- Specialty & Fine Chemicals

- Flocculants and Coagulants Market

Flocculants and Coagulants Market Size, Share, and Growth Forecast 2026 - 2033

Flocculants and Coagulants Market by Product Type (Coagulant, Flocculant) and End-use Industry (Municipal Wastewater Treatment, Mining & Mineral Processing, Pulp & Paper, Oil & Gas, Others), and Regional Analysis for 2026 - 2033

Flocculants and Coagulants Market Size and Trend Analysis

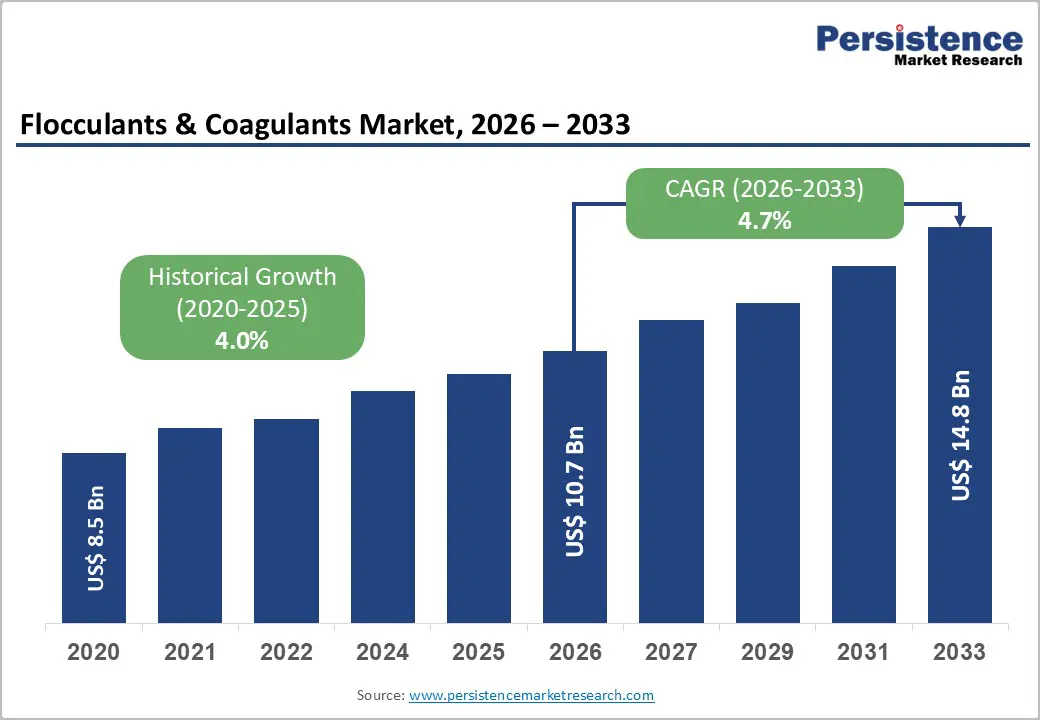

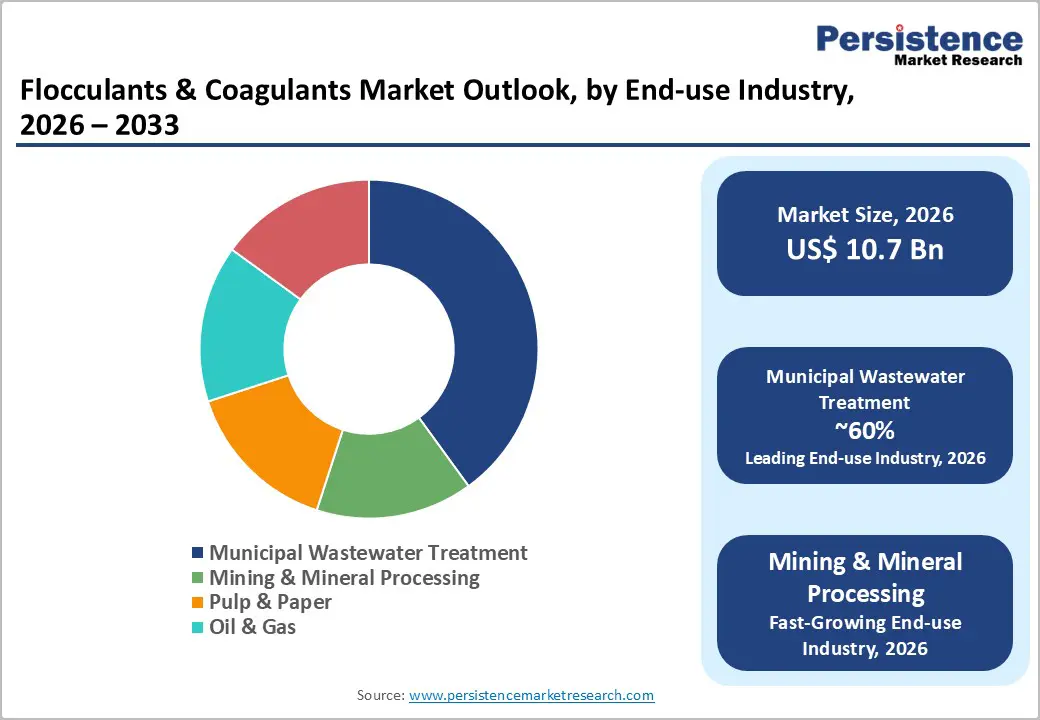

The global Flocculants and Coagulants market size is supposed to be valued at US$ 10.7 billion in 2026 and is projected to reach US$ 14.8 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

Sustained market expansion is principally supported by the rising global demand for potable water and industrial wastewater treatment, coupled with the enforcement of increasingly stringent discharge regulations across major economies. Significant federal investment in water infrastructure in the United States, most notably through the Bipartisan Infrastructure Law, which allocated over USD 50 billion for improvements in drinking water, wastewater, and stormwater systems, reinforces long-term chemical demand. Parallel public-sector spending initiatives in the Asia Pacific and Europe further strengthen the outlook, creating a stable and enduring requirement for coagulation and flocculation solutions throughout the forecast period.

Key Industry Highlights:

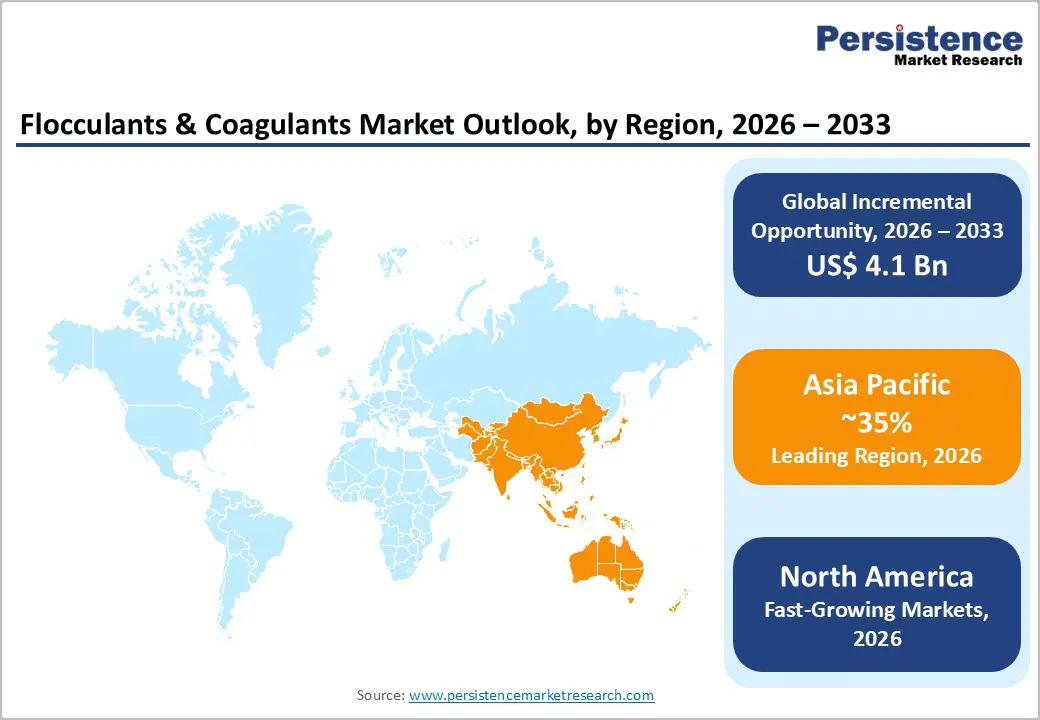

- Leading Region: Asia Pacific dominates the global Flocculants and Coagulants market, with 35% market share, driven by China, India, Japan, and Indonesia's rapid industrial growth, rising municipal treatment investment, and national environmental regulations mandating large-scale wastewater treatment chemical adoption.

- Fastest Growing Region: North America is the fastest-growing region through 2033, with a comprehensive federal regulatory framework in the U.S., including the Safe Drinking Water Act, the Clean Water Act, and the EPA’s National Pollutant Discharge Elimination System, imposing rigorous treatment standards on over 150,000 public water systems.

- Dominant Segment: The Coagulant product type holds the dominant share, with approximately 55% share of the total market, underpinned by its critical role in charge neutralization in water treatment, broad pH compatibility, and widespread use across municipal, pulp and paper, and industrial applications.

- Fastest Growing Segment: Mining and Mineral Processing is the fastest-growing end-use segment, fueled by accelerating global demand for critical minerals, lithium, cobalt, and copper, generating large volumes of process wastewater requiring specialty high-performance flocculants for solid-liquid separation.

- Key Opportunity: Bio-based flocculants derived from natural sources such as chitosan, moringa oleifera, and guar gum present a high-value opportunity, supported by EU and U.S. sustainability mandates and early commercialization by leaders including Kemira Oyj and SNF Group.

| Key Insights | Details |

|---|---|

|

Flocculants and Coagulants Market Size (2026E) |

US$ 10.7 Bn |

|

Market Value Forecast (2033F) |

US$ 14.8 Bn |

|

Projected Growth CAGR (2026–2033) |

4.7% |

|

Historical Market Growth (2020–2025) |

4.0% |

Market Dynamics

Drivers - Rise in Global Demand for Clean Water and Wastewater Treatment Infrastructure

Access to safe drinking water and adequate sanitation remains one of the most pressing global challenges of the twenty-first century. The United Nations reports that approximately 703 million individuals still lack basic safe drinking water, while over 2 billion people remain without safely managed drinking water services. Rapid urbanization further intensifies this strain. According to World Bank projections, the global urban population is expected to more than double by 2050, with nearly 70% of people living in cities.

Such accelerated growth places substantial pressure on existing water treatment systems and necessitates sustained investment across Asia, Africa, and Latin America. Flocculants and coagulants continue to play an indispensable role in primary water and wastewater treatment. In the United States, stringent requirements under the Safe Drinking Water Act and Clean Water Act ensure consistent demand for these treatment chemicals.

Stringent Regulatory Mandates Compelling Industrial Wastewater Treatment Adoption

The enforcement of increasingly stringent effluent standards by national and supranational regulatory authorities remains a fundamental driver of demand for flocculants and coagulants. In the United States, the Environmental Protection Agency’s National Pollutant Discharge Elimination System regulates wastewater discharges from tens of thousands of industrial and municipal facilities, reinforcing the need for advanced treatment solutions.

A significant regulatory milestone occurred in April 2024 with the introduction of the first federal drinking water standards for PFAS, expanding mandatory treatment requirements for public water systems. Concurrently, the European Union’s revised Urban Wastewater Treatment Directive and Water Framework Directive impose advanced treatment obligations across member states, compelling major industrial sectors to adopt coagulation-flocculation technologies to meet stringent limits on solids, metals, and emerging contaminants.

Restraints - Emergence of Alternative Water Treatment Technologies

The flocculants and coagulants market faces growing competitive pressure from alternative and emerging water treatment technologies, including electrocoagulation, membrane filtration, and advanced oxidation processes (AOPs). Electrocoagulation, in particular, generates coagulant ions electrochemically — eliminating the need for external chemical dosing — while also producing less sludge than conventional coagulation, making it attractive for industrial applications with zero-liquid-discharge mandates. As the capital costs of membrane systems and electrochemical reactors continue to decline through technology maturation and scale, certain high-specification industrial end users - particularly in the semiconductor, pharmaceutical, and food processing sectors - may shift toward these alternatives, moderating the growth rate for chemical coagulant and flocculant consumption in these specific segments over the medium term.

Volatility in Raw Material Prices and Supply Chain Disruptions

A persistent challenge for flocculant and coagulant manufacturers is the volatility in prices of key raw materials, including acrylamide monomer for polyacrylamide-based flocculants, aluminum sulfate, ferric chloride, and petrochemical derivatives. These inputs are subject to energy price fluctuations, geopolitical supply disruptions, and demand competition from other polymer-intensive industries. Cost escalations compress operating margins for mid-tier producers and can trigger price increases for end users, particularly in price-sensitive municipal markets operating under multi-year procurement contracts. This dynamic was evident when SNF Group committed a USD 300 million capacity expansion in the United States in November 2022, partly to vertically integrate feedstock and reduce exposure to acrylamide supply-chain volatility across its North American manufacturing base.

Opportunities - Bio-based and Sustainable Flocculants Emerging as a High-Value Growth Frontier

The shift toward green chemistry represents a significant and time-critical opportunity within the global flocculants and coagulants market. Rising scientific and regulatory concerns over the environmental persistence of synthetic polyacrylamide and related monomers in treated water and biosolids are accelerating the adoption of bio-based alternatives sourced from materials such as chitosan, moringa oleifera, starch derivatives, and guar gum. Research advancements, including those by the Fraunhofer Institute for Interfacial Engineering and Biotechnology, have demonstrated the effectiveness of bio-based functionalized flocculants in treating complex industrial effluents.

The commercial launch of bio-flocculants by Kemira Oyj in January 2025 and SNF Group’s 32.5% production expansion in 2023 further underscore market readiness. With EU and U.S. sustainability frameworks increasingly favoring biodegradable chemistry, early adopters are positioned to secure premium pricing and long-term municipal contracts.

Critical Mineral Mining Expansion Driving Demand for Specialty Mineral-Processing Flocculants

The accelerating global energy transition, particularly the expansion of electric mobility and renewable energy infrastructure, is generating exceptional demand for critical minerals such as lithium, cobalt, copper, and nickel, which serve as essential inputs for electric vehicle batteries, wind turbines, and large-scale energy storage systems. Mining and mineral processing activities associated with these commodities produce substantial volumes of process water and tailings, requiring advanced solid–liquid separation supported by specialty flocculants.

According to the International Energy Agency, demand for critical minerals may increase up to sixfold by 2040 under net-zero scenarios. This opportunity was further emphasized in November 2024 when Solenis LLC acquired BASF SE’s comprehensive mining flocculants portfolio, enhancing its position as a full-service provider for mineral processing. Specialty flocculants engineered for saline environments now enable up to 90% water recovery in copper and lithium tailings operations, supporting continued market expansion.

Category-wise Analysis

Product Type Insights

The coagulant segment remains the leading product category in the global flocculants and coagulants market, accounting for approximately 55% of total revenue. This dominance reflects the essential and irreplaceable role of coagulants in charge neutralization, a prerequisite for effective flocculation and efficient particle aggregation. Inorganic coagulants, such as aluminum sulfate, ferric sulfate, polyaluminum chloride, and sodium aluminate, continue to prevail across municipal drinking water and wastewater treatment due to their cost efficiency, broad pH tolerance, and strong regulatory acceptance.

Within the flocculant segment, cationic variants are expanding most rapidly, particularly in pulp and paper applications where they enhance fiber retention and drainage. Organic coagulants like polyDADMAC and polyamine are also gaining traction in processes requiring reduced sludge generation and reliable performance under low-temperature conditions.

Industry Insights

Municipal wastewater treatment remains the leading end-use segment in the global flocculants and coagulants market, accounting for nearly 40% of total revenue. Its dominance stems from the essential role of coagulation–flocculation processes in potable water production and sewage treatment, including turbidity control, removal of dissolved organic matter, phosphorus precipitation, and pathogen reduction.

With the United Nations projecting that 68% of the world’s population will reside in urban areas by 2050, pressures on municipal treatment infrastructure are expected to intensify. In the United States, the EPA’s 2024 PFAS drinking water standards are prompting utilities to upgrade treatment systems, further increasing coagulant demand. The pulp and paper industry represents the second-largest segment, while mining and mineral processing remain the fastest-growing category due to rising global extraction of critical minerals such as lithium and copper.

Regional Insights

North America Flocculants and Coagulants Market Trends

North America represents a structurally significant and mature market for flocculants and coagulants, led predominantly by the United States, which accounts for more than 85% of regional demand. This position is reinforced by a comprehensive federal regulatory framework, including the Safe Drinking Water Act, the Clean Water Act, and the EPA’s National Pollutant Discharge Elimination System, imposing rigorous treatment standards on over 150,000 public water systems and more than 40,000 industrial discharge facilities.

The Bipartisan Infrastructure Law, allocating over USD 50 billion to water infrastructure improvements, further strengthens long-term demand. In 2024, the EPA’s finalization of PFAS drinking water limits prompted widespread adoption of advanced coagulation processes. Canada also contributes significantly through its oil sands and base metals mining sectors, while the region continues to serve as a global hub for innovation, with leading companies such as Ecolab Inc. and Solenis LLC advancing sustainable and digital water chemistry solutions.

Europe Flocculants and Coagulants Market Trends

Europe represents a mature yet steadily evolving market, defined by stringent environmental regulations and an increasing focus on sustainable, circular water management practices. The European Union’s revised Urban Wastewater Treatment Directive and Water Framework Directive mandate advanced treatment standards across member states, ensuring consistent long-term demand for chemical treatment solutions. Major markets, including Germany, France, Spain, and the United Kingdom, benefit from extensive industrial and municipal water treatment infrastructure.

Kemira Oyj has demonstrated strong regional commitment, announcing in November 2023 a capacity expansion at its Goole, UK facility to achieve an annual ferric sulfate output of 70,000 tons by 2025. Simultaneously, the EU Green Deal is accelerating the adoption of bio-based flocculants, while producers such as Feralco AB continue to support niche high-purity inorganic coagulant applications across Northern and Western Europe.

Asia Pacific Flocculants and Coagulants Trends

Asia Pacific remains the largest regional market for flocculants and coagulants, with 35% market share, supported by rapid industrial expansion, accelerating urbanization, rising critical mineral extraction, and increasingly stringent environmental regulations. China, India, Japan, and Indonesia constitute the core demand centers. China continues to advance comprehensive national environmental standards under its “Beautiful China” initiative, driving major upgrades to industrial and municipal wastewater treatment systems and sustaining high consumption of coagulation-flocculation chemicals.

India represents an especially strong growth opportunity, with the AMRUT 2.0 program allocating over INR77,640 crore to enhance urban water supply and sewage infrastructure across more than 500 cities. Reflecting this momentum, Kurita Water Industries Ltd. established a dedicated local subsidiary in June 2024. Additionally, the region’s expanding mining operations, including lithium extraction in Australia, nickel mining in Indonesia, and bauxite processing in Southeast Asia, continue to elevate demand for high-performance mineral-processing flocculants.

Competitive Landscape

The global flocculants and coagulants market is characterized by a moderately fragmented competitive structure, with a select group of multinational chemical corporations exerting substantial influence over supply, pricing dynamics, and technological innovation. Leading firms, such as SNF Group, Kemira Oyj, Ecolab Inc., and Solenis LLC, maintain their positions through vertical integration, broad manufacturing footprints, and proprietary polymer technologies. Emerging competitive advantages include advancements in bio-based flocculant platforms, AI-enabled dosing systems, and digital water-management service models, while regional players remain active in niche, innovation-driven segments.

Key Developments:

- February 2026: Kemira Oyj announced the acquisition of SIDRA Wasserchemie, a family-owned coagulant producer with two production facilities in Germany, serving customers in Germany, Belgium, and the Netherlands. The purchase price is approximately EUR 75 million.

- November 2024: Solenis LLC completed the acquisition of BASF SE's mining flocculants portfolio, including Magnafloc®, Rheomax®, Alclar®, and Jetwet®, significantly expanding its mineral processing capabilities and global mining customer base.

- September 2024: Kemira Oyj announced expansion of coagulant production capacity at its Fredrikstad, Norway manufacturing facility to address growing demand across Nordic markets, with new capacity scheduled for commissioning by end of 2025.

Top Companies in Flocculants and Coagulants Market

SNF Group (France) is the world's largest manufacturer of polyacrylamide-based flocculants and a preeminent force in the global water treatment chemicals industry. Operating manufacturing facilities across North America, Europe, Asia, and Latin America, the company commands a commanding share of global flocculant supply. Its commitment of USD 300 million for capacity expansion in Plaquemine, Louisiana, announced in November 2022, adding 30,000 metric tons per year of powder polyacrylamide, demonstrates the company's strategy of scale-driven, vertically integrated growth to meet rising global demand.

Kemira Oyj (Helsinki, Finland) is a globally recognized water chemistry company serving water-intensive industries with a broad portfolio spanning inorganic coagulants, synthetic flocculants, and pioneering bio-based solutions. The company's vertically integrated monomer-to-polymer manufacturing model and regional production network provide significant cost stability and technical service advantages. Active investments, including the USD 80 million facility upgrade in Alabama, U.S., completed in 2021 and ongoing capacity expansions in the U.K. and Norway, reinforce Kemira's long-term growth trajectory in both established and emerging markets.

Ecolab Inc. (Minnesota, U.S.) is a global leader in water, hygiene, and infection prevention solutions, with its Nalco Water division being a dominant force in industrial water treatment chemistry. The company's acquisition of Barclay Water Management for approximately USD 50 million in November 2024 integrates real-time digital water quality monitoring with chemical treatment, enabling clients to optimize flocculant and coagulant dosing dynamically. Ecolab's scale, technology integration capabilities, and global service network across 170+ countries position it as a leading value-added chemicals and services partner in the global market.

Companies Covered in Flocculants and Coagulants Market

- SNF Group

- Kemira Oyj

- BASF SE

- Ecolab Inc.

- Solenis LLC

- SUEZ Group

- Evoqua Water Technologies

- Solvay SA

- Kurita Water Industries Ltd.

- Feralco AB

- Ashland Inc.

- IXOM Holdings Pty Ltd.

- Buckman Laboratories, Inc.

Frequently Asked Questions

The global Flocculants and Coagulants market is valued at US$ 10.7 Bn in 2026 and is projected to reach US$ 14.8 Bn by 2033, expanding at a compound annual growth rate (CAGR) of 4.7% over the forecast period from 2026 to 2033.

The primary demand drivers include escalating global need for safe drinking water and industrial wastewater treatment, rapid urbanization projected to reach 68% of the world population living in cities by 2050, and increasingly stringent regulatory mandates. Key regulatory frameworks, including the U.S. EPA's NPDES program covering over 40,000 industrial dischargers and the landmark PFAS drinking water standards finalized in April 2024, are compelling both municipalities and industries to deploy effective coagulation-flocculation treatment processes.

The Coagulant segment leads the global market, accounting for approximately 55% of total market revenue. This dominance is driven by the fundamental role of coagulants in the charge-neutralization phase of water treatment, with inorganic coagulants such as aluminum sulfate (alum), polyaluminum chloride (PAC), and ferric sulfate widely used across municipal drinking water systems due to their cost efficiency, broad pH compatibility, and established regulatory acceptance.

Asia Pacific is the dominant regional market, led by China, India, Japan, and Indonesia. The region's leadership reflects its rapid industrialization, mounting municipal water treatment investment, including India's AMRUT 2.0 program committing over INR77,640 crore to urban water infrastructure, and the expanding critical minerals mining sector, which generates substantial demand for specialty mineral-processing flocculants throughout the forecast period.

The most compelling emerging opportunity lies in the commercialization of bio-based and sustainable flocculants derived from natural sources, including chitosan, moringa oleifera, guar gum, and starch derivatives. Tightening sustainability procurement policies under the EU Green Deal, evolving U.S. environmental regulations, and growing corporate commitments to green chemistry are accelerating market acceptance