- Medical Devices

- Glucose Analysis Tubes Market

Glucose Analysis Tubes Market Size, Share, and Growth Forecast 2026 - 2033

Glucose Analysis Tubes Market by Product (Sodium Fluoride Tubes, Potassium Fluoride Tubes, Fluoride Oxalate Tubes, Others), by Form Factor (Plastic Tubes (PET), Glass Tubes), by End User (Hospitals & Clinics, Diagnostic Laboratories, Research & Academic Institutes, Others), by Regional Analysis, 2026-2033

Glucose Analysis Tubes Market Size

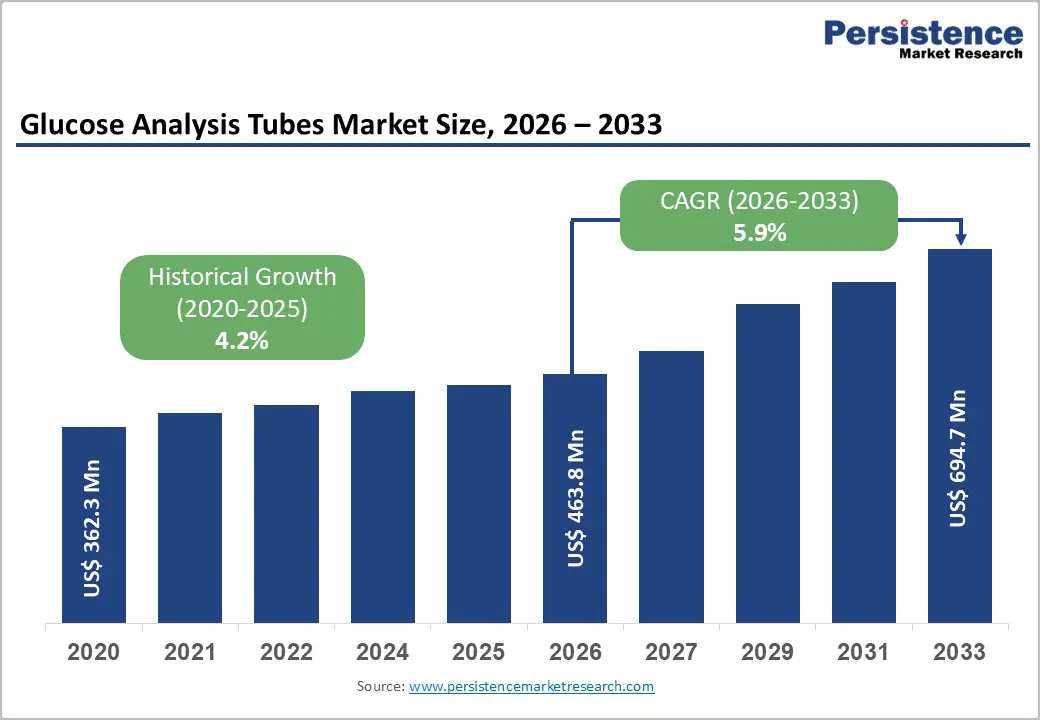

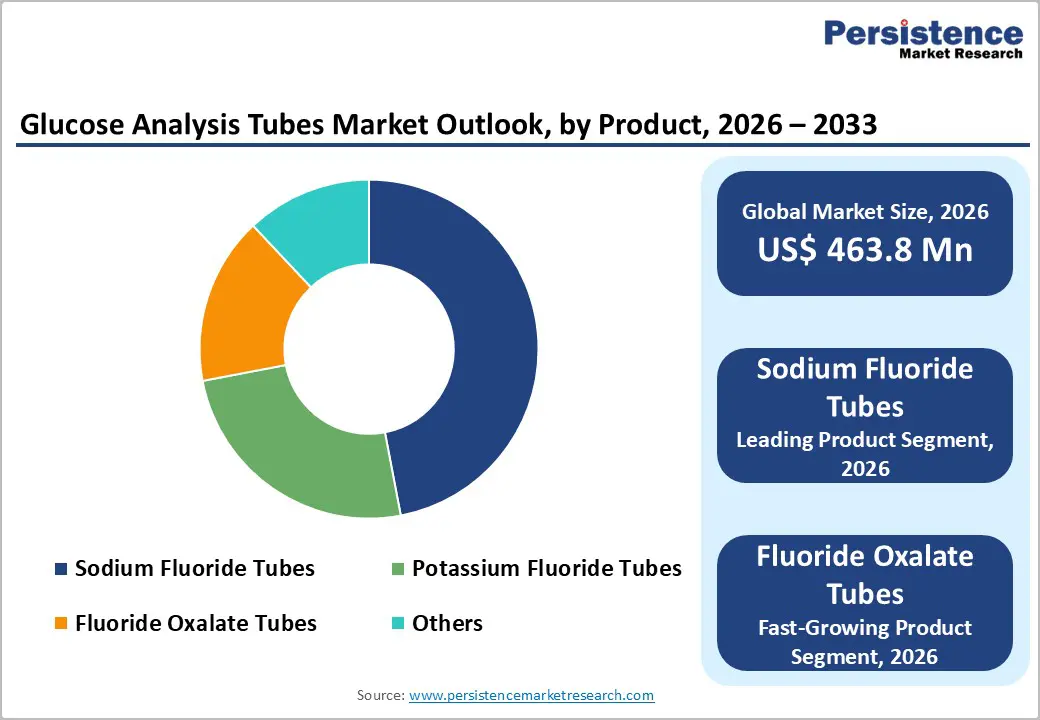

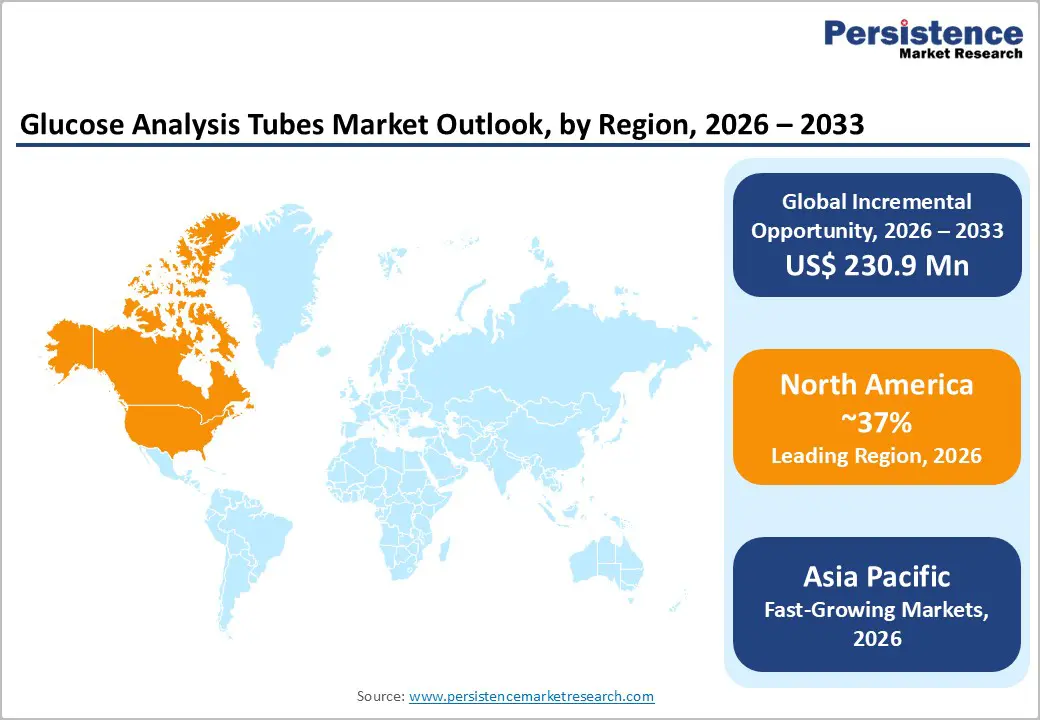

The global Glucose Analysis Tubes Market size is expected to be valued at US$ 463.8 million in 2026 and projected to reach US$ 694.7 million by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

Rising prevalence of diabetes and advancements in diagnostic technologies drive this growth. World Health Organization reports over 422 million diabetes cases worldwide, necessitating frequent glucose testing that relies on stable sample preservation in specialized tubes. Enhanced tube formulations inhibit glycolysis effectively, supporting accurate results in high-volume labs amid increasing chronic disease burdens.

Key Market Highlights

- North America commands 37% share in 2025, driven by U.S. leadership in diagnostics and regulatory excellence.?

- Asia Pacific emerges fastest-growing, propelled by diabetes surge in China and India.?

- Sodium Fluoride Tubes dominate products at 47% share for glycolysis inhibition efficacy.?

- Fluoride Oxalate Tubes grow fastest, offering enhanced stability for research.?

- Emerging markets expansion unlocks revenue via infrastructure investments.?

| Key Insights | Details |

|---|---|

|

Glucose Analysis Tubes Size (2026E) |

US$ 463.8 million |

|

Market Value Forecast (2033F) |

US$ 694.7 million |

|

Projected Growth CAGR(2026-2033) |

5.9% |

|

Historical Market Growth (2020-2025) |

4.2% |

Market Dynamics

Market Drivers: Rising Diabetes Prevalence

The global surge in diabetes cases is a primary driver fueling demand for glucose analysis tubes. According to the International Diabetes Federation, approximately 537 million adults were living with diabetes in 2021, and this number is projected to escalate to 783 million by 2045. This dramatic rise necessitates frequent blood glucose monitoring for early detection, diagnosis, and management of diabetes, creating sustained demand for reliable blood collection tools. Glucose analysis tubes, particularly those containing glycolysis inhibitors such as sodium fluoride, maintain sample stability for 24–48 hours, ensuring accurate glucose readings even in resource-limited or remote testing environments. The adoption of these tubes is further reinforced as healthcare systems increasingly emphasize preventive care and routine screening programs. In both hospital and diagnostic laboratory settings, the ability to preserve sample integrity over extended periods enhances efficiency and reliability, driving the expansion of the glucose analysis tubes market globally.

Advancements in Tube Technology

Technological innovations in glucose analysis tubes are significantly influencing market growth. Improvements in tube additives, such as enhanced fluoride formulations, and the development of materials that improve sample stability, are increasing the adoption of these products in clinical and research settings. Studies indicate that sodium fluoride tubes can maintain glucose stability more effectively than traditional serum tubes over extended periods, minimizing errors in laboratory testing. Moreover, these tubes are increasingly designed to be compatible with automated laboratory systems, which streamline workflows in high-throughput environments and reduce human error. Additional functionalities, such as simultaneous lactate and hemoglobin measurement, expand their clinical utility. The ongoing research into RNA and metabolite stabilization further enhances the versatility of glucose analysis tubes, making them a valuable tool not only for routine diagnostic monitoring but also for advanced metabolic and biopharmaceutical studies. Such innovations continue to boost the market by aligning product performance with evolving laboratory requirements.

Regulatory Compliance Challenges

The glucose analysis tubes market faces significant restraints from stringent regulatory frameworks. Regulatory authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) enforce strict compliance requirements, including ISO 13485 certification and biocompatibility testing, which can delay product approvals and increase operational costs. Smaller manufacturers often struggle with these compliance obligations due to limited resources, creating barriers to entry and limiting innovation in the market. Non-compliance carries substantial risks, including fines and product recalls, which further discourage new entrants. Moreover, differing regulatory standards across countries complicate global expansion strategies, as manufacturers must navigate multiple frameworks to ensure approval. This regulatory complexity increases time-to-market and constrains the introduction of advanced tubes with novel additives. Collectively, these compliance challenges pose a substantial restraint on market growth, especially for smaller players attempting to compete with established multinational manufacturers.

Supply Chain Vulnerabilities

Supply chain disruptions present another notable restraint to the glucose analysis tubes market. The production of these tubes depends heavily on the availability of specialized raw materials, such as fluoride compounds and anticoagulants, which are sourced from a limited number of suppliers worldwide. Global events, including geopolitical tensions, natural disasters, or logistic challenges, can disrupt supply chains, leading to shortages in hospitals and diagnostic laboratories. These interruptions increase production costs and limit product availability, particularly in emerging markets where local manufacturing capacity is often insufficient. Additionally, dependency on specialized components slows the ability of manufacturers to scale production in response to rising demand, which can hamper market expansion. Maintaining a consistent supply of high-quality additives is critical for preserving sample integrity, and any disruption directly affects the reliability of glucose measurements. Consequently, supply chain vulnerabilities act as a key market restraint by impacting both cost efficiency and accessibility of glucose analysis tubes.

Expansion in Emerging Markets

Emerging markets, particularly in Asia Pacific, represent a significant growth opportunity for glucose analysis tubes. Countries like China and India are witnessing rapid improvements in healthcare infrastructure, coupled with a growing burden of diabetes among their populations. The rising prevalence of diabetes has increased demand for routine blood glucose testing, driving adoption of stable and reliable tubes such as sodium fluoride and fluoride oxalate variants. Local manufacturing capabilities in these regions help reduce production and distribution costs, making tubes more accessible for hospitals, diagnostic labs, and point-of-care facilities. Investments in modern diagnostic laboratories, government health initiatives, and private healthcare expansion further support market growth. Fluoride oxalate tubes, in particular, are gaining traction due to their superior sample stabilization properties, aligning with the rising need for accurate glucose monitoring. The convergence of improved healthcare infrastructure and cost-effective production presents high CAGR potential for glucose analysis tubes in these emerging economies.

Rising Research Applications

Beyond routine clinical use, glucose analysis tubes are increasingly applied in research and academic settings, creating new market opportunities. These tubes allow long-term preservation of blood samples, enabling studies related to metabolic disorders, diabetes, and other chronic conditions. The rise in biopharmaceutical and clinical research trials has amplified the demand for tubes that can reliably stabilize glucose and related analytes, such as lactate or hemoglobin. Innovative tube variants that support RNA stabilization and metabolite preservation further extend their utility for molecular biology and translational research applications. Academic institutions and research laboratories benefit from these products for longitudinal studies, epidemiological research, and pharmacokinetic analyses. The increasing emphasis on precision medicine and personalized treatment approaches also necessitates high-quality, stable sample collection, reinforcing the demand for advanced glucose analysis tubes. Consequently, the expanding scope of research applications serves as a strong growth driver for the market, complementing routine diagnostic demand.

Category-wise Insights

Product Analysis

Sodium fluoride tubes dominate the glucose analysis tubes market, capturing approximately 47% share in 2025. Their widespread adoption is largely due to their ability to inhibit glycolysis effectively, maintaining glucose stability for 24–48 hours. This ensures highly accurate test results, even when samples experience delays before analysis, a crucial factor for large diagnostic laboratories and hospital settings. Clinical studies have consistently demonstrated that sodium fluoride tubes outperform traditional serum tubes in preserving glucose integrity, making them the preferred choice for fasting glucose tests, oral glucose tolerance assessments, and routine monitoring. Hospitals and diagnostic centers favor these tubes because they reduce measurement errors, enhance reliability, and integrate smoothly with automated laboratory workflows. The combination of proven accuracy, extended sample stability, and compatibility with modern lab systems reinforces their leading position in the market.

End User Analysis

Hospitals and clinics represent the largest end-user segment of the glucose analysis tubes market, accounting for over 50% share in 2025. This dominance is driven by high patient volumes requiring rapid and precise blood glucose testing for both routine and specialized care. For instance, in the U.S., the Centers for Disease Control and Prevention (CDC) reports more than 38 million adults diagnosed with diabetes, underscoring the continuous need for glucose monitoring. Hospitals increasingly rely on tubes compatible with point-of-care testing systems to streamline workflows and ensure timely results for physicians and patients. Integrated laboratory setups, combined with high-throughput testing demands, make hospitals a critical consumer of sodium fluoride and other glucose-stabilizing tubes. As healthcare systems emphasize preventive care and chronic disease management, hospitals’ central role in driving demand for reliable, efficient glucose analysis solutions remains firmly established.

Regional Insights

North America Glucose Analysis Tubes Market Trends

North America, led by the United States, remains the largest market for glucose analysis tubes, accounting for around 37% of the regional share in 2025. This dominance is supported by a highly advanced healthcare ecosystem, a strong culture of medical research, and stringent regulatory oversight by the FDA, which ensures high-quality production and safety standards. Significant investments in R&D are focused on next-generation tubes compatible with continuous glucose monitoring systems and automated laboratory workflows, improving efficiency and reducing testing errors. High diabetes prevalence in the U.S., with over 38 million adults affected as per CDC data, drives strong demand in hospitals and diagnostic laboratories. Additionally, mature laboratory infrastructure, widespread adoption of point-of-care testing, and an emphasis on preventive healthcare initiatives further strengthen the region’s leading position in the global glucose analysis tubes market.

Asia Pacific Glucose Analysis Tubes Market Trends

The Asia Pacific region is experiencing rapid growth in the glucose analysis tubes market, primarily driven by China and India. Rising diabetes prevalence in these countries, coupled with expanding healthcare infrastructure, has significantly increased the need for accurate, stable, and cost-effective blood glucose testing solutions. Local manufacturing capabilities enable lower production costs, making tubes such as sodium fluoride and fluoride oxalate more accessible to hospitals, diagnostic laboratories, and research facilities. Japan contributes advanced technological expertise, particularly in automated and high-throughput laboratory systems, enhancing efficiency and reliability in glucose testing. ASEAN countries benefit from affordable manufacturing, growing hospital networks, and increased awareness of diabetes management. Overall, improvements in healthcare access, government initiatives for preventive care, and rising adoption of modern diagnostic systems make Asia Pacific the fastest-growing regional market for glucose analysis tubes.

Competitive Landscape

Market Structure Analysis

The market remains moderately consolidated, led by established players focusing on R&D for additives and safety features. Leaders employ expansion via local manufacturing and partnerships for emerging regions. Key differentiators include automation compatibility and eco-friendly materials. Emerging models emphasize sustainable, recyclable tubes amid regulatory pressures.

Key Market Developments

- In May 2024, Nova Biomedical announced that the U.S. Food and Drug Administration (FDA) had granted 510(k) clearance for a micro capillary sample mode on the Stat Profile Prime Plus® Critical Care analyzer. The Prime Plus was then able to perform an 11-test panel, including pH, PCO2, PO2, Na, K, iCa, iMg, Cl, glucose, lactate, and hematocrit, using just 90 microliters of capillary blood, or a complete 22-test profile with only 135 microliters of blood.?

Companies Covered in Glucose Analysis Tubes Market

- Becton, Dickinson and Company

- Greiner Bio-One International GmbH

- Guangzhou Improve Medical Instruments Co. Ltd

- AB Medical Inc.

- SARSTEDT AG & Co. KG

- InterVac Technology

- Cardinal Health, Inc.

- Poly Medicure Ltd.

- FL Medical

- Chengdu Rich Science Industry Co., Ltd.

- Sekisui Medical Co., Ltd.

- APTACA S.p.A.

Frequently Asked Questions

The market is expected to reach US$ 463.8 million in 2026.

Rising diabetes prevalence, with over 500 million cases globally, necessitates reliable glucose preservation.

North America holds 37% share in 2025, led by U.S. innovation.

Expansion in Asia Pacific via manufacturing and research demand.

Leaders include Becton, Dickinson and Company, Greiner Bio-One, and SARSTEDT AG & Co. KG.