- Hardware & Software IT Services

- Humanoid Robot Market

Humanoid Robot Market Size, Share, and Growth Forecast, 2026 - 2033

Humanoid Robot Market by Locomotion Type (Bipedal Humanoid Robots, Wheeled Humanoid Robots, Hybrid.), Level of Autonomy (Semi-Autonomous, Fully Autonomous, Tele-Operated), Component Type (Hardware, Software, Services), Industry (Industrial & Logistics, Commercial & Public Services, Healthcare & Assisted Living, Defense & Security, Residential / Consumer, Research & Education), and Regional Analysis for 2026 - 2033

Humanoid Robot Market Size and Trends Analysis

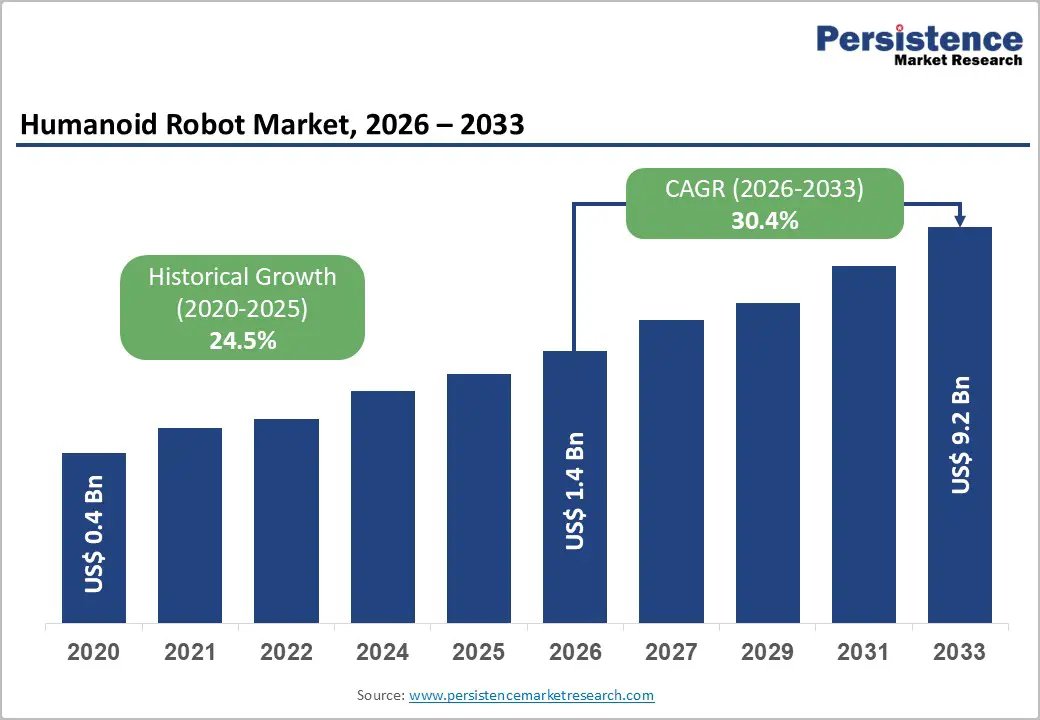

The global humanoid robot market is likely to be valued at US$ 1.4 billion in 2026 and is projected to reach US$ 19.6 billion by 2033, growing at a CAGR of 30.4% between 2026 and 2033. This extraordinary expansion reflects a fundamental shift in automation technology, with humanoid robots transitioning from research prototypes to commercially viable solutions across industrial, healthcare, defence, and consumer applications.

Industrial adoption is accelerating rapidly, with over 800 million yuan in commercial orders already recorded for industrial humanoid platforms, while government procurement increased 214 percent in China during 2024, signalling strong institutional confidence in humanoid robot capabilities for real-world deployment. Investment activity reached unprecedented levels, exemplified by Apptronik securing US$ 935 million in Series A funding, positioning the company among the top three most funded humanoid robotics firms globally and directing capital toward scaling production of its Apollo humanoid robot for industrial and factory environments.

Key Industry Highlights:

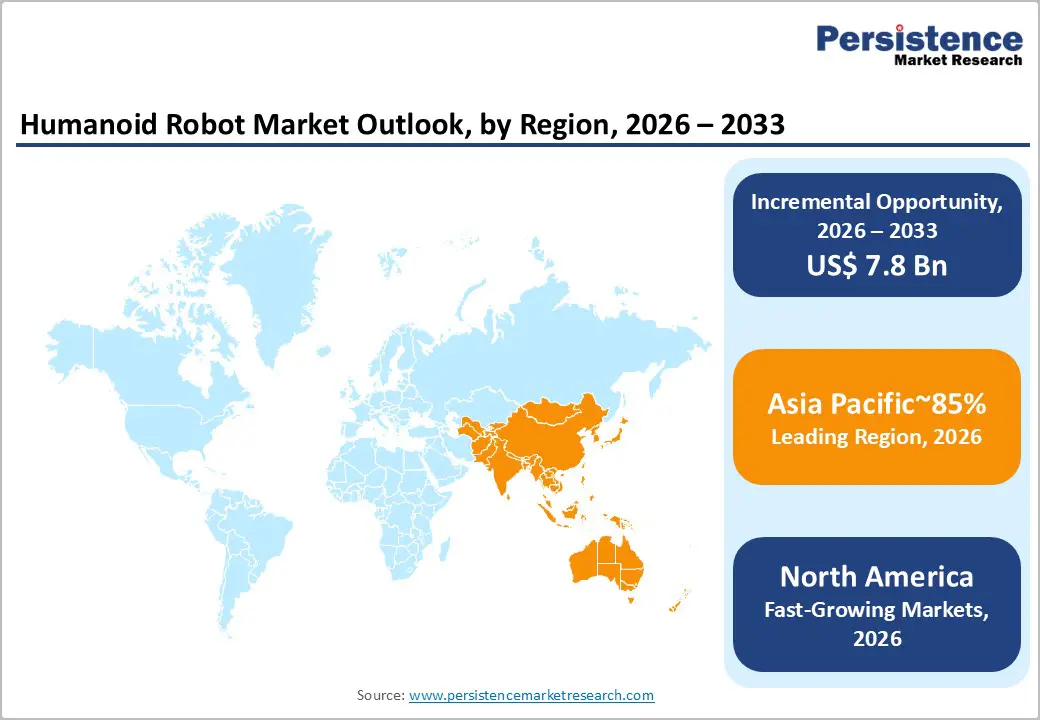

- Leading Region: Asia Pacific leads the Humanoid Robot Market with 85% share, driven by government subsidies, large-scale manufacturing, and industrial policies across China, Japan, South Korea, and India.

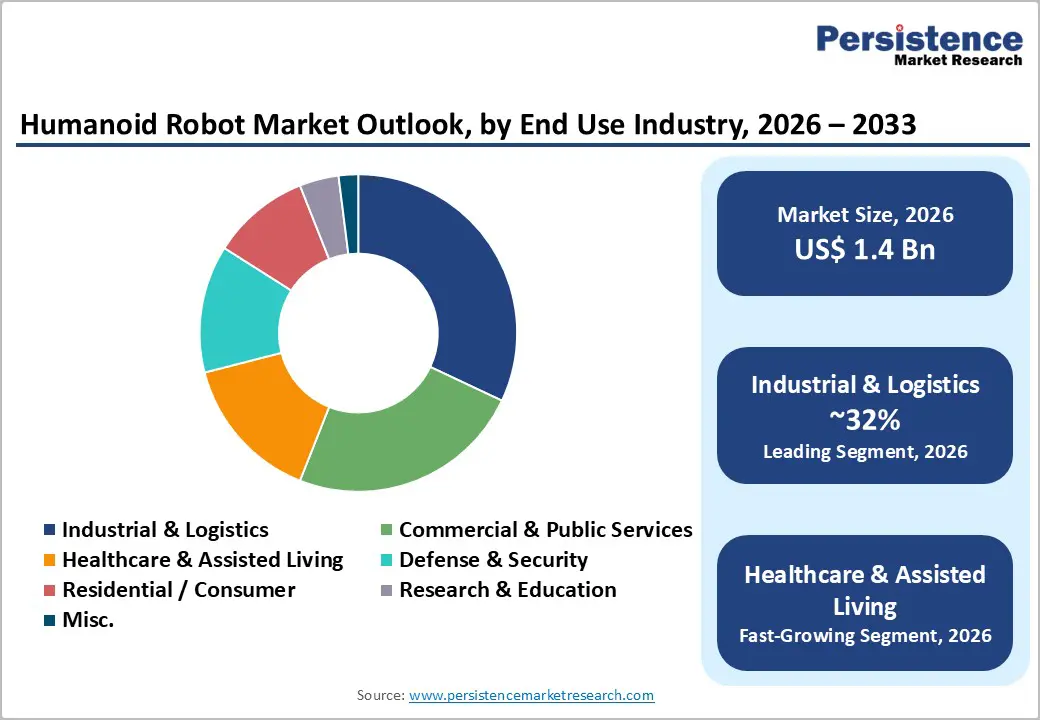

- Leading Industry: Industrial and logistics applications account for 32% market share, propelled by high labor intensity, operational ROI, and adoption of warehouse automation solutions.

- Leading Component Type: Defence and security is the fastest-growing segment, driven by government procurement, strategic initiatives, and rising defense budgets globally.

- Leading Locomotion: Bipedal humanoid robots hold 59% market share, preferred for navigating human-centric environments with stairs, uneven surfaces, and confined spaces.

- Growth Indicator: Fully autonomous humanoid robots are the fastest-growing segment of the autonomy market, enabled by AI, advanced sensors, and large-scale industrial deployments.

- North America Market Scenario: North America holds 8% market share, supported by advanced enterprise adoption, a robust industrial ecosystem, and leading companies like Boston Dynamics, Agility Robotics, and Apptronik.

- Europe’s Technology Focus: Europe accounts for 4% share, backed by strong R&D, defence modernisation, and advanced humanoid development by companies like Agile Robots and PAL Robotics.

| Key Insights | Details |

|---|---|

| Humanoid Robot Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 9.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 30.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 24.5% |

Market Dynamics

Drivers - Acute Manufacturing and Skilled Labor Shortages Driving Automation Adoption

Manufacturing and industrial sectors face unprecedented workforce constraints that fundamentally limit production capacity and economic growth, compelling enterprises to embrace robotic automation as a strategic necessity. According to data aggregated by Area Development and Lightcast, American employers report nearly 2.9 million job openings annually across skilled trades, while education and training systems collectively produce only approximately 1.25 million qualified graduates, creating a structural shortfall of 1.7 million workers annually.

The manufacturing Institute projects 2.1 million unfulfilled manufacturing jobs by 2030, resulting from skilled labour shortages. Global labour market analyses project a shortfall of nearly 85 million workers worldwide by 2030, equivalent to US$ 8.5 trillion in unrealised revenue. The International Federation of Robotics reports that global industrial robot installations reached 541,000 units in two thousand twenty three, with robot density hitting a record 162 units per 10,000 employees, more than double the 74 units measured in two thousand seventeen, reflecting accelerating automation adoption. These workforce constraints position the Humanoid Robot Market as a critical solution for manufacturers seeking to maintain operational continuity, with humanoid platforms offering flexibility to perform diverse tasks across manufacturing, machine tending, material handling, and logistics operations previously dependent on human labor.

Technological Convergence of AI, Embodied Intelligence, and Physical Robotics

Rapid advancements in artificial intelligence, particularly large behavior models, reinforcement learning, and vision language action systems, are eliminating longstanding technical barriers to humanoid robot deployment and enabling autonomous, adaptive performance in unstructured environments. Boston Dynamics and Google DeepMind announced a strategic AI partnership to integrate DeepMind's Gemini Robotics foundation models with Atlas humanoid robots, enabling robots to perform a wide range of industrial tasks combining advanced physical capabilities with cutting-edge AI for perception, reasoning, tool use, and human interaction.

Boston Dynamics and Toyota Research Institute demonstrated Atlas robots powered by Large Behaviour Models performing complex whole-body manipulation and locomotion tasks autonomously without manual programming, marking a significant step toward general-purpose, AI-driven humanoid robots. Geek+ introduced Gino 1, the world's first humanoid robot specifically engineered for warehouse operations, utilising embodied AI and vision language action intelligence with multi-eye vision, dexterous three-finger hands, and dual force-controlled arms integrated with AMR fleets.

These technological breakthroughs enable the Humanoid Robot Market to transition from research demonstration platforms to commercially viable systems capable of real-world industrial and service applications, with AI enabling rapid skill acquisition, environmental adaptation, and safe human robot collaboration essential for scaled deployment.

Restraint - High Capital Investment and Total Cost of Ownership Barriers

The substantial upfront capital requirements and ongoing operational costs associated with humanoid robot deployment create significant adoption barriers, particularly for small and medium enterprises and cost-sensitive applications. Commercial humanoid robot platforms typically command premium pricing, with leasing models positioned around US$ 100,000 per robot per year for general-purpose labour platforms, substantially exceeding annual labour costs in many markets and requiring multi-year payback periods to achieve return on investment.

Beyond acquisition costs, humanoid robots require supporting infrastructure, including charging or battery swapping systems, integration with enterprise software and building management systems, ongoing maintenance, and specialised technical personnel for operation and troubleshooting, collectively raising the total cost of ownership. While large-scale production and manufacturing optimisation efforts aim to reduce unit costs, current pricing structures limit market penetration primarily to large enterprises with substantial capital budgets and applications with clear, quantifiable productivity gains, constraining broader adoption across the commercial and industrial landscape until cost curves decline through volume manufacturing and technological maturation.

Opportunity - Rapid Expansion of Commercial Deployment Programs

The transition from pilot testing to large-scale commercial deployment represents a transformative opportunity for humanoid robot manufacturers, with multiple Fortune 500 companies now committing to fleet-based implementations across logistics and manufacturing operations. Mercado Libre announced a commercial agreement with Agility Robotics to deploy Digit humanoid robots in its San Antonio fulfillment facility, marking significant progress toward integrating AI-powered humanoid platforms into large-scale logistics operations with future expansion planned across Latin America. Boston Dynamics unveiled the production version of its fully electric Atlas humanoid robot, featuring 56 degrees of freedom and a 50-kilogram payload capacity, and announced immediate manufacturing with fully committed deployments to Hyundai’s Robotics Metaplant Application Centre and Google DeepMind.

UBTECH Robotics secured substantial orders for its Walker S2 industrial humanoid robot, targeting delivery of hundreds of units this year and planning to scale annual production capacity across automotive manufacturing, smart factories, and intelligent logistics.

These high-profile commercial agreements establish proof points that reduce perceived risk for subsequent adopters, creating market momentum that accelerates broader industry acceptance and drives follow-on orders from competitors seeking operational parity.

The opportunity extends beyond individual robot sales to encompass recurring revenue from software subscriptions, maintenance services, operational analytics platforms, and continuous capability upgrades delivered through over-the-air updates, fundamentally shifting business models from capital equipment sales toward ongoing service relationships that improve customer lifetime value and revenue predictability for humanoid robot manufacturers.

Cross-Border Infrastructure and Public Service Applications

Government agencies are increasingly deploying humanoid robots for public infrastructure management, border security operations, and citizen service delivery, creating substantial institutional procurement opportunities beyond traditional commercial markets. UBTECH Robotics secured a major contract to deploy Walker S2 humanoid robots at China–Vietnam border crossings in Fang Chenggang for traveler guidance, inspections, patrols, and logistics operations, marking one of the first real-world government-backed deployments. These large-scale implementations demonstrate confidence in humanoid robot reliability for mission-critical public infrastructure applications, with 24-hour continuous operation enabled by autonomous battery replacement systems.

The public sector opportunity extends to smart city initiatives, transportation hubs, emergency response coordination, and facility management, where humanoid robots navigate environments designed for humans while delivering consistent service without fatigue or performance degradation. Educational institutions also represent a growing segment, with SoftBank Group donating Pepper humanoid robots to expand STEM programs and provide early exposure that fosters long-term market acceptance. These institutional deployments generate valuable operational data, establish safety precedents, and create reference cases that accelerate private-sector adoption in the Humanoid Robot Market.

Technological Convergence Enabling Advanced Capabilities

The integration of large behaviour models, foundation AI systems, and cloud-based edge computing is significantly enhancing humanoid robot capabilities, reducing manual programming requirements, and accelerating deployment timelines. Strategic collaborations, such as Boston Dynamics with Google DeepMind, leverage Gemini Robotics foundation models to enable Atlas robots to perform a wide range of industrial tasks, including perception, reasoning, tool use, and human interaction, without task-specific programming.

Partnerships with Toyota Research Institute have demonstrated that Atlas robots can autonomously execute complex whole-body manipulation and locomotion, marking progress toward general-purpose, AI-driven humanoid robots for industrial and research applications.

SoftBank and Yaskawa Electric’s collaboration on Physical AI, combining AI-RAN with multi-access edge computing, further enables multi-skilled functionality and real-time integration with building management systems. These technological advancements harness artificial intelligence, computer vision, and natural language processing to produce humanoid platforms that learn faster, adapt more quickly, and generalise across broader tasks, reducing the total cost of ownership and expanding the addressable applications across industries in the Humanoid Robot Market.

Category-wise Analysis

Locomotion Type Insights

Bipedal humanoid robots commanded 59% market share in 2026, reflecting strong customer preference for platforms capable of navigating environments designed for human workers without requiring infrastructure modifications. The bipedal configuration enables operation on stairs, uneven surfaces, and in confined spaces where wheeled systems cannot function effectively, providing maximum deployment flexibility in manufacturing facilities, warehouses, and commercial buildings with existing architectural constraints.

On February 16, 2026, the Beijing Innovation Center of Humanoid Robotics launched its Embodied Tien Kung 3.0 general-purpose humanoid platform, featuring enhanced balance, high-dynamic whole-body motion control, tactile interaction, and fully autonomous operation, powered by the proprietary Wise KaiWu embodied AI platform.

Wheeled humanoid robots are among the fastest-growing locomotion categories, driven by advantages in energy efficiency, movement speed, payload capacity, and mechanical simplicity compared to bipedal alternatives for applications prioritising throughput over environmental adaptability. Platforms like Geek+’s Gino 1 demonstrate their effectiveness in warehouse operations, performing picking, sorting, packing, and inspections using embodied AI and vision-language-action intelligence while integrating with existing autonomous mobile robot fleets. The wheeled configuration reduces power consumption per distance traveled, enables faster transit between workstations, and simplifies maintenance through fewer actuators and mechanical joints, lowering total cost of ownership in high-volume logistics environments where floor surfaces are optimised, and navigation complexity is moderate.

Level of Autonomy Insights

Semi-autonomous humanoid robots accounted for 46% of the market in 2026, reflecting a preference for systems that combine autonomous task execution with human oversight for exception handling and quality assurance. This mode balances productivity and risk management, allowing operators to supervise multiple robots while intervening only when unexpected situations occur. Semi-autonomous platforms also reduce operator training needs compared to fully teleoperated systems and avoid regulatory and liability concerns associated with fully autonomous operation in shared human environments.

Fully autonomous humanoid robots are the fastest-growing segment, driven by advances in AI, sensor technology, and operational datasets that enable reliable independent decision-making in complex environments. Platforms like Agile ONE and Agility Robotics’ enhanced Digit demonstrate capabilities such as layered AI architecture, autonomous docking, extended battery life, advanced safety features, and precision manipulation, enabling fully autonomous industrial operation. These innovations reduce supervision requirements, lower operational costs, improve ROI, and accelerate fueling adoption of fully autonomous humanoid systems across warehouses, manufacturing, and other commercial applications.

Industry Insights

Industrial and logistics applications commanded 32% market share in 2026, representing the largest deployment segment, driven by clear return-on-investment metrics, high labor intensity, and operational environments conducive to robotic automation. Warehouse operations support 4.7 million commercial robots installed across 50,000+ facilities globally by 2026, with logistics robot sales reaching 450,000 units in 2025, up from 75,000 in 2019, demonstrating sustained momentum in automated material handling adoption. Companies deploying warehouse automation report 25 to 30 percent reductions in labor costs, 300 percent faster order fulfillment, and accuracy rates approaching 99%, creating a compelling economic justification for humanoid robot investment.

Defence & Security is driven by government procurement, national security priorities, and growing defence budgets worldwide. Policy support, strategic initiatives, and investments in advanced robotics across the U.S., Europe, and India are accelerating the deployment of humanoid robots for surveillance, border security, and military applications, making this the fastest-expanding end-use segment.

Regional Insights

Asia Pacific Humanoid Robots Market Trends

Asia Pacific leads the global humanoid robot market with an estimated 85% regional share, driven by strong government industrial policies, large-scale capital investments, and rapid manufacturing expansion across China, Japan, South Korea, and India. China has established state-backed venture funds that have attracted nearly 1 trillion yuan (US$ 138 billion) from local governments and the private sector to support robotics, AI, and advanced innovation, building on its growth from roughly one-fifth to over half of global industrial robot installations.

Government subsidies to humanoid robot companies exceeded US$ 20 billion, including purchase incentives, free land, discounted rent, and additional financial support for companies that meet sales targets, while the procurement of robots and technologies surged by more than 200 percent.

The number of humanoid robot manufacturers in China nearly doubled to over 200, with the market projected to reach approximately RMB 10.471 billion (US$ 1.4 billion) and expected to account for around 32.7 percent of the global market. Japan is leveraging humanoid robots to address a projected shortfall of specialised caregivers, providing billions in subsidies, introducing robots into thousands of facilities, and integrating robotics into healthcare infrastructure.

India’s aerospace and defence ecosystem benefits from rising expenditure, increased indigenous production, and expansion of MSME suppliers from 8,000 to 16,000 companies, strengthening component manufacturing capacity. Municipal initiatives, such as Shenzhen’s Guangdong Embodied Intelligent Robot Innovation Center and a RMB 10 billion (US$ 1.4 billion) AI and robotics industry fund, further support AI software, hardware, and embodied AI development, reinforcing Asia Pacific’s dominance in the humanoid robot market.

North America Humanoid Robots Market Trends

North America accounts for approximately 8% of the global humanoid robot market, driven by strong innovation, advanced enterprise adoption, and a robust industrial ecosystem. The United States aerospace and defence sector contributes significantly to technology leadership, supporting over 2.2 million workers and generating US$ 443 billion in economic value, with highly skilled labour driving automation adoption.

Rising labour shortages, increasing manufacturing productivity, and the 82 percent of mid-sized manufacturers that are implementing or planning automation upgrades create favourable conditions for the deployment of humanoid robots. Policy frameworks, including centralised robotics offices, tax incentives, government procurement leadership, workforce training, and research funding, further support market growth.

Key players headquartered in the region include Boston Dynamics, Agility Robotics, and Apptronik, with Apptronik securing US$ 935 million in Series A funding, ranking among the top three most-funded humanoid robotics firms globally. Canada’s expanding e-commerce market, projected to reach US$ 104 billion, also drives demand for logistics automation, creating additional opportunities for humanoid robots.

Europe Humanoid Robots Market Trends

Europe accounts for around 4% of the global humanoid robot market, supported by advanced manufacturing, strong research institutions, and defense modernization programs that are driving robotics integration across industrial and military applications.

The aerospace and defence sector demonstrates robust performance, with turnover exceeding €325 billion, high-skilled employment, and substantial R&D investment of over €25 billion, emphasizing technological innovation and strategic autonomy. European companies like Agile Robots and PAL Robotics showcase regional capabilities, with Agile ONE demonstrating advanced industrial humanoid development in Germany and PAL Robotics leading service and bipedal humanoid innovation across research, healthcare, retail, agri-food, and industrial sectors. These developments highlight Europe’s focus on high-technology humanoid robotics, combining industrial commercialisation with research-driven innovation.

Competitive Landscape

The global humanoid robot market exhibits an emergent yet increasingly consolidated competitive landscape, with a handful of technologically advanced players driving commercialisation and real-world deployment. Established robotics innovators such as Boston Dynamics, Agility Robotics, UBTECH Robotics, PAL Robotics, and Unitree Technology are leading the pack by investing heavily in AI integration, industrial applications, and scalable production. Boston Dynamics’ Atlas and Agility Robotics’ Digit exemplify breakthroughs in mobility and automation, while UBTECH’s Walker series and Unitree’s H2 highlight rapid moves toward mass production and broader commercial use cases. PAL Robotics continues to influence research and service robotics, bridging the gap between academic and industrial demand.

Competition is intensifying with new entrants and partnerships (e.g., Boston Dynamics with Google DeepMind and Toyota Research Institute), but the market remains concentrated among these key players due to high development costs, deep AI expertise requirements, and significant capital investments. As adoption accelerates across logistics, manufacturing, and service sectors, strategic alliances and innovation leadership will further shape this consolidating yet dynamic market environment.

Key Industry Developments

- January 5, 2026, Boston Dynamics revealed the fully electric Atlas humanoid robot with immediate 2026 deployments to Hyundai and Google DeepMind. Featuring 56 degrees of freedom, 50 kg payload capacity, autonomous battery swapping, and integration with industrial systems via Orbit™ software, this launch represents a major step toward large-scale industrial adoption of humanoid robots, particularly in automotive and manufacturing sectors.

- November 17, 2025, UBTECH began mass production and delivery of its industrial humanoid robot Walker S2, with initial orders exceeding 800 million yuan and a target of 500 units within the year, scaling to 10,000 units by 2027. This milestone highlights one of the first large-scale commercial deployments of industrial humanoid robots, accelerating market adoption in manufacturing, logistics, and smart factories.

- February 11, 2026, Apptronik raised US$935 million to scale production and commercialisation of its Apollo humanoid robot, aimed at industrial and factory environments. The investment underlines strong investor confidence and supports next-generation product upgrades, broader deployment, and collaboration with humans, signalling a robust expansion trajectory for the global humanoid robot market.

Companies Covered in Humanoid Robot Market

- SoftBank Robotics Group

- PAL Robotics

- Figure AI

- Agility Robotics

- UBTECH Robotics Corp. Ltd.

- Apptronik

- ROBOTIS Co. Ltd.

- Boston Dynamics

- Hanson Robotics

- YuShu Technology Co.Ltd. (UNITREE)

Frequently Asked Questions

The global Humanoid Robot Market is projected to be valued at US$ 1.4 Bn in 2026.

The Bipedal Humanoid Robots segment is expected to account for approximately 59% of the Global Humanoid Robot Market by Wheeled Humanoid Robots in 2026.

The market is expected to witness a CAGR of 30.4% from 2026 to 2033.

The Humanoid Robot Market is driven by acute global skilled labor shortages and rapid technological advances in AI, embodied intelligence, and robotics, enabling autonomous, adaptable, and scalable industrial and service applications.

Key market opportunities in the Humanoid Robot Market lie in large-scale commercial deployments, government and public service applications, and leveraging AI and advanced robotics technologies for versatile, high-value industrial and service use cases.

Key players in the Humanoid Robot Market include Boston Dynamics, Agility Robotics, UBTECH Robotics, PAL Robotics, and Unitree Technology.