- Bulk Chemicals

- Lime Market

Lime Market Size, Share, and Growth Forecast 2026 - 2033

Lime Market by Product Type (Quicklime, Hydrated Lime), Purity Level (High Calcium Lime, Dolomitic Lime), Application (Metallurgical Processes, Environmental Uses, Chemical Manufacturing, Construction, Glass and Ceramics, Pulp and Paper, Others), and Regional Analysis, 2026 - 2033

Lime Market Size and Trend Analysis

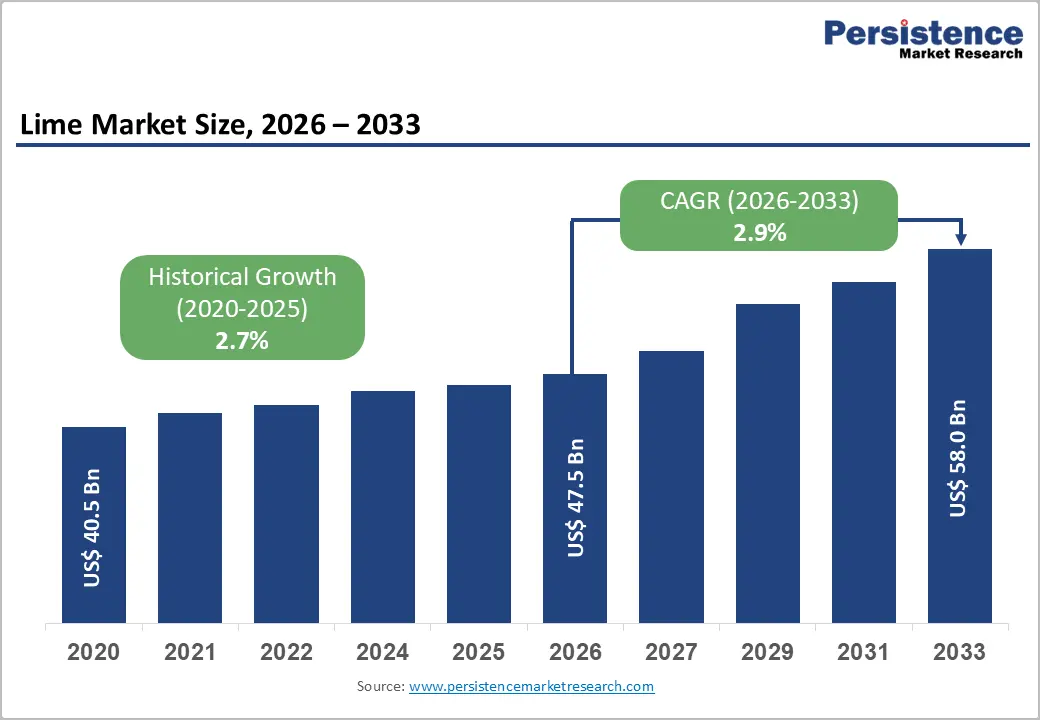

The global lime market size is expected to be valued at US$ 47.5 billion in 2026 and projected to reach US$ 58.0 billion by 2033, growing at a CAGR of 2.9% between 2026 and 2033. This steady, volume-driven expansion is primarily underpinned by the critical and non-substitutable role of lime in steel production, environmental remediation, and water treatment, sectors experiencing consistent global demand growth.

The market grew from US$ 40.5 billion in 2020 at a historical CAGR of 2.7%, supported by expanding steel manufacturing in the Asia Pacific, increasing regulatory requirements for flue gas desulfurization (FGD) and wastewater treatment, and growing construction activity across emerging economies in Latin America, the Middle East, and Southeast Asia.

Key Industry Highlights:

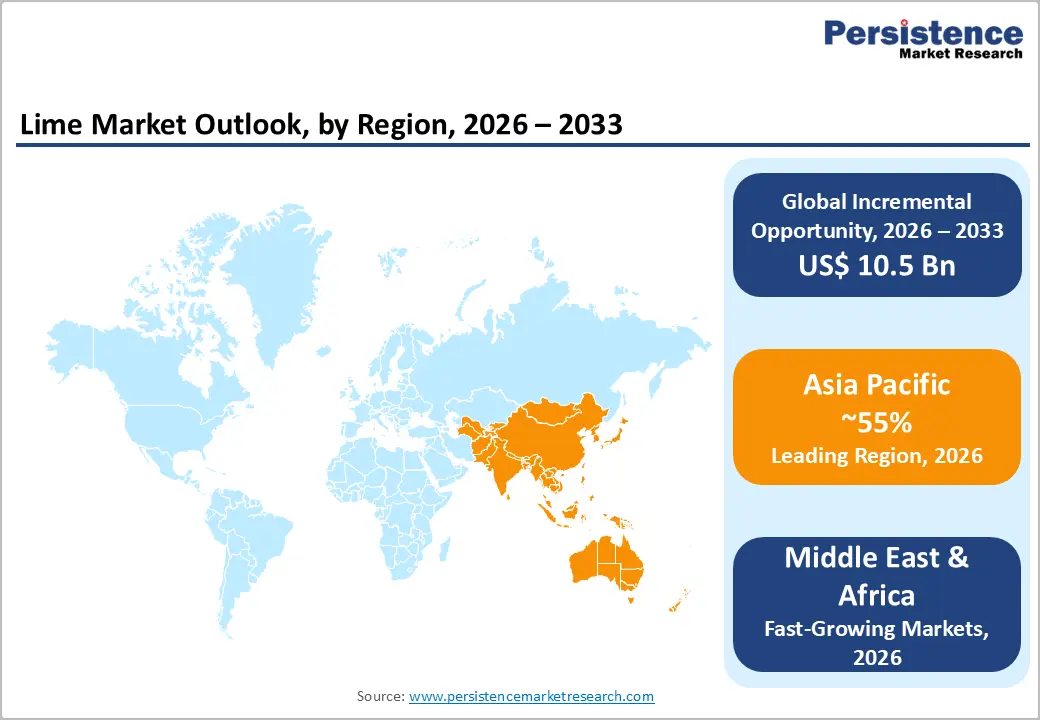

- Leading Region: Asia Pacific commands 55% of the global lime market share in 2025, anchored by China's dominant steel production of over 1 billion tonnes per year, India's expanding metallurgical sector targeting 300 MTPA by 2030, and Japan's mature industrial lime consumption.

- Fastest-Growing Region: MEA is the fastest-growing lime region through 2026 - 2033, driven by Gulf Cooperation Council infrastructure mega-projects, expanding steel and construction industries in Saudi Arabia and UAE under Vision 2030, and growing environmental treatment compliance requirements across Africa's mining sector.

- Dominant Product Type: Quicklime holds 65% market share in 2025, dominating through its superior reactivity, cost efficiency in industrial applications, and critical role in steelmaking, consuming 40-60 kg per tonne of crude steel, with global annual crude steel output of approximately 1.9 billion tonnes per the World Steel Association.

- Fastest-Growing Application: Environmental applications are the fastest-growing lime use category, driven by expanding EPA Clean Air Act FGD compliance, EU Industrial Emissions Directive mandates, and the expansion of WHO/EPA-compliant water treatment infrastructure across rapidly urbanizing developing economies in Asia, Africa, and Latin America.

- Key Opportunity: EAF green steelmaking growth, projected by the World Steel Association to reach 45-50% of global production by 2050, sustains lime demand, while emerging lime-based carbon mineralization and CCUS applications open new high-value product categories for forward-looking lime producers through 2033.

Market Dynamics

Drivers - Indispensable Role of Lime in Global Steel Production and Metallurgical Processes

Lime is a critical and non-substitutable reagent in steelmaking, consumed at rates of approximately 40-60 kg per tonne of crude steel produced for slag formation, desulfurization, and flux applications. The World Steel Association reports global crude steel production of approximately 1.9 billion tonnes annually, with demand projected to grow in line with urbanization and infrastructure investment, particularly across South and Southeast Asia.

India's steel production target of 300 million tonnes per annum (MTPA) by 2030 under the National Steel Policy, and China's sustained position as the world's largest steel producer, consuming over 1 billion tonnes per year, collectively guarantee enormous and growing primary quicklime consumption in metallurgical applications, making steel the single most important structural demand anchor for the lime market globally.

Accelerating Environmental Regulations Driving Lime Demand in Flue Gas Desulfurization and Water Treatment

Tightening environmental regulations worldwide are creating strong structural demand for lime in pollution control and water treatment applications. The U.S. Environmental Protection Agency (EPA) has expanded requirements for SO2 and NOx emission reductions from coal-fired power plants under the Clean Air Act, with lime-based flue gas desulfurization (FGD) systems consuming millions of tonnes of hydrated lime and limestone annually. The European Union's Industrial Emissions Directive (IED) and Large Combustion Plant (LCP) BREF similarly mandate FGD installation at thermal power stations across member states.

In water treatment, lime is the reagent of choice for pH adjustment, softening, and heavy-metal precipitation, with WHO and U.S. EPA standards driving municipal water utilities globally to expand treatment infrastructure, sustaining consistent growth in hydrated lime demand.

Market Restraints

High Energy Intensity of Lime Calcination and Carbon Emissions Compliance Costs

Lime production via limestone calcination is highly energy-intensive, requiring kiln temperatures of approximately 900-1,200°C and consuming 3.2-4.5 GJ per tonne of quicklime produced. Energy costs typically represent 30-40% of total lime production costs, making lime producers acutely sensitive to fuel price volatility. Additionally, lime production is inherently a significant source of process CO2 emissions, approximately 0.78 tonnes of CO2 per tonne of quicklime from limestone decomposition alone, creating growing compliance cost exposure under the EU Emissions Trading System (EU ETS) and similar carbon pricing mechanisms globally.

Availability of Alternative Reagents in Select Applications

In certain applications, particularly water treatment and some environmental uses, lime faces competition from alternative alkaline reagents. Caustic soda (sodium hydroxide) and soda ash can substitute for lime in specific pH adjustment and precipitation applications where logistics, handling safety, and process consistency favor liquid alkali systems.

The American Water Works Association (AWWA) technical literature notes that large municipal plants in some regions have transitioned to caustic soda delivery systems to avoid on-site lime slaking infrastructure costs. While lime remains dominant due to its cost advantage at scale, competition from alternative reagents constrains price realization and market share in select treatment applications.

Opportunities - Carbon Capture and Steel Decarbonization: Lime as a Critical Input for Green Steel Technologies

The accelerating transition toward low-carbon steelmaking presents a significant dual opportunity for lime producers. Electric arc furnace (EAF) steelmaking, which uses scrap steel rather than virgin iron ore and is the basis of green steel production, consumes comparable lime volumes to basic oxygen furnace (BOF) routes for slag conditioning and desulfurization. The World Steel Association projects EAF's share of global steel production to grow substantially toward 45-50% by 2050.

Additionally, emerging carbon capture, utilization, and storage (CCUS) technologies, including lime carbonation processes, position lime producers as potential participants in the emerging carbon removal economy. Lhoist Group and Graymont have begun exploring lime-based carbon mineralization applications, opening new high-value product categories beyond traditional industrial uses.

Environmental Remediation and Soil Stabilization in Infrastructure Development

Growing global infrastructure investment and tightening environmental remediation standards are creating an expanding demand opportunity for hydrated lime in soil stabilization and contaminated land treatment applications. Lime-treated soil, where quicklime or hydrated lime is mixed with clay soils to improve bearing capacity and reduce plasticity, is a widely used ground improvement technique for road construction, airport runways, and building foundations.

The U.S. Federal Highway Administration (FHWA) technical guidelines endorse lime soil stabilization as a cost-effective pavement subgrade improvement method. India's Bharatmala Pariyojana highway expansion program and ASEAN's cumulative US$ 210 billion annual infrastructure investment pipeline are generating significant incremental demand for lime in soil stabilization and environmental remediation across high-growth developing economy markets.

Category-wise Analysis

Product Type Insights

Quicklime dominates the Product Type segment, accounting for approximately 65% market share in 2025. Quicklime (calcium oxide, CaO) is the direct product of limestone calcination and the preferred form for high-temperature industrial applications, including steelmaking, glass production, and chemical manufacturing, where its high reactivity and concentrated calcium content deliver superior process performance per unit mass.

The National Lime Association (NLA) reports that steel production and chemical manufacturing collectively account for the majority of quicklime consumption in the United States, a pattern replicated across major industrial economies globally. Quicklime's cost advantage over hydrated lime, its requirement for no additional slaking process, and its suitability for bulk logistics via rail and truck further entrench its dominance in heavy industrial supply chains served by producers including Carmeuse, Lhoist Group, and Mississippi Lime Company.

Purity Level Insights

High calcium lime represents the leading purity level segment, accounting for approximately 72% market share in 2025. High-calcium lime, defined as having a calcium oxide content of 90-98% (CaO basis), is the preferred specification for steelmaking, chemical manufacturing, water treatment, and flue gas desulfurization applications where high reactivity and purity are critical to process performance and product quality. ASTM C110 and EN 459 standards for lime quality in construction and industrial applications define minimum CaO content requirements that most end-use specifications reference.

Dolomitic lime, containing both calcium and magnesium oxides, commands premium pricing in niche applications, including refractory lining, soil stabilization on magnesium-deficient soils, and specific glass formulations, but its smaller addressable market limits its overall revenue share relative to high-calcium variants.

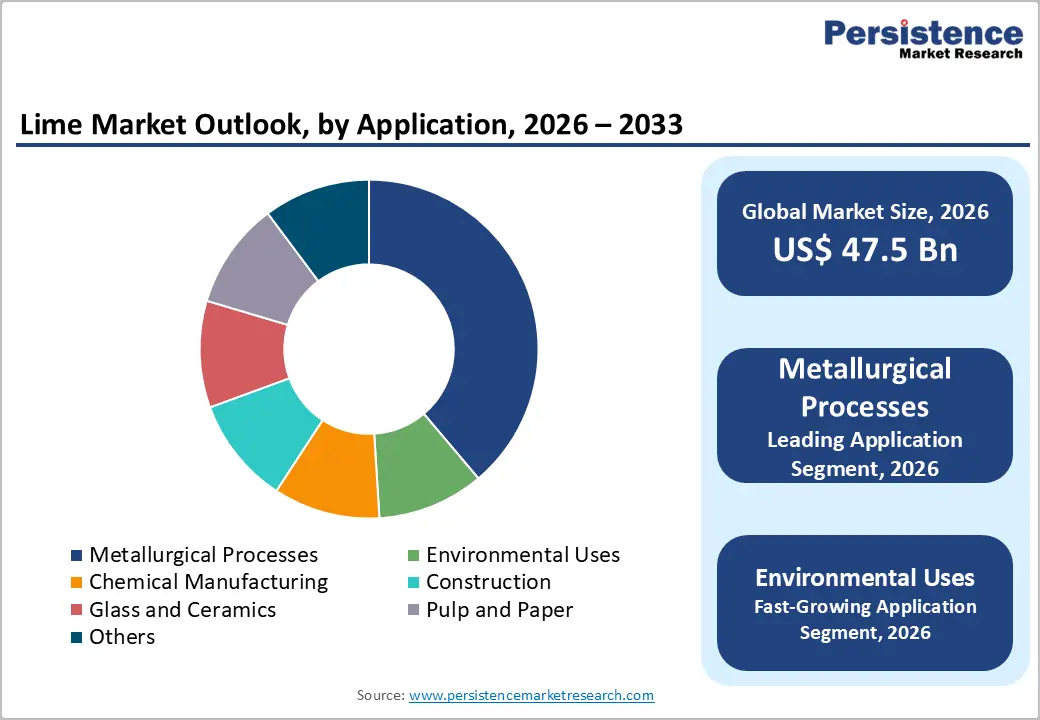

Application Insights

Metallurgical processes represent the dominant Application segment, accounting for approximately 40% of total lime market share in 2025. Steel, iron, and non-ferrous metal production collectively constitute the world's largest end-use category for quicklime, consuming it for slag fluidity control, sulfur removal, and flux chemistry optimization. The World Steel Association's data on annual global crude steel output of approximately 1.9 billion tonnes directly quantifies the scale of metallurgical lime demand.

Beyond steel, lime is used in copper, lead, zinc, and gold processing for pH control and precipitate separation. The industry's geographic concentration in China, India, Japan, South Korea, and Germany, all major steel-producing economies, means metallurgical lime demand closely tracks industrial output and infrastructure investment cycles in these key markets.

Regional Insights

Asia Pacific leads the global lime market with approximately 55% market share in 2025, while Middle East & Africa (MEA) is the fastest growing region, projected to record the highest CAGR through 2026 - 2033, driven by infrastructure construction, industrial expansion, and environmental compliance investment.

North America Lime Market Trends and Insights

North America is a mature lime market driven by consistent steel sector demand, expanding environmental applications, particularly FGD for power plant emission compliance and municipal water treatment, and infrastructure construction activity. The region benefits from high-quality limestone reserves and well-established lime production infrastructure. The growing demand for lime in soil stabilization under the U.S. Infrastructure Investment and Jobs Act represents an incremental catalyst for growth.

U.S. Lime Market Size

The United States accounts for approximately 81% of the North American lime market revenue in 2025. According to U.S. Geological Survey (USGS) data, U.S. lime production capacity exceeds 20 million tonnes annually, with steel, chemical manufacturing, and environmental treatment as the leading end-use sectors. United States Lime & Minerals, Inc., Mississippi Lime Company, and Graymont are among the key domestic suppliers sustaining this well-developed market.

Europe Lime Market Trends and Insights

Europe is a technologically advanced lime market shaped by stringent environmental regulations under the EU Industrial Emissions Directive, active steel production clusters in Germany, France, and the UK, and growing construction sector demand. The EU ETS is driving lime producers to invest in kiln efficiency and carbon capture, while environmental compliance applications, FGD, wastewater treatment, and soil remediation remain strong structural growth vectors across the region.

Germany Lime Market Size

Germany holds approximately 21% of the European lime market in 2025. Germany's integrated steel industry, anchored by thyssenkrupp Steel and Salzgitter AG, is the largest single consumer of quicklime in the country. Environmental applications, including FGD at coal-fired power plants and industrial wastewater treatment, are further significant demand sources. Lhoist Group operates major German production facilities serving these industrial customers.

U.K. Lime Market Size

The United Kingdom accounts for approximately 11% of the European lime market in 2025. UK lime demand is driven by water treatment, with Water UK reporting continued infrastructure investment in drinking water and wastewater treatment, construction, and environmental remediation. Tarmac Building Products (part of CRH plc) and Nordkalk Corporation serve the UK market through domestic production and import supply chains.

France Lime Market Size

France contributes approximately 10% of the European lime market in 2025. French lime demand is anchored by steel production at ArcelorMittal facilities, the country's significant chemical manufacturing sector, and water treatment requirements for one of Europe's largest urban populations. Lhoist Group's French operations and Carmeuse's European network both maintain strategic supply presence in the French industrial market.

Asia Pacific Lime Market Trends and Insights

Asia Pacific dominates global lime consumption, led by China, which accounts for approximately 55% of Asia Pacific demand, through its unparalleled steel production volumes and active construction sector. Chinese producers, including Anhui Conch Group and Jiangxi Wannianqing Cement Co., Ltd., serve extensive domestic industrial demand. India, Japan, and Southeast Asian markets are secondary but growing demand centers, each driven by distinct steel, construction, and environmental compliance drivers.

India Lime Market Size

India represents approximately 16% of the Asia Pacific lime market revenue in 2025. India's rapidly expanding steel sector, targeting 300 MTPA capacity by 2030 per the National Steel Policy, combined with construction growth from PMAY and Smart Cities Mission, and expanding water treatment infrastructure, drives multi-sector lime demand. Tata Chemicals and Shree Cement Ltd. are among India's key lime producers serving domestic industrial customers.

Japan Lime Market Size

Japan contributes approximately 9% of the Asia Pacific lime market revenue in 2025. Japan's mature but stable steel industry, producing approximately 85-90 million tonnes of crude steel annually per World Steel Association data, is the primary lime consumer. Environmental applications, including FGD at coal and LNG power plants, and specialized glass and ceramic production for the country's advanced manufacturing sector, provide additional steady demand streams.

Southeast Asia Lime Market Size

Southeast Asia collectively represents approximately 10% of the Asia Pacific lime market revenue in 2025. Vietnam, Indonesia, and Thailand are the primary demand markets, driven by rapidly expanding construction sectors, growing steel mini-mill activity, and increasing environmental compliance requirements for industrial wastewater treatment. The ASEAN Economic Community's infrastructure investment priorities and the region's growing mining activity, which require lime for ore processing and tailings treatment, are key growth drivers sustaining expanding lime demand.

Competitive Landscape

The global lime market demonstrates a moderately consolidated structure, with a limited number of large, vertically integrated producers controlling substantial limestone reserves and operating multi-regional production networks. Entry barriers remain high due to resource ownership, capital-intensive kiln infrastructure, and logistical dependence on proximity to end-use industries such as steel and chemicals, reinforcing the dominance of established players.

From a strategic standpoint, companies are prioritizing operational efficiency and sustainability through investments in energy-efficient kiln technologies and emissions reduction initiatives aligned with tightening carbon regulations. Long-term supply agreements with key industrial consumers ensure demand stability, while regional expansion is largely driven by bolt-on acquisitions of quarries and production assets. Additionally, players are exploring emerging applications such as carbon capture and mineralization to diversify revenue streams and align with global decarbonization trends.

Key Developments

- July, 2025: Pacific Lime and Cement Limited launched its quicklime business in Western Australia, establishing an integrated supply chain to mining customers and positioning itself as a cost-effective, high-quality supplier with plans for regional expansion.

- February, 2025: SaltX Technology achieved a breakthrough in electrified, emission-free quicklime production, meeting key quality and runtime targets at its pilot plant and advancing commercialization with successful material testing for steel industry applications.

Lime Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 40.5 Billion |

| Current Market Value (2026) | US$ 47.5 Billion |

| Projected Market Value (2033) | US$ 58.0 Billion |

| CAGR (2026 - 2033) | 2.9% |

| Leading Region | Asia Pacific, 55% market share (2025) |

| Dominant Product Type | Quicklime, 65% market share (2025) |

| Top-Ranking Purity Level | High Calcium Lime, 72% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 10.5 Billion |

Companies Covered in Lime Market

- Carmeuse

- Graymont

- Lhoist Group

- Mississippi Lime Company

- Cheney Lime & Cement Company

- United States Lime & Minerals, Inc.

- Anhui Conch Group

- Nordkalk Corporation

- Xinjiang Zhongtai Chemical Co., Ltd.

- Jiangxi Wannianqing Cement Co., Ltd.

- Cimpor - Cimentos de Portugal

- Omya AG

- Tata Chemicals

- Shree Cement Ltd.

- Cimsa Cimento

- Sibelco

- Pete Lien & Sons, Inc.

- Cape Lime (Pty) Ltd.

Frequently Asked Questions

The global lime market is projected to reach US$ 47.5 billion by 2026, driven by steady demand from steelmaking, environmental applications, and construction.

Key drivers include its essential use in steel production and rising demand from environmental regulations for air pollution control and water treatment.

Asia Pacific leads the market with around 55% share, supported by strong steel production in China and expanding industrial activity in India.

Major growth opportunities lie in green steel production, carbon capture applications, and infrastructure-driven soil stabilization projects.

Key players include Lhoist Group, Carmeuse, Graymont, United States Lime & Minerals, Inc., Mississippi Lime Company, Nordkalk Corporation, Anhui Conch Group, Tata Chemicals, Omya AG, Shree Cement Ltd., and Cimsa Cimento.