- Metals & Minerals

- Ferroniobium Market

Ferroniobium Market Size, Share, and Growth Forecast, 2026 – 2033

Ferroniobium Market by Grade Type (Standard, High Purity, Vacuum Grade), Application (HSLA Production, Steel Production, Superalloys, Automotive, Aerospace), and Regional Analysis for 2026 – 2033

Ferroniobium Market Size and Trends Analysis

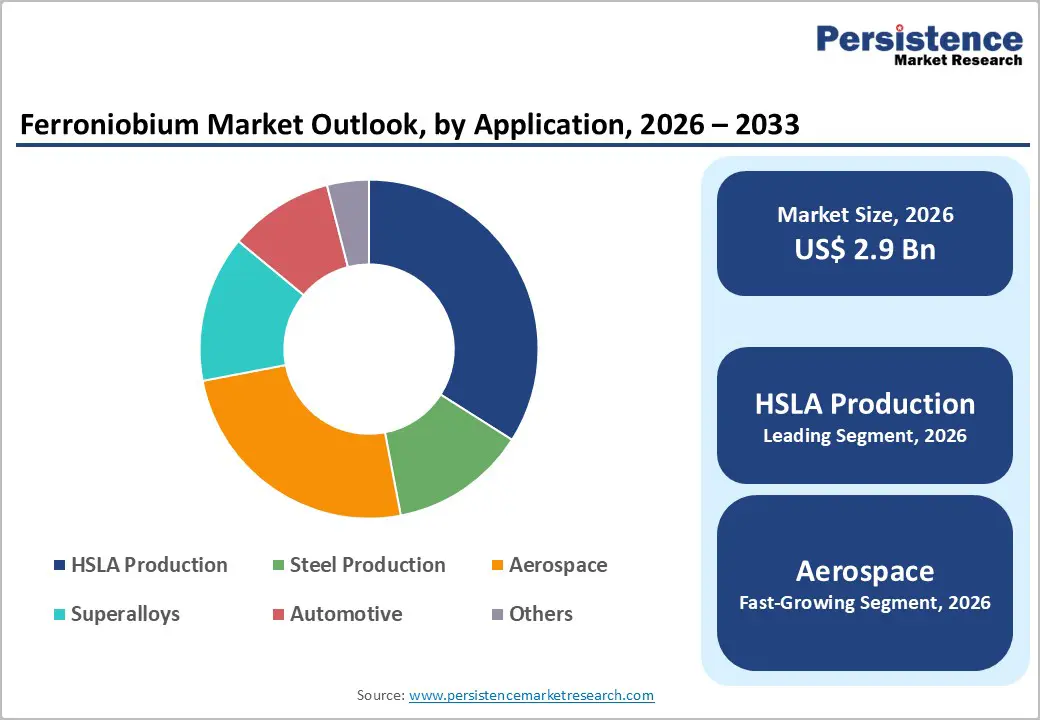

The global ferroniobium market size is likely to be valued at US$2.9 billion in 2026 and is expected to reach US$4.4 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by its essential role as a micro-alloying element in advanced steel production.

Ferroniobium, an alloy composed of iron and niobium, is widely used to enhance the mechanical properties of steel, including strength, toughness, weldability, and resistance to corrosion and high temperatures. Even in small quantities, ferroniobium significantly improves steel performance, making it a critical material for the production of high-strength low-alloy (HSLA) steels. These steels are extensively used in infrastructure projects such as bridges, buildings, pipelines, and rail systems, as well as in the automotive sector, where manufacturers aim to produce lighter and stronger vehicle components to improve fuel efficiency and safety. The demand for ferroniobium is closely linked to steel manufacturing trends and the expansion of the construction and transportation industries. Advancements in metallurgical technologies and the growing focus on lightweight yet durable materials are encouraging wider adoption of niobium-based alloys.

Key Industry Highlights:

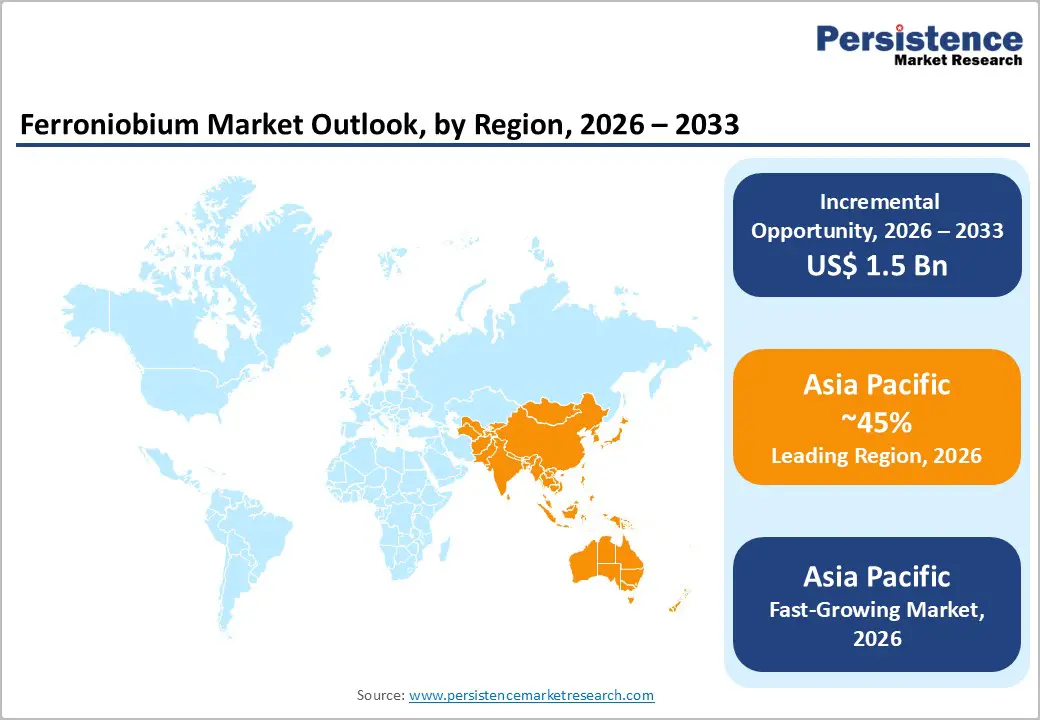

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by strong steel production and expanding infrastructure and automotive industries.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in ferroniobium in 2026, supported by rapid industrialization and rising demand from the automotive and construction sectors.

- Leading Grade Type: The standard grade is projected to represent the leading grade type in 2026, accounting for 65% of the revenue share, driven by its widespread use in HSLA and general steel production due to its cost-effectiveness and reliable performance.

- Leading Application: HSLA production is anticipated to be the leading application, accounting for over 70% of the revenue share in 2026, supported by increasing demand for high-strength steel in infrastructure, pipelines, and large-scale construction projects.

| Key Insights | Details |

|---|---|

| Ferroniobium Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$4.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for High-Strength Low-Alloy (HSLA) Steel in Infrastructure and Construction

Ferroniobium acts as a critical micro alloying element that enhances steel strength, weldability, and durability while allowing manufacturers to reduce material weight. Governments worldwide are investing heavily in bridges, rail networks, pipelines, and urban infrastructure, which require stronger and longer-lasting steel materials. HSLA steel produced using ferroniobium provides improved performance in demanding environments, making it ideal for modern construction projects. As countries continue expanding transportation networks and energy infrastructure, the use of ferroniobium-enhanced steel is becoming increasingly important for structural reliability and safety.

Another factor supporting this driver is the growing need for efficient construction materials that balance strength and cost. Ferroniobium allows steel producers to achieve higher performance levels using smaller alloying additions compared to traditional materials. This efficiency reduces overall steel consumption while maintaining structural strength, which is beneficial for large-scale projects. Pipeline construction for oil, gas, and water distribution requires steels capable of withstanding high pressure and harsh conditions. Ferroniobium-based HSLA steels meet these requirements effectively. With rapid urbanization and infrastructure development in emerging economies, demand for HSLA steel is expected to remain a major growth catalyst for the ferroniobium market.

Automotive Lightweighting and Fuel-Efficiency Regulations

Automakers are increasingly adopting advanced high-strength steels that incorporate ferroniobium to improve vehicle performance while reducing weight. Lighter vehicles consume less fuel and produce fewer emissions, making them essential for meeting strict environmental regulations. Ferroniobium helps improve the strength-to-weight ratio of steel, enabling manufacturers to design thinner yet stronger automotive components. This allows carmakers to maintain vehicle safety while reducing material usage. As automotive manufacturers continue focusing on efficiency and sustainability, ferroniobium demand is rising across vehicle production.

Government regulations aimed at lowering carbon emissions are accelerating this trend. Many countries have introduced stricter fuel-efficiency and emission standards that encourage the use of lightweight materials in vehicles. Ferroniobium-enhanced steels support these goals by enabling manufacturers to produce stronger body structures, chassis components, and safety systems with reduced weight. The transition toward electric vehicles is also contributing to material innovation in automotive manufacturing. EV producers require durable yet lightweight structural materials to offset battery weight. Ferroniobium alloyed steels provide an effective solution, making the automotive sector an important contributor to market growth.

Barrier Analysis - Regulatory and Environmental Hurdles in Mining

Niobium, the key element used to produce ferroniobium, is obtained from specialized ore deposits that require extensive mining operations. Governments and environmental agencies have implemented stringent regulations related to land use, water management, waste disposal, and emissions from mining activities. Compliance with these regulations increases operational costs for mining companies and can delay project approvals. These regulatory hurdles can limit new production capacity and restrict supply growth, ultimately influencing the availability of ferroniobium in markets.

Environmental concerns related to mining activities also contribute to this restraint. Communities and regulatory bodies increasingly demand sustainable mining practices that minimize environmental impact. Mining companies must invest in advanced technologies and responsible resource management to meet these expectations. While these improvements promote sustainability, they also increase operational complexity and capital expenditure. Permitting processes for new mines can take several years, slowing the development of new supply sources. These factors create potential supply constraints and market uncertainties, which can affect long-term production planning and investment in the ferroniobium industry.

Competition from Alternative Alloying Elements

Steel manufacturers often evaluate different alloying materials such as vanadium, titanium, and molybdenum to achieve specific mechanical properties in steel products. These elements can sometimes provide similar strengthening effects depending on the application. Steel producers may substitute ferroniobium with alternative alloying elements when cost conditions or material availability change. This flexibility in steelmaking formulations creates competitive pressure within the alloying materials market and may limit the growth potential of ferroniobium in certain applications.

Price fluctuations in alloying materials also influence substitution decisions within the steel industry. When ferroniobium prices increase or supply becomes constrained, manufacturers may shift toward other alloying solutions that provide comparable performance at lower cost. Ongoing research in metallurgy continues to develop new steel compositions that optimize material performance using different combinations of elements. Although ferroniobium remains highly effective for strengthening HSLA steels, the presence of viable alternatives introduces uncertainty in long-term demand patterns. This competitive landscape requires ferroniobium producers to maintain a stable supply and demonstrate clear performance advantages.

Opportunity Analysis - Emerging Applications in Renewable Energy and Electric Vehicles

The expansion of renewable energy infrastructure is creating new opportunities for the ferroniobium market. Renewable energy systems such as wind turbines, solar structures, and power transmission networks require high-strength materials capable of withstanding extreme environmental conditions. Ferroniobium-alloyed steels provide improved strength, durability, and resistance to fatigue, making them suitable for these demanding applications. As governments and energy companies invest in clean energy projects worldwide, the demand for advanced structural materials is increasing. Ferroniobium can support the production of stronger steel components used in turbine towers, transmission pipelines, and heavy-duty structural frameworks.

Electric vehicles are also contributing to new growth opportunities in the ferroniobium market. EV manufacturers require lightweight yet strong materials to compensate for the weight of battery systems. Ferroniobium-enhanced steel can improve structural strength without significantly increasing material weight, making it useful for vehicle frames and safety components. In addition, expanding EV production is driving demand for stronger steel used in charging infrastructure and transportation systems. As economies increasingly adopt sustainable energy systems and electrified transportation, ferroniobium plays an important role in advanced engineering materials.

Technological Advancements in High Purity Grades

Technological progress in metallurgy and refining processes is creating opportunities for the development of high-purity ferroniobium grades. These specialized materials contain minimal impurities and are designed for high-performance applications that require exceptional strength and stability. Industries such as aerospace, defense, and advanced manufacturing demand materials that can perform reliably under extreme temperatures and mechanical stress. High-purity ferroniobium is increasingly used in superalloys and specialty steels for these applications. As research and development efforts continue to improve alloy processing techniques, manufacturers are able to produce more advanced grades of ferroniobium with enhanced properties.

The growing demand for specialized materials in high-technology industries is supporting this opportunity. Aerospace manufacturers require materials that can maintain strength and corrosion resistance in high-temperature environments. High-purity ferroniobium contributes to the production of advanced alloys used in aircraft engines, turbines, and other critical components. Improved refining technologies also allow producers to achieve greater consistency and quality in ferroniobium products. These advancements expand the potential applications of ferroniobium beyond traditional steelmaking, enabling suppliers to capture new market segments in high-value industrial sectors.

Category-wise Analysis

Grade Type Insights

Standards are expected to lead the ferroniobium market, accounting for approximately 65% of revenue in 2026, driven by their widespread use in steelmaking applications. This grade is primarily utilized in the production of high-strength low-alloy (HSLA) steels and conventional carbon steels used across construction, transportation, and energy infrastructure. Steel manufacturers prefer standard grade ferroniobium because it offers an effective balance between performance and cost, enabling improved strength, weldability, and durability without significantly increasing production expenses. For example, the production of HSLA steel plates used in long-distance oil and gas pipelines, where standard grade ferroniobium improves structural strength and resistance to pressure.

The high purity segment is likely to represent the fastest-growing segment, supported by its increasing use in advanced metallurgical and high-performance applications. This grade contains very low impurity levels, making it suitable for industries that require materials with high reliability and consistent performance. Sectors such as aerospace, defense, and specialized manufacturing rely on high purity ferroniobium to produce superalloys and high-performance steels capable of operating under extreme temperatures and mechanical stress. For example, high purity ferroniobium is used in the production of aerospace superalloys applied in aircraft engine components, where material consistency and strength are critical.

Application Insights

HSLA production is projected to lead the market, capturing around 70% of the revenue share in 2026, supported by its extensive use in strengthening steel for infrastructure and industrial applications. Ferroniobium acts as a micro-alloying element that significantly improves the mechanical properties of HSLA steel, including strength, toughness, and resistance to wear and corrosion. These properties make HSLA steel highly suitable for demanding structural applications such as bridges, pipelines, railways, and heavy construction equipment. For example, the use of HSLA steel in oil and gas pipelines, where ferroniobium-enhanced steel provides the strength needed to withstand high pressure and harsh environmental conditions.

Aerospace is likely to be the fastest-growing application, driven by the increasing focus on lightweight and high-performance materials. Manufacturers in these industries require advanced alloys that provide superior strength while reducing overall structural weight. The aerospace industry demands materials capable of maintaining structural integrity under extreme conditions such as high temperatures and mechanical stress. Ferroniobium contributes to the production of advanced superalloys used in aircraft engines and structural components. For example, niobium-containing superalloys are utilized in jet engine turbine parts where durability and heat resistance are critical. As technological innovation continues to shape transportation industries, the demand for advanced alloy materials is increasing.

Regional Insights

North America Ferroniobium Market Trends

North America is likely to be a significant market for ferroniobium, driven by steady demand from the region’s mature steel and automotive industries, where ferroniobium is widely used to enhance steel strength, toughness, and corrosion resistance. In the U.S. and Canada, infrastructure maintenance and modernization efforts continue to support HSLA steel consumption, driving consistent use of ferroniobium in structural applications such as bridges, pipelines, and heavy construction projects. Automotive manufacturers in the region also contribute to ferroniobium demand through the production of high-strength components that meet stringent safety and fuel efficiency standards.

A key trend in North America is the increasing focus on advanced materials for high-performance applications, including aerospace and defense. For example, Niobec Inc., known for its niobium production and supply of high-quality ferroniobium feedstock, supports regional metallurgical industries with specialized material solutions. Niobec’s capacity to provide consistent niobium-based products enables steelmakers and alloy producers to maintain quality and performance standards. Innovations in processing techniques and material formulations are enabling suppliers to meet the evolving needs of regional end-user sectors.

Europe Ferroniobium Market Trends

Europe is likely to be a significant market for ferroniobium, due to the region’s emphasis on advanced manufacturing, infrastructure renewal, and stringent environmental regulations that drive demand for high-performance steel grades. Steel producers across Germany, France, Italy, and Spain utilize ferroniobium extensively to manufacture high-strength low-alloy (HSLA) steels that offer superior strength, weldability, and corrosion resistance for construction, transportation, and heavy machinery. Investments in urban infrastructure upgrades and renewable energy projects, such as wind turbines and electric grid expansions, support ferroniobium consumption in structural applications.

Regulatory frameworks focused on sustainability and material efficiency also drive the adoption of high performance alloys that improve product longevity and recyclability, reinforcing ferroniobium's role in advanced steel production across the region. For example, Metallurgical Products India Pvt. Ltd. (MPI), which supplies ferroniobium to several steel manufacturers in Europe, helps them meet quality and performance requirements for specialty steels. MPI’s products are used in the production of HSLA steels that form critical components in European industrial sectors. This collaboration underscores how supply relationships support regional steelmaking needs, ensuring steel producers have consistent access to essential alloying materials.

Asia Pacific Ferroniobium Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by rapid industrialization, urbanization, and expansion of infrastructure projects across major economies such as China, India, Japan, and ASEAN countries. It is also the fastest-growing region. Strong steel production capacity in China is a major factor supporting ferroniobium consumption, as the nation continuously invests in large infrastructure, transportation, and construction initiatives that require high performance steel. India, with its accelerated infrastructure development plans and growing automotive industry, is also a significant market contributor. The region’s automotive sector is increasingly adopting lightweight materials to meet fuel efficiency and emissions norms, which supports ferroniobium demand in high strength automotive steel applications.

Technological advancements in steelmaking and robust foreign investments in manufacturing facilities strengthen the region’s metallurgical landscape. For example, China Molybdenum Co., Ltd., plays a key role in the Asia Pacific market by supplying niobium bearing materials that are processed into ferroniobium for steel producers. China Molybdenum’s production activities support regional steelmakers by ensuring reliable access to alloying materials that enhance mechanical properties in structural and automotive steels. The company’s integration into the supply chain helps address the demand for consistent quality ferroniobium grades required for high strength applications.

Competitive Landscape

The global ferroniobium market exhibits a moderately fragmented structure, driven by the specialized nature of niobium extraction, processing, and alloy production, where access to high-quality ore deposits and advanced metallurgical technology are key competitive advantages. A small number of multinational producers control the bulk of supply, leveraging vertical integration from mining to finished product distribution. Product quality, consistency, and technical support services are important differentiators, especially where high purity ferroniobium grades are required.

With key leaders including giants such as Companhia Brasileira de Metalurgia e Mineração (CBMM), CMOC Group Limited, and Niobec holding significant shares due to their resource bases and established supply chains, the competitive environment remains focused on securing raw material access and meeting varied industrial requirements. These players compete through a mix of long term supply agreements with major steelmakers, continuous investment in production technology, and diversification of product portfolios to serve different application segments such as HSLA steel, aerospace alloys, and automotive steels.

Key Industry Developments:

- In June 2025, Niobec Inc. reached a long term agreement with its blue collar workforce, successfully concluding negotiations that ensure stable labour relations at its niobium mining operations in Saint Honoré, Quebec. The pact, approved by union members and extending into the next business cycle, supports continued production of niobium, a critical raw material for ferroniobium, which is essential for advanced steelmaking and high strength alloys used in infrastructure, automotive, and industrial applications.

- In April 2025, Companhia Brasileira de Metalurgia e Mineração (CBMM) strengthened its position as a pivotal supplier in the niobium and advanced materials market, reaffirming Brazil’s strategic role in supplying critical micro alloying elements essential for high performance steels and industrial applications. The company’s Araxá operations remain central to niobium supply, highlighting the concentrated nature of the market and the reliance of major industries on CBMM’s production capacity. Niobium’s role in improving strength and durability in steel for infrastructure, automotive, and aerospace applications continues to attract attention, with CBMM positioned to address sustained demand in traditional and emerging applications.

Companies Covered in Ferroniobium Market

- CBMM

- Niobec Inc.

- China Molybdenum Co., Ltd.

- Anglo American Plc

- American Plc

- Molycorp Inc.

- CMOC Group Limited

- AMG Advanced Metallurgical Group

- Kamman Group

- Changsha South Tantalum Niobium Co., Ltd.

Frequently Asked Questions

The global ferroniobium market is projected to reach US$2.9 billion in 2026.

The ferroniobium market is driven by the rising demand for high-strength low-alloy (HSLA) steels in construction, automotive, and infrastructure applications.

The ferroniobium market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

Key market opportunities lie in the growing use of ferroniobium in renewable energy, electric vehicles, and high-performance aerospace and automotive alloys.

CBMM, Niobec Inc., China Molybdenum Co., Ltd., Anglo American Plc, Globe Specialty Metals, Inc., and Advanced Metallurgical Group N.V. (AMG) are the leading players.