- HVAC

- HVAC System Analyzer Market

HVAC System Analyzer Market Size, Share, and Growth Forecast, 2026 - 2033

HVAC System Analyzer Market by Offering (Hardware, Software, Services), Measurement Type (Temperature & Humidity Analysis, Airflow Analysis, Pressure & Differential Pressure Analysis, Power & Energy Consumption Analysis, Vibration & Noise Analysis, Combustion Analysis, Air Quality Analysis, Leak Detection / Refrigerant Analysis, Others), Industry and Regional Analysis for 2026 - 2033

HVAC System Analyzer Market Size and Trends

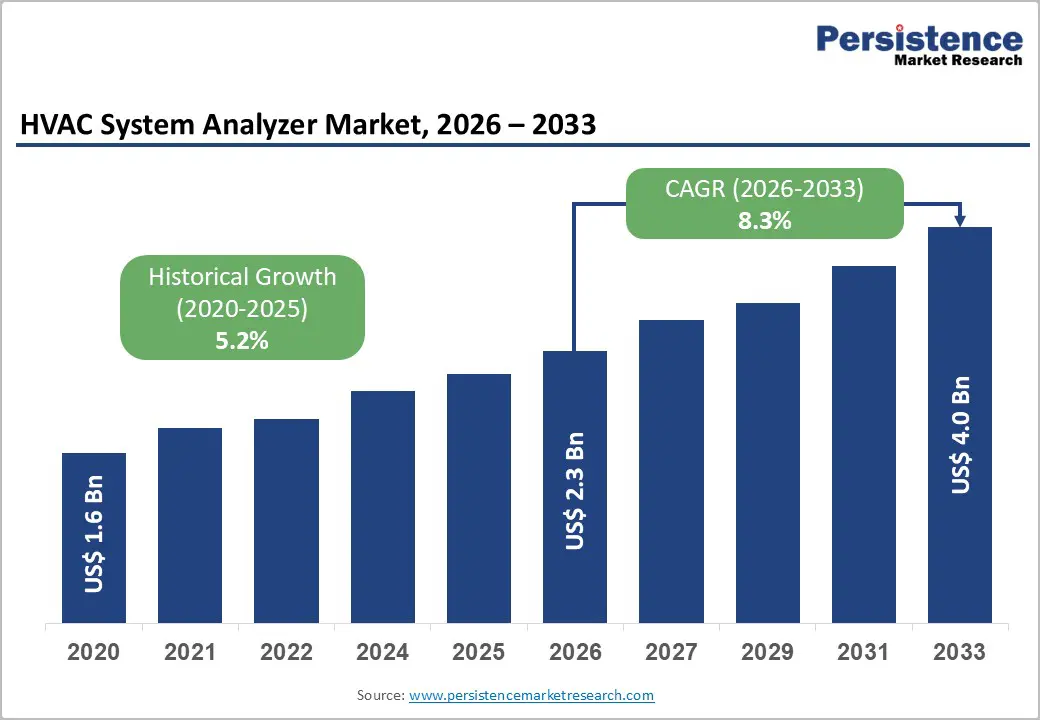

The global HVAC system analyzer market size is projected to rise from US$2.3 billion in 2026 to US$4.0 billion by 2033. It is anticipated to grow at a CAGR of 8.3% over the forecast period from 2026 to 2033, driven by escalating demand for energy-efficient HVAC systems, stringent government regulations mandating carbon-emission reductions, and the widespread adoption of IoT and artificial intelligence for predictive maintenance and system optimization.

These factors work synergistically to create a compelling business case for facility managers and building operators to invest in advanced diagnostic equipment that extends equipment lifespan, reduces operational costs, and ensures regulatory compliance.

Key Industry Highlights:

- Leading Offering: Hardware dominates with over 55% share in 2026, valued at more than US$ 1.3 Bn, driven by the need for accurate, real-time, on-site diagnostics using durable sensors, probes, and handheld devices. Software is the fastest-growing segment at 12.1% CAGR, supported by rising adoption of cloud analytics, predictive maintenance, remote monitoring, and compliance-driven performance tracking across multi-site facilities.

- Leading Measurement Type: Temperature & humidity analysis leads with over 24% market share in 2026, exceeding US$ 552 Mn, as these parameters are the primary indicators of comfort, energy efficiency, and system health across commercial and industrial HVAC systems. Air quality analysis is the fastest-growing at a 10.7% CAGR, driven by stricter indoor air quality regulations, health-focused building design, and the need to balance ventilation efficiency with energy consumption.

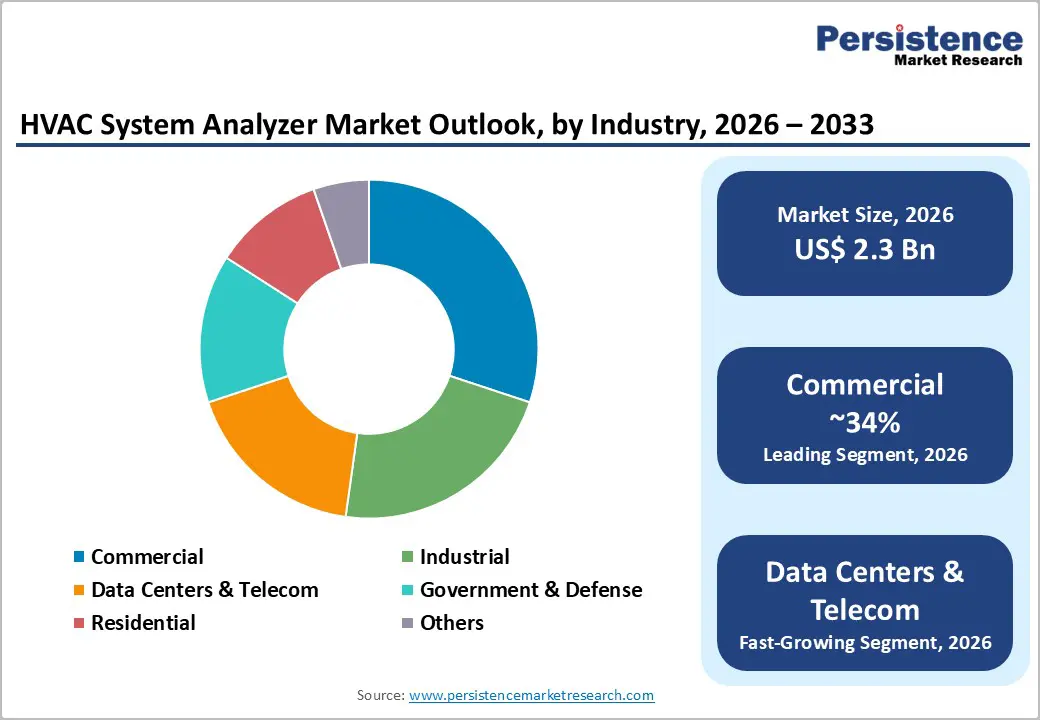

- Leading Industry: The commercial sector holds the largest share at over 34% in 2026, valued at over US$782 Mn, driven by high energy costs, regulatory pressures, and the need for continuous performance optimization across large building portfolios. Data centers & telecom represent the fastest-growing industry at an 11.4% CAGR, fueled by rising rack densities, 24/7 operations, and critical requirements for precise thermal and airflow monitoring to ensure uptime and reduce PUE.

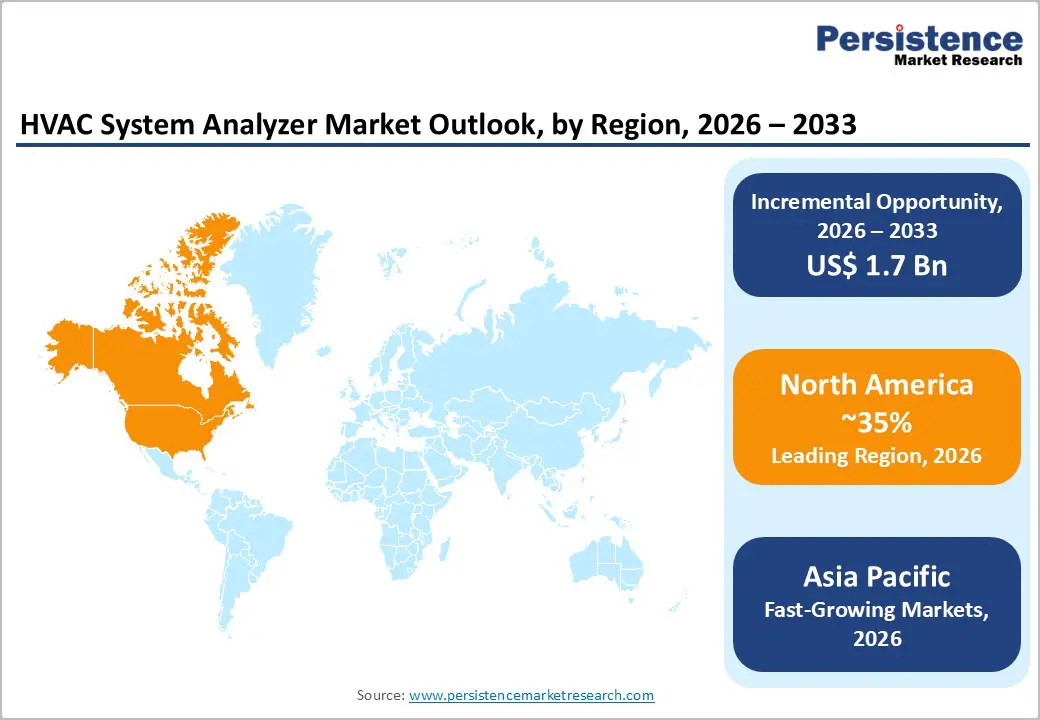

- Leading Region: North America leads the global market with over 35% share in 2026, reaching approximately US$ 805 Mn, supported by stringent EPA and DOE regulations, high commercial building density, and strong adoption of advanced wireless and AI-enabled diagnostic tools. Asia-Pacific is the fastest-growing region, with a 13.4% CAGR, driven by rapid urbanization, smart city initiatives, expanding data center infrastructure, and cost-competitive manufacturing in China, India, and Southeast Asia.

| Key Insights | Details |

|---|---|

| HVAC System Analyzer Market Size (2026E) | US$2.3 Bn |

| Market Value Forecast (2033F) | US$4.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Dynamics

Driver - Stringent Energy Efficiency Regulations and Compliance Requirements

Frameworks such as the U.S. EPA standards, the EU Energy Performance of Buildings Directive, and similar regulations in Japan, South Korea, and China mandate continuous monitoring and higher efficiency benchmarks for commercial buildings. Non-compliance results in significant penalties, prompting facility managers to invest in advanced diagnostic tools. HVAC analyzers with real-time monitoring help technicians detect inefficiencies within minutes, reducing diagnostic time by 50-70% versus traditional methods. With energy costs accounting for 30-40% of operational expenses in commercial properties, the need for compliance-driven performance optimization is a major driver of procurement.

Rapid Adoption of IoT, AI, and Predictive Maintenance Technologies

The convergence of IoT, AI, and cloud computing is shifting HVAC diagnostics from reactive repairs to predictive maintenance, enabling real-time monitoring and advanced fault detection. Modern HVAC analyzers now feature wireless connectivity, data logging, and mobile apps, allowing technicians to capture field data and transmit it to centralized analytics platforms. AI-driven predictive maintenance helps reduce unexpected equipment failures and emergency service calls, while extending system lifespans and lowering maintenance costs. Integration of HVAC analyzers into smart building management systems is driving broader adoption in new construction and retrofit projects across North America, Western Europe, and Asia-Pacific urban centers.

Restraint - High Initial Capital Investment and Operational Complexity

Advanced HVAC system analyzers with digital interfaces, wireless connectivity, and cloud integration typically cost US$2,500 to US$15,000 per unit, depending on measurement capabilities and sensor sophistication. For small and medium-sized HVAC service contractors with limited capital budgets, this high upfront cost creates a significant investment barrier and extends payback periods. The complex diagnostic features require specialized training to operate the equipment and accurately interpret detailed measurement data. Regional disparities in technician availability and skill levels further limit adoption. Training and certification programs often demand 40-80 hours of technical instruction, increasing personnel costs and making it difficult for smaller service providers to compete with larger firms that have dedicated training resources.

Technological Integration Challenges with Legacy HVAC Infrastructure

Many commercial and industrial facilities still rely on older electromechanical HVAC controls that lack digital interfaces, making them incompatible with modern analyzers and wireless communication protocols. Retrofit projects often encounter unexpected compatibility issues, necessitating costly control-system upgrades or custom adapter solutions. This fragmentation extends implementation timelines and increases project costs, especially in aging building stock across Western Europe, the Eastern United States, and major industrial regions. As a result, facility managers frequently delay adopting advanced diagnostic systems due to perceived complexity and high upfront investment.

Opportunity - Explosive Growth in Data Center Cooling and High-Performance Computing Infrastructure

The explosive growth of AI training, cloud expansion, and edge computing is driving unprecedented heat loads in data centers, with NVIDIA H100 GPUs producing power densities above 20-40 kW per rack compared to 5-15 kW in traditional servers. To manage this extreme thermal stress, operators in North America, China, and Western Europe are rapidly deploying liquid cooling, precision air conditioning, and real-time thermal monitoring solutions. This is creating strong demand for advanced HVAC system analyzers that monitor refrigerant pressure, liquid flow, thermal gradients, and energy consumption. Such diagnostic tools are critical for optimizing cooling performance, improving reliability, and reducing Power Usage Effectiveness (PUE).

Transition to Low-GWP Refrigerants and Environmental Compliance Solutions

The global phase-out of high-GWP refrigerants like HCFC-22 (R-22) and the shift toward low-GWP alternatives such as R-32, R-454B, and R-290 are driving strong demand for advanced HVAC analyzers with leak detection and refrigerant identification capabilities. Regulatory frameworks such as the EPA rules and Montreal Protocol mechanisms in North America, along with the EU’s F-Gas Regulation, require strict monitoring and reporting of refrigerant emissions in commercial and industrial HVAC systems. Next-generation analyzers, using ultra-precise electronic sensors and infrared technology, offer multi-refrigerant compatibility and enhanced leak-detection sensitivity, supporting compliance and documentation.

Category-wise Analysis

Offering Insights

Hardware dominates the global market, capturing more than 55% market share in 2026 with a value exceeding US$ 1.3 Bn, as real-time measurement and diagnostics require robust physical tools that withstand varied field conditions and deliver accurate data. Technicians depend on reliable sensors, probes, and handheld analyzers to quickly identify faults and optimize system performance. The need for precision, durability, and ease of use in on-site troubleshooting drives stronger investment in hardware solutions. Hardware often integrates seamlessly with software platforms, reinforcing its central role in practical HVAC diagnostics.

Software demonstrates a significant rate at 12.1% CAGR due to buildings increasingly relying on data-driven operations to improve efficiency and reduce energy costs. Software enables real-time monitoring, predictive maintenance, and automated fault detection, which are essential as HVAC systems become more complex. It also supports remote diagnostics and cloud-based analytics, allowing facility managers to optimize performance across multiple sites. As sustainability and regulatory pressure increase, software tools become the primary way to continuously track compliance and improve indoor air quality.

Measurement Type Insights

Temperature & humidity analysis holds over 24% market share in 2026, with a value exceeding US$ 552 Mn, as they are the most fundamental indicators of indoor comfort and system efficiency. Most HVAC issues, like improper cooling, high energy consumption, and uneven airflow, first show up as temperature or humidity imbalances, making them the most common targets for routine diagnostics. Monitoring these factors helps facilities quickly detect leaks, insulation problems, or malfunctioning components, enabling faster corrective action. Many industries require strict temperature and humidity control, driving frequent and continuous analysis.

Air quality analysis is expected to grow at the highest rate, with a CAGR of 10.7%, due to buildings being designed increasingly and operated with occupant health and comfort as a top priority. Rising awareness of indoor pollution, allergens, and airborne pathogens is pushing businesses to continuously monitor ventilation and filtration performance. Stricter indoor air quality standards and workplace safety regulations are driving demand for real-time air quality monitoring tools. The growing focus on energy-efficient HVAC operations requires accurate air quality data to balance ventilation needs with energy use.

Industry Insights

Commercial commands the largest market share at over 34% in 2026, with a value exceeding US$ 782 Mn, due to commercial buildings having higher operational and maintenance demands compared to residential setups. These facilities require continuous performance monitoring and preventive diagnostics to ensure energy efficiency, meet regulatory standards, and minimize downtime. The complexity and scale of commercial HVAC systems also necessitate advanced analyzers for accurate system optimization, fault detection, and compliance reporting. Businesses prioritize cost reduction through predictive maintenance and improved indoor air quality for occupant comfort and productivity.

Data centers & telecom are expected to grow at a CAGR of 11.4% as they run 24/7 and require precise climate control to avoid overheating, equipment failure, and service downtime. As rack densities and power loads increase, continuous monitoring of temperature, airflow, and humidity becomes critical to maintain reliability and efficiency. HVAC system analyzers help operators detect hotspots, optimize cooling performance, and reduce energy consumption. With stricter uptime requirements and higher operational costs, these sectors increasingly rely on advanced HVAC analysis for stable and resilient operations.

Regional Insights

North America HVAC System Analyzer Market Trends

North America holds over 35% share in 2026, reaching US$ 805 Mn value, due to the United States’ advanced industrial base, technology-focused business environment, and strict EPA energy regulations. Federal mandates from the U.S. DOE and incentives like ENERGY STAR boost investments in efficient HVAC diagnostics. Major cities such as New York, Los Angeles, Chicago, and Houston lead procurement due to high commercial building density and modernization initiatives. North America also leads in innovation, with companies like Fluke, Fieldpiece, TSI, etc. investing heavily in wireless systems, AI analytics, and mobile apps, enabling premium pricing and global technology leadership. Strong distribution through HVAC contractors, electrical wholesalers, and e-commerce ensures fast adoption and robust after-sales support.

Asia Pacific HVAC System Analyzer Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 13.4%, due to rapid urbanization, commercial real estate expansion, and strong government support for green building and smart city initiatives. China leads regional growth with concentrated demand in major metropolitan areas, while India’s infrastructure development and expanding data center capacity are boosting adoption. Cost-competitive manufacturing in China and Vietnam allows local producers to offer HVAC analyzers at lower prices, supporting market share gains through affordability and localized product offerings. Southeast Asian markets such as Thailand, Indonesia, and the Philippines are also rising due to increasing cooling needs and infrastructure growth, creating new opportunities for manufacturers with strong distribution and service networks.

Europe HVAC System Analyzer Market Trends

Europe is expected to hold more than 22% share by 2026, driven by energy efficiency regulations and growing use of heat pump technologies. Germany leads the region, supported by manufacturing strength and stringent EU directives. France, the UK, and Spain show rapid growth due to commercial building upgrades, sustainability goals, and compliance requirements. Western Europe is increasingly focused on smart building solutions and IoT integration, boosting demand for advanced diagnostic tools. While Eastern Europe trails due to lower energy budgets and limited skilled technicians, the Nordic countries are accelerating adoption through heat pump deployment and smart HVAC initiatives.

Competitive Landscape

The HVAC system analyzer market is moderately fragmented, with a mix of global instrumentation leaders and regional specialized players competing. Manufacturers focus on product differentiation through advanced sensor accuracy, faster diagnostics, and integrated cloud analytics to meet rising efficiency and compliance needs. Many adopt partnership strategies with HVAC service providers and energy management firms to expand reach and offer bundled solutions.

Key Developments:

- In February 2025, Mojave Energy Systems launched ArctiDry HP liquid desiccant HVAC system, combining heat pump technology with advanced humidity control, generating substantial demand for specialized analyzers capable of validating performance across integrated heating, cooling, and dehumidification functions in commercial facilities pursuing sustainable building certification.

- In January 2025, Fieldpiece Instruments expanded Job Link ecosystem with advanced wireless pressure probes, psychrometer accessories, and cloud-based reporting integration, reinforcing its market leadership position in handheld analyzer innovation and comprehensive system diagnostics for HVACR professionals across residential and commercial applications.

Companies Covered in HVAC System Analyzer Market

- Fluke Corporation

- Testo SE & Co. KGaA

- Fieldpiece Instruments, Inc.

- TSI Incorporated

- Dwyer Instruments, Inc.

- UEi Test Instruments

- Klein Tools, Inc.

- FLIR Systems

- Amprobe

- Bacharach, Inc.

- PCE Instruments

- Sauermann Group

- Others

Frequently Asked Questions

The global HVAC system analyzer market is projected to be valued at US$2.3 Bn in 2026.

The need for precise system diagnostics, energy efficiency optimization, and regulatory compliance, as building owners and technicians seek tools to reduce operating costs, ensure indoor comfort, and meet tightening environmental standards, are key drivers of the market.

The market is expected to witness a CAGR of 8.3% from 2026 to 2033.

Rapid adoption of smart buildings, data centers, and green infrastructure, creating demand for advanced HVAC analyzers with digital connectivity, real-time monitoring, and predictive maintenance capabilities, is creating strong growth opportunities.

Fluke Corporation, Testo SE & Co. KGaA, Fieldpiece Instruments, Inc., TSI Incorporated, Dwyer Instruments, Inc., UEi Test Instruments, Klein Tools, Inc., FLIR Systems are among the leading key players.