- Industrial Machinery

- Grinding Mill Market

Grinding Mill Market Size, Share, and Growth Forecast, 2026-2033

Grinding Mill Market by Mill Type (Ball Mills, Rod Mills, Semi-Autogenous Grinding Mills, Autogenous Grinding Mills, Vertical Mills), Application (Ore Grinding, Clinker & Raw Material Grinding, Coal Grinding, Chemical & Pigment Milling, Food & Pharma Milling), End-User (Mining Companies, Cement Plants, Power Plants, Chemical Manufacturers, Food & Pharma Companies), and Regional Analysis for 2026-2033

Grinding Mill Market Share and Trends Analysis

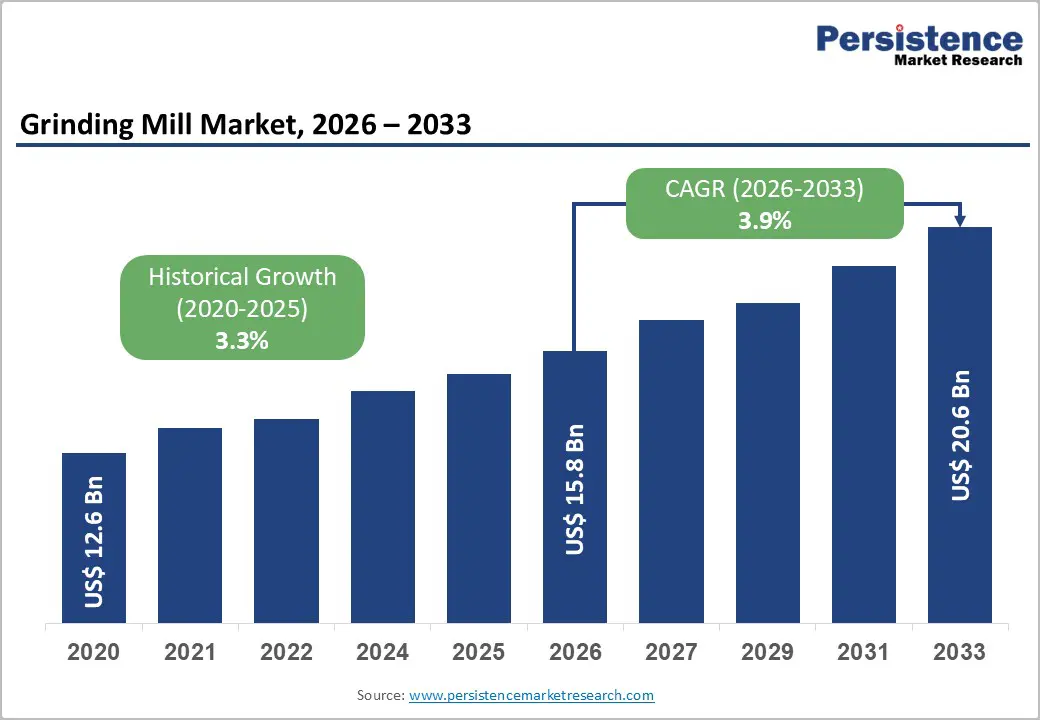

The global grinding mill market size is likely to be valued at US$ 15.8 billion in 2026, and is projected to reach US$ 20.6 billion by 2033, growing at a CAGR of 3.9% during the forecast period 2026–2033. This growth reflects a strong and increasing industrial demand across mining, cement, chemical, food, and pharmaceutical sectors, driven by ongoing infrastructure development and rapid urbanization in emerging economies. Companies are actively investing in advanced grinding technologies to enhance efficiency, productivity, and product consistency.

The market is benefiting from the widespread adoption of energy-efficient and automated milling solutions, which reduce operational costs while improving throughput. Manufacturers are optimizing their processes to meet stricter material quality and particle size specifications, while industries continuously scale production capacity to address rising consumption and evolving regulatory standards, sustaining robust market expansion.

Key Industry Highlights

- Dominant Mill Types: Ball mills are set to command around 43% revenue share in 2026, while vertical mills are likely to grow the fastest through 2033, driven by automation and energy-efficient designs.

- Leading Applications: Ore grinding is expected to hold approximately 39% share in 2026, while chemical and pigment milling is likely to expand fastest during 2026–2033, fueled by precision and fine particle requirements.

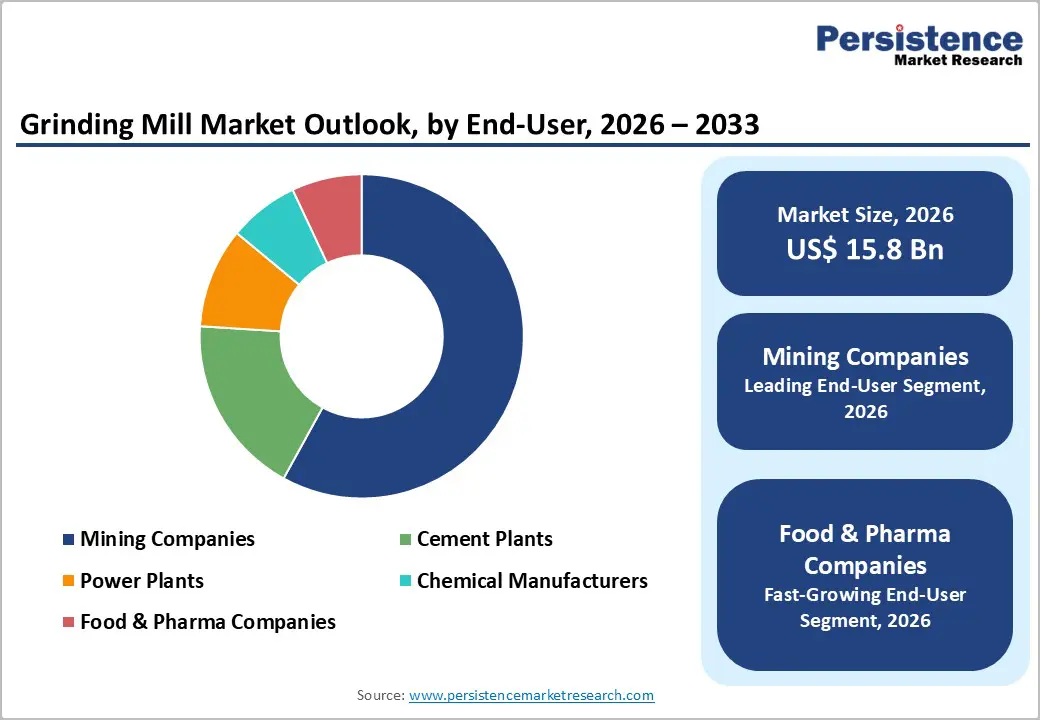

- Dominant End-Users: Mining companies are projected to account for about 45% revenue share in 2026, while food and pharma sectors are likely to grow the fastest at 6.1% CAGR.

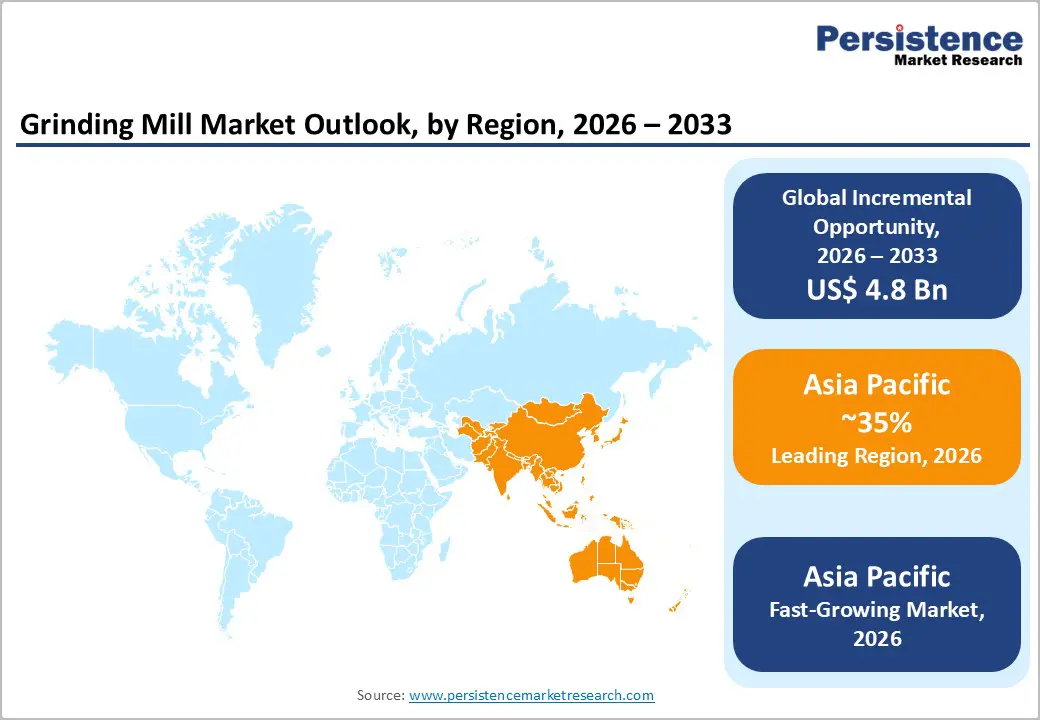

- Regional Leadership: Asia Pacific is poised to secure around 35% share in 2026 and register a 5.5% CAGR through 2033, led by industrial expansion and infrastructure growth.

- Competitive Environment: Key developments include the adoption of energy-efficient mills, automation integration, mergers, and strategic technology partnerships enhancing global presence.

| Key Insights | Details |

|---|---|

| Grinding Mill Market Size (2026E) | US$ 15.8 Bn |

| Market Value Forecast (2033F) | US$ 20.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Expansion and Intensifying Mining Activities

Global industrial growth, especially across mineral processing, cement production, and construction sectors, is bolstering demand for high-capacity milling systems worldwide. Grinding mills play a crucial role in achieving fine particle sizes for ores and raw materials, which directly supports productivity gains in mining and construction value chains. Rapid urban infrastructure development across Asia Pacific, particularly in China, India, and Australia’s mining and cement sectors, underscores this trend. Major trade and investment platforms such as Expo Real Asia Pacific 2026, focusing on infrastructure investment and development, signal sustained construction activity and capital inflows in the region through 2026 and beyond, linking demand for heavy industrial equipment to broader real estate and infrastructure growth.

Mining sector momentum continues to shape equipment investment patterns. A significant milestone was achieved with the Simandou iron-ore project in Guinea starting commercial exports in late 2025, supplying iron ore at scale to global steel and processing markets, including China. This underscores the ongoing expansion of hard-rock mining operations demanding advanced grinding and beneficiation systems. The critical minerals remain strategic for national economies: the Government of Canada announced a CA$ 165.2 million investment in critical minerals infrastructure in March 2026, enhancing planning, development and processing capacity across multiple provinces and supporting grid power upgrades tied to major mining expansions. These sustained infrastructure spending, major mining exports, and public support for critical mineral projects reinforce long-term demand for grinding mill systems and aftermarket services across key global markets.

Adoption of Energy-Efficient and Automated Technologies

Grinding mill manufacturers are increasingly integrating energy-efficient designs, automation, and digital monitoring technologies to reduce operating costs and improve sustainability outcomes. Automated control systems and IoT-enabled diagnostics enable real-time performance insights, predictive maintenance, and optimized throughput, all critical for capital-intensive industries managing cost and environmental pressures. Regulatory frameworks globally are reinforcing these shifts, incentivizing equipment investments that offer reduced energy consumption and carbon footprint improvements. In Europe, policymakers in early 2026 announced strategic energy efficiency measures for industrial systems, including electrification of core energy loads and regulatory support to curb dependency on traditional heat sources, underscoring the growing regulatory focus on energy performance in industrial settings.

Sector advancements also reflect broader innovation and sustainability priorities. For example, in gold processing and mining, there is increasing adoption of energy efficiency technologies and process improvements, driven by both operational optimization goals and environmental targets. This aligns with industry focus on lowering the energy intensity of production processes, including grinding circuits. The construction and industrial sectors are witnessing sustained investments in digitization and automation, with many new infrastructure projects embedding control-ready systems that enhance performance and tracking productivity. Combined with stronger governmental energy standards and sustainability reporting requirements, these developments are accelerating the transition to intelligent, energy-efficient grinding solutions that deliver measurable cost and environmental benefits across mature and emerging markets.

High Capital Intensity and Total Cost of Ownership Pressures

Grinding mill equipment typically requires sizeable upfront capital expenditure for procurement, installation, and commissioning. Advanced, automated systems with energy efficient technologies carry higher price points compared to legacy designs, which can deter smaller operators in price-sensitive regions and slow replacement cycles. Ongoing power consumption and maintenance costs remain substantial components of total cost of ownership. These financial pressures can constrain demand, especially in markets with tighter industrial budgets or weaker commodity pricing. Operators must often balance modernization priorities against broader capital allocation demands.

Recent cost pressures across industrial supply chains are highlighted by developments in the steel sector in early 2026, where hot-rolled coil prices in India climbed to two-year highs due to raw material cost surges and imported input tariffs, illustrating how input cost dynamics can rapidly increase finished equipment pricing pressures beyond initial capital costs. Large industrial manufacturers also continue to navigate elevated producer prices in early 2026, with official data showing rising upstream service and supply chain costs that ripple through logistics and distribution channels. These trends emphasize that capital outlays alone are not the only cost burden; operational and supply chain inflation can further amplify total ownership costs, reinforcing restraint on equipment procurement decisions.

Commodity Price Volatility and Supply Chain Instability

The supply chain of grinding mills is sensitive to fluctuations in raw material prices for steel, alloys, and specialized wear components. Commodity price volatility increases manufacturing costs, which are often passed to end customers or erode manufacturer margins. Furthermore, geopolitical tensions and logistics constraints can disrupt supply chains, delaying deliveries, straining inventories, and reducing planned capital expenditure in grinding equipment procurement cycles. These structural challenges can compress demand in the near term and create variability in forecast growth trajectories.

In early 2026, container shipping surcharges were introduced by major carriers in response to regional geopolitical tensions, effectively doubling freight costs on key routes, a shift that complicates planning for heavy equipment imports and export logistics. Separately, the 2026 Strait of Hormuz crisis has disrupted maritime traffic through a critical global energy and cargo chokepoint, forcing re-routing and longer transit times that raise international transport costs and delivery unpredictability. These developments illustrate how external geopolitical shocks and logistics bottlenecks continue to affect industrial supply chains, escalating raw material and transportation costs and reinforcing volatility that restrains procurement activity and investment decisions.

Modernization of Aging Infrastructure and Technological Upgrades

Many aging industrial plants in mining, cement, and chemical sectors continue operating older grinding mills with sub-optimal energy performance and limited automation. This presents significant replacement and modernization opportunities. Transitioning to next-generation milling solutions, including high pressure rollers and digitally integrated systems, can deliver energy savings and throughput improvements. Modern systems also support predictive maintenance, real-time diagnostics, and improved operational safety. As energy costs rise and environmental compliance becomes more stringent, these upgrades can improve competitiveness and extend plant lifecycles.

Government and industry trends in early 2026 further reinforce this opportunity. For example, China’s Ministry of Industry and Information Technology highlighted industrial upgrading and cultivation of future industries as a key priority for 2026, emphasizing smart factory transformation, advanced materials, and intelligent manufacturing, developments that align with modernization of industrial process equipment. Similarly, Canada announced a US$ 165.2 million investment to accelerate planning, development, and processing in critical minerals projects, including infrastructure upgrades that will require modern grinding and processing equipment. These developments underscore broad policy support for industrial renewal and deeper application of advanced technologies across key sectors.

Diversification into Emerging Economies and Precision Industrial Applications

Emerging markets in Latin America, Africa, and parts of Southeast Asia remain under-penetrated relative to North America and Europe. Growth in infrastructure construction, mining operations, and power generation capacity in these regions supports rising demand for grinding mills. Increasing foreign direct investments and private capital flows into industrial expansion also create favorable conditions for market growth. This is supported by recent investment trends indicating a surge in private credit into emerging markets infrastructure projects, with significant funding directed toward energy, digital networks, and processing facilities. As new plants and upgrades proceed, demand for scalable, cost-effective grinding solutions is expected to rise steadily.

The demand for precision milling in food processing, pharmaceuticals, and specialty chemicals presents a strong adjacent growth opportunity. In February 2026, the Ministry of Food Processing Industries reaffirmed infrastructure expansion and incentive support under national food processing schemes, accelerating investments in integrated processing clusters that require hygienic and high-precision grinding systems. Similarly, in early 2026, the Department of Pharmaceuticals continued advancing production-linked incentive programs and bulk drug park development to strengthen domestic active pharmaceutical ingredient (API) manufacturing. Advanced drug production depends on micron-level particle size control and contamination-free milling environments. These policy-backed expansions directly support demand for fine and ultra-fine grinding technologies beyond traditional heavy industrial applications.

Category-wise Analysis

Mill Type Insights

Ball mills are likely to command an estimated 52% share of industry installations in 2026 due to their broad applicability across primary crushing and fine grinding circuits in mining, cement, and heavy process industries. Their versatility allows use in both wet and dry configurations with diverse feed materials, supporting broad operational deployment. Recent project activity demonstrates ongoing demand: in late 2025, the Artemis Gold Blackwater mine placed orders for both a large SAG mill and an 18 MW ball mill as part of its Phase 2 expansion, underlining continued capital investment in ball mill–based grinding circuits at large mining operations. Enhanced digital monitoring and automated feedback loops help reduce downtime and improve performance consistency across complex ore feeds. This balance of robust performance and adaptability sustains ball mills as the backbone of large-scale grinding infrastructure globally.

Vertical mills are projected to represent the fastest growing segment, slated to grow at approximately 6.8% CAGR through 2033 as operations seek better energy efficiency and process integration. In 2025, stirredmills such as Metso’s Vertimill® recorded record sales, with units delivering up to ~35 % energy savings compared to conventional ball mills and expanded adoption into secondary and tertiary grinding applications in mining. Additionally, vertical roller mills are being ordered widely for new plants: for example, multiple vertical roller mill orders were placed by cement producers in India and Iraq through 2025, with commissioning planned by end-2026. These mill types offer compact footprints, reduced power consumption, and automation-ready controls, contributing to their rapid adoption and reinforcing their position as innovation drivers in mill type segmentation.

End-User Insights

Mining companies are poised to hold around 58% of the grinding mill market revenue share in 2026. Large-scale ore processing operations require robust milling systems capable of high-capacity throughput and durability. The scale of mineral beneficiation and concentration processes supports both base equipment sales and ongoing aftermarket revenue through wear parts and maintenance. For example, in April 2025, Metso was awarded a major grinding equipment order for a greenfield iron ore processing plant in Odisha, India, underscoring continued capital investments in mining grinding infrastructure.

Food and pharmaceutical industries are projected to be the fastest-growing end-use segment, advancing at a CAGR of about 7.5% through 2033. These sectors demand precise particle size control to meet stringent product quality and regulatory standards. Regulatory requirements for hygiene, contamination control, and uniformity are accelerating the adoption of specialized fine and ultra-fine grinding equipment, such as jet mills and advanced bead mills, particularly for pharmaceutical powder production and certain food ingredients. While specific installations are less frequently reported in global industry news, broader ultra-fine grinding market analyses highlight increasing mill demand from pharmaceutical and related chemical processing segments, driven by rising demand for finer particle sizes and bioavailability enhancements

Regional Insights

North America Grinding Mill Market Trends

North America represents a technologically advanced and investment-stable market for grinding mills, supported by a diversified industrial base. The United States continues to anchor regional performance due to its extensive mining infrastructure and strong cement manufacturing capacity. In January 2026, Eagle Materials Inc. announced modernization investments at its Texas cement plant, including efficiency upgrades to grinding systems to improve throughput and reduce energy intensity. Such upgrades reflect the region’s emphasis on operational optimization rather than capacity overexpansion. Strong aftermarket networks and digital monitoring integration further enhance lifecycle service revenues. These factors collectively sustain North America’s strategic importance in the global grinding mill ecosystem.

The region is projected to expand with a steady industrial output and modernization spending. Regulatory alignment with the U.S. Environmental Protection Agency (EPA) continues to encourage deployment of energy-efficient milling technologies. In 2025, several U.S.-based cement producers accelerated plant retrofits to comply with tightening emissions and efficiency standards, reinforcing demand for upgraded grinding systems. Industrial automation penetration remains high, with predictive maintenance solutions gaining traction. Competitive positioning centers on technological enhancement and service contracts. North America therefore maintains stable, innovation-driven growth within a mature industrial framework.

Europe Grinding Mill Market Trends

Europe maintains a strong engineering-led grinding mill market shaped by sustainability and regulatory harmonization. Major industrial economies such as Germany, France, Spain, and the United Kingdom continue to modernize cement and specialty chemical processing facilities. In March 2025, Heidelberg Materials announced efficiency upgrades across multiple European cement plants, focusing on reducing clinker factor and improving grinding efficiency. These investments directly support advanced vertical and energy-optimized grinding technologies. The region prioritizes performance enhancement, emissions reduction, and digital system integration. Strong OEM presence reinforces Europe’s role as a technology hub.

Europe is expected to grow supported by sustainability mandates under the European Commission (EC). The European Union (EU) Green Deal framework continues to push industrial decarbonization, encouraging replacement of conventional grinding equipment with energy-efficient alternatives. In 2026, multiple cement producers reported integration of automated mill control systems to improve power consumption metrics. Competitive differentiation emphasizes engineering quality and environmental compliance. Investment patterns remain steady, centered on modernization rather than aggressive greenfield expansion. Europe thus reflects measured growth aligned with long-term sustainability objectives.

Asia Pacific Grinding Mill Market Trends

Asia Pacific is projected to be both the leading and fastest-growing regional market, expected to account for approximately 35% of global revenue share in 2026 and expand at a CAGR of about 5.5% through 2033. Rapid infrastructure development and mineral extraction activities across China, India, and Southeast Asia underpin strong demand for high-capacity grinding mills. In February 2026, UltraTech Cement announced capacity expansion projects across India, including new grinding units to support regional cement demand growth. Large-scale mining investments in Australia and Indonesia further stimulate mill procurement. These developments reinforce the dominant position of Asia Pacific in global installation volumes.

The region benefits from cost-competitive manufacturing ecosystems and strong domestic equipment production capabilities, which support both local demand and export opportunities. In mid-2025, a major vertical roller mill contract executed by Chinese contractor CBMI in Ivory Coast further illustrates the extension of Asia Pacific engineering influence into adjacent markets, with mill commissioning planned for 2026. Policy initiatives promoting domestic production and energy efficiency accelerate upgrades to grinding systems in new and existing plants. Automation and smart control integration rise steadily in new installations, strengthening operational performance. Global original equipment manufacturers (OEMs) are expanding regional service hubs to capture aftermarket growth, while local manufacturers compete on cost and customization.

Competitive Landscape

The global grinding mills market structure is moderately consolidated, with leading vendors such as Metso, FLSmidth, thyssenkrupp AG, and CITIC Heavy Industries accounting for a substantial portion of global revenue. These companies leverage strong relationships with mining and cement producers and offer integrated engineering, procurement, and construction (EPC) and aftermarket capabilities. Their competitive edge lies in delivering high-capacity, energy-efficient grinding systems supported by digital monitoring solutions. Continuous R&D investment strengthens advancements in wear-resistant materials and process optimization technologies. Extensive global service networks further reinforce long-term customer retention and recurring revenue streams.

Regional and specialized players such as Gebr. Pfeiffer, Loesche GmbH, and NETZSCH Group focus on niche applications including vertical roller mills and fine grinding systems. High capital intensity and complex plant integration requirements create strong barriers to entry. However, rising digitalization is enabling collaboration with software providers offering predictive maintenance and smart control platforms. OEMs increasingly pursue strategic partnerships and geographic expansion to strengthen their competitive footprint. Gradual consolidation is anticipated as technology integration becomes central to long-term differentiation.

Key Industry Developments

- In March 2026, Metso and Loesche partnered to launch a vertical roller mill (VRM) dry grinding solution for mineral processing applications. The technology combines Loesche’s proven VRM system with Metso’s mineral processing expertise to improve efficiency and simplify process flows.

- In February 2026, Navoi Mining & Metallurgical Company (NMMC) commissioned Grinding Mill No. 8 at Hydrometallurgical Plant No. 3 as part of the Kokpatas and Daugyztau gold deposit expansion project. The new mill can process 700,000 tons of gold-bearing ore annually, supporting the company’s plan to raise total ore processing capacity from over 10 million tons to 10.8 million tons.

- In July 2025, UltraTech Cement commissioned its second cement grinding mill at the Maihar unit in Madhya Pradesh, adding 1.8 million tons per annum (MTPA) to production capacity. The expansion raises the company’s domestic grey cement capacity to 186.86 MTPA and global capacity to about 192 MTPA, strengthening its ability to meet rising construction demand.

Companies Covered in Grinding Mill Market

- Metso Outotec

- FLSmidth & Co. A/S

- thyssenkrupp AG

- CITIC Heavy Industries

- Gebr. Pfeiffer SE

- KHD Humboldt Wedag

- NETZSCH Group

- Retsch GmbH

- Loesche GmbH

- Eirich Group

Frequently Asked Questions

The global grinding mills market is projected to reach US$ 15.8 billion in 2026.

Rising mining output, cement capacity expansion, and growing adoption of energy-efficient automated milling technologies are driving market growth

The market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Opportunities lie in modernization of aging grinding infrastructure, expansion in emerging mining economies, and adoption of digital mill control systems.

Metso, FLSmidth, thyssenkrupp AG, and CITIC Heavy Industries are among the leading global players in the market.