapies fail. Its ability to relieve chronic pain, suppress pro-inflammatory cell activity, and potentially stimulate bone repair is driving adoption among aging populations with long-standing joint disease.

In oncology, LDRT supports the treatment of lymphomas and leukemias, early-stage solid tumors, and symptom relief in advanced cancers, such as reducing pain from bone metastases or shrinking tumors compressing vital structures. Broader medical applications, including prevention of heterotopic ossification after orthopedic surgery and management of keloids, further expand its utility.

Growing scientific interest is also emerging in neurological conditions, with early clinical observations indicating temporary cognitive improvement in Alzheimer’s disease following iterative low-dose brain imaging. Collectively, expanding indications, improved precision technologies, and its favorable safety profile position LDRT as a versatile, patient-friendly alternative to high-dose radiotherapy.

Restraints - Persistent Safety Concerns, High System Costs, and Limited Global Accessibility Slow Adoption

Persistent safety concerns, limited accessibility, and infrastructure-related challenges challenge the global low-dose radiotherapy market. However, LDRT delivers radiation at levels far below 1 Gray (Gy) per fraction, misconceptions around radiation-induced toxicity-particularly fears of secondary cancers, cumulative exposure, and long-term organ effects-continue to influence patient and physician acceptance.

These perceptions are reinforced in regions where radiophobia remains strong and standardized clinical guidelines are lacking. Adoption is also hindered by variability in global practice patterns; for example, while Europe treats thousands of patients with benign conditions annually, large markets such as the United States and parts of Asia remain conservative due to inconsistent evidence, regulatory caution, and limited training in non-oncologic indications.

Operational barriers further slow expansion-the high cost of radiotherapy systems, inadequate reimbursement frameworks, and uneven distribution of treatment centres restrict access, especially in low- and middle-income countries.

Additionally, side effects-though typically mild, such as transient fatigue, skin irritation, or temporary discomfort-require careful monitoring, adding to clinical complexity. Collectively, safety misconceptions, infrastructure gaps, and economic limitations restrain broader global integration of LDRT despite its therapeutic potential.

Opportunity - Rising Evidence in Osteoarthritis and Combination Therapies Unlocks New High-Value Clinical Applications

Global opportunities for the Low-dose radiotherapy market are expanding rapidly as new clinical evidence, technological innovation, and widening therapeutic scope reshape its value proposition.

A major catalyst is the rising volume of high-quality randomized and sham-controlled trials, such as the September 2025 Korean multicenter study presented at the American Society for Radiation Oncology (ASTRO) annual meeting, demonstrating meaningful improvements in pain, stiffness, and functional scores in patients with knee osteoarthritis treated with doses as low as 0.3-3 Gray (Gy).

These results reinforce LDRT’s role as a non-invasive, cost-efficient alternative to long-term medication use or joint surgery.

Parallel research in inflammatory and degenerative disorders, as well as dermatologic and benign soft-tissue conditions, is broadening its clinical relevance, supported by favourable long-term safety findings and standardized guidelines from organizations such as the German Society for Radiation Oncology (DEGRO).

In oncology, emerging data showing synergy between LDRT and chemo-immunotherapy in aggressive malignancies, including small cell lung cancer with liver metastasis, create new combination-therapy opportunities. Collectively, expanding indications, growing clinical validation, and its uniquely low-toxicity profile position LDRT for significant global adoption across both malignant and non-malignant diseases.

Category-wise Analysis

By Component Insights

Equipment is expected to account for a leading 74.1% share of the global low-dose radiotherapy market by 2025 as healthcare providers increasingly invest in precision-enhancing radiotherapy platforms, digital imaging upgrades, and automated treatment planning technologies. Growing demand for systems offering improved targeting accuracy, reduced operator dependence, and enhanced workflow efficiency further strengthens the segment’s dominance.

Rising replacement cycles in developed markets, combined with expanding installation of advanced radiotherapy infrastructure in emerging economies, support continued equipment uptake. Moreover, regulatory emphasis on high-quality radiation delivery and safety-driven system enhancements accelerates the transition toward next-generation low-dose radiotherapy technologies, maintaining equipment leadership globally.

By Technology Insights

External Beam Radiotherapy (EBRT) is expected to account for the largest 84.7% share of the global low-dose radiotherapy market by 2025, driven by its wide clinical applicability across oncology and non-oncology indications, offering non-invasive, precise, and highly customizable treatment delivery. Its ability to modulate dose intensity, minimize exposure to surrounding tissues, and integrate with advanced imaging systems drives significant provider preference.

Technology also benefits from continuous innovation in linear accelerators, image-guided platforms, and adaptive radiotherapy techniques. Additionally, EBRT’s strong penetration in both high-income and emerging healthcare systems, coupled with favorable reimbursement and established treatment protocols, solidifies its dominant market position through 2025.

By Application Insights

Cancer treatment remains the largest application segment, accounting for 38.4% of the total share, as the global oncology burden continues to rise and clinical acceptance of low-dose radiotherapy for select tumor types increases. Providers increasingly deploy low-dose approaches to reduce toxicity, improve tolerability, and enable treatment of elderly or comorbid patient groups.

Technological advancements supporting precise tumor targeting further expand its use in both primary and adjunct therapeutic settings. The growing integration of low-dose regimens into multimodal cancer care pathways, supported by evidence demonstrating favorable outcomes and quality-of-life benefits, sustains the segment’s strong and expanding market share.

By End-user Insights

Hospitals are expected to account for a leading 64.8% share of the global low-dose radiotherapy market by 2025 as they remain the primary centers equipped with advanced radiotherapy systems, specialized infrastructure, and multidisciplinary oncology teams required for safe low-dose radiotherapy delivery. Their ability to manage complex cases, perform integrated diagnostics, and coordinate follow-up care strengthens patient preference and referral inflow.

Hospitals also account for the majority of capital investments in new linear accelerators and imaging-guided platforms, enabling higher throughput and broader service offerings. Favorable reimbursement alignment, stronger clinical governance, and expanding oncology departments-especially within tertiary and academic hospitals-further reinforce their dominant market contribution through 2025.

Regional Insights

North America Low-dose Radiotherapy Market Trends

By 2025, North America is projected to command nearly 36.1% of the global Low-dose radiotherapy (LDRT) market, reflecting rising clinical acceptance of low-dose regimens for chronic, non-malignant conditions. A growing patient pool shapes the region’s leadership. Osteoarthritis affects 32.5 million U.S. adults, while Plantar Fasciitis impacts nearly 1 million Americans annually, creating sustained demand for alternatives to surgery or long-term medication.

LDRT, typically delivered in fractionated schedules of 0.5-1 Gray (Gy) per session and maintaining total doses below 20 Gy, is gaining traction due to its anti-inflammatory benefits and emerging clinical evidence. Momentum further accelerated with major ecosystem investments; in May 2025, Siemens Healthineers announced a USD 150 million expansion to strengthen U.S. radiotherapy manufacturing, supply-chain resilience, and product availability.

Clinical adoption also expanded in July 2025, when Advocate Radiation Oncology began offering LDRT for Osteoarthritis, Plantar Fasciitis, and early-stage Dupuytren’s Contracture, highlighting the growing preference for minimally invasive, conservative therapies. Together, rising disease burden, renewed scientific interest, industrial investment, and increasing provider adoption firmly position North America as the leading market for LDRT.

Europe Low-dose Radiotherapy Market Trends

By 2025, Europe is expected to account for around 29.3% of the global Low-dose radiotherapy market, supported by its long-standing clinical acceptance of low-dose radiation for benign, inflammatory, and degenerative conditions.

Countries such as Germany and Spain routinely use LDRT for joint pain and musculoskeletal disorders, with Germany alone applying 10-30% of its radiotherapy treatments to non-cancer indications- an adoption level significantly higher than in most regions.

Although awareness remains uneven across Europe and high-quality randomized evidence has historically been limited, ongoing trials and clinical standardization continue to strengthen confidence in LDRT’s therapeutic value.

Market momentum accelerated further in May 2025, when England launched a nationwide upgrade of radiotherapy infrastructure under a £70 million government program, deploying new Linear Accelerator (LINAC) systems across 28 hospitals.

These advanced machines, designed for higher precision and reduced toxicity, improve treatment delivery and indirectly support LDRT expansion by modernizing capacity and reducing equipment-related delays. With strong clinical heritage, expanding infrastructure, and increasing validation of low-dose regimens, Europe remains one of the most established and influential regions driving LDRT adoption.

Asia Pacific Low-dose Radiotherapy Market Trends

Asia Pacific is emerging as one of the fastest-growing regions globally, projected to expand at a CAGR of 6.7% during the forecast period. Rapid oncology infrastructure upgrades, government-supported technology adoption, and increasing clinical acceptance of low-dose radiation for benign and inflammatory conditions drive growth.

- In September 2025, BEBIG Medical GmbH, a global radiation therapy technology provider with over 40 years of experience, deepened its investment in India to expand access to advanced radiotherapy systems.

- In September 2025, the Health Minister of Andhra Pradesh, India, inaugurated the BEBIG Medical SagiNova High-Dose-Rate (HDR) Brachytherapy system at King George Hospital, Visakhapatnam, the largest government hospital in the state.

Such deployments, supported by coordinated efforts among industry, local partners, and government bodies, strengthen treatment capacity, accelerate the modernization of radiotherapy departments, and indirectly enable broader adoption of LDRT across India and neighbouring Asia-Pacific countries.

Collectively, rising patient volumes, expanding equipment installations, and sustained investment commitments position the Asia Pacific as a high-momentum region for LDRT growth.

Competitive Landscape

The competitive landscape is defined by rapid innovation in imaging-guided, AI-enabled, and precision radiotherapy platforms. Vendors are focusing on expanding clinical capabilities, integrating real-time imaging, simplifying workflows, and improving treatment accuracy. Rising investments, technology upgrades, and strong participation in global oncology meetings are intensifying competition as players race to deliver more efficient, patient-centric radiation therapy solutions.

Key Industry Developments:

- In September 2025, UCLA Health received a $2 million grant from ViewRay Systems, Inc. to advance clinical trials in MRI-guided radiotherapy, supporting research that enhances real-time tumor-targeting accuracy and reduces healthy-tissue exposure, thereby improving overall radiation therapy outcomes.

- In September 2025 at the American Society for Radiation Oncology (ASTRO) annual meeting in San Francisco, Royal Philips unveiled the Philips Rembra RT, Areta RT CT platforms, and helium-free BlueSeal RT 1.5T MR system, introducing AI-enabled technologies to improve precision, efficiency, and patient-centric radiation therapy planning.

Companies Covered in Low-dose Radiotherapy Market

- Siemens Healthineers AG

- ViewRay Systems, Inc.

- Elekta

- BEBIG Medical

- Xstrahl

- GE HealthCare

- CQ Medical

- Luminis Health

- Eckert & Ziegler

- CivaTech Oncology Inc.

Frequently Asked Questions

The global low-dose radiotherapy market is projected to be valued at US$ 605.7 Million in 2025.

Growing adoption of low-dose radiation for benign inflammatory conditions, rising clinical evidence, expanding geriatric population, and increasing access to advanced radiotherapy infrastructure drive market growth.

The global market is poised to witness a CAGR of 5.4% between 2025 and 2032.

Expansion into emerging markets, wider adoption for noncancerous musculoskeletal disorders, and integration of imaging-guided precision technologies present major growth opportunities.

Major players in the global are Siemens Healthineers AG, ViewRay Systems, Inc., Elekta, BEBIG Medical, Xstrahl, and others.