- Smart Packaging

- Gable Box Market

Gable Box Market Size, Share, and Growth Forecast, 2026 - 2033

Gable Box Market by Material (Paper, Plastic, Others), Distribution Channel (Supermarkets, Online Sales, Others), End-user, and Regional Analysis for 2026 - 2033

Gable Box Market Size and Trends Analysis

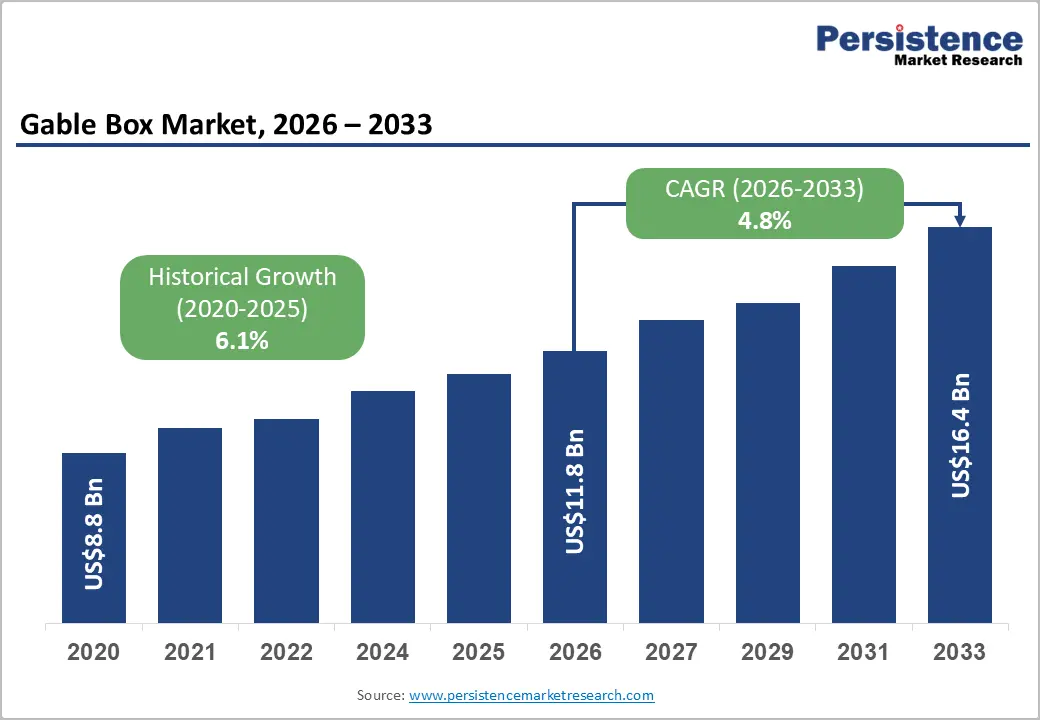

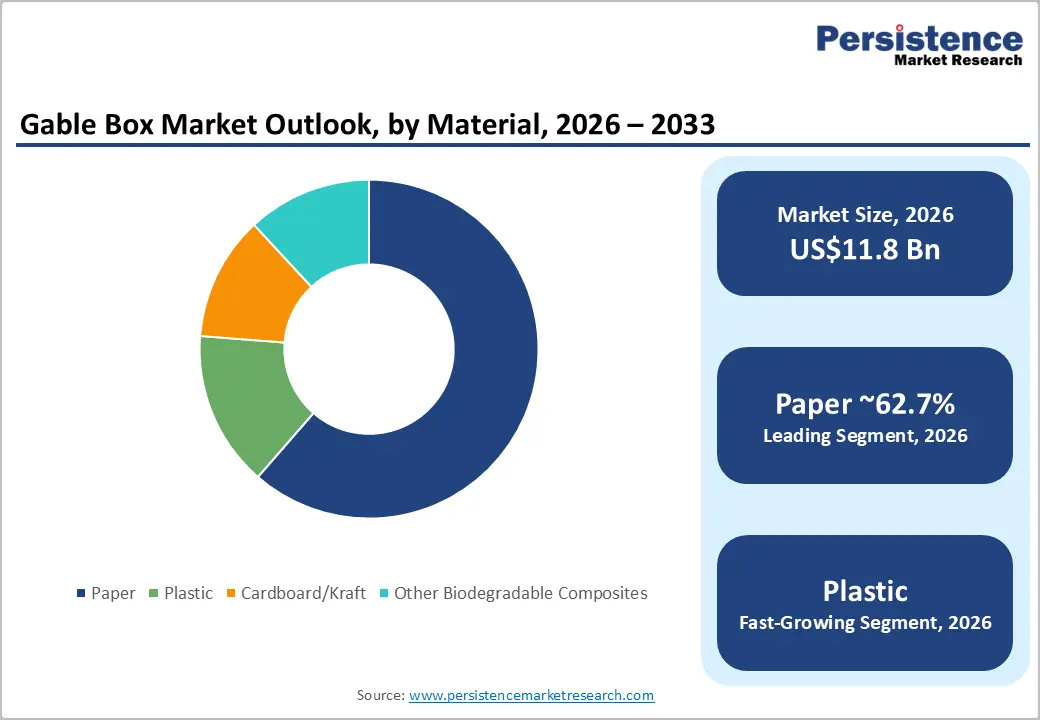

The global gable box market size is likely to be valued at US$11.8 billion in 2026 and is expected to reach US$16.4 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by expanding packaged food consumption, increasing sustainability mandates, and rapid e-commerce penetration. Paper-based gable boxes dominate due to recyclability advantages, while premium customization and smart packaging features are driving value expansion.

Mature markets provide stable, recurring demand, whereas Asia Pacific delivers incremental growth through urbanization and retail modernization.

Key Industry Highlights

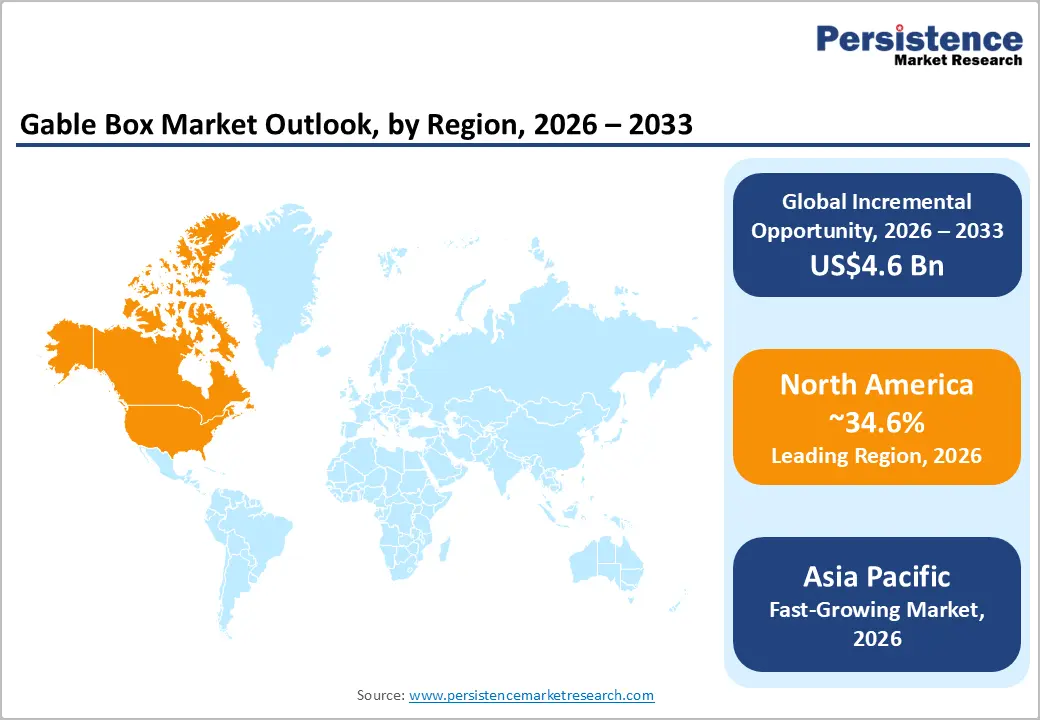

- Leading Region: North America is projected to hold 34.6% of the market share, supported by mature foodservice infrastructure and strong fiber-based packaging adoption.

- Fastest-Growing Region: Asia Pacific, driven by urbanization, retail expansion, and rising packaged food consumption.

- Investment Plans: Capacity expansion in recyclable paperboard, digital printing, and biodegradable barrier technologies across the U.S., Europe, and Asia.

- Dominant Material: The paper is anticipated to hold 62.7% market share, favored for recyclability, cost efficiency, and regulatory compliance.

- Leading End-user: The food & beverages segment is estimated to hold 41.3% of market share, led by takeout meals, bakery, dairy, and ready-to-eat applications.

| Key Insights | Details |

|---|---|

| Gable Box Market Size (2026E) | US$11.8 Bn |

| Market Value Forecast (2033F) | US$16.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand in Food & Beverage Packaging

The food and beverage sector remains the primary demand engine, accounting for more than 41.3% of global gable box consumption. Structural shifts toward ready-to-eat meals, takeaway dining, and meal kit subscriptions continue to expand packaging volumes. Consumers increasingly prioritize convenience, portability, and hygiene, attributes well-suited to gable box designs. Quick-service restaurants, dairy processors, bakeries, and grocery chains rely on gable formats for bundled offerings and promotional packaging.

The format’s integrated handle improves portability, while flat printable surfaces enhance brand communication. Growth in food delivery platforms and urban takeaway culture reinforces recurring demand cycles. Food sector dependency creates stable, high-volume procurement contracts, supporting long-term manufacturing capacity utilization and predictable revenue streams.

Expansion of E-Commerce and Omni-Channel Retail

Global retail continues to shift toward omni-channel distribution models. Direct-to-consumer (DTC) brands increasingly select gable boxes for subscription kits, seasonal gift sets, and limited-edition bundles. The structural strength of gable packaging enhances product protection during transit, reducing damage rates and reverse logistics costs. Large printable panels allow QR codes, brand messaging, and personalized marketing campaigns. As e-commerce penetration deepens across developed and emerging markets, packaging demand grows in parallel.

Small and medium enterprises are also adopting custom gable packaging to strengthen differentiation in crowded digital marketplaces. Online retail growth diversifies demand sources beyond traditional brick-and-mortar, smoothing seasonality and supporting long-term volumetric stability.

Sustainability Regulations and Circular Packaging Mandates

Environmental policy shifts have reshaped packaging procurement criteria. Extended Producer Responsibility (EPR) frameworks and recycling targets across North America and Europe incentivize fiber-based solutions. Brands increasingly commit to recyclable or compostable packaging targets within ESG roadmaps. Paperboard and kraft gable boxes align well with sustainability mandates due to high recycling compatibility and lower perceived environmental impact compared to rigid plastics.

Consumer awareness also influences purchasing decisions, particularly in premium retail and food service environments. Sustainability alignment enhances pricing resilience for recyclable formats and encourages investment in advanced coatings and biodegradable composites.

Barrier Analysis - Raw Material Price Volatility

Paperboard, kraft paper, and recycled fiber prices fluctuate based on pulp supply, energy costs, and logistics constraints. Input cost instability compresses margins, especially for mid-sized converters with limited hedging capacity. Inability to fully pass costs to customers during procurement cycles may reduce profitability. Volatility also impacts capital expenditure planning, slowing expansion in some regions. Long-term contracts partially mitigate risk but do not eliminate exposure.

Competition from Alternative Packaging Formats

Flexible pouches, clamshell containers, rigid folding cartons, and corrugated boxes compete across various applications. Certain formats offer superior moisture resistance or lower transportation costs per unit. High-volume commodity products may prioritize cost efficiency over branding flexibility, limiting gable box penetration. Competition remains particularly strong in beverage packaging and electronics bundling segments, where structural alternatives provide enhanced protective features.

Opportunity Analysis - Expansion in Emerging Markets

Asia Pacific and Latin America represent substantial untapped growth potential for the gable box market. Rapid urbanization, rising middle-class populations, and increasing disposable incomes are driving higher consumption of packaged foods, bakery products, dairy beverages, and personal care items. Retail formalization, through supermarket chains, convenience store networks, and expanding e-commerce platforms, further accelerates the shift from loose to branded packaged goods.

Domestic packaging manufacturers in countries such as China, India, Brazil, and Mexico are expanding paperboard converting capacity to meet local demand, reducing reliance on imported cartons and improving cost competitiveness. Government initiatives supporting local manufacturing and sustainability are also encouraging fiber-based packaging adoption. At the same time, multinational food and cosmetic brands entering these markets rely on differentiated and visually appealing packaging to establish brand recognition, creating incremental demand for customizable gable box formats.

Smart Packaging and Functional Coatings

Technological advancements in barrier coatings, moisture-resistant laminates, greaseproof layers, and oxygen-blocking materials are significantly expanding the functional scope of gable boxes. These innovations allow the format to serve moisture-sensitive bakery items, chilled dairy products, ready-to-eat meals, and select personal care products that require enhanced protection.

In parallel, integration of QR codes, serialized barcodes, and NFC-enabled labels supports product traceability, anti-counterfeiting measures, and direct consumer engagement. Brands increasingly use smart features to link packaging to digital promotions, ingredient sourcing information, and sustainability disclosures. These enhancements enable premium pricing strategies and improve supply chain transparency, particularly in cosmetics, specialty foods, and electronics gift packaging segments.

Customization and Premium Branding

High-resolution digital printing, embossing, foil stamping, die-cut windows, and specialty matte or gloss finishes are elevating the aesthetic appeal of gable packaging. Premium cosmetic brands, artisanal food producers, and seasonal confectionery companies frequently adopt custom-designed gable boxes for gift sets, influencer campaigns, and limited-edition launches.

Short-run production capabilities and rapid design turnaround cycles are becoming competitive differentiators, particularly for e-commerce-driven brands requiring frequent packaging refreshes. Customization not only enhances shelf visibility but also strengthens brand storytelling and customer loyalty. As consumer preference shifts toward visually distinctive and sustainable packaging, converters capable of combining structural innovation with premium finishing techniques are positioned to capture higher-margin opportunities.

Category-wise Analysis

Material Insights

Paper and cardboard materials are anticipated to maintain a dominant 62.7% share of the market through the forecast period, supported by recyclability advantages, cost efficiency, and alignment with environmental regulations. Paperboard gable boxes are widely used across food, bakery, confectionery, and dairy applications where lightweight construction and structural rigidity are required. For example, bakery chains and dairy brands frequently use coated paperboard gable cartons for pastries, meal bundles, and flavored milk packaging due to their balance of strength and branding visibility.

Developed markets such as North America and Western Europe benefit from established fiber recycling systems, reinforcing long-term supply reliability and regulatory compliance. Paper substrates also provide superior print quality, allowing high-resolution graphics, promotional messaging, and QR-enabled consumer engagement. Corporate ESG commitments increasingly prioritize recyclable fiber-based formats, which strengthens procurement preference for paper gable solutions among multinational foodservice and retail operators.

Plastic-based gable formats and biodegradable composite materials represent the fastest-growing material category, particularly in applications requiring enhanced barrier protection. These materials deliver improved resistance to moisture, grease, and oxygen exposure, making them suitable for temperature-sensitive foods, frozen desserts, specialty beverages, and premium cosmetic kits. For instance, moisture-resistant laminated gable boxes are increasingly used for gourmet meal kits and refrigerated confectionery products where shelf-life stability is critical.

Bio-based polymer blends and compostable coatings are also emerging as alternatives that combine durability with sustainability compliance. Innovation in bio-plastic technologies allows manufacturers to maintain performance standards while meeting environmental targets. Growth in this segment is closely tied to premium packaging applications and regulatory encouragement of lower-impact material solutions.

End-user Insights

The food and beverage sector is anticipated to account for more than 41.3% of market share, maintaining its position as the largest end-use segment. Takeout meals, dairy beverages, bakery assortments, snack bundles, and ready-to-eat offerings rely on gable designs for portability, convenience, and branding flexibility.

Quick-service restaurants often package family meal deals and combo sets in handled gable boxes, improving customer carrying convenience and product presentation. Expansion of urban dining culture and food delivery platforms reinforces consistent packaging procurement. Dairy processors also use gable-style cartons for flavored milk and juice products, where integrated handles enhance consumer usability. Stackability and flat-fold shipping formats reduce storage and logistics costs, improving supply chain efficiency for high-volume food producers.

The personal care and cosmetics segment is projected to record the fastest growth among end-user categories. Premium beauty brands increasingly adopt customized gable packaging for seasonal gift sets, limited-edition influencer collaborations, and subscription-based skincare kits. The format supports high-quality printing, embossing, metallic finishes, and specialty coatings, enabling visually distinctive packaging.

For example, holiday cosmetic bundles and fragrance collections frequently utilize decorative gable boxes to enhance perceived value and gifting appeal. Growth in direct-to-consumer beauty brands further accelerates adoption, as packaging plays a central role in unboxing experiences and social media visibility. Consumer demand for sustainable yet aesthetically appealing packaging strengthens the use of recyclable paper-based gable formats in this segment, supporting above-average growth momentum through 2033.

Regional Insights

North America Gable Box Market Trends - U.S.-Led Growth Driven by QSR, E-Commerce, and Fiber Substitution

North America is anticipated to maintain its leadership position in the market, accounting for an estimated 34.6% of revenue share through the forecast period. The U.S. represents the dominant contributor, supported by high per-capita packaged food consumption, an advanced quick-service restaurant ecosystem, and strong e-commerce penetration. Large foodservice operators and grocery chains continue to rely on handled carton formats for meal bundles, bakery assortments, and seasonal promotional packaging. The expansion of meal kit providers and club-store retailing further reinforces recurring procurement of durable, stackable packaging formats.

Sustainability policy plays a critical role in shaping material demand. Several U.S. states, including California and New York, have implemented stricter packaging waste reduction frameworks, encouraging retailers and consumer goods companies to shift toward recyclable fiber-based formats.

Major packaging producers such as WestRock Company and International Paper have expanded investments in automated converting lines and digital printing technologies to meet demand for customized, short-run packaging solutions. In 2024-2025, Graphic Packaging International continued upgrading its paperboard capacity and recyclable barrier technologies, supporting fiber substitution in food applications.

Industrial clusters across the Midwest and Southeast provide integrated supply chains, including pulp processing, paperboard production, and final conversion. Long-term procurement agreements between packaging suppliers and multinational retailers stabilize revenue streams and reduce demand volatility. Growth in subscription commerce and direct-to-consumer beauty brands in the U.S. also contributes incremental demand for premium printed gable packaging, reinforcing North America’s structural market leadership.

Europe Gable Box Market Trends - Regulation-Driven Fiber Transition Under PPWD and EPR

Europe represents a highly regulated and sustainability-driven market environment. Demand is concentrated in Germany, the U.K., France, and Spain, where strict environmental standards and strong retail consolidation influence packaging procurement strategies. The European Union’s Packaging and Packaging Waste Directive (PPWD) and Extended Producer Responsibility (EPR) frameworks have accelerated the shift toward recyclable and lightweight fiber-based materials.

Major regional packaging companies such as Mondi Group, DS Smith, and Smurfit Kappa have expanded sustainable paperboard solutions and recyclable barrier coatings to comply with tightening regulations. For example, Smurfit Kappa has strengthened its circular packaging portfolio across Western Europe, aligning with retailer sustainability targets. Germany’s strong recycling infrastructure supports high recovery rates of paper-based materials, reinforcing the economic viability of fiber gable packaging.

Retail groups increasingly require documented lifecycle assessments and recycled content verification from packaging suppliers. In the U.K., supermarket chains have accelerated the removal of hard-to-recycle plastics, indirectly encouraging fiber-based handled cartons for bakery and takeaway applications. France’s anti-waste legislation and Spain’s tourism-driven foodservice sector further contribute to regional packaging demand. Investment trends across Europe emphasize biodegradable coatings, lightweight structural engineering, and digital printing to support customization while meeting regulatory thresholds.

Asia Pacific Gable Box Market Trends - Urbanization and Retail Modernization Fuel High-Growth Expansion

Asia Pacific is projected to record the highest growth rate among all regions, driven by urbanization, rising disposable incomes, and rapid retail modernization in China, India, Japan, and Southeast Asia. Expanding middle-class populations are increasing consumption of packaged foods, bakery products, dairy beverages, and ready-to-eat meals, core applications for gable packaging formats. China remains a central growth engine due to large-scale food processing and e-commerce ecosystems.

Domestic and international packaging suppliers have expanded converting capacity to meet the rising demand for customized retail packaging. In India, increased penetration of organized retail chains and food delivery platforms has stimulated the procurement of handled carton formats for bundled takeaway meals. Government initiatives supporting domestic manufacturing have encouraged local production of paperboard packaging, reducing reliance on imports. Japan’s mature retail market emphasizes high-quality printing and structural precision, driving adoption of premium gable designs for confectionery and gift packaging.

ASEAN economies such as Indonesia, Thailand, and Vietnam are experiencing accelerated growth in quick-service restaurants and café chains, which increases demand for portable packaging solutions. Global packaging firms, including Mondi Group and Smurfit Kappa, have expanded their footprint in Asia through facility upgrades and regional partnerships, strengthening localized supply networks. Sustainability awareness is gradually increasing across the region, although regulatory enforcement varies by country. Investments in digital printing technology and advanced barrier coatings are enhancing regional competitiveness, positioning Asia Pacific as the primary incremental growth driver through 2033.

Competitive Landscape

The global gable box market is moderately fragmented, with top players collectively controlling approximately 40-50% of global volume. Competition centers on material innovation, operational efficiency, and customization capability. Large multinational firms compete alongside regional converters, creating balanced competitive intensity.

Key strategies include product innovation, cost optimization through automation, geographic expansion in emerging markets, and enhanced customization services. Sustainability positioning and digital printing capabilities represent major competitive differentiators.

Key Industry Developments:

- In July 2025, SIG launched the world’s first 1-liter aseptic carton pack using SIG Terra Alu-free + full barrier paper material, aiming to increase sustainability and extend shelf life across beverage applications globally.

- In March 2025, Elopak secured exclusive global rights for Blue Ocean Closures AB’s fiber-based closure technology to enhance the sustainability and performance of gable-top carton packs offered under its Pure-Pak® and D-PAK™ portfolios, strengthening its innovation capabilities in sustainable packaging.

Companies Covered in Gable Box Market

- WestRock Company

- International Paper

- Graphic Packaging International

- Mondi Group

- Smurfit Kappa

- DS Smith

- Stora Enso

- Amcor plc

- Huhtamaki

- Georgia-Pacific

- Oji Holdings Corporation

- Nippon Paper Industries

- Packaging Corporation of America

- Mayr-Melnhof Karton AG

- Cascades Inc.

- UFP Packaging

- Rengo Co., Ltd.

- SCG Packaging

Frequently Asked Questions

The global gable box market size is estimated to reach approximately US$11.8 billion in 2026.

The gable box market is projected to reach approximately US$16.4 billion by 2033.

Key trends include rising adoption of recyclable paperboard materials, investment in biodegradable barrier coatings, digital printing for customization, and increasing demand from e-commerce and premium gift packaging segments.

Paper & paperboard is the leading segment, accounting for 62.7% of market share, due to recyclability, cost efficiency, and regulatory alignment.

The gable box market is projected to grow at a CAGR of 4.8% through 2033.

Major players include WestRock Company, International Paper, Graphic Packaging International, Mondi Group, and Smurfit Kappa.