- Technology

- LegalTech Market

LegalTech Market Size, Share, and Growth Forecast, 2026 - 2033

LegalTech Market by Offering (Software, Services), Application (Case & Practice Management, Document Management, Legal Research, E-discovery, Contract Lifecycle Management, Time-Tracking & Billing, Compliance & Risk Management, Legal Analytics & Knowledge Management, Others), End-user, and Regional Analysis for 2026 - 2033

LegalTech Market Size and Trends Analysis

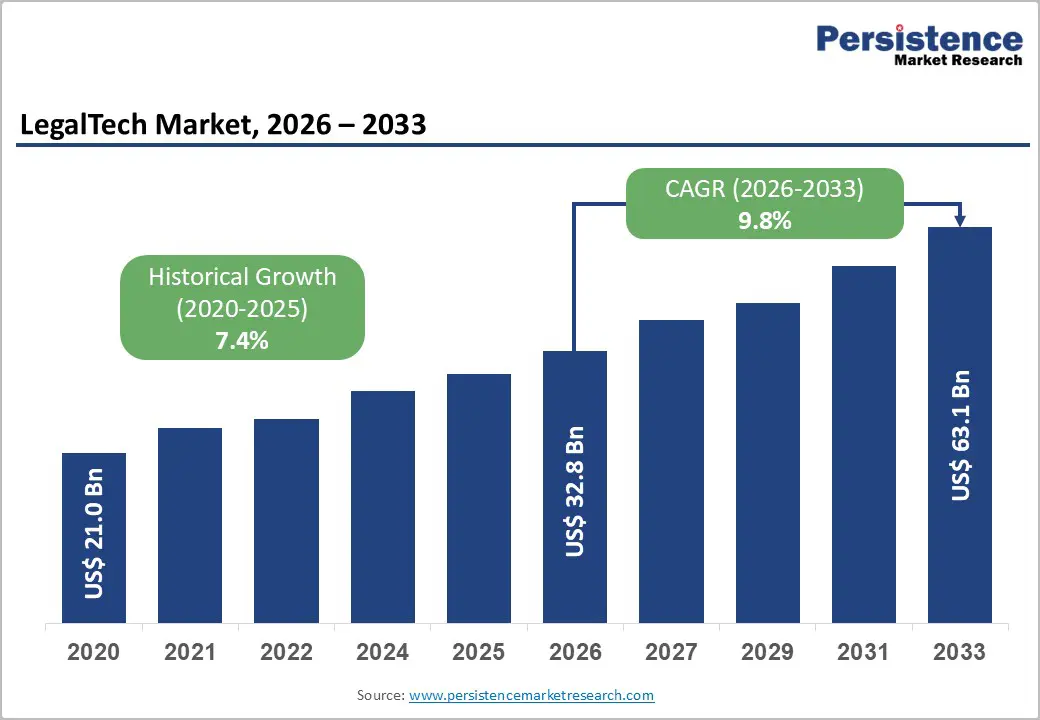

The global legaltech market size is projected to rise from US$32.8 billion in 2026 to US$63.1 billion by 2033, growing at a CAGR of 9.8% during the forecast period from 2026 to 2033, driven by the rapid adoption of AI-powered automation and intelligent routing technologies, which reduce operational costs, increase enterprise investment in unified customer data platforms that enable hyper-personalization and real-time journey orchestration, and the exponential growth of mobile-first engagement strategies and conversational commerce.

The market is transitioning from reactive support models to predictive, autonomous engagement platforms, with cloud-based deployment models growing fastest due to superior scalability and cost efficiency compared to on-premises solutions.

Key Industry Highlights:

- Prominent Offering: Software dominates with over 72% market share in 2026, valued at more than US$ 23.6 Bn, driven by the need for scalable automation, AI-enabled workflows, and repeatable legal processes that reduce human error and operational costs. Services are the fastest-growing segment at 8.6% CAGR, supported by rising demand for implementation, customization, training, and managed support for complex legal technologies.

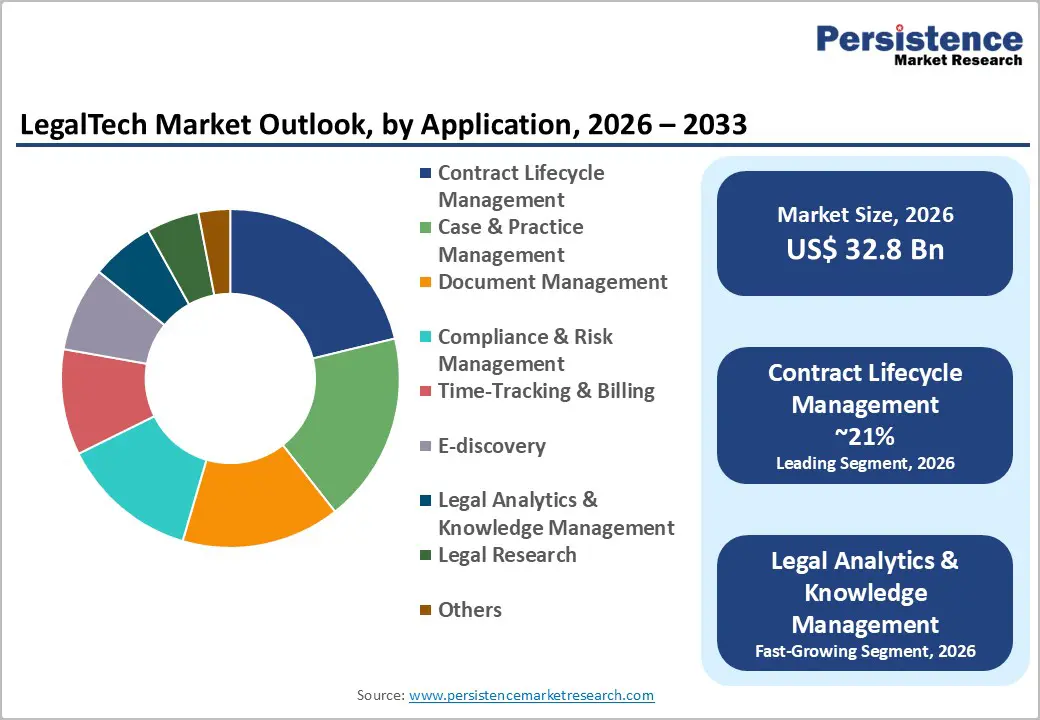

- Leading Application: Contract lifecycle management holds over 21% market share in 2026, valued at more than US$ 6.9 Bn, due to the critical need for centralized contract control, compliance, audit readiness, and revenue leakage prevention. Legal analytics & knowledge management is the fastest-growing application at 13.9% CAGR, driven by the need for predictive insights, institutional knowledge capture, and data-backed decision-making.

- Leading End-user: Law Firms hold the largest market share at over 48% in 2026, valued at more than US$15.8Bn, driven by high document volume, time-sensitive case management, and rising client expectations for transparency and speed. Corporate Legal Departments grow fastest at 15.1% CAGR, driven by regulatory pressure, global expansion, contract complexity, and demand for cost-effective internal legal operations.

- Leading Region: North America leads with over 38% share in 2026, valued at US$ 12.5 Bn, driven by high digital maturity, early technology adoption, and strong regulatory complexity that fuels automation and risk management investments. Asia Pacific is the fastest-growing region at 15.7% CAGR, fueled by improving digital infrastructure, rising legal complexity, and government-led digital transformation initiatives.

| Key Insights | Details |

|---|---|

| LegalTech Market Size (2026E) | US$32.8 Bn |

| Market Value Forecast (2033F) | US$63.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.4% |

Market Dynamics

Driver - Rising Demand for Omnichannel Experiences and Real-Time Personalization

Rising client expectations for seamless, omnichannel legal experiences are driving the adoption of advanced LegalTech platforms across law firms and corporate legal departments. Organizations leveraging end-to-end client and case journey mapping report 15-20% improvements in engagement efficiency, matter conversion, and client lifetime value through personalized communication and proactive updates. The proliferation of mobile devices, cloud-based legal platforms, and connected workflows enables real-time, context-aware interactions across portals, virtual consultations, and case management systems. Intelligent routing and workflow automation improve resource utilization while reducing response times and service bottlenecks. This demand is structural rather than cyclical, as digitally native clients increasingly view transparent, always-available legal services as a baseline expectation rather than a premium offering.

AI and Generative AI Adoption for Workflow Automation

AI and generative AI are accelerating LegalTech adoption by automating knowledge-intensive workflows and enhancing customer engagement through predictive analytics. According to the Federal Bar Association, 54% of legal professionals use AI to draft correspondence, while 14% use it to analyze firm data and legal matters. Generative AI automates a large share of routine legal tasks such as document preparation, information gathering, and data analysis, improving efficiency and accuracy. Firms implementing AI-driven workflow and engagement solutions achieve meaningful reductions in handling time and better first-contact resolution. Larger law firms adopt these technologies faster due to scalability advantages, driving sustained investment.

Restraint -Compliance, Ethical, and Regulatory Complexity in Technology Implementation

Stringent data privacy, consumer protection, and AI governance regulations, particularly in Europe and North America, require significant investment in security infrastructure, data governance, and ongoing regulatory monitoring. Ensuring human oversight and legal accuracy of AI-driven outputs poses operational and ethical challenges for law firms and enterprises. Organizations must conduct extensive risk assessments, implement governance frameworks, and maintain detailed audit trails to demonstrate compliance. Fragmented regulations across geographies increase localization costs and implementation complexity. High non-compliance penalties discourage adoption, especially among mid-sized and smaller firms, while favoring large, well-resourced market leaders.

Cost Barriers and the Complexity of Technology Integration with Legacy Systems

Organizations often face dual-cost structures, needing to maintain existing platforms while deploying new technologies during transition phases. Integration becomes more challenging when multiple systems, such as case management, billing, document repositories, and client databases, must be connected. Mid-sized and smaller firms typically lack in-house IT expertise, increasing reliance on costly external consultants. Although cloud-based models reduce initial capital expenditure, recurring subscription costs strain budgets for firms accustomed to perpetual licensing. These factors disproportionately limit adoption among smaller players, accelerating market consolidation and restricting adoption to organizations with sufficient scale.

Opportunity - Convergence of Emerging Technologies into Intelligent Omnichannel Platforms

The convergence of AI, machine learning, NLP, blockchain, and IoT within unified LegalTech platforms creates strong opportunities for differentiation and the creation of entirely new solution categories. Advanced and predictive analytics enable law firms and enterprises to anticipate client needs and shift from reactive service delivery to proactive, data-driven engagement. Machine-learning-powered personalization engines allow individual-level customization of legal workflows, documents, and advisory services at unprecedented scale. NLP-driven conversational platforms streamline client interactions via intuitive, frictionless interfaces. Solutions integrating three or more technologies command premium valuations and deliver 10-20% higher client retention, accelerating adoption of vertical-specific LegalTech solutions across legal services, finance, healthcare, and e-commerce.

Rising Demand for Data-Driven Legal Insights and Expansion of In-House Legal Teams

The growing demand for data-driven legal decision-making is pushing organizations to adopt platforms that deliver actionable insights through analytics, AI, and predictive modeling. Law departments increasingly rely on data to assess litigation risk, forecast case outcomes, optimize spend, and benchmark performance, creating strong demand for legal analytics and intelligence tools. The expansion of in-house legal departments is shifting work away from external law firms toward technology-enabled internal teams. In-house teams prioritize efficiency, cost control, and scalability, driving adoption of contract lifecycle management, e-discovery, compliance, and workflow automation solutions. As in-house teams take on more strategic roles, demand rises for tools that translate legal data into business-aligned insights.

Category-wise Analysis

Offering Insights

Software is a dominant category likely to capture more than 72% share in 2026 with a value exceeding US$ 23.6 Bn, due to the need for scalable, repeatable, and automation-driven solutions rather than labor-intensive services. Organizations rely on software to handle high volumes of documents, contracts, compliance checks, and legal research with speed and accuracy. Software platforms embed AI, analytics, and workflow automation, enabling consistent outcomes while reducing human error and operational costs. Software supports remote collaboration, data security, audit trails, and regulatory compliance, which are critical daily needs across jurisdictions.

Services are projected to grow at an 8.6% CAGR, driven by organizations' need for hands-on support to implement, customize, and integrate complex legal technologies into existing workflows. Law firms and corporate legal departments require advisory and consulting services to ensure regulatory compliance, data security, and ethical use of AI. Ongoing support, managed services, and training are critical to drive user adoption and maintain system accuracy as laws and regulations change.

Application Insights

Contract lifecycle management accounts for over 21% market share in 2026, with a value exceeding US$6.9Bn. Organizations urgently need tighter control over contracts to reduce legal, financial, and compliance risks. Businesses manage thousands of contracts across vendors, customers, and partners, making manual tracking inefficient and error-prone. CLM platforms centralize drafting, negotiation, approvals, and renewals, improving visibility and accountability across departments. The growing focus on regulatory compliance, audit readiness, and revenue leakage prevention further drives adoption.

Legal analytics & knowledge management is expected to grow at the highest rate, with a 13.9% CAGR, as legal teams face rising pressure to make faster, data-driven decisions while managing an explosion of legal information. Firms and in-house counsels need predictive insights on case outcomes, litigation risks, contract performance, and judicial behavior to control costs and improve success rates. Knowledge management tools address the need to capture institutional expertise, reduce dependency on individual lawyers, and avoid repeated work. As efficiency, risk mitigation, and outcome predictability become strategic priorities, analytics-driven intelligence becomes essential.

End-user Insights

Law Firms command the largest market share at over 48% in 2026, with a value exceeding US$ 15.8 Bn, due to their core operations being highly document-intensive, time-sensitive, and compliance-driven, creating strong demand for automation and efficiency tools. They face constant pressure to reduce turnaround time, control billable hours, and improve accuracy in legal research, drafting, and case management. Growing client expectations for transparency, cost predictability, and faster outcomes further push firms to adopt digital platforms.

Corporate legal departments are expected to grow at a 15.1% CAGR as they face increasing regulatory pressure, contract complexity, and litigation risk as businesses scale globally. They need automation to manage high volumes of contracts, compliance tracking, and e-discovery while controlling external legal spending. LegalTech enables in-house teams to improve visibility, standardization, and turnaround time without expanding headcount. The demand for data-driven decision-making and real-time legal risk insights further accelerates technology adoption within corporate legal functions.

Regional Insights

North America LegalTech Market Trends

North America holds over 38% of the market in 2026, reaching US$12.5 B in value, driven by a highly developed legal services ecosystem, strong digital maturity, and a culture of early technology adoption. Regulatory complexity around compliance, data privacy, and AI governance continues to stimulate sustained investment in legal risk management and automation solutions. The U.S. leads regional demand, and advancements in AI and machine learning are expanding use cases and improving efficiency across law firms and enterprises. The region features intense competition between established software providers and innovative startups, with ongoing consolidation shaping the market. Venture capital activity remains strong, increasingly favoring companies with scalable models and a clear path to profitability.

Asia Pacific LegalTech Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 15.7%, driven by great, untapped demand and rapidly improving digital infrastructure across major economies. Growth is supported by expanding industrial activity, rising legal complexity, and strong government-led digital transformation of legal and judicial systems. China, India, Japan, South Korea, and Southeast Asia each play distinct roles, with growth ranging from high-growth emerging markets to more mature but stable adopters. Price sensitivity is higher than in Western markets, making value-based offerings and flexible pricing essential. Success in the region depends heavily on localization, regulatory alignment, and partnerships with regional firms and government bodies.

Europe LegalTech Market Trends

Europe is expected to hold more than 22% share by 2026, shaped by strong regulatory oversight and a fragmented, multi-country legal landscape. Stringent EU data protection requirements, ongoing regulatory updates, and the need for compliant, secure legal technology solutions. Cross-border expansion and consolidation within the legal profession are increasing the demand for integrated platforms that operate across jurisdictions. Corporate legal departments are also expanding their use of technology to improve efficiency and risk management. Investment activity has traditionally been conservative, but growing awareness of LegalTech’s return on investment is accelerating funding and innovation across the region.

Competitive Landscape

The LegalTech market is moderately fragmented, with a mix of global platform leaders and numerous niche solution providers. Companies are focusing on product differentiation through AI-driven automation, analytics, and workflow intelligence to improve accuracy and efficiency for law firms and enterprises. Manufacturers emphasize cloud-first and scalable SaaS models to reduce deployment complexity and support omnichannel legal operations. Strong compliance, data security, and regulatory alignment are leveraged as key competitive advantages, especially in highly regulated jurisdictions.

Key Developments:

- In December 2025, Filevine acquired AI-powered contract redlining company Pincites in an all-cash deal. The acquisition brings Pincites co-founders Sona and Mariam Sulakian and their team to Filevine, strengthening its AI-first strategy and building on prior moves into contract lifecycle management.

- In January 2025, Relativity announced that starting Jan. 1, 2028, all new matters must be hosted on its cloud platform, RelativityOne, signaling the end of its legacy on-premises Relativity Server. With over 75% of its business already in the cloud, the move marks a major shift toward cloud-based e-discovery in the legal industry.

Companies Covered in LegalTech Market

- Docusign, Inc.

- Wolters Kluwer N.V.

- Thomson Reuters

- iManage LLC

- Relativity ODA LLC

- Mitratech Holdings, Inc.

- Casetext Inc.

- Icertis, Inc.

- Everlaw, Inc.

- Harvey AI Corporation

- Filevine Inc

- Others

Frequently Asked Questions

The global market is projected to be valued at US$32.8 Bn in 2026.

The need to reduce legal costs and improve efficiency through automation, while ensuring faster, more accurate handling of documents, contracts, and compliance tasks, is a key driver of the market.

The LegalTech market is expected to witness a CAGR of 9.8% from 2026 to 2033.

The convergence of AI, blockchain, and automation into intelligent omnichannel legal platforms and the growing demand for data-driven legal insights is creating strong growth opportunities.

Docusign, Inc., Wolters Kluwer N.V., Thomson Reuters, iManage LLC, Relativity ODA LLC, Mitratech Holdings, Inc. are among the leading key players.