- Medical Devices

- Immunodiagnostics Market

Immunodiagnostics Market Size, Share, and Growth Forecast, 2026 - 2033

Immunodiagnostics Market by Product (Instruments, Reagents & Consumables), Technology (Enzyme-linked Immunosorbent Assay, Others), Application (Oncology & Endocrinology, Others), End-user (Clinical Laboratories, Others), and Regional Analysis for 2026 - 2033

Immunodiagnostics Market Size and Trends Analysis

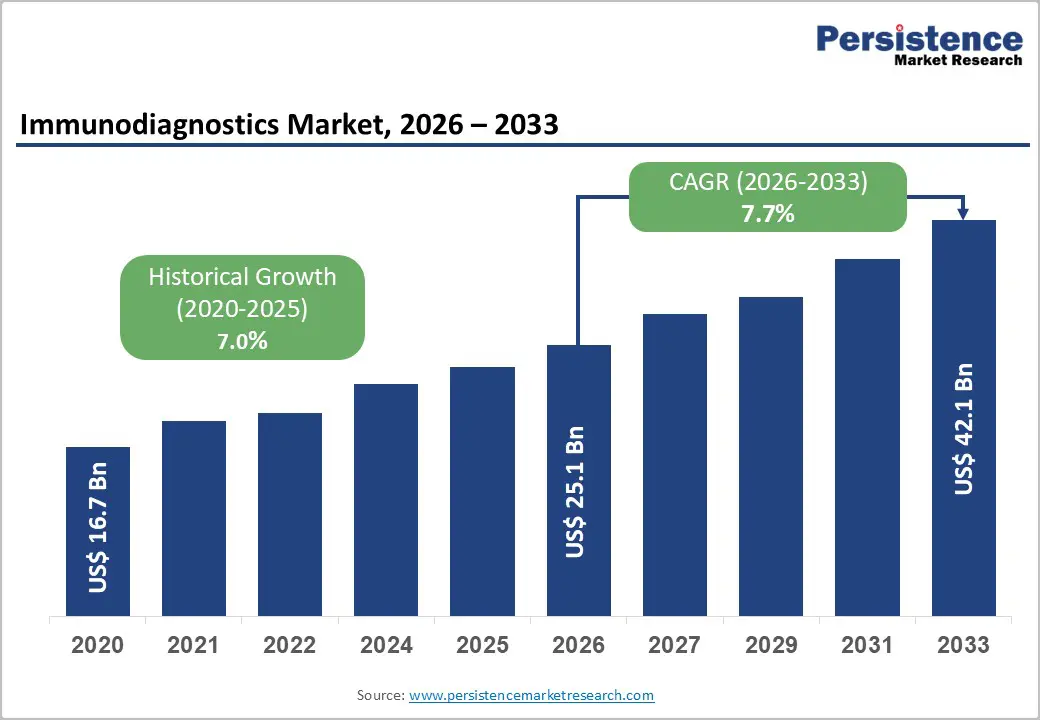

The global immunodiagnostics market size is projected to be valued at US$ 25.1 billion in 2026 and is expected to reach US$ 42.1 billion by 2033, growing at a CAGR of 7.7% during the forecast period from 2026 to 2033, driven by a convergence of factors: the rising global burden of chronic and infectious diseases, rapid expansion of clinical laboratory infrastructure in emerging markets, growing adoption of fully automated immunoanalyzers in hospital and reference laboratory settings, increasing integration of point-of-care immunodiagnostic platforms in decentralized care environments, and sustained pharmaceutical and biotechnology pipeline activity generating novel immunodiagnostic companion testing requirements.

Key Industry Highlights:

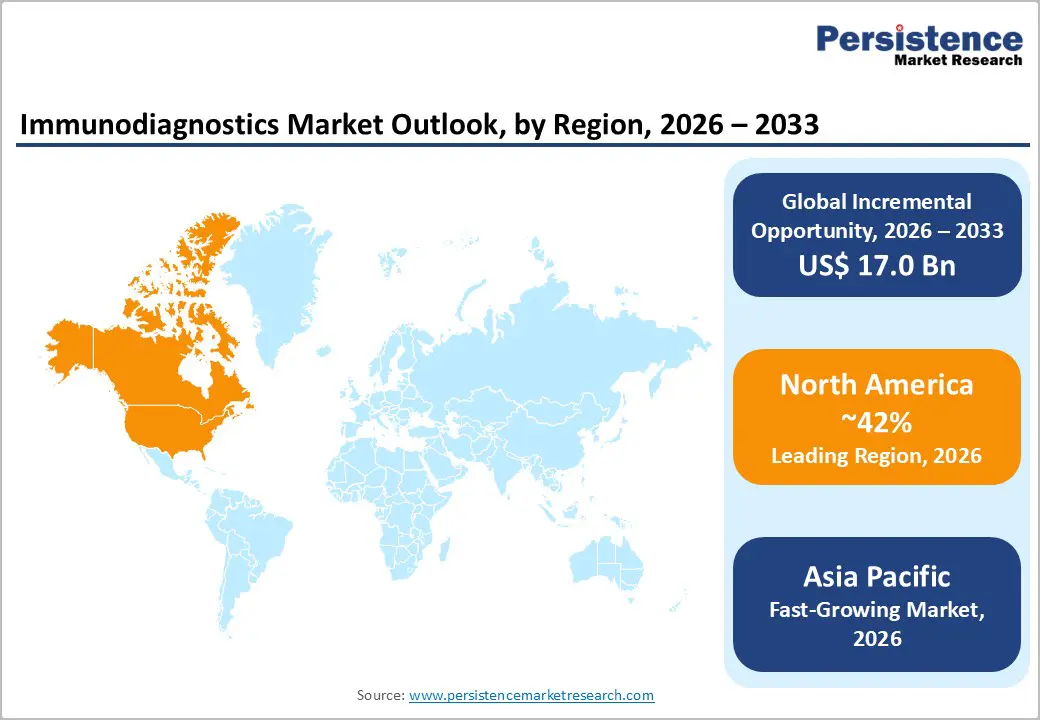

- Dominant Region: North America is expected to dominate, holding approximately 42% revenue share in 2026, supported by advanced clinical laboratory infrastructure, comprehensive reimbursement frameworks, and the concentrated presence of leading immunodiagnostics manufacturers and reference laboratory networks.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing immunodiagnostics market, driven by expanding laboratory infrastructure investments in China and India, rising chronic disease burden, and growing government health spending across the region.

- Leading Product Type: Reagents & consumables are expected to dominate, capturing approximately 65% of market revenue in 2026, reflecting the high-volume, recurring-purchase nature of immunoassay reagent consumption across clinical laboratories and hospital testing facilities.

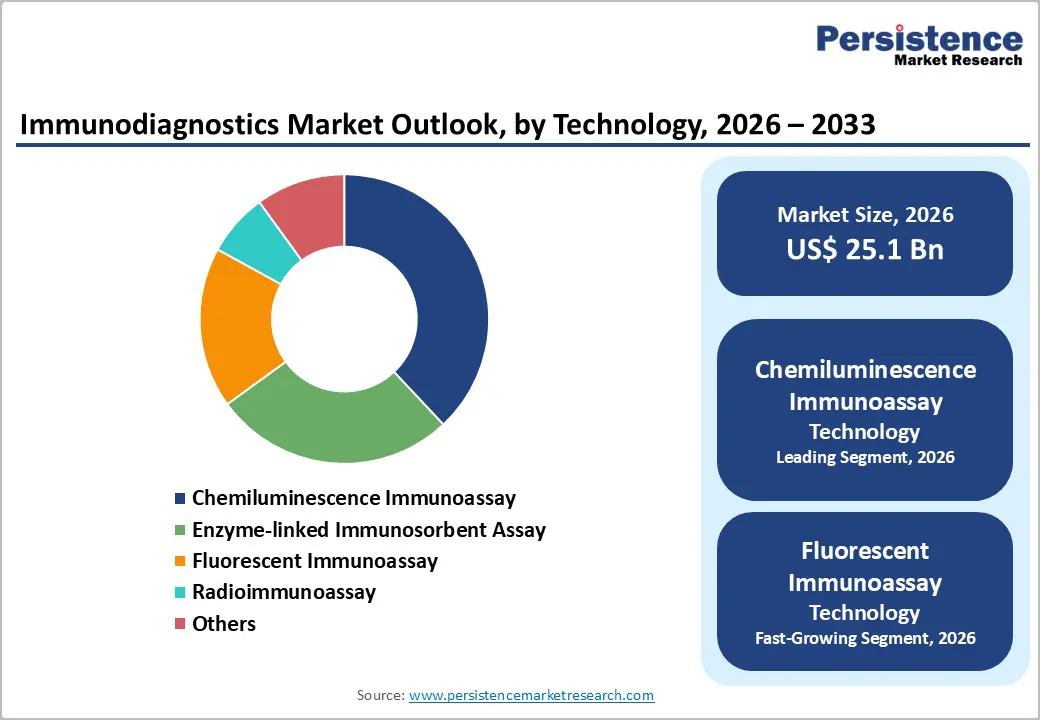

- Dominant Technology: Chemiluminescence immunoassay (CLIA) technology is the leading segment with approximately 38% share in 2026, owing to its superior analytical sensitivity, broad assay menu applicability, and full automation compatibility on high-throughput immunoanalyzers.

DRO Analysis

Driver - Technological Advancement in Automated Immunoanalyzers and Chemiluminescence Platforms

Continuous technological innovation in immunodiagnostic instrumentation, particularly the evolution of fully automated, high-throughput chemiluminescence immunoanalyzer platforms, is driving both market expansion and competitive differentiation. Modern immunoanalyzers from market leaders Abbott (Alinity i), Roche (cobas e 8000), and Beckman Coulter (DxI 9000) deliver testing throughputs exceeding 1,000-2,000 tests per hour, with random-access multi-analyte capability, integrated quality control automation, and bidirectional laboratory information system (LIS) connectivity.

The U.S. FDA's 510(k) clearance pathway and the European Union's In Vitro Diagnostic Regulation (IVDR, EU 2017/746), which took effect in May 2022, are reshaping immunodiagnostic product development timelines and clinical evidence requirements, particularly for higher-risk Class C and D immunoassays. While IVDR compliance creates near-term regulatory burden, it simultaneously establishes higher performance standards that favor established platforms with robust clinical validation data, reinforcing competitive moats for leading immunodiagnostics manufacturers.

Restraint - Stringent Regulatory Requirements and Extended Product Development Timelines

The immunodiagnostics market faces substantial regulatory complexity as a defining operational constraint. In the European Union, the transition from the legacy In Vitro Diagnostic Directive (IVDD, 98/79/EC) to the IVDR (EU 2017/746) has imposed significantly enhanced clinical evidence requirements, performance evaluation documentation, and notified body review obligations, particularly for the higher-risk immunoassay categories encompassing cancer biomarkers, infectious disease serology, and cardiac marker panels.

In the U.S., the FDA's evolving oversight of laboratory-developed tests (LDTs), which includes many advanced immunoassay applications deployed by reference laboratories, introduces regulatory uncertainty for clinical laboratory operators and immunoassay developers. The FDA issued a final rule in May 2024, phasing out the general enforcement discretion policy for LDTs, which will require laboratory-developed immunoassays to comply with standard medical device regulatory requirements over a multi-year transition timeline.

Opportunity - Precision Oncology and Companion Immunodiagnostics Driving High-Value Testing Growth

The precision oncology revolution, built on molecularly targeted therapies and immune checkpoint inhibitor treatment regimens, is creating substantial new demand for specialized immunodiagnostic companion testing. The U.S. FDA has approved over 50 companion diagnostic tests to date, a significant proportion of which are immunoassay-based platforms measuring protein biomarker expression (PD-L1, HER2, ER/PR) in tumor tissue or liquid biopsy specimens.

Liquid biopsy immunoassays measuring circulating tumor markers, cell-free DNA methylation signatures, and tumor-associated autoantibody panels in blood specimens represent a particularly high-growth opportunity, enabling minimally invasive cancer monitoring without repeat tissue biopsy procedures. Companies including Thermo Fisher Scientific, Roche, and DiaSorin are actively investing in next-generation immunodiagnostic oncology panels that integrate tumor marker quantification with immune response profiling.

Category-wise Analysis

Product Type Insights

Reagents & consumables are anticipated to dominate the segment, accounting for approximately 65% of total market revenue in 2026. This dominant share reflects the fundamental economics of the immunodiagnostics business model: each installed immunoanalyzer instrument generates an ongoing, high-volume stream of reagent kit, calibrator, and quality control consumable purchases that typically deliver 3-5× the lifetime revenue value of the initial instrument capital sale. Roche Diagnostics generates substantial recurring revenue through its cobas® immunodiagnostic analyzer portfolio, where hospitals and laboratories continuously purchase proprietary reagent kits, calibrators, controls, and consumables required for every diagnostic test run.

Instruments represent the fastest-growing product segment. This growth is propelled by the ongoing wave of clinical laboratory automation investments globally, particularly in Asia Pacific, Latin America, and the Middle East, as healthcare infrastructure modernization programs drive the replacement of legacy semi-automated immunoassay platforms with next-generation fully automated, high-throughput immunoanalyzers. Abbott Laboratories, which launched its GLP systems Track automation solution in India to help laboratories manage rising high-volume testing demand.

Technology Insights

Chemiluminescence Immunoassay (CLIA) is estimated to dominate with over 38% market share in 2026, propelled by its high sensitivity, accuracy, and fast test processing, making it ideal for large-scale clinical testing. The technology supports full automation, allowing hospitals and laboratories to handle high sample volumes efficiently with minimal manual intervention. Siemens Healthineers offers ADVIA Centaur® XP/XPT CLIA systems that deliver high sensitivity, rapid results, and fully automated high-throughput testing, enabling hospitals and laboratories to efficiently process large volumes of infectious disease, cardiac, and hormone tests.

Fluorescent Immunoassay (FIA) represents the fastest-growing segment, due to rising demand for rapid, sensitive, and point-of-care diagnostic testing. FIA provides quick and accurate results, making it suitable for infectious disease detection, chronic disease monitoring, and emergency testing. Increasing adoption in clinics, diagnostic centers, and decentralized healthcare settings is accelerating market growth. Anbio Biotechnology offers the AF-100S Fluorescent Immunoassay (FIA) analyzer, a rapid point-of-care diagnostic system that provides fast and highly sensitive testing for infectious diseases, cardiac markers, and hormones across clinics and decentralized healthcare settings.

Application Insights

Oncology & endocrinology represents the dominant application segment of the immunodiagnostics market, accounting for approximately 30%-33% of global market revenue in 2026. This segment's leadership reflects both the clinical primacy of immunoassay-based biomarker testing in cancer and hormone disorder management and the premium pricing commanded by high-sensitivity, high-specificity tumor marker and hormone quantification assays. Roche Diagnostics offers the Elecsys® immunoassay portfolio for oncology and endocrinology testing, including high-sensitivity tumor marker assays such as PSA and CA 125, along with hormone assays like TSH and insulin for accurate cancer and endocrine disorder diagnosis.

Infectious diseases are likely to be the fastest-growing application segment. The COVID-19 pandemic fundamentally elevated infectious disease immunodiagnostic testing infrastructure globally, creating installed base expansions, workflow standardizations, and healthcare system awareness of immunoassay-based serology testing that continue to generate sustained demand for infectious disease immunodiagnostic platforms beyond SARS-CoV-2. Roche Diagnostics and its Elecsys® Anti-SARS-CoV-2 immunoassay platform, which saw widespread global adoption during the COVID-19 pandemic for high-throughput infectious disease serology testing.

End-user Insights

Clinical laboratories are expected to dominate with over 45% of revenues in 2026, due to their high testing volumes and advanced automated testing systems. Major laboratory networks such as Quest Diagnostics, Labcorp, Sonic Healthcare, and Synlab play a key role by providing fast and large-scale immunoassay testing services. Quest Diagnostics, one of the world’s largest clinical laboratory networks, operates high-throughput automated immunoassay testing systems for infectious diseases, oncology, endocrinology, and cardiovascular diagnostics.

Hospitals represent the fastest-growing end-user segment. The trend toward hospital laboratory insourcing of immunodiagnostic testing, driven by the need for faster turnaround times for acute care decision-making, reduced reference laboratory logistics dependency, and cost center management optimization, is driving significant immunoanalyzer capital investment across hospital laboratory settings globally. Siemens Healthineers and its Atellica® Solution immunoanalyzer platform, which has been adopted by hospitals to improve in-house immunodiagnostic testing efficiency and reduce turnaround times.

Regional Insights

North America Immunodiagnostics Market Trends

North America market is projected to dominate, capturing around 42% of the total revenue in 2026, propelled by its advanced healthcare and laboratory infrastructure. The U.S. accounts for the majority of regional demand, supported by a strong network of reference laboratories, hospitals, and physician labs using automated immunodiagnostic systems. In addition, favorable healthcare reimbursement policies and high adoption of diagnostic testing continue to drive market growth across the region.

U.S Immunodiagnostics Market Insights

The U.S. immunodiagnostics market is fueled by the National Cancer Institute's cancer screening program investments, generating large-scale tumor marker immunoassay test volumes and the American Heart Association's cardiovascular risk biomarker monitoring guidelines, which sustain cardiac marker immunoassay demand across emergency medicine, cardiology, and primary care settings.

Canada Immunodiagnostics Market Insights

The Canada market is supported by provincially administered public health laboratory networks and hospital laboratory systems that deploy immunoanalyzer platforms for routine and specialized immunoassay testing. Health Canada's Medical Devices Regulations (SOR/98-282) govern the immunodiagnostic device market clearance, with provincial health technology assessment bodies influencing clinical adoption of novel immunoassay platforms.

Europe Immunodiagnostics Market Trends

Europe's market growth is powered by universal healthcare systems, comprehensive cancer screening programs, and mature clinical laboratory networks across Western Europe. The EU IVDR framework, with its enhanced clinical evidence requirements for Class C and D immunoassays, is reshaping the European immunodiagnostics competitive landscape, creating compliance-driven consolidation among smaller manufacturers while reinforcing the market positions of IVDR-compliant platform leaders, including Roche, Abbott, and bioMérieux.

Germany Immunodiagnostics Market Trends

Germany is the leading European market, fueled by its advanced hospital laboratory infrastructure, robust statutory health insurance (GKV) reimbursement system covering immunodiagnostic testing, and the presence of leading immunodiagnostics manufacturers, including Roche Diagnostics GmbH (headquartered in Basel with major German operations) and QIAGEN (headquartered in Hilden, Germany).

U.K. Immunodiagnostics Market Trends

The U.K. National Health Service (NHS) represents a major structured demand channel for immunodiagnostics, with NHS England's cancer diagnostic improvement programs including the National Optimal Lung Cancer Pathway and BreastScreen program, generating systematic immunoassay testing demand through NHS pathology networks.

Asia Pacific Immunodiagnostics Market Trends

Asia Pacific is likely to be the fastest-growing regional market, driven by rapidly expanding hospital and clinical laboratory infrastructure, rising chronic disease burden, increasing government healthcare expenditure, and growing awareness of immunoassay-based diagnostic testing among healthcare professionals and patients.

China Immunodiagnostics Market Trends

China represents the dominant Asia Pacific immunodiagnostics market. China's 14th Five-Year Plan (2021-2025) allocates significant healthcare infrastructure investment to hospital laboratory modernization and national disease surveillance capability enhancement, directly driving immunoanalyzer platform procurement across tertiary hospitals and regional reference laboratory networks.

India Immunodiagnostics Market Trends

India is one of the highest-growth immunodiagnostics markets in Asia Pacific. The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PM-JAY) health insurance program, covering approximately 500 million beneficiaries, is expanding access to clinical laboratory diagnostics across India's underserved rural and semi-urban populations, generating new institutional demand for immunoassay-based testing.

Competitive Landscape

The global immunodiagnostics market is moderately consolidated, with Abbott, Hoffmann-La Roche AG, Danaher Corporation (Beckman Coulter), bioMérieux, DiaSorin, QIAGEN, Thermo Fisher Scientific, and Quest Diagnostics collectively defining competitive dynamics through platform innovation, assay menu breadth, global distribution strength, and strategic acquisitions.

Abbott and Roche maintain co-leadership positions across the high-volume automated immunoanalyzer segment, Abbott through its Alinity i and ARCHITECT immunoassay system platforms, and Roche through its cobas e immunoassay analyzer family, each commanding global immunoanalyzer installed bases of tens of thousands of instruments across clinical laboratory and hospital settings worldwide.

DiaSorin has differentiated through a specialty immunodiagnostic focus, particularly in vitamin D, infectious disease serology, and transplantation monitoring, serving market segments where clinical specialty depth creates competitive advantages that broad-menu generalist platform providers struggle to match. QIAGEN maintains competitive strength in molecular-immunoassay hybrid platforms and sample preparation technologies that complement immunodiagnostic workflows.

Key Industry Developments:

- In May 2026, Revvity, through its subsidiary Immunodiagnostic Systems (IDS), received clearance from the U.S. Food and Drug Administration (FDA) for its Total Testosterone automated chemiluminescence immunoassay (ChLIA). The company expanded its portfolio of FDA-cleared ChLIA assays, which already included tests for free testosterone and sex hormone-binding globulin (SHBG), to offer the industry’s first comprehensive solution for diagnosing testosterone-related disorders on a single platform.

- In March 2026, Thermo Fisher Scientific opened a new $18 million distribution and labeling center in Uppsala, Sweden, to strengthen its global immunodiagnostics supply chain for allergy and autoimmune disease testing. The facility enhanced logistics efficiency and supported the growing global demand for diagnostic solutions.

Companies Covered in Immunodiagnostics Market

- Abbott

- Hoffmann-La Roche AG

- DiaSorin

- Danaher Corporation

- QIAGEN

- bioMérieux

- Thermo Fisher Scientific

- Quest Diagnostics

Frequently Asked Questions

The global immunodiagnostics market is projected to reach US$25.1 billion in 2026.

Technological advancement in fully automated chemiluminescence immunoanalyzer platforms and the expansion of point-of-care immunodiagnostic testing in both developed and emerging market healthcare settings further accelerate market growth.

The immunodiagnostics market is poised to witness a CAGR of 7.7% from 2026 to 2033.

Major growth opportunities in the immunodiagnostics market include the expansion of point-of-care testing in emerging healthcare markets and the rising demand for companion diagnostics in precision oncology.

Key players include Abbott, Hoffmann-La Roche AG, DiaSorin, Danaher Corporation (Beckman Coulter), QIAGEN, bioMérieux, Thermo Fisher Scientific, and Quest Diagnostics.