- Pharmaceuticals

- General Anesthesia Drugs Market

General Anesthesia Drugs Market Size, Trends, Share, and Growth Forecast 2026 - 2033

General Anesthesia Drugs Market by Drug Type (Inhalational Anesthetics, Intravenous (IV) Anesthetics, Adjunct Anesthetics), by Application (Cardiovascular Surgery, Orthopedic Surgery, Neurosurgery, General Surgery, Obstetrics & Gynecology, Others), End-user (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), by Regional Analysis, 2026 - 2033

Anesthesia Drugs Market Share and Trends Analysis

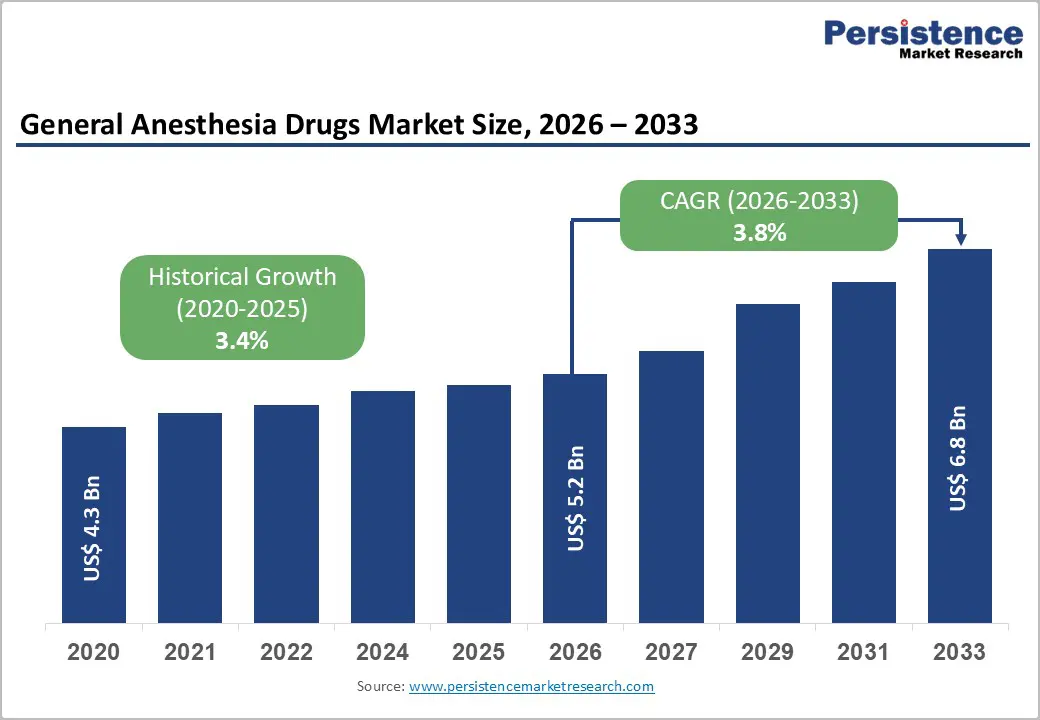

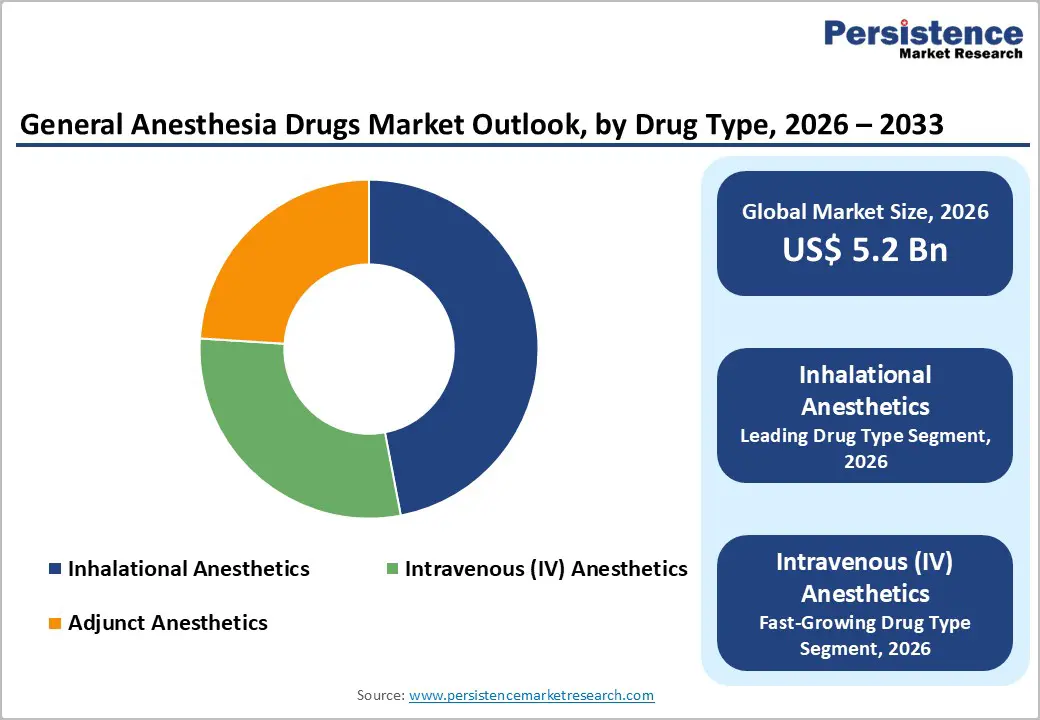

The global general anesthesia drugs market size is expected to be valued at US$ 5.2 billion in 2026 and projected to reach US$ 6.8 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033.

Rising surgical procedure volumes, an expanding geriatric population, and the increasing burden of chronic diseases are the primary drivers of steady global demand for general anesthetics. This growth trajectory is reinforced by improvements in perioperative safety, better access to essential surgery in low and middle-income countries, and innovation in inhalational and intravenous agents that support faster recovery and reduced postoperative complications. The market further benefits from enhanced monitoring technologies and standardized perioperative pathways that enable higher surgical throughput, particularly in high-income regions with mature hospital and ambulatory care networks.

Key Industry Highlights:

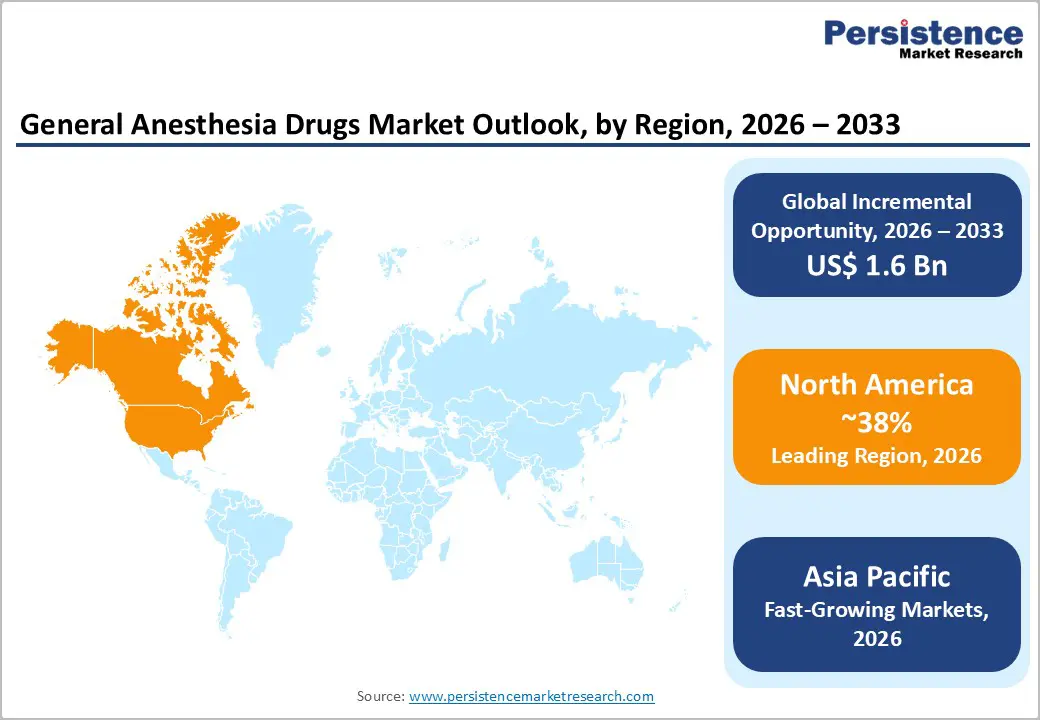

- North America is projected to remain the leading regional market for general anesthesia drugs, supported by high surgical procedure volumes, strong insurance coverage, and a sophisticated anesthesia care ecosystem centered on the U.S. and Canada.

- Asia-Pacific is expected to be the fastest-growing region, driven by expanding hospital infrastructure, increased access to essential surgery in China, India, and ASEAN, and competitive regional manufacturing capabilities for

- generic anesthetic agents.

- By drug type, inhalational anesthetics dominate with about 47% share in 2025, reflecting their entrenched role in the maintenance of general anesthesia across a wide spectrum of surgeries and their compatibility with advanced anesthesia workstations.

- Intravenous (IV) anesthetics are anticipated to be the fastest-growing segment, benefiting from the rapid expansion of ambulatory and day-care surgery, demand for fast onset and recovery, and wider adoption of enhanced recovery protocols.

- A key market opportunity lies in developing safer, more convenient formulations and integrated anesthesia solutions aligned with enhanced recovery pathways, targeting high-risk geriatric patients and high-throughput surgical centers seeking better outcomes and efficiency.

| Key Insights | Details |

|---|---|

| General Anesthesia Drugs Market Size (2026E) | US$ 5.2 billion |

| Market Value Forecast (2033F) | US$ 6.8 billion |

| Projected Growth CAGR (2026 - 2033) | 3.8% |

| Historical Market Growth (2020 - 2025) | 3.4% |

Market Dynamics

Drivers - Rising global surgical procedure volumes and access to essential surgery

A key growth driver for the general anesthesia drugs market is the sustained rise in surgical procedure volumes across both developed and emerging economies. The Lancet Commission on Global Surgery estimated that roughly 313 million surgical procedures are performed annually worldwide, highlighting a substantial and persistent need for perioperative anesthesia services. Many low and middle-income countries still perform far below the benchmark of 5,000 surgeries per 100,000 population, with averages around 877 surgeries per 100,000 in some analyses, suggesting significant latent demand as health systems scale up surgical capacity. As governments invest in universal health coverage, trauma care, obstetric services, and non-communicable disease management, the number of procedures requiring general anesthesia is expected to increase, thereby increasing the utilization of both inhalational and intravenous agents.

Growing geriatric population and complex comorbidities

The rapid growth of the global geriatric population is another strong structural driver of demand for general anesthetic drugs. Older adults undergo a disproportionately higher share of surgeries for conditions such as hip fractures, cardiovascular disease, cancer, and degenerative orthopedic disorders, all of which often necessitate general anesthesia. Clinical literature shows that elderly surgical patients have elevated postoperative complication rates, with studies reporting complication incidences ranging from 12.5% to 43% and postoperative delirium affecting up to around 26% of patients over 60 years in some cohorts. This necessitates careful anesthetic planning, including titratable agents and adjunct drugs to support hemodynamic stability and rapid recovery, thereby sustaining demand for newer formulations and optimized dosing strategies in this population.

Restraints - Safety concerns, postoperative complications, and shifting preference to regional techniques

One of the main restraints for the general anesthesia drugs market is the growing scrutiny around safety, particularly in high-risk and very elderly patients. Comparative studies have indicated that general anesthesia can be associated with higher rates of postoperative pulmonary and cardiac complications versus regional techniques in selected procedures, with some cohorts demonstrating postoperative complication rates exceeding 30% in general anesthesia groups. Evidence that spinal or regional anesthesia may reduce certain complications and shorten hospital stay has encouraged clinicians to prefer these modalities when clinically appropriate. As enhanced recovery protocols and minimally invasive techniques expand, this preference could modestly temper the growth in general anesthesia utilization for specific surgeries, especially in high-income regions with strong anesthesia practice standards.

Regulatory, pricing, and supply-chain pressures on anesthetic drugs

Regulatory requirements for anesthetic agents remain stringent due to their potent pharmacologic effects, narrow therapeutic window, and abuse potential in some cases. Manufacturers face rigorous quality, pharmacovigilance, and manufacturing compliance standards from agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), which can increase development and production costs. Furthermore, episodes of injectable anesthetic shortages have been reported in multiple regions over the past decade, with supply disruptions linked to manufacturing issues, consolidation of active pharmaceutical ingredient suppliers, and pricing pressures on generic injectables. These challenges can constrain availability of certain agents, prompt formulary substitutions, and affect hospital purchasing decisions, thereby acting as a restraint on consistent market expansion.

Opportunities - Expansion of ambulatory and day-care surgery supported by fast-acting IV anesthetics

The rapid expansion of ambulatory surgical centers and day-care procedures presents a significant opportunity for vendors of general anesthetic drugs, particularly intravenous (IV) anesthetics with rapid onset and recovery. High-income health systems continue to shift suitable procedures from inpatient hospitals to outpatient centers to reduce costs and improve patient convenience, favoring anesthetic protocols with short-acting IV agents and optimized adjuncts. In markets such as the U.S., bundled anesthesia solutions, tailored dosing systems, and ready-to-use vials support efficient turnover in ambulatory settings. As more complex procedures migrate to ambulatory platforms and as middle-income countries replicate these models, suppliers that provide portfolio depth in IV anesthetics, antiemetics, and analgesic adjuncts are positioned to capture a disproportionately high share of incremental demand.

Innovation in safer formulations and monitoring-integrated anesthesia care pathways

Another significant opportunity lies in developing improved formulations and delivery systems that enhance the safety, stability, and ease of use of general anesthetic drugs. Ongoing advances in inhalational agents, target-controlled infusion technologies, and multimodal analgesia are enabling clinicians to tailor anesthetic depth and minimize postoperative cognitive dysfunction, particularly in vulnerable populations. Integration of anesthesia drug protocols with advanced monitoring (e.g., depth-of-anesthesia monitoring, hemodynamic optimization) and enhanced recovery after surgery pathways can reduce complications and length of stay, thereby amplifying the clinical and economic value of high-quality anesthetic products. Companies that invest in evidence-backed formulations, novel delivery devices, and education programs for anesthesiologists can differentiate themselves and unlock premium segments within the broader general anesthesia drugs market.

Category-wise Analysis

Drug Type Insights

In drug type, inhalational anesthetics represent the leading segment, accounting for about 47% market share in 2025. Volatile agents such as sevoflurane and desflurane have become mainstays for maintenance of general anesthesia due to their favorable pharmacokinetic profiles, controllable depth of anesthesia, and compatibility with modern anesthesia workstations. These agents allow rapid titration and relatively quick emergence, which is important for both inpatient and day-care surgical workflows. Clinical practice guidelines and training worldwide still emphasize inhalational maintenance for a broad range of procedures, especially in high-income hospitals where advanced vaporizers and gas monitoring are standard. As surgical volumes grow and operating room infrastructures improve in emerging markets, the adoption of inhalational agents is likely to remain strong, sustaining their dominant share even as IV anesthetics show faster percentage growth.

Application Insights

Within the application, general surgery can reasonably be identified as the leading segment by procedure volume and, consequently, by anesthetic drug utilization. General surgery encompasses a wide range of operations, including appendectomies, cholecystectomies, hernia repairs, and gastrointestinal procedures, many of which rely on general anesthesia, especially in complex or laparoscopic cases. OECD analyses of surgical activity show consistently high rates of common general surgical procedures such as appendectomy and cholecystectomy across high-income countries, underscoring their central role in hospital workload. In low and middle-income settings, scaling up access to essential general surgical care is a key health system priority, further reinforcing this segment’s importance. Given the breadth of indications, diversity of patient profiles, and frequency of these operations, general surgery is expected to command the largest share of anesthetic drug use across the application spectrum.

End-user Insights

Among end users, hospitals are the largest segment, accounting for the majority of global consumption of general anesthetic drugs. Most complex and high-risk surgeries, including cardiovascular, neurosurgical, major oncologic, and emergency trauma procedures, are performed in hospital operating rooms that require fully equipped anesthesiology departments and intensive care capabilities. Hospitals also manage a high volume of elective and essential general surgeries, obstetric procedures, and pediatric operations, all driving sustained demand for both inhalational and IV anesthetics. While ambulatory surgical centers are gaining share for selected procedures in high-income countries, hospital-based surgery remains dominant in many regions, particularly in low and middle-income countries where ambulatory infrastructure is still developing. Consequently, hospital purchasing decisions, formulary policies, and group procurement strategies play a central role in shaping competitive dynamics within the general anesthesia drugs market.

Regional Insights

North America General Anesthesia Drugs Market Trends and Insights

North America, led by the U.S., represents the largest regional market, with an estimated 38% share of global general anesthesia drugs demand in 2025. High surgical procedure volumes, strong insurance coverage, and advanced hospital and ambulatory infrastructures underpin this leadership position. The region also benefits from a dense network of board-certified anesthesiologists, robust residency training programs, and widespread adoption of enhanced recovery after surgery protocols, all of which drive standardized use of high-quality anesthetic agents.

The regulatory frameworks overseen by bodies such as the U.S. FDA and Health Canada enforce strict quality, safety, and pharmacovigilance standards for anesthetic drugs, thereby encouraging continuous product improvement and post-marketing surveillance. North America also hosts several leading pharmaceutical manufacturers and innovators in anesthesia, fostering an active ecosystem for clinical trials, new formulation launches, and partnerships with ambulatory surgical centers. In recent years, there has been growing emphasis on optimizing anesthesia care for high-risk geriatric and cardiac patients, promoting adoption of titratable IV agents, adjunct anesthetics, and advanced monitoring solutions to reduce complications and readmissions.

Asia Pacific General Anesthesia Drugs Market Trends and Insights

Asia-Pacific is the fastest-growing region in the general anesthesia drugs market, supported by large and aging populations in China, Japan, and India, and by expanding surgical capacity across ASEAN countries. Many health systems in this region are investing heavily in hospital infrastructure, surgical training, and universal health coverage, which is increasing access to essential and elective surgery. As surgical volumes rise from below-benchmark levels in several low and middle-income countries, demand for basic and advanced anesthetic agents is expected to grow at a rate higher than the global average.

Asia-Pacific also offers significant manufacturing and cost advantages, particularly for generic injectable anesthetics and inhalational agents produced by regional pharmaceutical companies. Governments are focusing on strengthening supply chains for essential medicines, which supports local production and partnerships with multinational manufacturers. In parallel, leading tertiary hospitals in metropolitan centers are adopting Western-style enhanced recovery protocols and advanced anesthesia monitoring, driving uptake of modern inhalational agents, IV anesthetics, and multimodal adjuncts. These dynamics position the Asia Pacific as a key growth engine for the global general anesthesia drugs market over the next decade.

Competitive Landscape

The global general anesthesia drugs market features a competitive landscape driven by innovation in anesthetic formulations, safety profiles, and delivery methods. Players differentiate through development of agents with faster onset, shorter recovery times, and improved patient tolerability, while responding to stringent regulatory standards. The market also sees increasing focus on combination therapies and improved pain management adjuncts to optimize surgical outcomes. Competition is shaped by clinical efficacy data, cost-effectiveness, and inclusion in hospital formularies, with strategic emphasis on expanding geographic reach and addressing growing demand in emerging healthcare markets.

Key Developments:

- In April 2025, Avenacy, a specialty pharmaceutical company focused on supplying critical injectable medications, announced that it had launched Propofol Injectable Emulsion, USP in the United States as a therapeutic generic equivalent to Diprivan®, following approval by the U.S. Food and Drug Administration.

Companies Covered in General Anesthesia Drugs Market

- Baxter International Inc.

- Fresenius SE & Co. KGaA (Fresenius‑Kabi)

- AbbVie Inc.

- AstraZeneca

- B. Braun Melsungen AG

- Pfizer Inc.

- Hospira Inc.

- Aspen Pharmacare Holdings Ltd.

- Hikma Pharmaceuticals PLC

- Abbott Laboratories

- Maruishi Pharmaceutical Co., Ltd.

- Piramal Critical Care (Piramal)

Frequently Asked Questions

The global general anesthesia drugs market size is expected to reach about US$ 5.2 billion in 2026, reflecting steady demand growth from rising surgical procedure volumes and expanding access to essential surgery worldwide.

The main demand driver is the increasing number of surgical procedures globally, supported by aging populations, higher prevalence of chronic diseases, and health system investments that expand access to essential and elective surgery across regions.

North America, led by the U.S., currently leads the general anesthesia drugs market, supported by high surgical procedure volumes, advanced hospital and ambulatory infrastructures, and a strong base of anesthesiology specialists.

A key opportunity lies in developing safer, fast-acting formulations and integrated anesthesia solutions tailored to enhanced recovery pathways, especially for high‑risk geriatric and ambulatory surgery patients seeking shorter stays and fewer complications.

Major players include Baxter International Inc., Fresenius SE & Co. KGaA, AbbVie Inc., AstraZeneca, B. Braun Melsungen AG, Pfizer Inc., Hospira Inc., Aspen Pharmacare Holdings Ltd., Hikma Pharmaceuticals PLC, Abbott Laboratories, Maruishi Pharmaceutical Co., Ltd., and Piramal Critical Care (Piramal) among others, active in anesthetic and perioperative drug portfolios.