- Pharmaceuticals

- Ineffective Esophageal Motility Treatment Market

Ineffective Esophageal Motility Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Ineffective Esophageal Motility Treatment Market by Product (Devices including Reflux Management Systems, Endoscopic Pain Modulators, Endostaplers, Radiofrequency (RF) Ablation Devices, Myotomy, and Drugs including H2 Receptor Antagonist, Antacids, Proton Pump Inhibitors, Dopamine Antagonist, Prokinetic Agents, Calcium Channel Blockers), by Indication (Gastroesophageal Reflux Disease (GERD), Dysphagia, Achalasia, Others), by End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Retail & Online Pharmacies), by Regional Analysis, 2026-2033

Ineffective Esophageal Motility Treatment Market Size and Trends Analysis

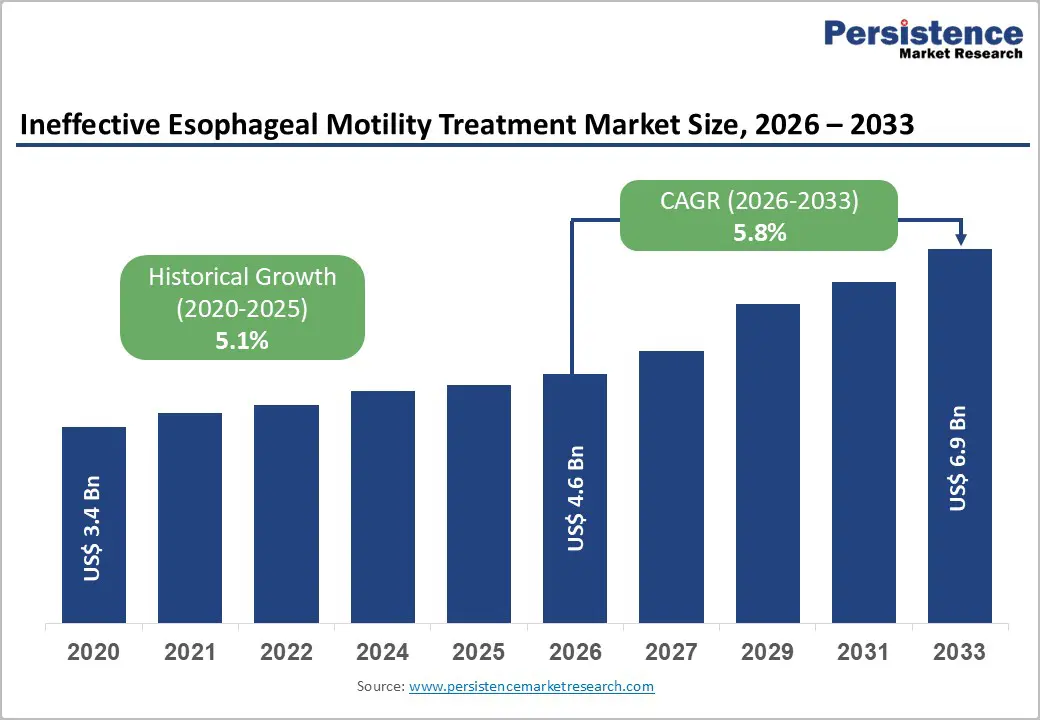

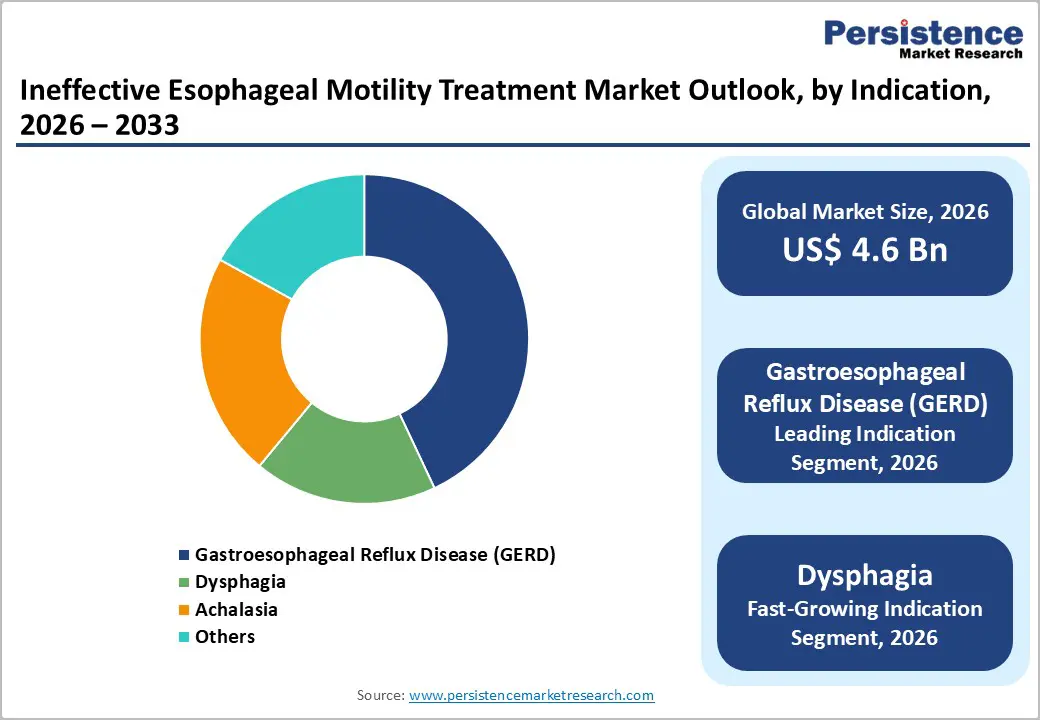

The global ineffective esophageal motility treatment market size is expected to be valued at US$ 4.6 billion in 2026 and projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

Market growth is primarily driven by the increasing prevalence of esophageal motility disorders, particularly gastroesophageal reflux disease (GERD), coupled with advancements in diagnostic technologies such as high-resolution manometry (HRM) and improved clinical recognition among healthcare providers. The rising incidence of dysphagia and achalasia, especially among aging populations with comorbid conditions such as diabetes and autoimmune disorders, continues to expand the addressable patient population. Additionally, the growing emphasis on minimally invasive treatment procedures and personalized medicine approaches is encouraging both pharmaceutical and medical device companies to invest substantially in research and development initiatives targeting motility-enhancing therapeutics.

Key Highlights

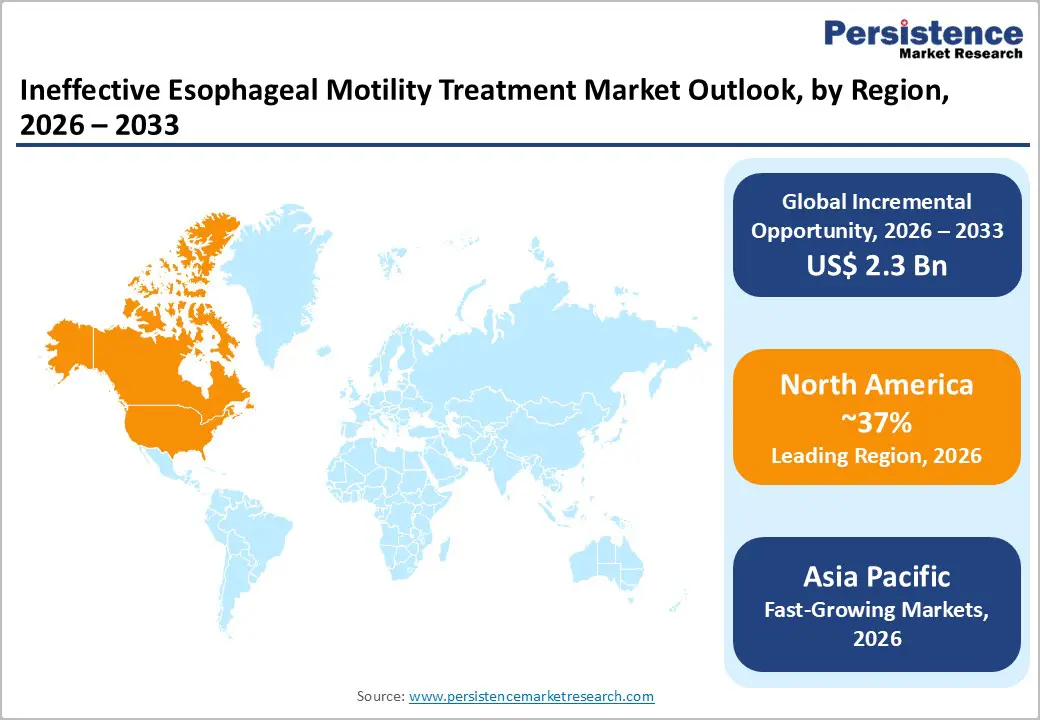

- North America leads the market with ~37% share in 2025, supported by advanced healthcare infrastructure, strong diagnostics, favorable reimbursement, and high treatment volumes.

- Asia-Pacific is the fastest-growing region, projected to grow at a CAGR of over 7–8% through 2032–2033, driven by healthcare expansion, aging populations, rising disease awareness, and increased adoption of minimally invasive therapies.

- GERD is the leading indication, accounting for ~43% market share in 2025 due to its high prevalence and consistent demand for drug-based and procedural treatments.

- Dysphagia is the fastest-growing indication, supported by aging demographics, neurological conditions, and advancements in endoscopic and rehabilitative therapies.

- Minimally invasive procedures such as POEM, RFA, and advanced endoscopic platforms represent key growth opportunities through 2033, addressing unmet needs in treatment-resistant patients.

| Global Market Attributes | Key Insights |

|---|---|

| Ineffective Esophageal Motility Treatment Market Size (2026E) | US$ 4.6 Billion |

| Market Value Forecast (2033F) | US$ 6.9 Billion |

| Projected Growth CAGR(2026-2033) | 5.8% |

| Historical Market Growth (2020-2025) | 5.1% |

Market Dynamics

Market Growth Drivers

Rising Prevalence of Esophageal Motility Disorders and Enhanced Diagnostic Awareness

The heightened recognition of ineffective esophageal motility as a distinct clinical entity is fundamentally reshaping the diagnostic and therapeutic landscape. Advances in high-resolution manometry (HRM) and esophageal impedance testing have significantly improved diagnostic accuracy, enabling clinicians to identify subtle motility changes that were previously misattributed to functional dyspepsia or non-specific reflux symptoms. Studies indicate that approximately 20-40% of patients presenting with reflux-type symptoms exhibit some degree of esophageal dysmotility, yet many remain underdiagnosed without access to advanced diagnostic tools. The growing body of clinical evidence establishing associations between motility dysfunction and treatment-resistant GERD has prompted increased referrals to specialized gastroenterology centers, accelerating earlier intervention and driving market expansion. Key opinion leaders and professional societies, including the American Gastroenterological Association (AGA) and American College of Gastroenterology (ACG), have increasingly emphasized the importance of manometric assessment in complex reflux cases, thereby strengthening clinical adoption and creating sustained demand for diagnostic and therapeutic interventions.

Expanding Aging Population and Associated Comorbidities Driving Treatment Demand

The global demographic shift toward aging populations significantly amplifies the incidence of esophageal motility disorders and related comorbidities requiring targeted treatment. Epidemiological data demonstrates that individuals aged 65 years and above experience substantially higher prevalence rates of dysphagia, achalasia, and reflux-related symptoms compared to younger cohorts. The aging process contributes to progressive weakening of esophageal peristalsis and lower esophageal sphincter (LES) dysfunction, compounded by comorbidities including diabetes mellitus, systemic sclerosis, and neurological disorders such as Parkinson's disease. Countries with mature healthcare systems, particularly in North America and Western Europe, are experiencing accelerated population aging, with projections indicating that individuals aged 60 and above will constitute nearly 35-40% of the population by 2050. This demographic transformation is expected to substantially increase the treatment-seeking population and drive sustained growth across all therapeutic categories, including pharmaceutical interventions and advanced minimally invasive procedures.

Market Restraints

Limited Efficacy of Current Pharmacological Options and Safety Concerns

Standard pharmaceutical interventions for esophageal motility disorders demonstrate significant efficacy limitations, with many patients exhibiting suboptimal response to conventional prokinetic agents. Metoclopramide, historically the primary pharmacological option, carries substantial long-term safety concerns, including the risk of tardive dyskinesia with prolonged use, which has prompted regulatory agencies including the U.S. FDA to restrict its duration of use to a maximum of 12 weeks. Alternative prokinetic agents such as domperidone show variable efficacy and remain unavailable in many developed markets due to regulatory concerns. The substantial proportion of patients developing tolerance to proton pump inhibitors (PPIs), the dominant reflux management therapy, creates therapeutic challenges, as these agents do not address underlying motility dysfunction. Furthermore, emerging evidence regarding potential long-term safety concerns associated with chronic PPI use, including increased risks of hypomagnesemia and vitamin B12 deficiency, has prompted clinicians to seek alternative approaches. The absence of universally effective pharmacological solutions with favorable side effect profiles constrains market expansion and necessitates development of novel therapeutic agents, which requires significant investment and regulatory approval timelines extending 8-12 years.

High Cost of Advanced Diagnostic and Procedural Interventions Limiting Access

The accessibility of advanced diagnostic modalities and minimally invasive therapeutic procedures remains significantly constrained by prohibitive costs in many healthcare settings, particularly in developing and middle-income economies. High-resolution manometry (HRM) systems and associated diagnostic catheters represent substantial capital investments ranging from US$ 150,000 to US$ 300,000 per system, limiting their availability to specialized tertiary care centers in developed nations. Minimally invasive procedural interventions such as peroral endoscopic myotomy (POEM), radiofrequency ablation (RFA) utilizing devices such as Stretta System, and advanced endoscopic techniques require specialized training, equipment infrastructure, and experienced multidisciplinary teams, restricting their deployment to high-volume academic and specialty centers. Reimbursement challenges further constrain market growth, as many insurance systems maintain restrictive coverage policies for novel therapeutic approaches pending long-term outcome data. The concentration of advanced treatment capabilities in developed healthcare systems creates significant treatment disparities, with patients in low- and middle-income countries predominantly reliant on older, less effective pharmaceutical approaches. This accessibility gap fundamentally limits the addressable market size and slows overall market expansion in geographically diverse regions.

Market Opportunities

Expansion of Minimally Invasive Therapeutic Procedures and Technological Innovation

The rapid evolution and clinical validation of minimally invasive endoscopic procedures represent a transformational opportunity for market participants to capture growing demand from patients and providers seeking alternatives to traditional surgical interventions. Peroral endoscopic myotomy (POEM), which represents a paradigm shift in achalasia and spastic esophageal disorder management, has demonstrated clinical success rates exceeding 88-96% in carefully selected patient populations, with significantly reduced morbidity compared to conventional laparoscopic approaches. The procedure is expanding globally, with clinical programs being established across North America, Europe, Asia-Pacific, and other regions, driving demand for specialized equipment, training, and supporting technologies. Radiofrequency ablation (RFA) devices, including the Stretta System from Mederi Therapeutics, continue demonstrating durable efficacy in GERD management with long-term follow-up studies demonstrating sustained symptomatic improvement and medication reduction in 70-75% of treated patients at 8-year follow-up. Novel endoscopic interventions including antireflux mucosectomy (ARM), transoral incisionless fundoplication (TIF), and advanced esophageal stenting technologies are emerging as effective options for refractory cases. Market participants investing in research, development, and clinical validation of these procedures, coupled with establishment of training infrastructure, are positioned to capitalize on the growing preference for minimally invasive approaches expected to drive 6-9% annual growth in the procedural device segment through 2033.

Advancement in Personalized Medicine and Novel Pharmacological Agents Addressing Unmet Needs

The therapeutic landscape for esophageal motility disorders is experiencing substantial innovation as pharmaceutical companies pursue novel drug classes targeting previously unaddressed pathophysiological mechanisms. Ghrelin agonists, serotonin modulators, and motilin receptor agonists represent emerging pharmacological categories demonstrating promising efficacy in preclinical and early clinical evaluations for enhancing esophageal peristalsis and improving symptom relief. The development of potassium-competitive acid blockers (P-CABs) offers superior acid suppression characteristics compared to conventional PPIs, with enhanced efficacy in refractory GERD cases, particularly those with concomitant motility dysfunction.

Category-wise Insights

Product Analysis

The product segment comprises therapeutic devices and pharmaceutical agents addressing esophageal motility dysfunction through distinct mechanisms of action. Within the device category, radiofrequency ablation (RFA) systems, endoscopic myotomy devices, and advanced reflux management systems are gaining significant clinical adoption. The Stretta System, representing the longest-established RF ablation platform with FDA approval since 2000 and documented efficacy in 10-year follow-up studies, maintains substantial market share within the minimally invasive device segment. Reflux management systems and endoscopic pain modulators are emerging device categories targeting procedural interventions for refractory reflux and associated pain manifestations. The pharmaceutical segment, representing approximately 55-60% of the overall market, is dominated by established drug classes including proton pump inhibitors (PPIs), which maintain therapeutic prevalence due to established efficacy and widespread clinical acceptance, despite limitations in addressing underlying motility dysfunction. Emerging pharmaceutical agents targeting novel mechanisms, including prokinetic agents, dopamine antagonists, and calcium channel blockers, represent growth opportunities as clinicians increasingly adopt personalized treatment algorithms combining pharmacological and procedural approaches for complex clinical presentations.

Indication Analysis

Gastroesophageal reflux disease (GERD) dominates the indication category with approximately 43% market share in 2025, driven by its high prevalence and substantial treatment-seeking behavior among affected populations. The condition represents a chronic disorder affecting 10-20% of the general population in developed healthcare systems and emerging higher prevalence rates in developing economies as lifestyle and dietary factors shift. The substantial unmet clinical need in GERD management, particularly in treatment-resistant cases unresponsive to conventional PPI therapy, drives demand for advanced diagnostic evaluation and innovative therapeutic approaches. Dysphagia, encompassing swallowing dysfunction from diverse etiologies including neurological, structural, and motility-related causes, represents the fastest-growing indication segment with projected CAGR exceeding 7-8% through 2032-2033. The expanding recognition of dysphagia prevalence in aging populations, neurological disease patients, and post-stroke rehabilitation cohorts is driving clinical focus and therapeutic investment. Achalasia, a rare primary motility disorder characterized by esophageal aperistalsis and LES dysfunction, represents an indication segment with high treatment intensity and emerging procedural opportunities. The adoption of POEM and other minimally invasive approaches for achalasia management is reshaping treatment paradigms and driving specialty procedure volume growth.

End User Analysis

Hospitals emerge as the leading end-user category, commanding dominant market share through their role in providing comprehensive diagnostic evaluation, procedural interventions, and inpatient care for acute esophageal motility-related presentations. Academic medical centers and tertiary referral hospitals concentrate expertise, advanced diagnostic infrastructure including high-resolution manometry, and specialized procedural capabilities, positioning them as principal treatment centers for complex cases. Specialty clinics dedicated to gastroenterology and esophageal disorders represent the fastest-growing end-user segment, driven by the proliferation of focused practice models and concentrated expertise in motility disorder management. Ambulatory surgical centers are increasingly offering advanced endoscopic procedures including POEM and radiofrequency ablation, capitalizing on the shift toward outpatient therapeutic interventions and improved reimbursement frameworks. Retail and online pharmacies demonstrate increasing significance as distribution channels for pharmaceutical interventions, particularly as direct-to-consumer awareness campaigns and telemedicine consultation models expand patient access to pharmacological therapies. The diversification of end-user channels reflects evolving healthcare delivery models emphasizing accessibility, cost-efficiency, and specialized care delivery across treatment modalities.

Regional Insights

North America Ineffective Esophageal Motility Treatment Market Trends and Insights

North America maintains dominant market positioning with approximately 37% market share in 2025, supported by sophisticated healthcare infrastructure, elevated disease awareness, and technological leadership in diagnostic and therapeutic innovation. The United States market, representing the largest geographic component, benefits from high diagnostic intensity driven by advanced high-resolution manometry availability and established clinical guidelines emphasizing specialist referral for reflux-refractory cases. The prevalence of GERD in North America is estimated at 15-20% of the adult population, creating substantial treatment volumes across pharmaceutical and procedural categories. Reimbursement frameworks in the United States demonstrate relatively favorable coverage for advanced diagnostics and minimally invasive procedures, supporting access to technologies such as radiofrequency ablation and emerging endoscopic interventions. The concentration of major medical device manufacturers including Johnson & Johnson, Medtronic, Torax Medical (producer of Stretta System), and emerging specialty companies in North America drives innovation velocity and rapid clinical technology adoption.

Asia-Pacific Ineffective Esophageal Motility Treatment Market Trends

The Asia-Pacific Ineffective Esophageal Motility (IEM) Treatment Market is emerging as a high-growth region, supported by rapid improvements in healthcare access, diagnostics, and specialist gastroenterology services. Rising awareness of digestive disorders, increasing prevalence of GERD and swallowing difficulties, and growing elderly populations are expanding the treated patient base across countries such as China, India, Japan, and South Korea. The region is witnessing wider adoption of high-resolution manometry and endoscopic interventions, enabling earlier and more accurate diagnosis of motility disorders. Cost-effective pharmacological therapies continue to dominate initial treatment, while demand for minimally invasive endoscopic procedures is increasing in urban tertiary hospitals. Expansion of private hospitals, medical tourism, and local manufacturing of GI devices is improving treatment affordability. In addition, physician education programs and growing patient willingness to seek care for chronic reflux and dysphagia symptoms are accelerating diagnosis rates. Collectively, these factors position Asia-Pacific as a key growth engine for the IEM treatment market over the forecast period.

Competitive Landscape

Market Structure Analysis

The Ineffective Esophageal Motility Treatment market is characterized by a moderately competitive landscape, driven by ongoing therapeutic innovation and expanding clinical adoption. Market participants focus on improving treatment efficacy through enhanced pharmacological formulations, minimally invasive endoscopic solutions, and supportive diagnostic technologies. Competition is influenced by product effectiveness, treatment safety, affordability, and physician preference. Regulatory approvals and clinical evidence play a critical role in shaping market positioning, while strategic collaborations with hospitals and specialty clinics support wider adoption. Increasing emphasis on patient-centric care, early diagnosis, and integrated treatment approaches is intensifying competition, particularly in developed healthcare markets.

Key Market Developments

- In May 2022, Dr. Reddy’s Laboratories entered into an exclusive partnership with South Korea, based HK inno. N Corporation, under which HK inno. N assumed responsibility for the supply and commercialization of tegoprazan. The medication is approved for the treatment of gastrointestinal disorders in India and other emerging markets.

Companies Covered in Ineffective Esophageal Motility Treatment Market

• Johnson & Johnson

• Mylan Pharmaceutical

• MediGus Ltd

• Torax Medical

• Medtronic Plc

• AstraZeneca Plc

• Teva Pharmaceutical Industries Ltd

• Takeda Pharmaceutical Company Limited

• Glaxosmithkline Plc.

• Bayer Ag

• Pfixer Inc

• Bausch Health Companies Inc.

• Laborie

• Mederi Therapeutics, Inc.

• Becton, Dickinson and Company.

Frequently Asked Questions

The global ineffective esophageal motility treatment market is expected to be valued at US$ 4.6 billion in 2026.

Market growth is principally stimulated by enhanced diagnostic awareness through high-resolution manometry (HRM) technologies, rising prevalence of esophageal motility disorders among aging populations, and expanding availability of minimally invasive therapeutic procedures, including POEM and radiofrequency ablation.

North America maintains dominant market leadership with approximately 37% market share in 2025, supported by advanced healthcare infrastructure, elevated disease awareness, and favorable reimbursement frameworks.

Minimally invasive therapeutic procedures, including peroral endoscopic myotomy (POEM), radiofrequency ablation (RFA) systems, and advanced endoscopic platforms, represent principal market opportunity domains, supported by expanding clinical evidence validation, growing specialist clinician adoption, emerging treatment center establishment, substantial unmet need in treatment-resistant cases, and patient preference for less invasive therapeutic approaches with improved safety-efficacy profiles.

Major market participants include Johnson & Johnson, Medtronic Plc, AstraZeneca Plc, Takeda Pharmaceutical Company Limited, Glaxosmithkline Plc, Bayer AG, Pfizer Inc.