- Agrochemicals

- Erucic Acid Market

Erucic Acid Market Size, Share, and Growth Forecast, 2026 - 2033

Erucic Acid Market by Grade (Erucic Acid 43-50%, Erucic Acid Less than 50%), Source (Rapeseed Oil, Others), Application (Slip Agent, Emollient, Hair Care and Textile Softening, Others), End-user (Plastic, Printing Ink, Food, Others), and Regional Analysis for 2026 - 2033

Erucic Acid Market Size and Trends Analysis

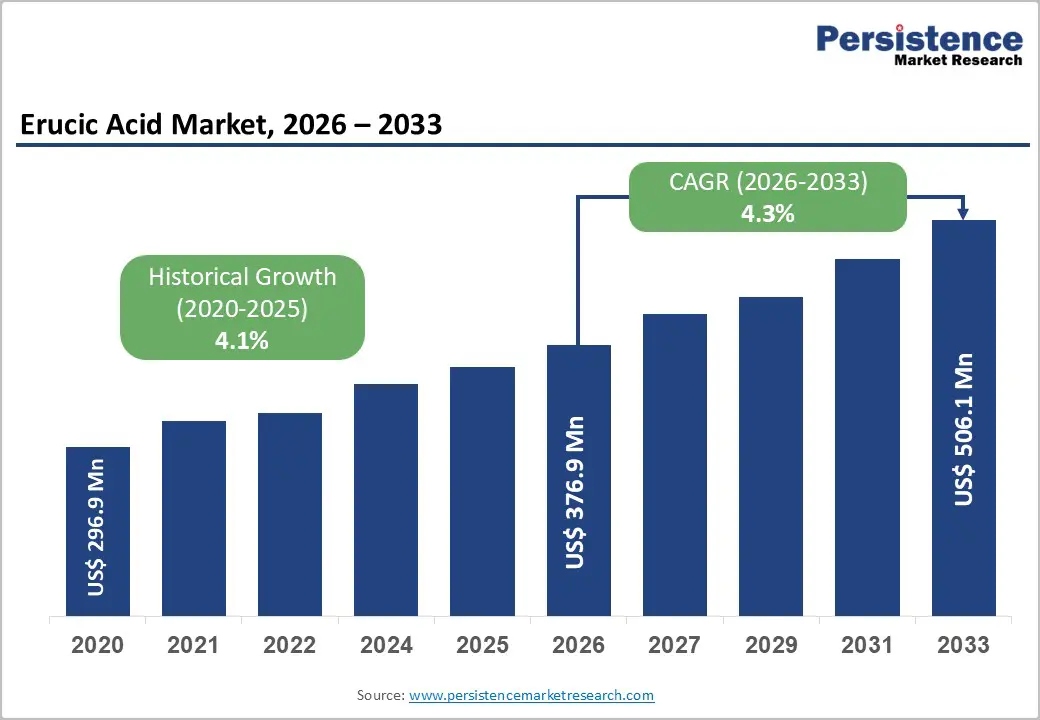

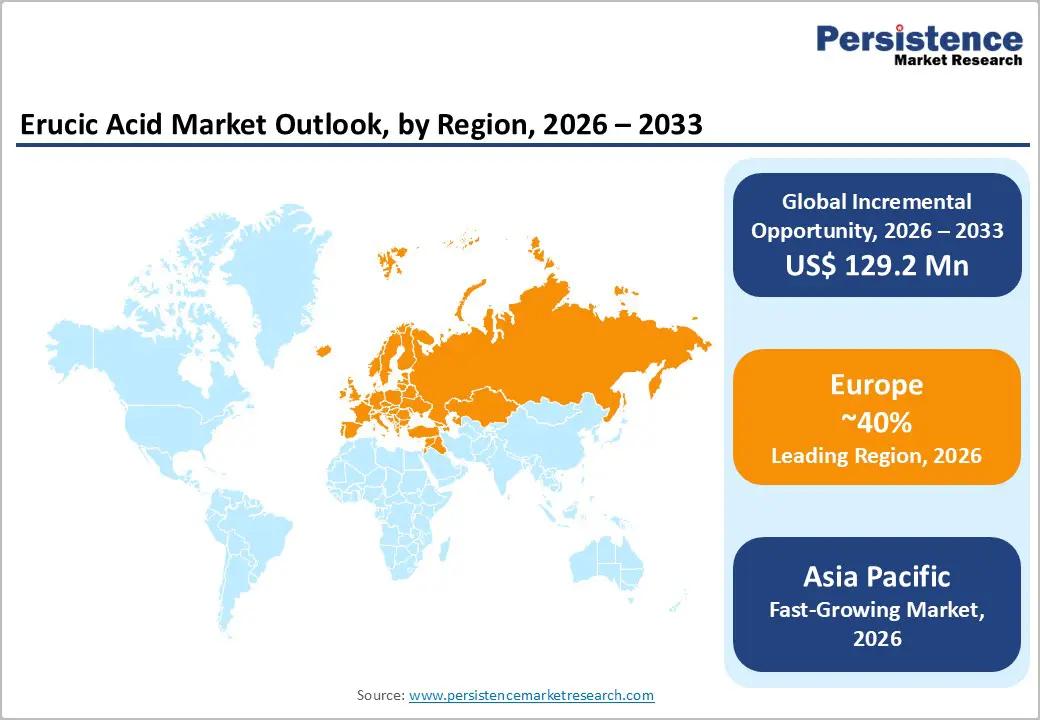

The global erucic acid market size is likely to be valued at US$376.9 million in 2026, and is expected to reach US$506.1 million by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of bio-based lubricants, the rising demand for high-performance slip agents in plastics, and advances in rapeseed-derived erucic acid processing.

The growing demand for versatile, sustainable erucic acid, especially the 43-50% grade from rapeseed oil, is accelerating adoption across applications. Advances in emollient and pour point depressant formulations are further boosting uptake by offering superior stability and functionality. The increasing recognition of erucic acid as a critical ingredient for eco-friendly industrial additives in emerging markets remains a major driver of market growth.

Key Industry Highlights:

- Leading Region: Europe, anticipated to account for a 40% market share in 2026, driven by strong rapeseed cultivation, regulatory support for bio-based chemicals, and high demand in Germany and France.

- Fastest-growing Region: Asia Pacific, fueled by expanding plastics and lubricant industries, rising bio-based material adoption in China and India.

- Dominant Grade: Erucic acid 43-50%, to hold approximately 70% of the revenue share, as it balances purity and cost for industrial use.

- Leading Source: Rapeseed oil accounts for over 80% of market revenue due to its high erucic acid content and abundant supply.

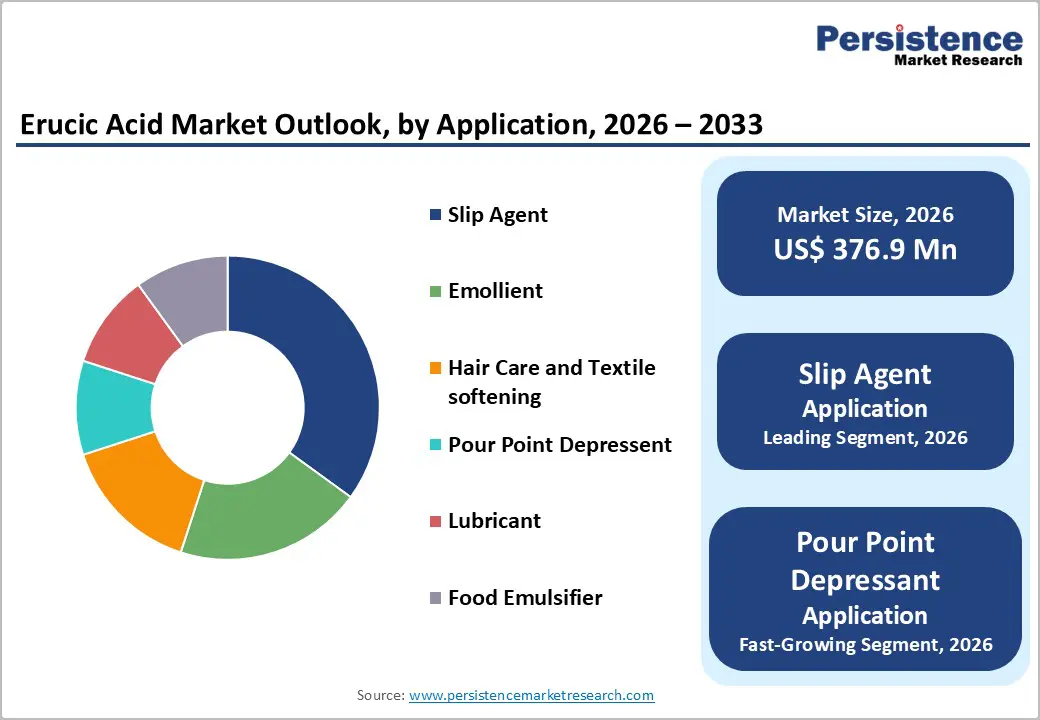

- Leading Application: Slip Agent, contributing nearly 35% of the market revenue, due to extensive use in polyethylene processing.

- Leading End-user: Plastic, with approximately 40% revenue share, due to anti-blocking and mold release needs.

| Key Insights | Details |

|---|---|

|

Erucic Acid Market Size (2026E) |

US$376.9 Mn |

|

Market Value Forecast (2033F) |

US$506.1 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Bio-Based Lubricants and High-Performance Slip Agents

The demand for bio-based lubricants and high-performance slip agents is growing rapidly due to a combination of environmental, regulatory, and performance-driven factors. Bio-based lubricants, derived from renewable resources such as vegetable oils, are gaining preference over traditional petroleum-based products as they offer superior biodegradability, reduced toxicity, and lower carbon footprints. Industries including automotive, manufacturing, and metalworking are increasingly adopting these eco-friendly alternatives to comply with stricter environmental regulations and sustainability goals.

High-performance slip agents are critical in enhancing the surface properties of materials such as plastics, films, and textiles. They reduce friction, improve process efficiency, and prevent defects during manufacturing, which is especially vital in high-speed production lines. The combination of enhanced operational efficiency and product quality drives their adoption across the packaging, automotive, and electronics industries. The rising focus on sustainability, coupled with the push for energy-efficient production processes, further fuels the integration of these products. As end-users become more conscious of environmental impact, manufacturers are investing in research to develop bio-based lubricants and slip agents with improved thermal stability, anti-wear properties, and compatibility with diverse materials.

High Development and Raw Material Volatility Costs

High development and raw material volatility costs present a significant barrier for companies advancing next-generation erucic acid and novel grades. Developing innovative grades such as ultra-high 43-50% purity, low-impurity <50%, or stabilized blends requires extensive research, specialized distillation, and advanced separation technologies that are far more expensive than basic extraction. Purity is an even greater challenge: many refined variants, contaminant-reduced lots, and stability-enhanced products are sensitive to oxidation, hydrolysis, and impurities, requiring rigorous optimization to ensure they remain effective throughout storage and use. Achieving long-term performance often requires costly stability trials, sophisticated GC testing, and the use of high-grade rapeseed, all of which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for food-contact limits, impurity thresholds, and batch consistency requires multiple validation studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled reactors, specialized purification lines, and quality-assurance systems, further driving up overall costs. For smaller producers, these challenges can limit premium diversification or delay commercialization.

Advancements in High-Purity and Bio-Based Delivery Platforms

Advancements in high-purity and bio-based erucic acid delivery platforms are transforming the global additive landscape by addressing two major challenges: impurity barriers and sustainability concerns. High-purity platforms are engineered to achieve >45% assay, reducing reliance on crude sources and enabling direct use in sensitive applications. Innovations, such as chromatographic purification, enzymatic enrichment, solvent-free extraction, and antioxidant stabilization, significantly improve quality and reduce odor, lowering formulation costs for coatings and cosmetics campaigns.

Progress in bio-based platforms, including non-GMO rapeseed, organic canola, traceable tame mustard, and renewable fish sources, supports more eco-conscious derivatives by minimizing synthetic dependence, the product’s first line of defense against regulations. These formats eliminate petroleum links, enhance biodegradability, and enable versatile use without compromise, making them highly suitable for large-scale lubricant programs. New technologies such as nano-emulsification, bio-adhesive stabilization, and VLP-based monitoring further enhance performance and response.

Category-wise Analysis

Grade Insights

Erucic acid 43-50% is anticipated to dominate the market, accounting for approximately 70% of the revenue share in 2026. Its dominance is driven by an optimal balance of purity and cost, high functionality, and versatility, making it preferred for industrial applications. Erucic acid 43-50% provides effective slip properties, ensures stability, and contributes to performance, making it suitable for large-scale plastic campaigns. PMC Biogenix, a leading specialty chemical manufacturer, markets a range of erucamide-based slip agents under its Armoslip® and Kemamide® product lines, which are derived from long-chain fatty acids, including erucic acid. These products are widely used by polymer producers to impart low friction and improved surface properties to polyolefin films (LDPE, LLDPE, and PP) for packaging and industrial applications.

Erucic acid less than 50% is likely to be the fastest-growing segment, due to its economical profile and expanding use in cost-sensitive sectors. Its lower-purity profile makes it ideal for targeted bulk, reducing premium needs. Continuous innovations in refining are further strengthening its acceptance, driving rapid adoption across emerging regions, where demand for affordable additives is accelerating. Gushan Environmental Energy, a Chinese biodiesel producer, generates erucic acid and erucic amide as by-products of its biodiesel production process. These lower-grade fatty acids are sold into bulk industrial markets, including lubricants, plastic additives, and anti-static agents for plastics and textiles, where cost-effectiveness is prioritized over ultra-high purity.

Source Insights

Rapeseed oil is both the leading and fastest-growing source in the erucic acid market, projected to account for nearly 80% of the share in 2026. Its dominance is supported by naturally high erucic acid concentration, large-scale agricultural cultivation, and a well-established global supply chain that ensures consistent availability for derivative production. Processors prefer rapeseed oil due to its reliable yields and suitability for industrial applications, enabling volume expansion as demand rises. Growing interest in low-erucic canola varieties and tame mustard cultivation reflects an industry shift toward diversified feedstocks, supporting flexibility while maintaining rapeseed oil’s leadership position.

Cargill, Inc., one of the world’s largest agribusiness and oilseed processors, has been expanding its rapeseed processing capacity, including a major new facility in Regina, Saskatchewan, Canada that will process up to 1 million metric tons of canola annually. This plant is designed to support both food and biofuel markets, reinforcing rapeseed oil’s central role in global supply chains and meeting rising demand for edible oils, industrial oils, and derivatives.

Application Insights

Slip agents are projected to dominate the market, accounting for nearly 35% of revenue in 2026, as they remain central to plastic processing, large polymer programs, and the management of products requiring anti-blocking properties. Their strong integration, skilled formulators, and ability to handle high-volume or premium polymer blends drive higher consumption. Slip agent applications currently lead 43–50% of rollouts and support emerging trials under 50%. Cargill’s Incroslip™ Slip & Anti-Block Additives are widely adopted by polymer producers and converters to enhance processing efficiency and final product quality across polyolefin applications, including LDPE, LLDPE, HDPE, and PP films. These additives are engineered to reduce surface friction, improve anti-blocking performance, and optimize demolding and handling, making them a preferred choice in high-volume packaging, film extrusion, and converting operations.

The point depressants segment is expected to be the fastest-growing, driven by their widespread use in lubricants and increasing applications in biofuels. They provide effective cold-flow improvement, appealing to users seeking reliable low-temperature performance. Expanded outreach programs, energy-focused initiatives, and broader availability of standard and premium additives are further accelerating adoption, particularly in urban and semi-urban regions. Afton Chemical Corporation offers a range of HiTEC® pour-point depressants, including HiTEC® 672 and HiTEC® 5788, specifically designed for lubricant and fuel applications. These additives improve the low-temperature fluidity of engine oils, gear oils, and diesel fuels by modifying wax crystallization, enhancing flow and pumpability in cold environments.

End-user Insights

Plastic is likely to dominate the market, with approximately 40% share in 2026, due to the high volume of polymer production and strong global emphasis on processing aids. Regular manufacturing schedules, anti-block requirements, and widespread access to rapeseed derivatives drive consistent demand. Rising focus on paints & coatings and rubber further strengthens plastic leadership. Optislip™ BR is a vegetable-derived slip and anti-block agent used with polyolefin films to maintain clarity while improving processing and reducing reliance on inorganic additives such as talc or silica. This kind of integration helps plastics producers achieve consistent performance across large production schedules and diverse product lines.

The cosmetics & personal care segment is estimated to be the fastest-growing field, driven by rising demand for natural emollients, growing concern about synthetic ingredients, and expanding adoption of hair and skin care products. Improved moisturizing, tailored grades, and stronger integration for clean beauty support rapid uptake. The growing use of food, pharmaceutical, and other high-tech sectors further accelerates market growth. Evonik Industries AG, a major global specialty chemicals company, recently opened a new production plant in Steinau, Germany, to significantly boost its capacity for sustainable cosmetic emollients. These emollients are typically esters produced enzymatically from vegetable-derived oils and act as moisturizing and conditioning ingredients in a wide range of skin care, hair care, and personal care formulations. The investment responds directly to rapid growth in demand for eco-friendly, natural-origin ingredients among cosmetics formulators and consumers, especially as brands shift away from petrochemical synthetics.

Regional Insights

North America Erucic Acid Market Trends

North America’s growth is fueled by the region’s advanced specialty chemical infrastructure, strong R&D capabilities, and high public awareness of the benefits of bio-based products. Processing systems in the U.S. and Canada provide extensive support for formulation programs, ensuring broad accessibility of erucic acid across plastics, paints & coatings, and cosmetics applications. Rising demand for high-purity, convenient, and easily incorporated forms is further accelerating adoption, as these formats enhance sustainability and reduce reliance on petroleum-based alternatives.

Advancements in erucic acid technology, including stable 43–50% refining, improved pour-point performance, and targeted emollient enhancements, are attracting substantial investment from both the public and private sectors. Government initiatives and sustainability campaigns continue to encourage its use as a greener alternative to synthetic chemicals, addressing environmental risks and emerging regulatory pressures. Growing emphasis on cosmetic-grade and specialty applications, particularly in lubricants and other niche areas, is expanding the range of target markets for erucic acid.

Europe Erucic Acid Market Trends

Europe is expected to lead with a market share of 40% in 2026, fueled by increasing awareness of sustainable benefits, strong chemical systems, and government-led green programs. Countries such as Germany, France, and the U.K. have well-established frameworks that support routine incorporation and encourage the adoption of innovative acid-delivery methods, including erucic acid. These eco-friendly formulations are particularly appealing for the plastic manufacturing sector, regulation-conscious operators, and personal care users, improving performance and coverage rates.

Technological advancements in erucic acid development, such as enhanced purity, application-targeted delivery, and improved bio-based grades, are further boosting market potential. European authorities are increasingly supporting research and trials for acids against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-impact options is aligned with the region’s focus on preventive sustainability and reducing emissions. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in extraction and novel variants to increase efficacy.

Asia Pacific Erucic Acid Market Trends

Asia Pacific is expected to be the fastest-growing market for erucic acid from 2026 to 2033, driven by rising industrial awareness, supportive government initiatives, and the expansion of application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting erucic acid applications to address manufacturing growth and emerging cosmetic needs. Erucic acid is particularly attractive in these regions due to its versatility, ease of scale-up, and suitability for large-scale plastic drives across both urban and rural populations.

Technological advancements are enabling the development of stable, effective, and easy-to-process erucic acid that can withstand challenging production conditions and minimize reliance on impurities. These innovations are critical for reaching remote facilities and improving overall functionality coverage. The growing demand for plastic, paints & coatings, and personal care applications is driving market expansion. Public-private partnerships, increased chemical expenditure, and rising investment in refining research and manufacturing capacity are further accelerating growth. The convenience of acid delivery, combined with improved performance and reduced defect risk, positions erucic acid as a preferred choice.

Competitive Landscape

The global erucic acid market features competition between established oleochemical leaders and emerging specialty producers. In North America and Europe, Cargill and BASF lead through strong R&D, distribution networks, and industry ties, bolstered by innovative grades and sustainability programs. In Asia Pacific, Wilmar International Ltd advances with localized solutions, enhancing accessibility. High-purity delivery boosts performance, cuts impurity risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand sourcing, and speed commercialization. Bio-based formulations solve environmental issues, aiding penetration in green-focused areas.

Key Industry Developments

- In September 2024, Croda International announced a €45 million (US$50 million) investment to expand its specialty oleochemicals production facility in the Netherlands, including enhanced erucic acid processing capabilities. The expansion will increase production capacity by 35% and incorporate advanced purification technologies for high-purity applications.

- In July 2024, Cargill, a global leader in oilseed processing, announced it had surpassed the 50 percent completion milestone in the construction of its new canola facility located at the Global Transportation Hub in West Regina, Sask. The new facility had the capacity to process 1 million metric tons of canola per year, producing crude canola oil for food and biofuel markets and canola meal for animal feed.

- In March 2024, Emery Oleochemicals launched a new high-purity erucic acid product line specifically designed for pharmaceutical and cosmetic applications. The products achieve 99.5% purity through proprietary purification processes and target premium market segments that require superior quality standards.

Companies Covered in Erucic Acid Market

- Cargill

- BASF

- Wilmar International

- Vantage Specialty Chemicals

- Evonik Industries

- Arkema

- Jiangsu Sopo Biotech

- Yasho Industries

- Shandong Kexing

Frequently Asked Questions

The global erucic acid market is projected to reach a value of US$376.9 million by 2026.

The growing use of bio-based and renewable raw materials is driving the adoption of erucic acid, which offers enhanced thermal stability and performance advantages.

The acid market is poised to witness a CAGR of 4.3% from 2026 to 2033.

Key market opportunities include the growth of biofuels, with the IEA forecasting a twofold increase by 2030, as well as innovations in bioplastics and pharmaceuticals that harness natural sources to create more sustainable, eco-friendly alternatives.

Cargill, BASF, Wilmar International, Vantage Specialty Chemicals, and Evonik Industries are the key players.