- Food Packaging

- Fresh Food Packaging Market

Fresh Food Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Fresh Food Packaging Market by Material (Plastic, Paper & Paperboard, Others), Packaging Type (Rigid, Flexible, Others), Application, and Regional Analysis for 2026 - 2033

Fresh Food Packaging Market Size and Trends Analysis

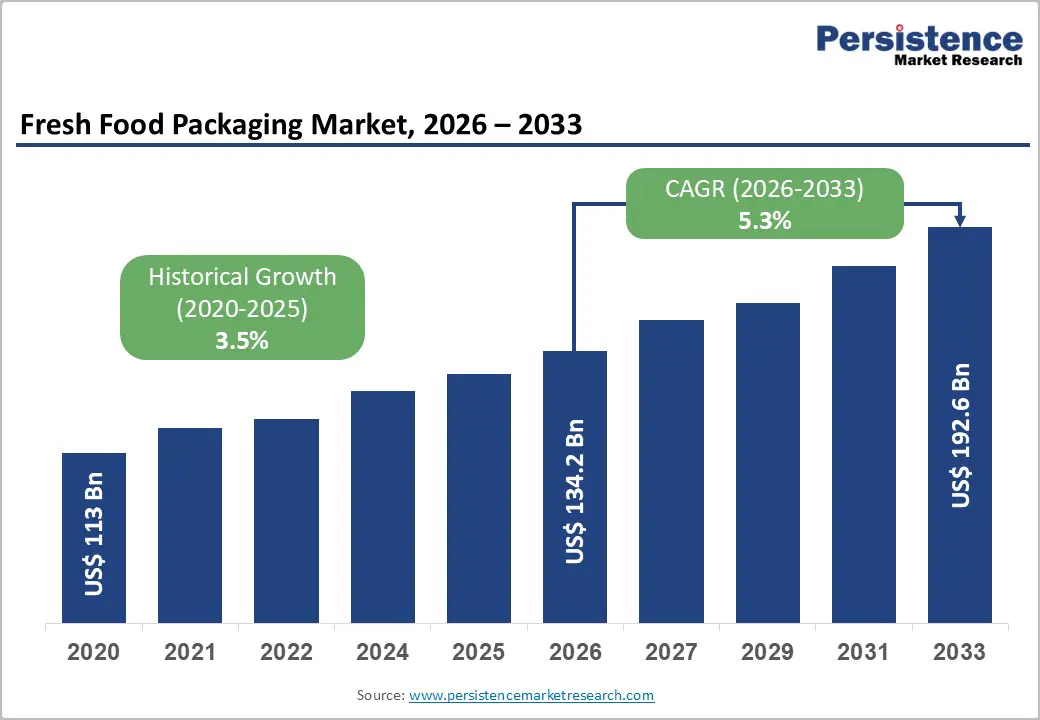

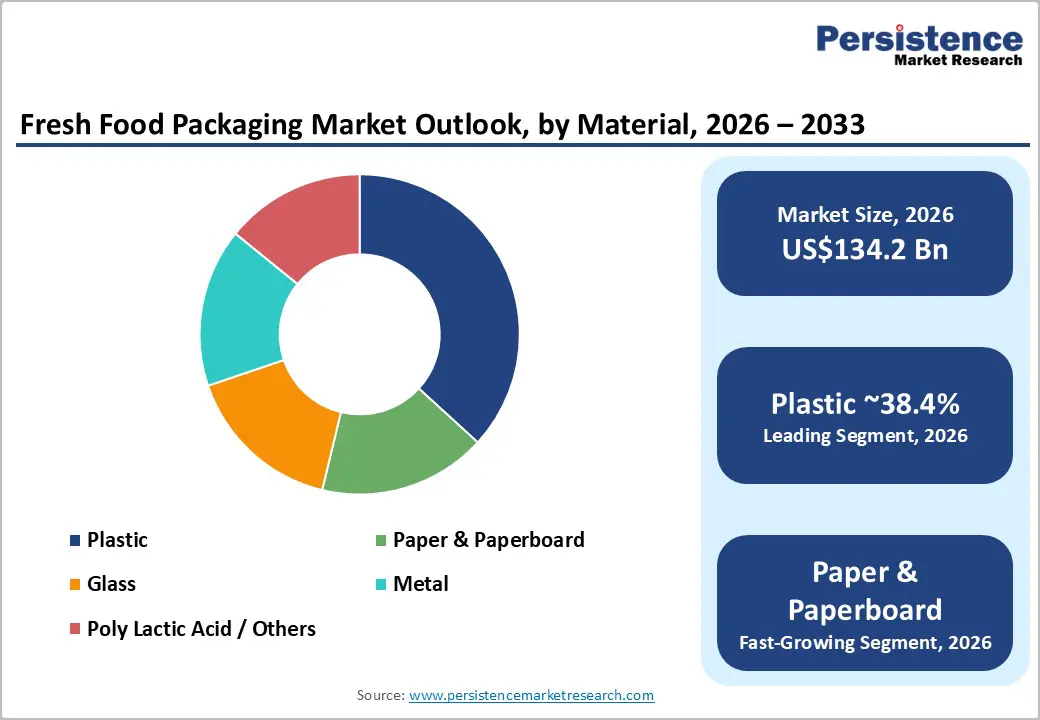

The global fresh food packaging market size is likely to be valued at US$134.2 billion in 2026 and is expected to reach US$192.6 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033, driven by structural changes in global food distribution systems.

Growth is supported by the increasing commercialization of fresh produce through modern retail and e-commerce channels, the expansion of cold-chain logistics in emerging markets, and the accelerated adoption of active and intelligent packaging solutions.

Key Industry Highlights:

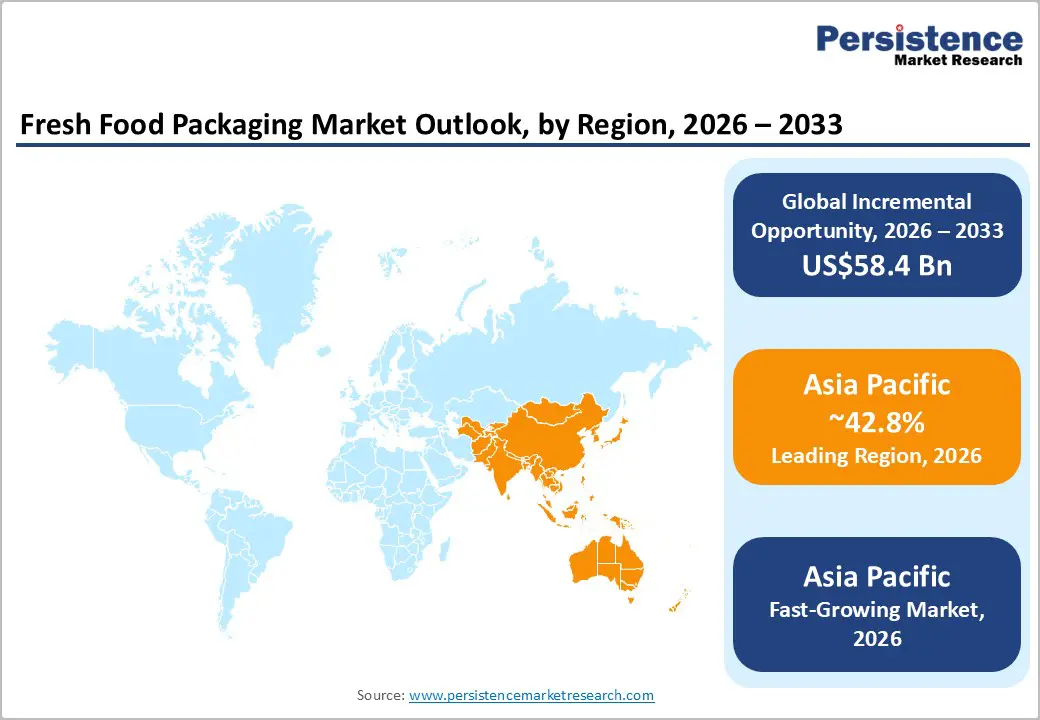

- Leading Region: Asia Pacific is projected to hold 42.8% share, driven by rapid urbanization, retail modernization, and strong manufacturing capacity across China, India, and ASEAN economies.

- Fastest-growing Region: Asia Pacific is projected to expand at the highest regional growth rate through 2033, supported by cold-chain investments, export-oriented fresh produce trade, and rising middle-class consumption.

- Investment Plans: Capital allocation is concentrated on recyclable mono-material packaging, post-consumer recycled (PCR) integration, barrier-coated fiber technologies, automation, and active/intelligent packaging solutions to align with regulatory and retailer sustainability mandates.

- Dominant Material: Plastic is anticipated to account for approximately 38.4% of the market, supported by its cost efficiency, transparency, and superior barrier properties for dairy, meat, and fresh produce applications.

- Leading Packaging Type: Rigid packaging is estimated to represent approximately 49.8% share, driven by strong demand for trays, clamshells, and tubs in meat, seafood, dairy, and fresh produce segments.

| Key Insights | Details |

|---|---|

| Fresh Food Packaging Market Size (2026E) | US$134.2 Bn |

| Market Value Forecast (2033F) | US$192.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Organized Retail, E-Commerce, and Cold-Chain Infrastructure

The rapid development of organized retail formats and omnichannel grocery fulfillment models is increasing demand for packaging that extends shelf life, enhances protection, and supports traceability. Urbanization and rising disposable income levels in Asia Pacific, Latin America, and parts of Africa are expanding the consumption of packaged fresh products. Cold-chain investments reduce post-harvest losses and improve distribution efficiency, increasing the economic value of protective packaging. Improved refrigeration, temperature monitoring, and logistics infrastructure support greater penetration of packaged fruits, vegetables, dairy, and meat products. Higher volumes of rigid trays, modified atmosphere packaging (MAP), breathable barrier films, and resealable formats. Packaging with enhanced protection capabilities commands premium pricing and supports reduced spoilage losses across the supply chain.

Regulatory and Corporate Push for Recyclability and Circularity

Governments across North America, Europe, and parts of Asia are implementing packaging waste regulations that mandate recyclability performance, recycled content targets, and labeling transparency. Corporate sustainability commitments from major retailers and food brands are reinforcing these requirements. The result is accelerated redesign of fresh food packaging toward mono-material structures, increased use of post-consumer recycled (PCR) plastics, and greater investment in fiber-based alternatives. While short-term costs increase due to reformulation and equipment upgrades, medium-term differentiation opportunities emerge for converters that offer compliant, recyclable, and lower-carbon solutions. Expanded research and development spending on recyclable films, paper-based barriers, and mono-polymer rigid trays, increasing overall addressable value within sustainable fresh food packaging.

Technology Adoption: Active, Intelligent Packaging, and Automation

Active packaging technologies, including oxygen scavengers and moisture regulators, reduce spoilage and extend product freshness. Intelligent packaging solutions, such as freshness indicators, RFID tags, and digital traceability features, enhance supply chain transparency and consumer confidence. Simultaneously, automation and digital quality control systems improve manufacturing precision and reduce per-unit costs. These technologies enable the production of complex formats such as pre-washed salads and ready-to-eat fruit portions at scale. Higher margins for value-added packaging formats, new service-based business models combining packaging and data analytics, and faster SKU proliferation across premium fresh categories.

Barrier Analysis -Raw Material Price Volatility and Capital Expenditure Requirements

Fluctuations in polymer and fiber prices directly affect converter margins. Transitioning to recyclable mono-material solutions or fiber-based alternatives requires significant capital investment in new equipment and process redesign. Companies with limited pricing power may experience EBITDA compression during transition periods. Smaller converters face consolidation risks as compliance and investment requirements increase. These structural cost pressures slow short-term adoption of advanced sustainable formats despite long-term demand.

Regulatory Complexity and Food-Safety Compliance

Food contact regulations vary by region and often require extensive validation testing for new materials, particularly recycled plastics. Achieving both recyclability compliance and food-safety certification creates technical and administrative challenges. Approval timelines for innovative materials can extend beyond 12-24 months in certain jurisdictions, delaying commercialization and increasing development expenses. Regulatory fragmentation increases operational complexity, particularly for companies operating across multiple regions.

Opportunity Analysis -Sustainable Material Substitution and Fiber Barrier Innovation

The shift away from multi-layer plastics toward recyclable mono-materials and fiber-based packaging presents a significant repositioning opportunity. With plastic currently leading and paper & paperboard identified as the fastest-growing segment, converters investing in scalable fiber-barrier technology and recyclable structures are well positioned for long-term growth. Retailers increasingly prioritize recyclable and low-carbon packaging in fresh produce categories. This transition represents a multi-billion-dollar opportunity by 2030 for companies capable of delivering functional, compliant, and cost-competitive alternatives.

Smart Packaging and Integrated Service Models

The integration of freshness sensors, QR codes, and traceability platforms enables packaging to provide both protection and data services. Even limited adoption across fresh SKUs can generate meaningful incremental revenue streams. High-value categories such as ready-to-eat salads, premium berries, and specialty dairy offer early adoption potential. Packaging suppliers that combine material innovation with digital services can differentiate themselves through performance guarantees, spoilage-reduction metrics, and consumer-engagement tools.

Category-wise Analysis

Material Insights

Plastic is anticipated to account for approximately 38.4% of market share in 2026, maintaining its position as the leading material due to cost efficiency, process versatility, transparency, and superior barrier performance. Polyethylene terephthalate (PET), polyethylene (PE), polypropylene (PP), and engineered polymers are extensively used across thermoformed trays, clamshells, lidding films, and modified atmosphere packaging (MAP) structures. These materials offer excellent moisture and oxygen barriers, which are essential for preserving freshness and extending shelf life. Plastic formats support high-volume processing, resealability, and product visibility, making them critical for fresh produce, meat, poultry, seafood, and dairy applications. For example, PET trays and PE-based lidding films are widely adopted for fresh meat and ready-to-eat salads due to clarity and seal integrity. Ongoing investments in post-consumer recycled (PCR) content integration, downgauging, and lightweighting initiatives reflect industry efforts to balance functional performance with evolving sustainability and regulatory expectations.

The paper and paperboard segment is expected to emerge as the fastest-growing material segment as retailers and regulators increasingly prioritize recyclability, renewable sourcing, and reduced plastic content. Growth is supported by advances in barrier coatings, dispersion technologies, and laminated fiber structures that enhance resistance to moisture, grease, and oxygen while maintaining recyclability in established paper waste streams. The adoption is strongest in bakery products, portioned ready meals, and selected fresh produce applications such as mushrooms, berries, and apples, where sustainability perception plays a decisive role in consumer choice. Examples include molded fiber trays with thin barrier linings and paper-based cartons with functional coatings for fresh-cut produce. Expansion is further supported by retailer commitments to fiber-first packaging strategies and rising consumer preference for packaging formats perceived as environmentally responsible.

Packaging Type Insights

Rigid packaging is anticipated to hold approximately 49.8% of market share in 2026, making it the dominant packaging type in the market. Formats such as trays, clamshells, tubs, and rigid containers provide superior mechanical protection, stackability, and tamper evidence, which are essential for maintaining product integrity across complex supply chains. These attributes make rigid packaging particularly suitable for meat, seafood, dairy, eggs, and delicate fresh produce. Rigid packaging also supports premium shelf presentation and branding differentiation through shape, clarity, and labeling compatibility. For example, rigid PET clamshells are commonly used for berries, while polypropylene tubs dominate yogurt and fresh dairy applications. Manufacturers are increasingly incorporating lightweight designs, mono-material constructions, and recyclable rigid formats to meet sustainability mandates without compromising structural performance.

Flexible packaging is projected to be the fastest-growing packaging type over the forecast period. Lightweight properties significantly reduce transportation costs, material usage, and overall environmental footprint compared to rigid alternatives. Flexible formats include films, pouches, sachets, and lidding materials used across fresh produce, ready-to-eat meals, and processed fresh foods. Technological improvements in high-barrier films, resealable closures, and modified atmosphere compatibility extend product shelf life, particularly for fresh-cut fruits, salads, and protein portions. For instance, breathable films are increasingly used for leafy greens, while high-barrier pouches support vacuum-sealed fresh meats. Flexible solutions are also well-suited to e-commerce and home-delivery distribution due to space efficiency, durability, and reduced breakage risk during transit.

Regional Insights

North America Fresh Food Packaging Market Trends - Omni-channel Retail Expansion and PCR-Driven Packaging Innovation

North America remains a high-value and innovation-driven market, supported by advanced cold-chain infrastructure, high labor productivity, and strong retail consolidation. The U.S. accounts for the majority of regional demand, underpinned by high per-capita consumption of packaged fresh foods and the rapid penetration of e-grocery and meal-kit services. Major retailers such as Walmart, Kroger, and Costco continue to expand fresh and private-label assortments, increasing demand for standardized, scalable packaging formats with consistent performance across distribution channels.

Key growth drivers include omnichannel grocery fulfillment, stringent food safety requirements, and retailer-led sustainability initiatives. Regulatory frameworks enforced by the U.S. Food and Drug Administration (FDA) and the U.S. Department of Agriculture (USDA) influence packaging material selection, labeling, and barrier performance, particularly for meat, poultry, and dairy products. In parallel, state-level policies in California and Washington targeting recycled content and plastic reduction are accelerating the adoption of PCR-integrated rigid trays and recyclable flexible films.

Investment activity in the region is concentrated on automation, active packaging technologies, and recycled content integration. Companies such as Amcor and Berry Global have expanded recyclable film portfolios and PCR capacity in North America, directly supporting retailer commitments to circular packaging targets. Strategic collaborations between packaging suppliers and retailers, including traceability pilots using smart labels and QR-enabled packaging, are strengthening supply-chain transparency and reducing food loss across fresh categories.

Europe Fresh Food Packaging Market Trends - EU Circular Economy Regulation Accelerating Fiber and Mono-Material Formats

Europe continues to demonstrate global leadership in regulatory harmonization and circular packaging implementation, shaping material innovation and procurement strategies across the fresh food packaging market. Germany, the U.K., France, and Spain collectively drive regional demand, supported by high fresh food consumption and strong supermarket penetration across meat, dairy, and fresh produce categories. Retail groups such as Tesco, Carrefour, Aldi, and Lidl play a central role in accelerating packaging transitions through private-label standards and supplier compliance requirements.

European Union policies, including the Packaging and Packaging Waste Regulation (PPWR) and extended producer responsibility (EPR) schemes, are materially influencing packaging design and material substitution. These regulations favor mono-material plastics, recyclable flexible films, and fiber-based packaging solutions, while discouraging complex multilayer structures that hinder recycling. As a result, packaging manufacturers such as Smurfit Kappa and DS Smith have increased investment in barrier-coated paperboard and fiber-based fresh food formats suitable for meat trays, produce punnets, and bakery packaging.

Southern Europe’s export-oriented fresh produce markets, particularly in Spain and Italy, continue to drive demand for lightweight, protective packaging that balances shelf-life extension with sustainability compliance. Investment across the region is focused on recyclable film development, barrier dispersion technologies, and compliance infrastructure to meet tightening regulatory thresholds. These dynamics position Europe as a reference market for sustainable fresh food packaging adoption globally.

Asia Pacific Fresh Food Packaging Market Trends - Urbanization, Cold-Chain Scale, and High-Volume Growth Leadership

Asia-Pacific is expected to account for 42.8% of global fresh food packaging revenue in 2026, making it both the largest and fastest-growing regional market. Growth is driven by rapid urbanization, rising middle-class incomes, dietary shifts toward packaged fresh foods, and the continued expansion of modern retail and foodservice infrastructure. Large population bases combined with improving cold-chain logistics create sustained demand for scalable, cost-efficient packaging solutions across fresh categories.

China leads the region in manufacturing capacity and domestic consumption, supported by large-scale packaging producers such as Yuto Packaging and Greatview Aseptic Packaging, which supply rigid and flexible formats for dairy, produce, and protein markets. Government-backed cold-chain expansion initiatives and stricter food safety enforcement are increasing demand for high-barrier packaging and MAP solutions. In India, organized retail players such as Reliance Retail and Tata Group-backed BigBasket are expanding fresh food distribution, driving uptake of standardized trays, films, and pouches compatible with longer distribution cycles.

Japan maintains technological leadership in active and intelligent packaging, with companies such as Toppan and Mitsubishi Chemical Group advancing oxygen-absorbing films and freshness-monitoring technologies. Across ASEAN economies, investment is focused on production capacity expansion, recyclable flexible films, and export-grade packaging to support fresh seafood, fruits, and vegetables destined for global markets. Collectively, these developments reinforce Asia Pacific’s central role in shaping global fresh food packaging supply and innovation trajectories.

Competitive Landscape

The global fresh food packaging market combines large multinational packaging companies with a fragmented base of regional converters. Global leaders maintain competitive advantages in advanced barrier technologies, aseptic systems, and sustainable material innovation. Regional players compete on cost, customization, and localized service. Consolidation trends reflect the need for scale and compliance capability.

Key strategies include sustainability-driven redesign, integration of recycled content supply chains, expansion into high-growth emerging markets, and digital traceability services. Market leaders differentiate through proprietary barrier technologies, compliance readiness, and global manufacturing footprints.

Key Industry Developments

- In July 2025, Dow introduced its INNATE™ TF 220 Precision Packaging Resin, enhancing recyclability and performance for flexible packaging films used across fresh food and other consumer goods, while also improving manufacturing efficiency.

- In March 2025, Placon launched its Fresh ’n Clear Dip Cup range, targeting eco-friendly thermoformed packaging for dips, spreads, and fresh food accompaniments.

Companies Covered in Fresh Food Packaging Market

- Amcor plc

- Tetra Pak International S.A.

- Berry Global Inc.

- Huhtamaki Oyj

- Sealed Air Corporation

- Mondi plc

- Smurfit Westrock plc

- Sonoco Products Company

- ALPLA Group

- DS Smith plc

- Constantia Flexibles Group GmbH

- Winpak Ltd.

- Coveris Holdings S.A.

- Greiner Packaging International GmbH

- Genpak LLC

- Pactiv Evergreen Inc.

- WestRock Company

- International Paper Company

Frequently Asked Questions

The global fresh food packaging market is projected to be valued at US$134.2 billion in 2026.

The fresh food packaging market is expected to reach US$192.6 billion by 2033.

Key trends include rising adoption of recyclable and mono-material packaging, integration of post-consumer recycled (PCR) content, expansion of active and intelligent packaging technologies, growth in flexible packaging formats, and increasing demand driven by e-grocery and cold-chain development in emerging markets.

Rigid packaging is the leading segment, accounting for approximately 49.8% share in 2026, driven by strong demand across meat, seafood, dairy, and fresh produce categories.

The fresh food packaging market is expected to grow at a CAGR of 5.3% between 2026 and 2033.

Major players include Amcor plc, Tetra Pak International S.A., Berry Global Inc., Huhtamaki Oyj, and Sealed Air Corporation (Cryovac).