- Hardware & Software IT Services

- Identity Analytics Market

Identity Analytics Market Size, Share, and Growth Forecast, 2026 - 2033

Identity Analytics Market by Component Type (Solution, Services), Deployment Mode (On-Premises, Cloud-Based), Application (Customer Management, Governance, Risk & Compliance (GRC) Management, Fraud Detection, Identity & Access Management (IAM), Misc.), End User (BFSI (Banking, Financial Services & Insurance), Government & Defense, Healthcare & Life Sciences, Telecom & IT, Misc.) and Regional Analysis for 2026 - 2033

Identity Analytics Market Size and Trends Analysis

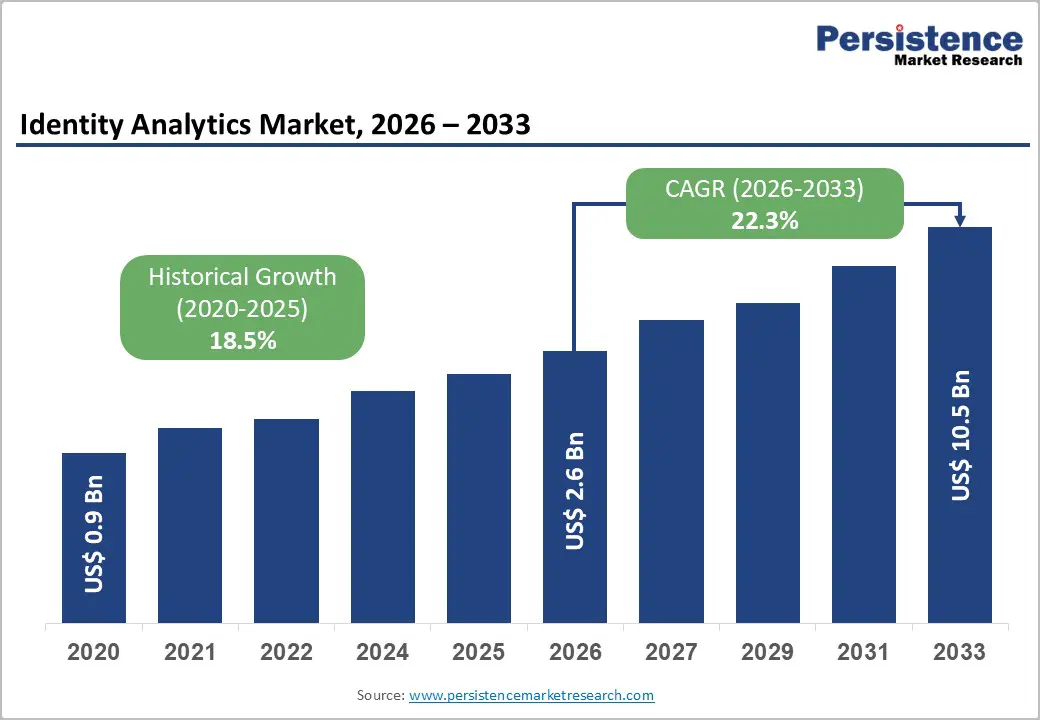

The Global Identity Analytics Market size was valued at US$ 2.6 billion in 2026 and is projected to reach US$ 10.5 billion by 2033, growing at a CAGR of 22.3% between 2026 and 2033. This substantial expansion reflects the urgent need for advanced identity governance solutions as organisations face unprecedented security challenges.

The market experienced a historical CAGR of 18.5% from 2020 to 2026, demonstrating consistent momentum driven by escalating cyber threats and regulatory pressures. The acceleration in growth rate to 22.3% post-2026 underscores the critical role identity analytics play in modern cybersecurity frameworks, particularly as enterprises adopt zero-trust architectures and cloud-based infrastructures that demand continuous identity verification and risk-based access management.

Key Industry Highlights:

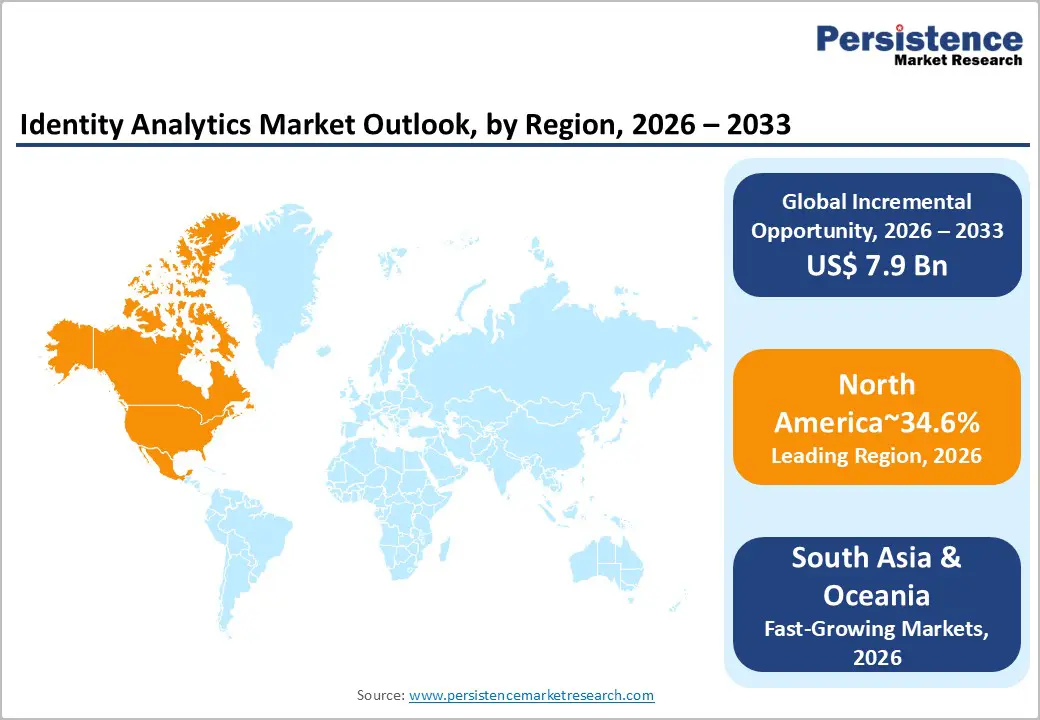

- Regional Leadership: North America leads the global Identity Analytics Market with 34.6% share, supported by advanced Zero Trust adoption, strong cybersecurity investments, and federal identity modernisation initiatives.

- Strong European Presence: Europe holds 22% share, driven by GDPR-driven compliance mandates, mature financial services adoption, and enterprise IAM integration across regulated industries.

- High-Growth East Asia Market: East Asia accounts for 20% share and remains one of the fastest-growing regions, powered by large-scale digital banking, fintech expansion, and accelerated Zero Trust implementation across Japan, China, and Singapore.

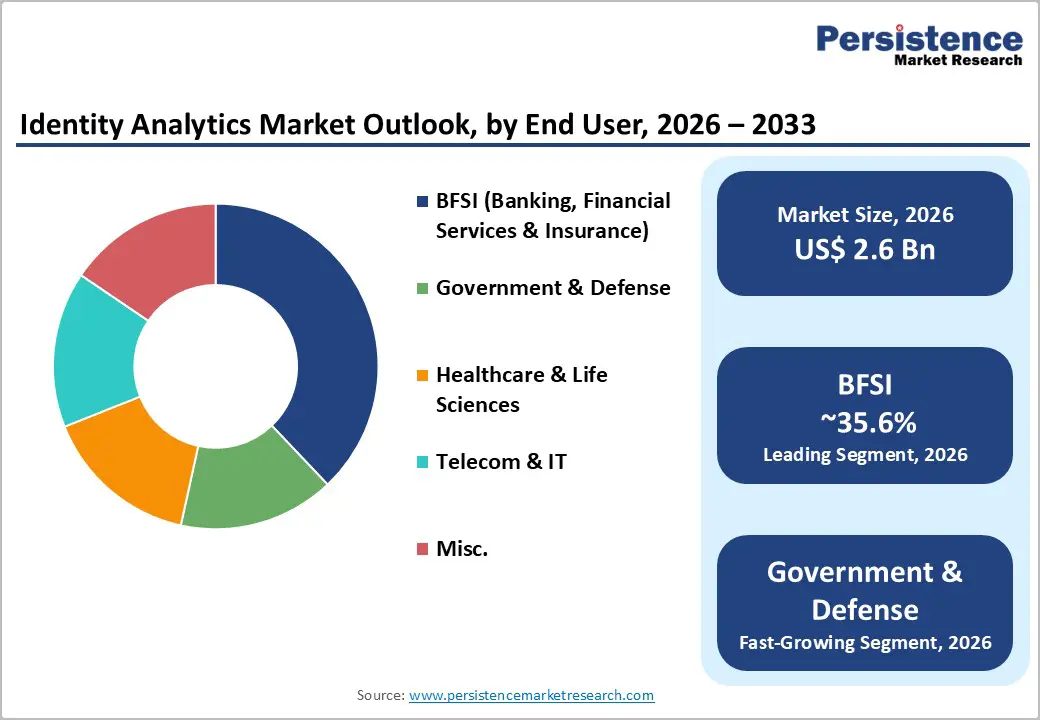

- Leading End-User Segment: The BFSI sector dominates with 35.6% share, reflecting stringent compliance, privileged access requirements, and high exposure to identity-based fraud and data breaches.

- Fastest-Growing End-User Sector: Government & Defence emerges as the fastest-growing segment, driven by Zero Trust mandates, defence digitalisation, and insider threat monitoring requirements.

- Leading Solution Type: Software platforms command 71.2% share, leveraging AI/ML-based behavioural analytics, risk scoring, and automated identity governance capabilities for enterprise environments.

| Key Insights | Details |

|---|---|

|

Identity Analytics Market Size (2026E) |

US$ 2.6 Bn |

|

Market Value Forecast (2033F) |

US$ 10.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

22.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

18.5% |

Market Dynamics

Growth Drivers

Escalation of Identity-Based Cyber Threats and Data Compromises

Identity-based attacks have become the primary vector for enterprise security breaches, fundamentally transforming how organisations approach access management. The Identity Analytics Market benefits directly from this threat landscape evolution, as traditional perimeter-based security models prove inadequate against sophisticated credential theft and insider threats.

According to the Identity Theft Resource Centre, 2024 recorded 3,158 data compromises in the United States, with over 1.35 billion victim notices issued, marking the second-highest number of data events since tracking began in 2005. The FBI's Internet Crime Report 2024 documented 859,532 cybercrime complaints with potential losses reaching $16.6 billion, up from $12.5 billion in 2023. Critically, stolen credentials emerged as the leading attack vector for cyberattacks against publicly traded companies in 2024, responsible for four of the five mega-breaches that year. Better cyber practices, including multi-factor authentication, could have prevented at least 196 compromises and more than 860 million victim notices. These statistics underscore the imperative for identity analytics solutions that can detect anomalous access patterns, identify high-risk user behaviours, and provide continuous monitoring capabilities that prevent credential-based attacks from succeeding.

Accelerated Adoption of Zero Trust Architecture Frameworks

The widespread implementation of Zero Trust Architecture represents a fundamental shift in cybersecurity strategy that directly propels the Identity Analytics Market expansion. Zero Trust operates on the principle of "never trust, always verify," requiring continuous authentication and authorisation of every access request regardless of network location.

By 2025, 60 percent of U.S. federal agencies aimed to meet Zero Trust mandates following the OMB Memorandum M-22-09, which established specific cybersecurity standards requiring agencies to enhance identity verification and implement multi-factor authentication by the end of FY 2024. The Asia Pacific region has emerged as a zero-trust pioneer, with over two-thirds of enterprises running formal ZTA programs, incentivised by government policies in Singapore, Australia, and Japan.

Identity analytics solutions serve as the foundational intelligence layer for zero trust implementations, providing risk scoring, behavioural analytics, and continuous identity verification capabilities that enable organisations to enforce least-privilege access and detect potential compromises in real-time. Theorganisations transition from VPN-based perimeter security, with 65 percent planning to replace VPN services within the year to zero trust models, the demand for sophisticated identity analytics that can handle dynamic policy enforcement and context-aware authentication intensifies significantly.

Regulatory Mandates and Compliance Requirements for Identity Governance

Stringent data protection regulations and industry-specific compliance frameworks are compelling organisations to implement comprehensive identity analytics capabilities. The European Union's General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) impose significant penalties for inadequate identity management and data protection measures. By 2024, 40 percent of U.S. states had enacted comprehensive privacy laws to better protect consumers, creating a complex regulatory landscape that requires robust identity governance and audit capabilities. The financial services sector faces particularly rigorous requirements, with regulatory bodies mandating detailed access certifications and privileged account monitoring.

The Identity Analytics Market directly addresses these compliance needs by automating access reviews, providing detailed audit trails of user activity, and enabling organisations to demonstrate adherence to regulatory standards through data-driven reporting. Identity analytics platforms leverage machine learning to continuously assess access risks, identify orphan and dormant accounts, and flag excessive privileges that violate least-privilege principles capabilities that are essential for meeting regulatory requirements while maintaining operational efficiency and reducing the manual burden of compliance activities on security teams.

Market Restraining Factors

Complex Integration with Legacy Infrastructure Systems

Organisations face significant technical challenges when implementing identity analytics solutions within heterogeneous IT environments containing legacy systems, on-premises applications, and diverse cloud platforms. Many enterprises operate identity and access management systems built on outdated technologies that lack modern API capabilities, making it difficult to extract and normalise identity data for analytics processing.

The complexity increases exponentially in large organisations with multiple identity repositories, decentralised access management, and inconsistent role definitions across business units. This integration burden requires substantial technical expertise, extended implementation timelines, and often necessitates middleware solutions that add cost and maintenance overhead. Organisations must address data quality issues, establish governance frameworks for identity data management, and reconcile conflicting access policies, all while maintaining business continuity and avoiding disruption to existing authentication workflows.

Key Market Opportunities

Expansion in Banking, Financial Services, and Insurance Sectors

The BFSI sector presents exceptional potential for Identity Analytics Market penetration given the industry's digital transformation trajectory and heightened security requirements. India's banking, financial services, and insurance sector demonstrated remarkable expansion, with market capitalisation growing 50-fold to reach Rs. 91,00,000 crore (US$ 1 trillion) in 2025 from US$ 20.28 billion in 2005, now contributing 27 percent to India's GDP compared to 6 percent previously. This growth, driven by financialization of savings, credit expansion, and improved balance sheets, has seen gross NPAs fall from 5.8 percent in FY22 to 2.2 percent in FY25. Non-Banking Financial Companies (NBFCs) have emerged as significant credit engines with 15 percent CAGR in net worth and a 31.7 percent CAGR in profit after tax, while life insurance assets under management reached US$ 693 billion and mutual fund AUM rose to Rs. US$ 844 billion by March 2025.

In Europe, the financial and insurance activities sector generated €0.9 trillion in value added across nearly 867,000 enterprises in 2022, while China's banking sector reached RMB 467.3 trillion in total assets with 7.9 percent year-on-year growth as of Q2 2025, maintaining strong asset quality with an NPL ratio of 1.49 percent. These institutions handle massive volumes of customer identities, privileged accounts for trading and transaction systems, and sensitive financial data that require continuous monitoring and advanced analytics to detect fraud, prevent insider threats, and ensure regulatory compliance.

The shift to digital banking platforms, mobile payment systems like Brazil's PIX, and open banking APIs creates complex identity ecosystems where traditional access controls prove insufficient, opening substantial opportunities for identity analytics solutions that can provide real-time risk assessment across digital channels.

Government and Defence Sector Modernisation Initiatives

Government agencies and defence organisations represent high-growth segments for the Identity Analytics Market as they undertake digital modernisation while facing sophisticated nation-state threats. The European aerospace and defence industry achieved a turnover of €183.4 billion in 2024, reflecting a 13.8 percent year-on-year increase, with employment reaching 633,000, an 8.6 percent increase from 2023.

Military aeronautics alone accounted for 240,000 jobs, growing 10.1 percent year-on-year, while defence exports rose 2.1 percent to €60.0 billion. The U.S. aerospace and defence industry generated nearly $995 billion in total business activity in 2024, contributing $443 billion in economic value and supporting over 2.2 million direct and indirect jobs with average wages of $115,000, 56 percent above the national average.

India's defence sector recorded its highest-ever defence production of 1.54 lakh crore in FY 2024-25, with indigenous production reaching 1,27,434 crore in FY 2023-24, marking 174% increase from FY 2014-15. Defence budgets rose from 2.53 lakh crore in 2013-14 to 6.81 lakh crore in 2025-26, while defence exports surged to 23,622 crore from under 1,000 crore in 2014.

The U.S. government's Federal Zero Trust Strategy mandated all federal agencies to adopt Zero Trust principles by the end of 2024, with CISA allocating billions to modernise federal IT under Zero Trust frameworks, focusing on identity-proofing and encrypted DNS solutions. Government and defense sectors manage highly sensitive classified information, command and control systems, intelligence databases, and critical infrastructure that demand the most rigorous identity governance. Identity analytics solutions enable these organisations to detect insider threats, enforce separation of duties, monitor privileged access to classified systems, and ensure compliance with security clearance requirements capabilities that become increasingly vital as defence organisations expand their use of cloud services, AI systems, and collaborate with private sector contractors.

Category-wise Analysis

Solution Type Insights

Software solutions dominate the Identity Analytics Market, capturing 71.2% market share in 2026, as organizations prioritize comprehensive platforms that integrate identity governance, risk analytics, and policy enforcement capabilities. These solutions leverage machine learning and artificial intelligence to automate identity risk detection, as demonstrated by Omada's May 2024 launch of its Identity Analytics solution within Omada Identity Cloud, which enables intelligent role mining and data-driven insights to optimise user roles, enhance security, and improve compliance reporting.

Identity analytics platforms provide real-time visibility into access patterns, enabling security teams to identify orphan accounts, detect excessive privileges, and flag anomalous user behaviour that may indicate compromised credentials or insider threats. The software segment benefits from the shift toward cloud-based deployment models that offer scalability, reduced infrastructure costs, and faster time-to-value for customers.

The services segment is experiencing rapid expansion as organizations require specialized expertise to implement, customise, and optimise their identity analytics deployments. Professional services encompassing consulting, implementation, and integration are critical given the complexity of modern identity environments and the need to align analytics capabilities with specific organisational risk profiles and compliance requirements.

End User Insights

The Banking, Financial Services, and Insurance sector commands the largest market share at 35.6 percent in 2026, reflecting the industry's critical need for robust identity governance to protect sensitive financial data and comply with stringent regulatory requirements. Financial institutions operate in heavily regulated environments where identity-related compliance failures result in substantial penalties, making identity analytics essential for demonstrating adherence to know-your-customer (KYC), anti-money laundering (AML), and data privacy regulations.

The European banking sector held total assets of €43.6 trillion in 2023, with loans outstanding at €26.8 trillion and deposits from businesses and households reaching €17.3 trillion, despite structural transformation reducing credit institutions to 5,304 through digitalisation and efficiency-focused restructuring.

The sector's workforce of over 2 million employees requires sophisticated privileged access management and continuous monitoring, particularly for personnel with access to customer financial records, trading systems, and payment processing platforms. BFSI organisations face elevated risk from both external attackers seeking financial gain and insider threats where employees might exploit access privileges for fraud or unauthorised transactions. Identity analytics platforms address these risks by establishing baseline access patterns for different roles, detecting anomalous activities such as unusual data exports or after-hours access to sensitive systems, and providing automated access certification workflows that ensure periodic review of user privileges. The sector's early adoption of identity analytics stems from both regulatory pressure and the direct financial impact of identity-related breaches, where compromised credentials can lead to fraudulent transactions, unauthorized fund transfers, and reputational damage that affects customer trust and market valuation.

Regional Insights and Trends

North America Market Trend

North America maintains market leadership in the Identity Analytics Market, accounting for 34.6% of global market share, driven by advanced cybersecurity infrastructure, stringent regulatory frameworks, and a high concentration of early technology adopters. The region benefits from extensive cloud adoption across enterprises, with organisations deploying multi-cloud and hybrid IT infrastructures that necessitate sophisticated identity governance and continuous monitoring capabilities.

The United States has implemented comprehensive federal mandates for zero trust adoption, with the Cybersecurity and Infrastructure Security Agency (CISA) allocating billions to modernise federal IT systems and requiring agencies to meet specific cybersecurity standards by the end of FY 2024, including enhanced identity verification, multi-factor authentication, and encrypted DNS implementations. Despite these investments, recent audits indicate only approximately one-fifth of federal agencies fully meet CISA's zero trust maturity benchmarks, highlighting ongoing implementation challenges and sustained demand for identity analytics solutions that can provide visibility, risk assessment, and policy enforcement capabilities required for compliance.

East Asia Market Trend

East Asia represents a rapidly expanding market for identity analytics solutions, capturing 20% of global market share, as the region's dynamic digital economy and technology-forward government policies drive adoption of advanced cybersecurity capabilities. China's banking sector demonstrated robust fundamentals as of Q2 2025, with total banking assets reaching RMB 467.3 trillion and insurance assets growing 9.2 percent to RMB 39.2 trillion, while maintaining strong asset quality with a non-performing loan ratio of 1.49 percent and capital adequacy ratio of 15.58 percent.

Large commercial banks accounted for 43.7 percent of total banking assets, with inclusive loans to micro and small enterprises rising 12.3 percent to RMB 36 trillion, reflecting continued financial inclusion efforts that expand the identity management challenge as more individuals and businesses gain access to formal financial services. Commercial banks' net profits reached RMB 1.2 trillion, while the insurance sector recorded primary premium income of RMB 3.7 trillion with a comprehensive solvency ratio of 204.5 percent, indicating financial stability that supports continued technology investment.

Asia Pacific has emerged as a zero trust pioneer, with over two-thirds of enterprises running formal ZTA programs dramatically higher than other regions with governments in Singapore and Australia providing tax breaks for SMEs adopting cloud-native ZTA solutions, while Japan's Financial Services Agency mandates ZTA for all fintech firms by Q3 2025, creating regulatory drivers for identity analytics adoption across the region's rapidly digitalizing economies.

Europe Market Trend

Europe captures 22% of the global Identity Analytics Market, supported by stringent data protection regulations, a mature financial services sector, and comprehensive cybersecurity frameworks that mandate robust identity governance capabilities. The European Union's financial and insurance activities sector generated €0.9 trillion in value added across nearly 867,000 enterprises in 2022, employing approximately 5 million people with notably high productivity reflected in a wage-adjusted labor productivity ratio of 236.1 per cent and gross operating rate of 24.0 percent, surpassing the business economy average.

The sector encompasses financial service activities excluding insurance and pension funding with the highest turnover at €1.2 trillion, and auxiliary activities supporting financial services, with Germany, France, Italy, Spain, and Poland together accounting for over 65 percent of value added and 66 percent of employment, highlighting concentrated economic significance within major European markets. The European banking sector held total assets of €43.6 trillion in 2023, though it underwent a structural transformation with credit institutions falling to 5,304 and bank branches reducing to approximately 129,400 due to digitalisation and efficiency-focused restructuring, demonstrating the sector's evolution toward digital channels that require sophisticated identity management.

Competitive Landscape

The Global Identity Analytics market exhibits a moderately consolidated yet competitive landscape, where a mix of established tech giants and specialized identity security firms drive innovation and market growth. Major players such as Microsoft Corporation, Oracle, Okta Inc., CyberArk Software Ltd., SailPoint Technologies, Inc., and One Identity LLC dominate large enterprise deployments by offering comprehensive identity analytics integrated with broader IAM and security platforms, leveraging AI and behavioral analytics to enhance threat detection and access governance.

Microsoft’s Azure/Entra ecosystem and Oracle’s enterprise suites benefit from deep cloud integrations, while Okta and SailPoint maintain strong footholds in cloud-native identity management and governance centric analytics. CyberArk and One Identity differentiate through privileged access monitoring and risk focused identity insights, catering to regulated industries and hybrid environments. Meanwhile, niche and emerging players like Radiant Logic, Gurucul, HID Global, Evidian, Nexis GmbH, and Securonix push specialized analytics capabilities, fueling competitive pressures and broadening solution diversity.

Key Industry Developments

- 13 November 2025, Rubrik’s research highlights the growing importance of Identity Resilience as AI adoption introduces non-human and agentic identities, expanding the identity attack surface. Organizations are increasingly prioritizing identity management, strengthening IAM strategies, and preparing for AI-driven threats, emphasizing that robust identity analytics and resilience are critical to quickly detect compromises, mitigate risks, and ensure cyber recovery in the evolving digital workplace.

- 10 October 2024, SpyCloud enhanced its Investigations solution by embedding Identity Analytics through the IDLink feature, enabling faster and more comprehensive analysis of digital identities for insider risk, supply chain threats, and cybercrime investigations. The analytics capability accelerates threat actor attribution, uncovers identity exposures across organizations, and strengthens security operations, fraud prevention, and law enforcement investigations.

Companies Covered in Identity Analytics Market

- CyberArk Software Ltd.

- Evidian (Atos Group)

- Gurucul

- HID Global Corporation (Assa Abloy AB)

- Microsoft Corporation

- Nexis GmbH

- Okta Inc.

- One Identity LLC

- Oracle

- Ping Identity

- Radiant Logic Inc.

- SailPoint Technologies, Inc.

- Securonix

Frequently Asked Questions

The global Identity Analytics Market is projected to be valued at US$ 2.6 Bn in 2026.

The Solution segment is expected to account for approximately 71.2% of the Global Identity Analytics Market by Component Type in 2026.

The market is expected to witness a CAGR of 22.3% from 2026 to 2033.

Escalating identity-based cyberattacks, accelerated Zero Trust adoption across federal and enterprise environments, and stringent regulatory/compliance mandates GDPR, CCPA, U.S. state privacy laws are collectively driving strong demand for advanced identity analytics that enable continuous monitoring, behavioral risk scoring, and automated identity governance.

Key market opportunities include expanding BFSI digitization and compliance-driven identity risk monitoring, and rapid government & defense modernization with Zero Trust mandates, both creating strong demand for advanced identity analytics to secure privileged access, detect insider threats, and ensure regulatory governance across complex digital ecosystems.

Key players in the Identity Analytics Market include Microsoft Corporation, Oracle, Okta Inc., CyberArk Software Ltd., SailPoint Technologies, Inc., and One Identity LLC