- Medical Devices

- Indwelling Catheters Market

Indwelling Catheters Market Size, Share, and Growth Forecast 2026 - 2033

Indwelling Catheters Market by Product (Indwelling Urinary Catheters, Indwelling Plural Catheters, Indwelling Peritoneal Catheters, Indwelling Nephrostomy Catheters, Peripheral Intravenous Catheters), by Material (Latex, PVC, Silicone, Tetrafluorethylene-Hexafluoropropylene, Others), by End User (Hospitals, Ambulatory Surgical Centers, Long-Term Care Centers, Home Care), by Regional Analysis, 2026-2033

Indwelling Catheters Market Size and Share Analysis

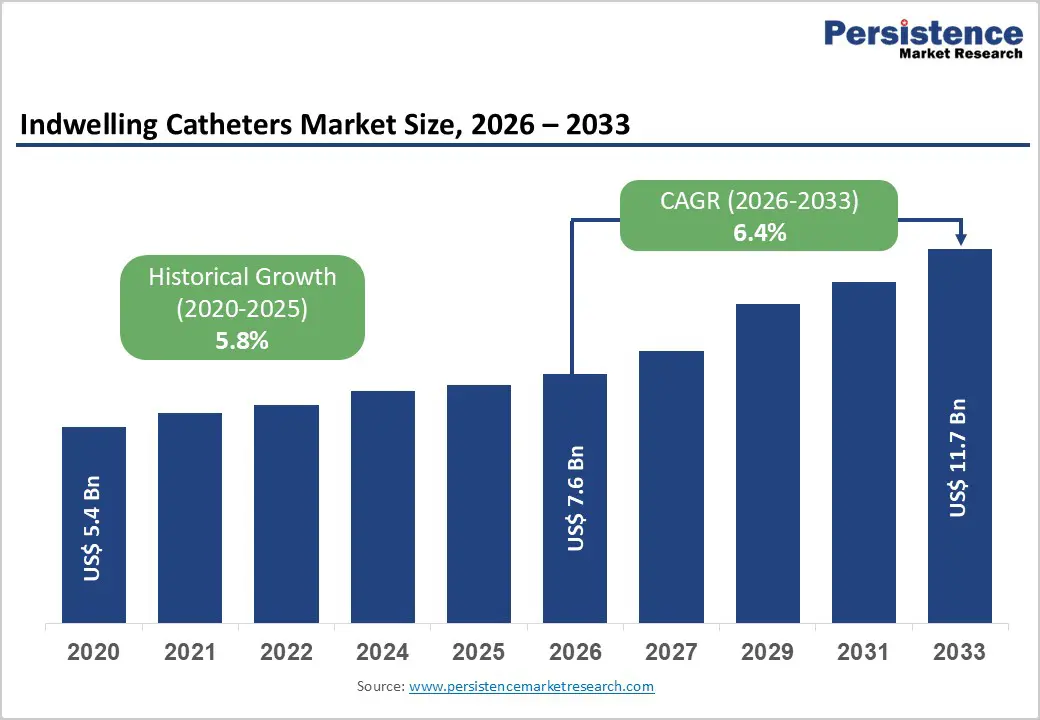

The global indwelling catheters market size is expected to be valued at US$ 7.6 billion in 2026 and projected to reach US$ 11.7 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

The market expansion is primarily driven by the escalating prevalence of chronic urological conditions, including urinary incontinence and urinary retention, which necessitate long-term catheterization solutions. The aging global population, coupled with increasing incidence of prostate cancer, spinal cord injuries, and neurological disorders such as multiple sclerosis, is generating sustained demand for indwelling catheter products across healthcare settings. Advanced technological innovations in antimicrobial coatings and biocompatible materials are addressing critical clinical concerns around catheter-associated urinary tract infections (CAUTIs), enhancing patient safety and driving product adoption rates worldwide. Government initiatives promoting minimally invasive procedures and favorable reimbursement policies further strengthen market dynamics.

Key Market Highlights

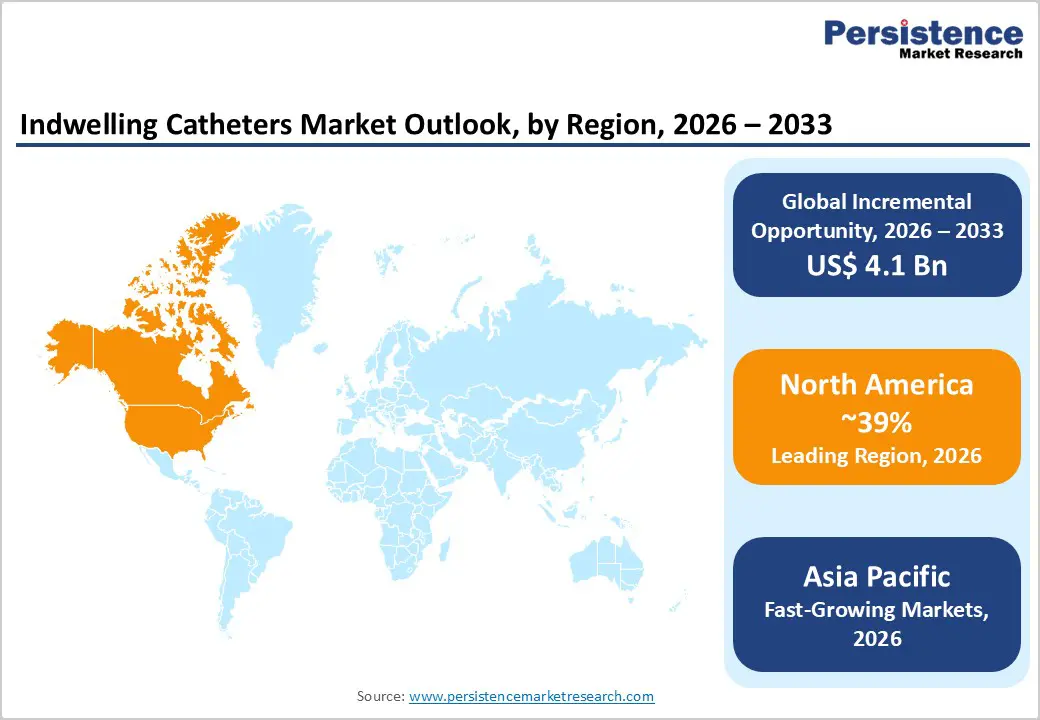

- North America Leadership: North America held ~39% of the global market in 2025, supported by advanced healthcare infrastructure, high surgical volumes, strong healthcare spending, and adoption of innovative antimicrobial and smart catheter technologies.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by healthcare expansion in China and India, rising surgical procedures, increasing urological disease burden, and government-led healthcare modernization.

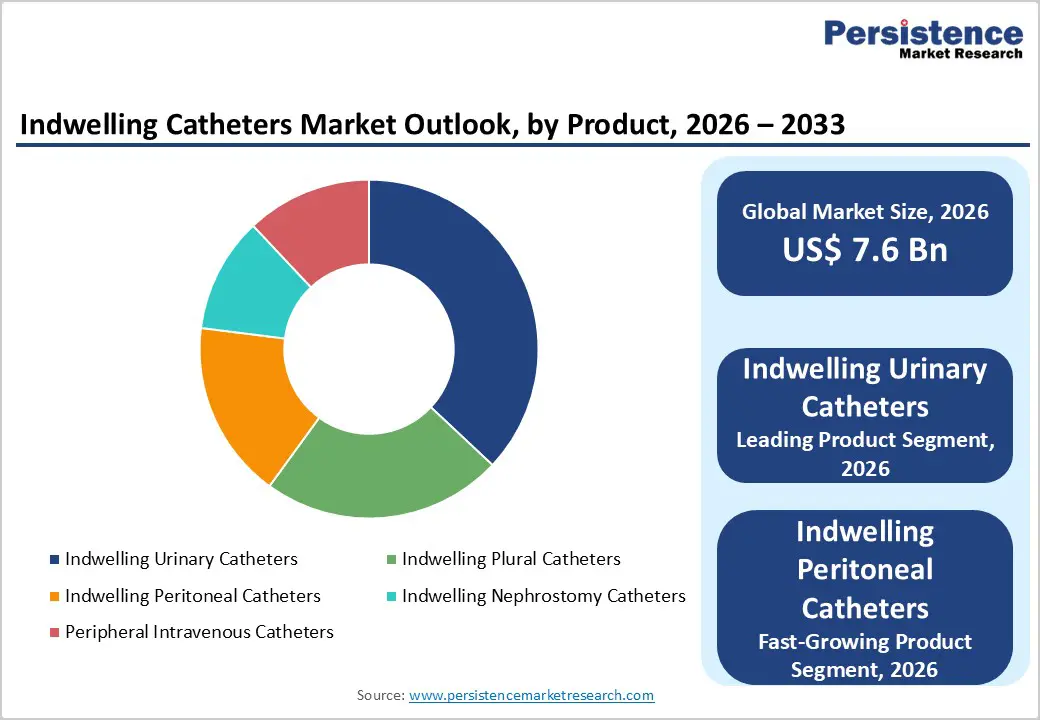

- Dominant Segment: Indwelling urinary catheters accounted for ~37% market share in 2025 due to extensive use in hospitals, surgical centers, and geriatric care.

- Fastest-Growing Segment: Indwelling peritoneal catheters are growing rapidly, supported by increasing peritoneal dialysis adoption in emerging markets.

- Key Opportunity: Advanced antimicrobial coatings and smart catheter technologies offer strong growth potential by significantly reducing catheter-associated infections and improving patient safety.

| Report Attribute | Details |

|---|---|

|

Indwelling Catheters Market Size (2026E) |

US$ 7.6 billion |

|

Market Value Forecast (2033F) |

US$ 11.7 billion |

|

Projected Growth CAGR (2026-2033) |

6.4% |

|

Historical Market Growth (2020-2025) |

5.8% |

Market Dynamics

Market Growth Drivers

Rising Prevalence of Chronic Urological Disorders

The global incidence of chronic urological diseases is experiencing significant growth, with urinary incontinence affecting over 30% of elderly populations in developed nations, according to healthcare epidemiological data. The Centers for Disease Control and Prevention (CDC) reports that approximately 15-25% of hospitalized patients require catheterization, with this proportion increasing substantially in geriatric and post-surgical populations. Conditions including benign prostatic hyperplasia, neurogenic bladder, and post-operative urinary retention create sustained demand for indwelling catheter solutions. The rising prevalence of diabetes and obesity—established risk factors for urinary dysfunction particularly in emerging economies, directly correlates with increased catheter utilization across hospitals, ambulatory surgical centers, and home care settings, driving market growth through expanded patient populations.

Technological Advancements in Antimicrobial Coatings

Next-generation catheter technologies featuring antimicrobial coatings and biocompatible materials have revolutionized infection prevention strategies, particularly addressing catheter-associated urinary tract infections (CAUTIs). Research published in 2024 demonstrates that silver alloy-coated catheters reduce CAUTI incidence by 69% compared to conventional catheters, while specialized BIP Foley catheters achieve infection reductions as high as 94% in controlled clinical settings. Bactiguard AB received European Medical Device Regulation (EU) 2017/745 approval in January 2023 for its innovative Latex BIP Foley Catheter featuring proprietary infection prevention coatings. These technological breakthroughs, combined with pH-responsive and bacteria-responsive coating technologies currently under development, significantly enhance patient comfort, reduce complications, and expand clinical applicability. Healthcare institutions increasingly prioritize advanced catheters for high-risk populations, driving market premiumization and overall revenue expansion.

Market Restraints

Risks Associated with Long-Term Catheterization

Extended indwelling catheterization carries substantial clinical risks that potentially limit market expansion despite technological improvements. The 3-7% daily risk of CAUTI acquisition during hospitalization creates liability concerns for healthcare providers and necessitates rigorous infection prevention protocols, increasing operational costs. Studies confirm that patients with catheterization duration exceeding 28 days develop bacteriuria almost universally, creating treatment burdens and elevated healthcare expenditures. Additionally, complications including urethral strictures, bladder tissue damage, and recurrent infections contribute to patient morbidity and reduce long-term catheter acceptance, particularly in home care settings where infection management becomes challenging. Regulatory bodies and hospital quality improvement initiatives increasingly incentivize catheter removal and alternative management strategies, which can suppress market growth by reducing catheterization rates in certain patient populations.

Reimbursement Constraints and Healthcare Cost Pressures

Healthcare systems across developed nations face mounting budget pressures, with reimbursement rates for catheter-related procedures remaining stagnant or declining in multiple jurisdictions. CAUTI-related complications impose significant financial burdens, with each infection adding USD 10,000-40,000 to patient care costs, creating institutional pressure to minimize catheter usage through alternative strategies and earlier device removal protocols. In developing economies, affordability constraints limit the adoption of advanced catheter technologies despite their superior clinical profiles, forcing manufacturers to maintain price-competitive conventional products with lower margins. Stringent reimbursement policies, particularly for indwelling peritoneal and nephrostomy catheters in certain regions, restrict patient access and reduce market penetration in potentially lucrative segments, thereby constraining overall market growth trajectories.

Market Opportunities

Expansion of Minimally Invasive Surgical Procedures and Peritoneal Dialysis Markets

The indwelling peritoneal catheters segment represents one of the fastest-growing opportunities within the broader market, driven by expanding peritoneal dialysis adoption in emerging economies where this treatment modality offers cost advantages compared to hemodialysis. The World Health Organization (WHO) emphasizes peritoneal dialysis as a viable renal replacement therapy particularly suited to resource-constrained settings, driving adoption across India, China, and Southeast Asian nations. India's dialysis market alone serves over 300,000 patients, with peritoneal dialysis penetration expected to increase substantially due to government healthcare initiatives and private sector expansion. Simultaneously, growth in minimally invasive surgical procedures including laparoscopic nephrectomy, urological interventions, and intra-abdominal procedures creates consistent demand for specialized peritoneal and nephrostomy catheters in operating rooms and post-operative recovery settings. Manufacturers can capitalize on this segment through targeted product development, strategic partnerships with dialysis centers, and geographic expansion into high-growth emerging markets.

Smart Catheter Technologies and Digital Health Integration

Emerging digital health ecosystems present substantial opportunities for manufacturers developing Bluetooth-enabled catheters, IoT-integrated monitoring systems, and smart tracking technologies that enable real-time catheter usage monitoring and urinary output assessment. These innovations address clinical concerns around infection detection, optimal catheter replacement timing, and patient compliance in home care settings. Teleflex Incorporated, a leading market player, invested USD 161.7 million in research and development during 2024, demonstrating commitment to next-generation catheter solutions, including smart monitoring systems. Similarly, Becton, Dickinson and Company announced exclusive global licensing agreements with Bactiguard to enhance its infection-prevention portfolio, signaling industry-wide recognition of technological innovation importance. Healthcare systems increasingly adopt digital monitoring platforms to optimize catheter care bundles and reduce CAUTI rates, creating addressable markets for smart catheter manufacturers. The integration of artificial intelligence-powered predictive analytics for infection risk assessment and personalized catheterization protocols represents a compelling growth avenue for market participants.

Category-wise Insights

Product Analysis

Indwelling Urinary Catheters: Dominance and Clinical Significance

Indwelling urinary catheters dominate the market with approximately 37% market share in 2025, driven by their widespread clinical utilization across diverse patient populations and healthcare settings. The 2-way indwelling urinary catheters segment constitutes the largest subcategory within this type, accounting for the majority of clinical placements due to their simplicity, cost-effectiveness, and suitability for routine urinary drainage in acute care hospitals. Clinical applications encompassing post-operative recovery, urinary retention management, and incontinence care in geriatric populations ensure sustained demand.

The regulatory landscape supports market dominance through established FDA approval pathways and standardized ISO 9001 manufacturing standards, enabling rapid market entry for compliant manufacturers. Government healthcare expenditure on catheterization procedures in developed nations, coupled with expanding surgical volumes in emerging economies, reinforces the dominance of indwelling urinary catheters within the overall market structure.

Material Analysis

Silicone Catheters Emerging as Preferred Material in Healthcare Settings

Silicone-based indwelling catheters represent the fastest-growing material segment, driven by superior biocompatibility, reduced inflammation response, and enhanced patient comfort compared to traditional latex alternatives. Clinical evidence demonstrates that silicone catheters reduce urethral irritation, decrease adverse tissue reactions, and maintain patency longer during extended catheterization periods exceeding 7-14 days. The inherent properties of silicone materials enable integration of advanced antimicrobial coatings and specialized surface modifications that improve infection prevention outcomes.

Coloplast, a major market participant, expanded its portfolio of silicone-based catheter systems including the Luja platform launched in May 2024, featuring women-specific designs and advanced material compositions. Growing awareness among healthcare providers regarding long-term catheterization complications drives purchasing decisions toward silicone alternatives, despite premium pricing compared to latex and PVC options. The material's proven performance in reducing CAUTI incidence by up to 50% compared to conventional materials positions silicone as the material of choice for quality-conscious healthcare institutions and patient-centric care providers.

Regional Insights

North America Indwelling Catheters Market Trends and Insights

North America dominates the global indwelling catheters market with 39% market share in 2025, driven by advanced healthcare infrastructure, elevated surgical volumes, and sophisticated reimbursement mechanisms supporting catheter adoption across diverse clinical settings. The United States market represents the largest regional contributor, underpinned by a high geriatric population prevalence, exceptional healthcare spending (approximately 17% of GDP), and widespread adoption of innovative medical technologies.

The FDA regulatory framework facilitates rapid market entry for novel catheter technologies, with manufacturers maintaining multiple approved products addressing diverse clinical indications, including urinary incontinence, neurogenic bladder, and post-operative retention.

Healthcare quality improvement initiatives focused on CAUTI reduction have catalyzed institutional investments in advanced catheter solutions and comprehensive infection prevention bundles. Organizations, including the Centers for Disease Control and Prevention (CDC) and The Leapfrog Group, promote evidence-based catheterization guidelines, driving procurement of antimicrobial-coated and technologically advanced catheters. Additionally, established reimbursement pathways through Medicare, Medicaid, and private insurance ensure robust market demand.

The region's mature healthcare system and strong presence of leading catheter manufacturers, including Teleflex, Cardinal Health, Becton Dickinson, and Coloplast, sustains competitive market dynamics and continuous product innovation.

Asia Pacific Indwelling Catheters Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, driven by expanding healthcare infrastructure, rising surgical volumes, and increasing prevalence of chronic urological diseases across China, India, Japan, and Southeast Asian nations. The region's rapidly growing elderly population, coupled with urbanization-driven lifestyle changes increasing diabetes and obesity prevalence, generates substantial catheterization demand. China commands significant regional market share through government-supported healthcare reforms, expanding hospital infrastructure and surgical capacity, with centralized procurement systems creating volume opportunities for manufacturers.

India's emerging status reflects expanding dialysis programs and surgical infrastructure development, with peritoneal dialysis penetration expected to increase substantially over the coming years. The Japanese market demonstrates advanced adoption of premium catheter technologies, reflecting high healthcare expenditure and quality-centric procurement practices. Manufacturing advantages in the Asia Pacific, including lower production costs enabling competitive pricing, attract significant market player investments, with Teleflex, Coloplast, and other major manufacturers establishing regional manufacturing facilities.

Additionally, government initiatives, including India's National Health Mission and China's healthcare modernization programs, provide supportive policy environments promoting catheter market expansion. The region's growth trajectory reflects favorable demographic trends, improving healthcare access, and expanding medical tourism, supporting catheterization procedure volumes across urban centers.

Competitive Landscape

The indwelling catheters market is highly competitive and characterized by the presence of global medical device manufacturers alongside specialized catheter technology developers. Competition focuses on product reliability, patient comfort, infection prevention, and ease of insertion and maintenance. Market participants invest heavily in antimicrobial coatings, biocompatible materials, and safety-enhancing designs to reduce catheter-associated complications. Regulatory compliance, strong distribution networks, and long-term supply contracts with hospitals and dialysis centers are key competitive factors.

Key Market Developments

- In July 2024, Mexple launched UroMen and UroWomen urine collection kits for males and females in the incontinence category. With the increasing demand for home medical products that combine functionality and comfort, Mexple’s UroMen and UroWomen were designed to address the diverse needs of patients requiring urine collection solutions, ensuring an optimal user experience.

Companies Covered in Indwelling Catheters Market

- Teleflex Incorporated

- Cardinal Health

- B. Braun Melsungen AG

- Coloplast

- Medtronic

- ConvaTec, Inc

- Sterimed Group

- Becton, Dickinson and Company

- McKesson Medical

- Poiesis Medical

- COOK Medical

- Smiths Medical

- Rocket Medical plc

Frequently Asked Questions

The global indwelling catheters market is anticipated to reach US$ 7.6 billion in 2026.

The primary market growth drivers include escalating prevalence of urinary incontinence and urinary retention affecting over 30% of elderly populations, increasing prostate cancer incidence, expanding surgical procedure volumes, and technological advancements in antimicrobial coatings reducing catheter-associated urinary tract infection rates by 69-94%.

North America maintains the dominant regional position with 39% global market share in 2025, driven by advanced healthcare infrastructure, high surgical volumes, sophisticated reimbursement mechanisms, strong presence of major manufacturers, and institutional quality improvement initiatives focused on CAUTI prevention.

The most compelling market opportunity exists in developing advanced antimicrobial coatings, smart monitoring technologies, and geographic expansion into Asia Pacific markets. Indwelling peritoneal catheters represent the fastest-growing segment driven by expanding peritoneal dialysis adoption across emerging economies. Additionally, digital health integration, IoT-enabled catheter monitoring systems, and artificial intelligence-powered infection prediction capabilities present substantial growth avenues for innovative manufacturers.

Leading market players include Teleflex Incorporated, Cardinal Health, B. Braun Melsungen AG, Coloplast, Medtronic, etc.