- Advanced Materials

- Geocells Market

Geocells Market Size, Share, and Growth Forecast, 2026 - 2033

Geocells Market by Material Type (High-Density Polyethylene (HDPE), Polypropylene (PP), Low-Density Polyethylene (LDPE), Polyvinyl Chloride (PVC), and others such as polyester and composite polymers.), Design (Perforated Geocells, Non-Perforated Geocells), Application (Load Support & Soil Reinforcement, Channel & Slope Protection, Retaining Walls & Earth Retention, Road Base & Pavement Reinforcement, Landfills & Waste Containment, and Others) Industry and Regional Analysis for 2026 - 2033

Geocells Market Size and Trends Analysis

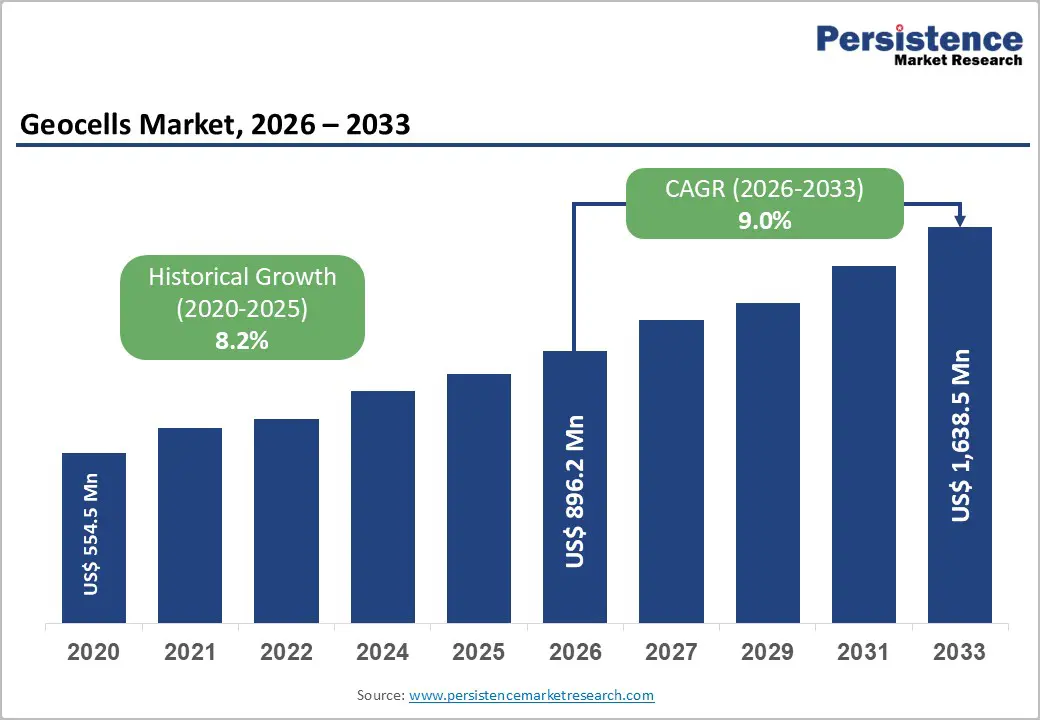

The global geocells market size is likely to be valued at US$ 896.2 million in 2026 and is projected to reach US$ 1,638.5 million by 2033, growing at a CAGR of 9.0% between 2026 and 2033.

This accelerated expansion reflects fundamental infrastructure imperatives across developed and emerging economies, where geocells three-dimensional cellular confinement systems, manufactured from high-strength polymers, address critical ground stabilization, erosion control, and load distribution requirements in transportation, environmental protection, and construction sectors.

Market growth is propelled by the convergence of macroeconomic factors, including rising public infrastructure investments in North America, Europe, and East Asia, regulatory emphasis on sustainable and resource-efficient construction, and the demonstrated cost advantages of geocell solutions over traditional soil stabilization methods. Technological advancements in polymer materials, optimized installation techniques, and environmental product declarations that validate lifecycle sustainability further reinforce market growth, enabling the sector to maintain strong double-digit expansion despite commodity price fluctuations and evolving regulations governing geosynthetic materials.

Key Industry Highlights:

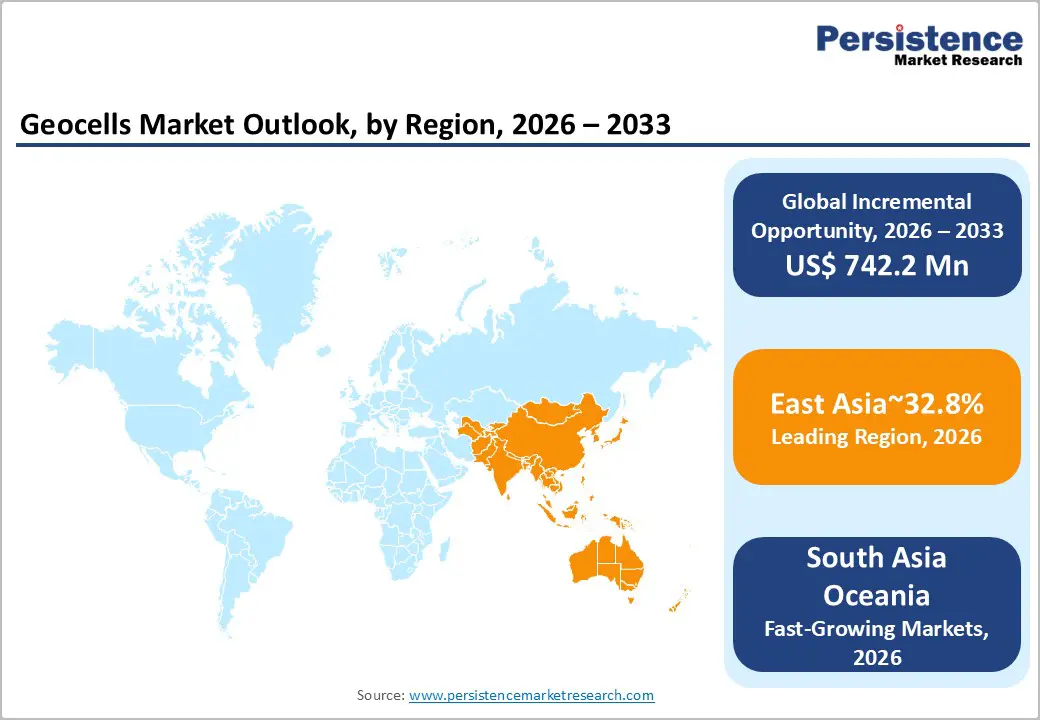

- Regional Leadership: East Asia dominates the global geocells market with 32.8% share, driven by large-scale highway and railway expansion in China and India, supported by sustained public infrastructure spending.

- North America Market Scenario: North America accounts for 21.4% of the market share, underpinned by extensive highway rehabilitation programs, advanced engineering standards, and a growing emphasis on lifecycle cost reduction.

- Europe Market Scenario: Europe holds 18.7% share, supported by dense transportation networks, stringent environmental regulations, and strong adoption of sustainable ground-stabilization solutions.

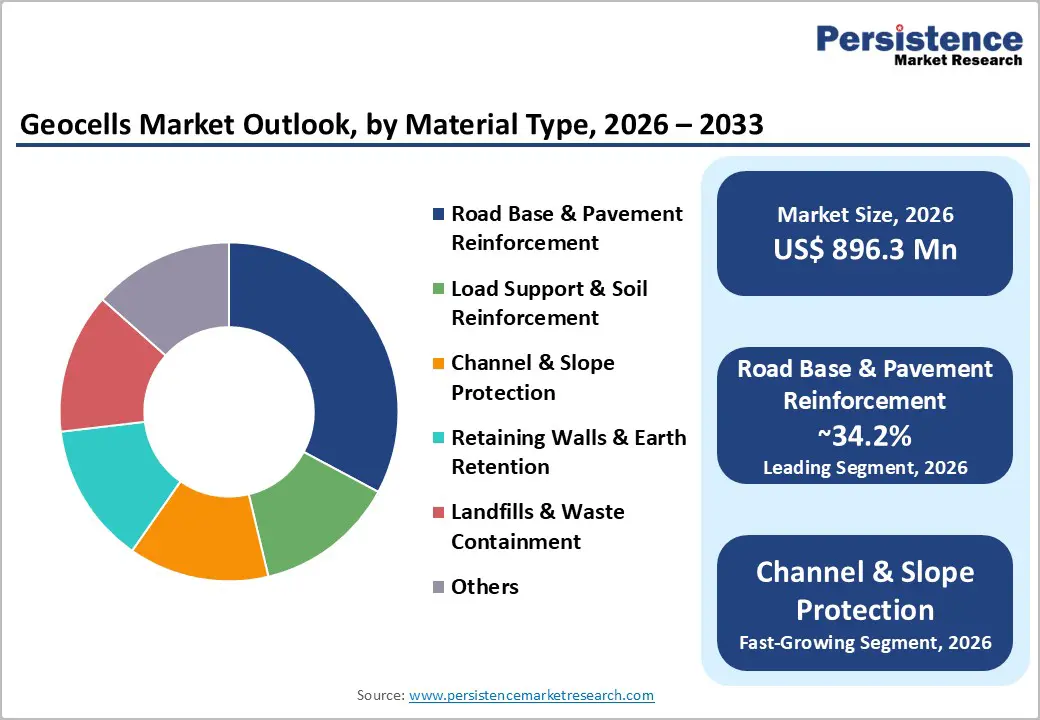

- Leading Application: Road Base & Pavement Reinforcement commands 34.2% market share, reflecting its critical role in subgrade stabilization, load distribution, and long-term pavement durability.

- Fastest-Growing Application: Channel & Slope Protection is expanding most rapidly, driven by climate-induced erosion risks, extreme rainfall events, and rising investment in resilient and nature-based infrastructure solutions.

| Key Insights | Details |

|---|---|

| Geocells Market Size (2026E) | US$ 896.3 Mn |

| Market Value Forecast (2033F) | US$ 1, 638.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 9.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

Market Dynamics

Drivers - Infrastructure Expansion and Transportation Network Development

Global infrastructure investment acceleration constitutes the primary driver of the geocells market, particularly through transportation network modernization across emerging economies and developed market maintenance cycles. India has undertaken transformative infrastructure expansion through PM GatiShakti, Bharatmala, and Sagarmala initiatives, expanding national highways by 60 percent to 146,204 kilometers and accelerating highway construction pace from 11.6 kilometers per day to 34 kilometers per day, with landmark projects including the Delhi-Mumbai Expressway and Atal Tunnel significantly reducing travel times and requiring ground stabilization across diverse geological conditions.

The United States maintains an extensive highway network spanning 4.19 million miles, supported by 340 million residents across 132.7 million households, and requires continuous pavement reinforcement, embankment stabilization, and slope protection investments that use geocell technology to enhance durability and extend maintenance intervals.

China's road network expansion to 6.49 million kilometers by August 2025, representing growth from 5.2 million kilometers in 2020, supports 440 million vehicle owners across a 1.41 billion population and creates sustained demand for soil reinforcement solutions across challenging terrain and high-traffic corridors, where geocells enhance load distribution capacity and reduce rutting in weak subgrades.

European motorway density, concentrated around capitals and economic hubs, with regions such as Utrecht (132 km/1,000 km²) and Berlin's railway network (764 km/1,000 km²) demonstrating infrastructure intensity, generates recurring demand for erosion control, slope protection, and pavement reinforcement applications, supported by geocell deployment in soil stabilization strategies.

Sustainable Construction Transition and Environmental Regulatory Mandates

Regulatory frameworks that prioritize resource efficiency and carbon footprint reduction drive material composition and design innovation in the geocells market, particularly through lifecycle assessment requirements and environmental product declaration frameworks. Presto Geosystems' publication of the industry's first Environmental Product Declaration for GEOWEB® geocells in April 2025 exemplifies a transparent environmental impact assessment that integrates quantification of carbon footprint, energy consumption, and resource use, enabling engineers, architects, and project owners to align material selection with green building objectives and sustainability certifications.

The circular economy imperative, reflected in European Union waste management policies, where global municipal solid waste generation is expected to rise from 2.1 billion tonnes in 2023 to 3.8 billion tonnes by 2050, creates regulatory pressure for sustainable foundation solutions: adopting effective waste prevention and circular economy models could yield net annual gains of US$ 108.5 billion by 2050 compared to business-as-usual scenarios.

European construction waste statistics demonstrate the scale of this imperative that is construction activities generated 38.4 percent of total EU waste in 2022, which is around 2,233 million tonnes, necessitating resource-efficient ground stabilization solutions that minimize excavation, reduce aggregate consumption, and enable the use of locally available infill materials that reduce transportation-related carbon emissions.

Polymeric material composition evolution reflects sustainability imperatives: the dominance of HDPE benefits from chemical resistance and established manufacturing efficiency, whereas the emergence of polypropylene as the fastest-growing segment reflects specialized applications, chemical resistance advantages, and bio-based polymer development trajectories that support reduced-carbon material alternatives.

Restraint - Installation Complexity and Technical Specification Knowledge Barriers

Geocell installation requires specialized expertise, site-specific design optimization, and proper compaction procedures that pose knowledge barriers, particularly for smaller contractors and developing market construction firms with limited prior geosynthetic experience. Improper installation, including inadequate infill material compaction, insufficient cellular confinement, or suboptimal drainage design,n can substantially underperform theoretical structural capabilities, create client perception barriers and limit adoption among price-sensitive, risk-averse contractor segments despite cost-effectiveness benefits.

Specification complexity, with design variables including cell height, material type (HDPE vs. polypropylene), perforation patterns (perforated vs. non-perforated), and infill material characteristics requiring engineering calculations and site evaluation, creates barriers for small- and medium-scale contractors unfamiliar with geosynthetic engineering principles, limiting market penetration in developing economies where construction sector sophistication varies substantially across project types and contractor capabilities.

Opportunity - Railway Infrastructure Modernization and Ballast Reinforcement Systems

Railway infrastructure expansion and modernization programs across Asia, particularly India's 45,000 route-kilometer electrification initiative and high-speed rail corridor development, create specialized opportunities for geocell ballast reinforcement applications that address settlement reduction, enhance track stability, and reduce maintenance costs on weak subgrades and in challenging terrain. Presto Geosystems' laboratory testing and Finite Element modeling demonstrated that geocell confinement reduces ballast settlement by up to 50 percent on weak subgrades while decreasing subgrade interface pressure and improving ballast resiliency under heavy freight loads, positioning geocells as superior alternatives to conventional ballast reinforcement methodologies like geogrids and asphalt.

Railway applications generate premium pricing opportunities through specialized design requirements, performance verification testing, and engineering consultation services that command higher margins than commodity road construction applications. Market penetration of railway ballast reinforcement remains nascent in many developing economies, creating substantial untapped demand, as rail authorities prioritize infrastructure durability, maintenance cost reduction, and track stability enhancement through advanced geosynthetic solutions.

Strata Geosystems' deployment of StrataWeb® geocells in railway transition slabs across India exemplifies this application specialization, demonstrating cost-effective, sustainable alternatives to conventional concrete or gravity walls while reducing differential settlement and long-term maintenance requirements, which are particularly valuable in high-speed rail corridors and mountainous terrain, where maintenance access complexity amplifies operational costs.

Coastal Protection and Climate Resilience Infrastructure

Rising sea levels, increasing frequency of extreme weather events, and growing recognition of the requirements for climate-resilient infrastructure create emerging market opportunities for geocells in coastal erosion control, embankment stabilization, and nature-based engineering solutions that address geomorphological threats to critical infrastructure and populated areas. Geocell-based coastal protection systems offer biodegradable alternatives to conventional reinforced concrete structures, enabling vegetation establishment and supporting ecosystem services while providing structural stability.

The Geocells Market expansion into climate resilience infrastructure addresses dual imperatives: physical protection of coastal communities and infrastructure assets against storm surge and erosion, combined with ecosystem restoration and nature-based engineering principles supporting biodiversity and environmental sustainability goals aligned with United Nations climate action frameworks and national adaptation strategies.

Government investment in climate adaptation infrastructure, particularly in island nations, deltaic regions, and coastal developing economies vulnerable to climate impacts, generates institutional demand for cost-effective, environmentally sustainable ground-stabilization solutions that support resilient infrastructure development.

Emerging market government programs prioritizing natural disaster mitigation, including landslide prevention, embankment stability, and flood-prone infrastructure protection, create demand for geocell-based slope stabilization and retaining wall solutions that reduce construction costs, minimize environmental impact, and provide long-term durability under extreme climatic stress conditions characteristic of monsoon zones, tropical storm-prone regions, and seismically active areas.

Category-wise Analysis

Material Type Insights

High-density polyethylene geocells hold the dominant market position in the global geocells market, accounting for 68.5% in 2026, reflecting proven durability, established manufacturing processes, and broad compatibility across diverse soil and climate conditions. HDPE geocells demonstrate superior chemical resistance, ultraviolet protection, and environmental stress crack resistance exceeding 5,000 hours, enabling multi-decade service life in harsh conditions ranging from high-temperature desert environments to freeze-thaw cycles characteristic of temperate climate zones.

The material's cost-effectiveness, combined with established supply chains, global manufacturing infrastructure, and proven performance record across transportation, environmental, and civil engineering applications, creates customer preference for HDPE specifications in standardized applications, including road pavement reinforcement, embankment stabilization, and landfill protection systems.

The HDPE segment's market leadership reflects structural advantages, including chemical durability enabling landfill geomembrane applications and waste containment environments incompatible with alternative materials, combined with cost positioning that maintains competitiveness in price-sensitive emerging market infrastructure projects where project economics fundamentally depend on material cost optimization without performance compromise.

Polypropylene geocells are the fastest-growing material category in the global market, driven by specialized applications requiring enhanced chemical resistance, superior performance in aggressive geochemical environments, and thermal properties that enable deployment in high-temperature industrial and energy-sector applications.

Design Insights

Perforated geocells maintain market leadership at 57.8% share in 2026, reflecting engineering advantages in drainage facilitation, pore-water pressure dissipation, and applications requiring free-draining systems integrated with vegetated slope protection and environmental restoration requirements. Perforation design enables pore-water pressure redistribution through the cellular structure, reducing hydrostatic pressure accumulation on slopes and embankments, particularly in high-rainfall regions, monsoon-prone areas, and applications that combine erosion control with vegetated slope stabilization to support ecosystem restoration objectives.

Application Insights

Road base and pavement reinforcement applications account for the largest share of the global geocells Market at 34.2% in 2026, reflecting the foundational role of geocells in addressing core highway engineering challenges, including subgrade stabilization, load distribution optimization, and pavement durability enhancement across diverse traffic volumes and soil conditions.

Highway authorities invest in geocell-based pavement reinforcement to reduce aggregate requirements by reducing base-layer thickness by up to 50 percent, thereby lowering material costs, minimizing excavation of inferior subgrades, and enabling the use of locally available, lower-quality infill materials that deliver cost-effective stabilization without compromising performance.

Channel and slope protection applications represent the fastest-growing segment of the geocells market, driven by escalating erosion-control requirements resulting from increased precipitation intensity, extreme weather events, infrastructure construction in geomorphologically unstable terrain, and integrated environmental restoration initiatives that combine engineering stability with ecosystem objectives.

Climate change impacts, amplifying rainfall intensity and flood frequency, drive demand for erosion control infrastructure, where geocells provide cost-effective solutions compared to conventional concrete lining, rip-rap placement, or structural retaining walls requiring higher capital investment.

Regional Insights and Trends

North America Geocells Market Trends

North America represents an established, mature geocells market characterized by advanced infrastructure systems, high capital investment, and sophisticated specifications combining technical performance requirements with sustainability and environmental compliance mandates. The United States maintains one of the world's largest transportation networks, spanning 4.19 million miles of roads and supporting 340 million residents. This network requires continuous pavement preservation and embankment stabilization investments, which increasingly incorporate geocell technology to reduce maintenance costs and extend infrastructure lifespan.

U.S. construction sector spending reached US$2.2 trillion in 2024, representing 4.5 percent of GDP and supporting 8.2 million workers. Geocell adoption is concentrated in transportation, heavy civil construction, and industrial infrastructure applications, where proven performance, durability, and cost-effectiveness justify specification in competitive-bidding environments.

The North American market demonstrates the highest contractor sophistication and technical knowledge regarding geocell design, installation, and performance optimization, enabling advanced applications, including composite-reinforced designs, specialized material selections, and integrated installation methodologies that maximize performance across diverse soil types and traffic conditions.

East Asia Geocells Market Trends

East Asia dominates the global geocells market consumption, accounting for 32.8% of the total market value, driven by China's rapid expressway capacity expansion, India's transformative infrastructure modernization programs, and emerging market transportation network development across Southeast Asia, supporting economic growth and regional connectivity objectives.

India's highway network expansion to 146,204 kilometers, accelerated by a construction pace of 34 kilometers per day, combined with 45,000 route-kilometer railway electrification initiatives, creates sustained infrastructure investment that supports geocell demand across diverse applications, including subgrade stabilization, slope protection in mountainous terrain, and railway ballast reinforcement.

China's road network expansion to 6.49 million kilometers by August 2025, representing growth from 5.2 million kilometers in 2020, combined with 440 million vehicle ownership, supporting high-traffic-volume expressways, creates demand for pavement reinforcement and embankment stabilization applications that address infrastructure durability under extreme traffic loading and diverse climatic conditions.

Europe Geocells Market Trends

Europe represents a mature geocells market characterized by sophisticated engineering standards, stringent environmental compliance frameworks, and infrastructure maintenance priorities that support steady demand across transportation, environmental protection, and climate-resilience applications.

European railway infrastructure density is concentrated in Germany, Czechia, Hungary, and the northwestern regions, with Berlin exhibiting a railway density of 764 km per 1,000 km², generating recurring demand for embankment stabilization, ballast reinforcement, and track geometry maintenance to support high-speed rail corridor operations and freight transportation network integrity.

Construction waste management imperatives, reflecting European Union waste statistics indicating that 38.4 percent of total waste originated from construction activities in 2022, drive regulatory pressure for resource-efficient ground stabilization solutions that minimize material consumption and support circular economy principles through recycled-content geocell systems and the utilization of locally available infill materials.

Competitive Landscape

The global geocells market is moderately consolidated with pockets of fragmentation, where a handful of established global players coexist with numerous regional and specialty manufacturers. This structure reflects high entry barriers due to technical expertise requirements, material quality standards, and project-specific engineering competencies, but also space for niche and local suppliers in emerging markets.

Strata Systems, Presto Geosystems, and Officine Maccaferri lead the industry with broad portfolios, strong R&D, and deep relationships in infrastructure and transportation projects across multiple regions. PRS Geo-Technologies and TMP Geosynthetics further strengthen the competitive core with advanced geocell solutions and engineering support services for complex civil and environmental applications.

Koninklijke Ten Cate B.V. and Terram Geosynthetics leverage their extensive geosynthetics expertise and wide distribution networks to capture a share in road base reinforcement, slope protection, and retaining structures. Mid-tier players like Flexituff International and Geo Products often compete on cost and regional responsiveness, particularly in Asia-Pacific and Latin America.

Key Industry Developments:

- In September 2025, Strata continues to expand its use of StrataWeb® geocells in India’s infrastructure sector, deploying them in specialized applications, including crusher walls in mining projects and railway transition slabs. These solutions provide cost-effective, sustainable alternatives to conventional concrete or gravity walls, enhance track stability, reduce differential settlement, and cut long-term maintenance costs. This development reflects the growing adoption of geocells in India, driven by government investments in highways, railways, metros, and rural connectivity, and highlights Strata’s role in pioneering geocell-based solutions for site-specific civil engineering challenges.

- In April 2025, Presto Geosystems announced the publication of the industry’s first Environmental Product Declaration (EPD) for GEOWEB® geocells, providing a transparent, life-cycle-based assessment of environmental impacts, including carbon footprint, energy consumption, and resource usage. This initiative reinforces the company’s commitment to sustainable infrastructure and empowers engineers, architects, and project owners to select geocell solutions that align with environmental and green building goals, further strengthening the adoption of geocells in civil and structural projects globally.

Companies Covered in Geocells Market

- Strata Systems

- PRS Geo-Technologies

- Presto Geosystems

- Koninklijke Ten Cate B.V.

- TMP Geosynthetics

- Terram Geosynthetics

- Berry Plastics

- Officine Maccaferri

- Flexituff International

- Geo Products

Frequently Asked Questions

The global geocells market is projected to be valued at US$ 896.3 Mn in 2026.

The High-Density Polyethylene (HDPE) segment is expected to account for approximately 68.5% of the Global Geocells Market by Use Industry in 2026.

The market is expected to witness a CAGR of 9.0% from 2026 to 2033.

The Geocells Market growth is driven by large-scale transportation infrastructure expansion across highways and railways, combined with rising regulatory pressure for sustainable, resource-efficient construction and cost-effective ground stabilization solutions.

Key market opportunities in the Geocells Market lie in railway infrastructure modernization through ballast reinforcement systems and in climate-resilient infrastructure, including coastal protection, erosion control, and slope stabilization driven by government investments and climate adaptation programs.

Key players in the Geocells Market include Strata Systems, Presto Geosystems, Officine Maccaferri, PRS Geo-Technologies, Koninklijke Ten Cate B.V., and Terram Geosynthetics.