- Non-food Packaging

- Envelope Market

Envelope Market Size, Share, and Growth Forecast, 2026 - 2033

Envelope Market by Product Type (Cushioned, Non-Cushioned, Others), Material Type (Paper-Kraft, Recycled/Sustainable, Others), Closure Type, End-user, and Regional Analysis for 2026 - 2033

Envelope Market Size and Trends Analysis

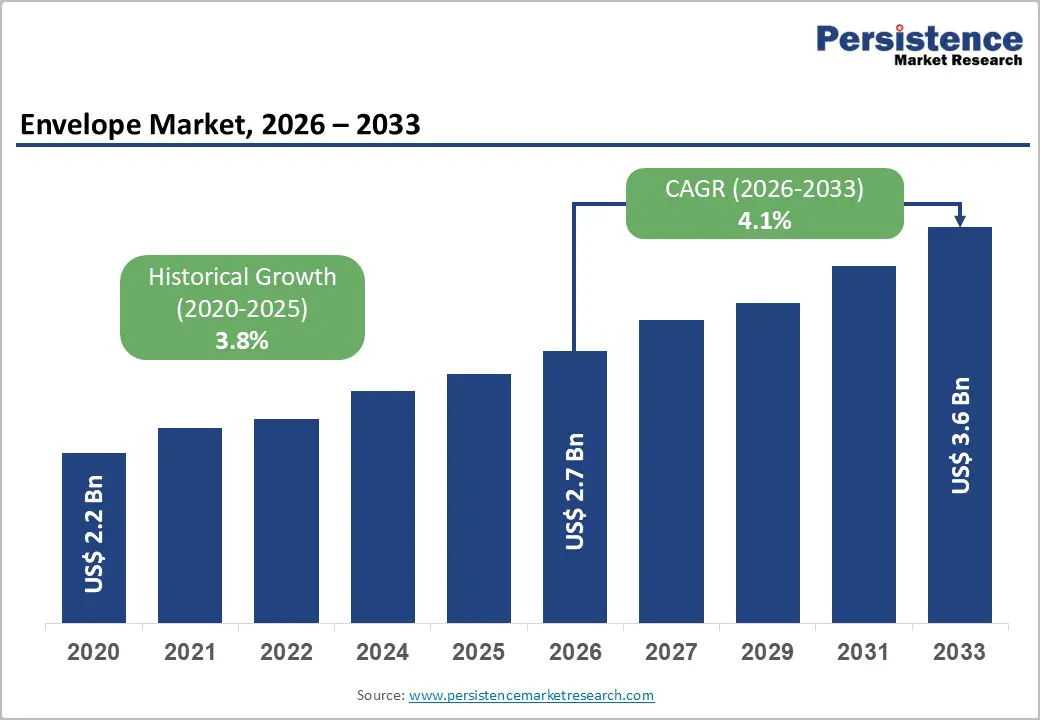

The global envelope market size is likely to be valued at US$2.7 billion in 2026 and is expected to reach US$3.6 billion by 2033, growing at a CAGR of 4.1% between 2026 and 2033, driven by the industry’s transition from structural decline toward a more balanced growth trajectory.

Declining demand for traditional envelopes in mature postal markets is being offset by growing use of mailer and cushioned envelopes, driven by e-commerce and protective shipping needs. At the same time, the shift toward sustainable materials is reshaping product offerings, with the strongest opportunities for converters and paper suppliers that pivot to e-commerce formats, value-added features, and recycled or recyclable solutions aligned with regulatory and sustainability goals.

Key Industry Highlights

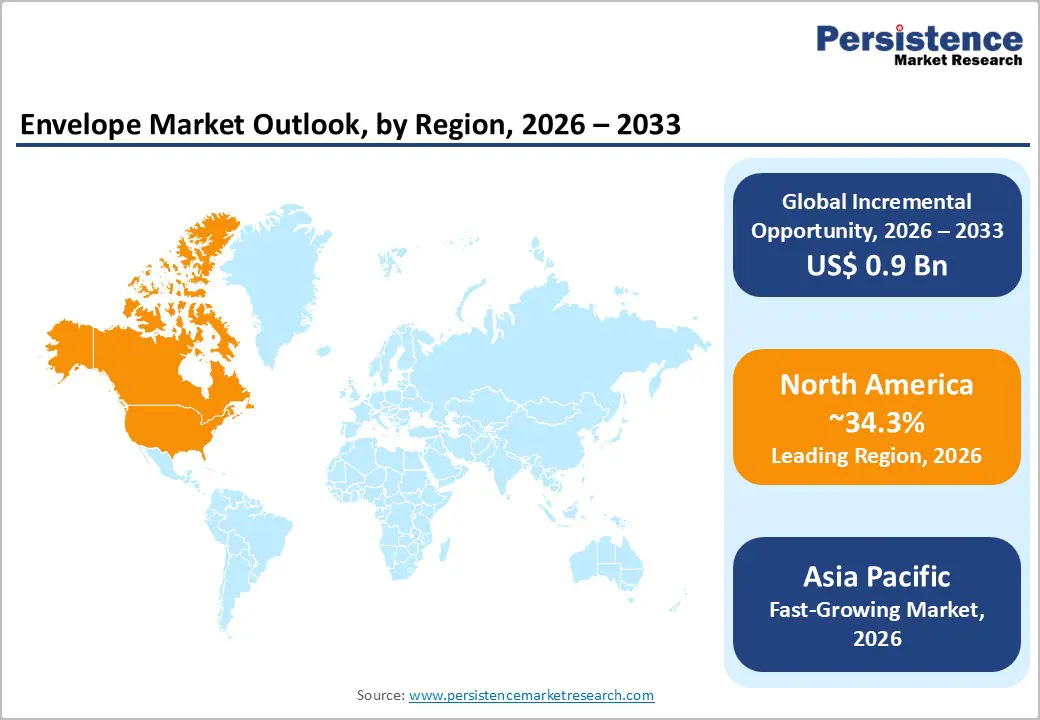

- Leading Region: North America is projected to hold approximately 34.3% market share, supported by strong e-commerce penetration, high parcel shipment volumes, and sustained demand for padded and value-added mailers in the U.S.

- Fastest-growing Region: Asia Pacific, driven by rapid e-commerce expansion across China, India, Japan, and ASEAN countries, along with cost-competitive manufacturing and rising consumer spending.

- Investment Plans: Ongoing investments focus on automation, recycled material integration, and capacity expansion, particularly in Asia Pacific manufacturing hubs and North American fulfillment-oriented converting lines.

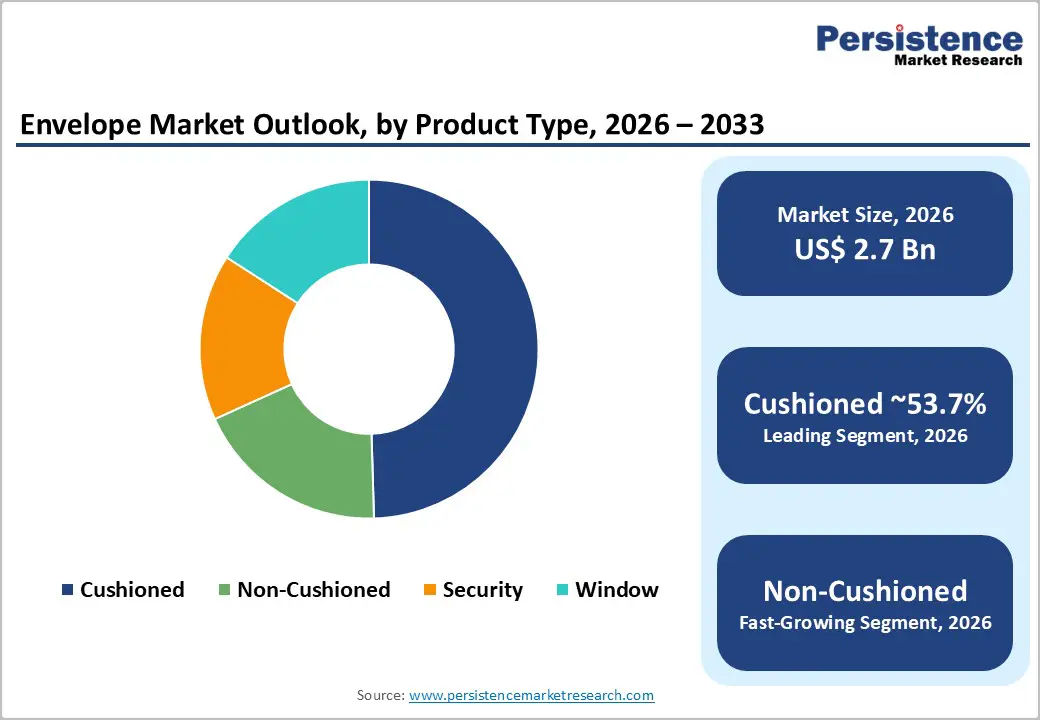

- Dominant Product Type: Cushioned envelopes are anticipated to hold 53.7% market share, driven by widespread adoption in e-commerce for product protection and damage reduction.

- Leading Material Type: Paper-based kraft materials are estimated to dominate, holding 63.4% market share, due to recyclability, strength, cost efficiency, and alignment with global sustainability and regulatory requirements.

| Key Insights | Details |

|---|---|

| Envelope Market Size (2026E) | US$2.7 Bn |

| Market Value Forecast (2033F) | US$3.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - E-commerce Shift toward Mailers and Padded Envelopes

Rapid growth in e-commerce volumes and sustained consumer preference for online retail are materially increasing demand for protective mailers and cushioned envelopes. As parcel shipments rise and letter mail volumes decline, demand has structurally shifted away from lightweight stationery envelopes toward padded and protective formats designed for small-parcel logistics. Cushioned mailers now represent a significant share of envelope-related packaging revenue, supported by higher unit values and consistent order volumes. This trend is reinforced by growth in product returns, decentralized fulfillment networks, and last-mile delivery optimization. In response, manufacturers are prioritizing padded and paper-based protective mailers, positioning these products as core growth drivers within the envelope ecosystem.

Sustainability-Driven Material Substitution

Sustainability considerations are increasingly influencing envelope material selection. Corporate environmental commitments, evolving regulatory frameworks in Europe and parts of Asia Pacific, and procurement standards set by large retailers are accelerating demand for recyclable and recycled envelope materials. As a result, manufacturers are expanding offerings of paper-only protective mailers, recyclable kraft envelopes, and high post-consumer recycled content products. This shift allows suppliers to command modest pricing premiums while improving recyclability and waste-stream compatibility. Investments in conversion lines capable of handling recycled grades and recyclable adhesive systems further support long-term demand growth. Recycled and sustainable materials now represent the fastest-growing material segment within envelope product mixes.

Resilient Specialized B2B Demand

Although commercial and institutional mail volumes are declining in absolute terms, they remain a high-margin segment for premium and security envelopes. Financial services, legal documentation, healthcare communications, and government correspondence continue to rely on physical envelopes for compliance, confidentiality, and record-keeping purposes. Security features such as tamper-evident closures, windowed remittance designs, and specialty coatings support pricing stability. Postal pricing adjustments have also created margin recovery opportunities, allowing suppliers to reinvest in product enhancements. As a result, B2B envelope demand demonstrates revenue resilience despite ongoing volume erosion.

Barrier Analysis - Structural Decline in Transactional Mail Volumes

Transactional and marketing mail volumes have declined significantly over the past decade across major developed markets. Digital billing, electronic communication, and online advertising have reduced reliance on physical mail, leading to sustained contraction in demand for standard stationery envelopes. In several mature postal systems, cumulative volume declines exceed 40-50% in certain mail classes. This structural shift constrains baseline demand growth and places pressure on manufacturers with heavy exposure to legacy document envelopes. Suppliers that fail to diversify into mailers, security formats, or value-added applications face underutilized capacity and declining profitability.

Input Cost Volatility and Capital Intensity

Envelope manufacturers are exposed to fluctuations in pulp prices, energy costs, labor expenses, and logistics rates. At the same time, transitioning toward padded mailers and sustainable materials requires capital investment in specialized converting equipment. Smaller and mid-sized converters may face financial constraints when upgrading production lines. Input cost volatility can compress margins, particularly for suppliers operating in price-sensitive segments. Without effective cost pass-through mechanisms or long-term supply agreements, margin pressure can reduce operating profitability by several percentage points during periods of elevated raw material costs.

Opportunity Analysis - Substitution of Plastic Mailers with Paper-Based Protective Envelopes

Replacing plastic-padded mailers with paper-based protective alternatives represents a significant growth opportunity. Demand for padded and protective mailers is expanding faster than the overall envelope market, as retailers and marketplaces seek fully recyclable packaging solutions. Even limited substitution of existing plastic mailer volumes can translate into hundreds of millions of dollars in incremental addressable market value over the forecast period. Manufacturers that scale paper-based protective mailers through partnerships with large retailers and fulfillment operators are well-positioned to capture premium volumes, strengthen customer relationships, and benefit from regulatory tailwinds.

Integrated Fulfillment and Branded Mailer Solutions

Envelope suppliers can increase revenue per unit by offering fulfillment-ready, branded, and return-enabled mailers tailored to e-commerce workflows. Pre-printed designs, self-seal closures, tamper-evident features, and embedded return functionality enhance operational efficiency for sellers while improving the consumer unboxing experience. These value-added features support higher average selling prices and reduce customer switching. The opportunity is especially attractive in North America and Europe, where brand differentiation and fulfillment efficiency are key purchasing criteria for online sellers.

Category-wise Analysis

Product Type Insights

Cushioned envelopes are anticipated to account for 53.7% market share, representing the leading product category due to their critical role in e-commerce and parcel shipping, where protection against impact and vibration is essential. These envelopes are widely used for electronics accessories, cosmetics, pharmaceuticals, books, and small consumer goods. Ongoing investments in improved padded liners, such as bubble cushioning, molded fiber padding, and paper-based cushioning, combined with durable kraft outer layers, have reinforced their dominance. Major logistics and e-commerce platforms increasingly standardize cushioned mailers to reduce return rates and in-transit damage, supporting sustained demand across North America, Europe, and Asia Pacific.

Non-cushioned envelopes are likely to be the fastest-growing product type, driven by cost-sensitive shipping requirements and the rapid expansion of document, apparel, and flat-item e-commerce shipments. These envelopes are favored for invoices, lightweight textiles, magazines, and direct-to-consumer apparel, where protection needs are minimal. Growth is further supported by sustainability benefits from lower material usage and improved compatibility with automated sorting and fulfillment systems. While average selling prices remain lower than cushioned formats, high shipment volumes, faster production cycles, and lower material costs enable strong margin realization through scale.

Material Type Insights

Paper-based kraft is anticipated to hold 63.4% market share, due to their high tensile strength, tear resistance, recyclability, and cost efficiency. Kraft paper is extensively used across both cushioned and non-cushioned envelopes, serving applications ranging from e-commerce shipping to business correspondence. Its widespread availability and compatibility with existing recycling infrastructure make it the preferred choice for postal services, retailers, and fulfillment providers. Many global packaging suppliers continue to optimize kraft grammage and fiber blends to balance durability with lightweighting, reinforcing kraft’s leadership across mature and emerging markets.

Recycled and sustainable materials are likely to be the fastest-growing material segment, supported by rising recycled-content mandates, corporate sustainability targets, and consumer preference for eco-friendly packaging. Envelopes made with high post-consumer recycled (PCR) kraft content and fiber-based cushioning are increasingly adopted by e-commerce brands and logistics providers aiming to reduce their environmental footprint. Certifications such as FSC and PEFC further enhance buyer confidence. The shift away from virgin pulp and plastic-based components supports regulatory compliance, enables premium positioning for sustainable product lines, and strengthens long-term supplier-buyer partnerships in environmentally regulated markets.

Regional Insights

North America Envelope Market Trends - E-Commerce Fulfillment, Automation, and Branded Mailer Demand

North America is projected to lead the market with approximately 34.3% market share, driven primarily by the U.S., which accounts for the majority of regional demand. The market benefits from a highly developed e-commerce ecosystem, large-scale fulfillment operations, and sustained parcel shipment growth, even as traditional letter mail volumes continue to decline. Major retailers and logistics platforms increasingly rely on padded and specialty mailers to protect higher-value shipments such as electronics accessories, health products, and subscription-based goods. This shift supports stable revenue generation despite structural declines in postal correspondence.

Investment activity in the region centers on automation, recycled material integration, and branded mailer innovation. Leading envelope and packaging producers have expanded automated converting lines to support higher throughput and consistent quality for e-commerce customers. Companies such as WestRock, International Paper, and Packaging Corporation of America have increased recycled fiber usage across kraft-based mailers to align with retailer sustainability commitments. Growth in custom-printed and self-seal envelopes reflects demand from direct-to-consumer brands seeking improved unboxing experiences and faster fulfillment. Strategic partnerships between envelope manufacturers and third-party logistics providers further reinforce North America’s leadership by embedding envelope solutions directly into fulfillment workflows.

Europe Envelope Market Trends - Regulation-Led Shift toward Recyclable and Fiber-Based Envelopes

Europe represents a mature yet innovation-driven envelope market, characterized by strong regulatory oversight, high environmental standards, and steady demand from both commercial and e-commerce channels. Germany, the U.K., and France lead regional consumption, supported by dense logistics networks and advanced recycling infrastructure. While overall mail volumes are stable to modestly declining, demand for paper-based mailers and sustainable envelope solutions continues to grow as businesses replace plastic alternatives.

Regulatory measures, particularly extended producer responsibility (EPR) schemes and packaging waste directives, have accelerated the adoption of recyclable and recycled-content envelopes across the region. In response, manufacturers such as DS Smith, Mondi Group, Smurfit Kappa, and Stora Enso have invested in lightweight kraft grades, recyclable adhesive systems, and fiber-based padding technologies. These developments allow envelope producers to reduce material usage while maintaining strength and machinability. Regulatory harmonization across the European Union enables manufacturers to standardize product designs and scale production efficiently across borders, improving supply-chain optimization and cost competitiveness. Sustainability-led procurement by large retailers and postal operators continues to shape material innovation and purchasing decisions throughout the region.

Asia Pacific Envelope Market Trends - High-Growth E-Commerce Volumes and Cost-Efficient Manufacturing Hub

Asia Pacific is the fastest-growing regional envelope market, supported by rapid expansion of e-commerce, rising consumer spending, and continued development of logistics and fulfillment infrastructure. China, India, Japan, and key ASEAN economies are the primary growth engines, with high parcel shipment volumes driven by online retail, digital payments, and mobile-first shopping behavior. The region’s strong manufacturing base and competitive production costs further enhance its attractiveness for both domestic consumption and export-oriented envelope production.

Regional investments focus on capacity expansion, automation, and cost-efficient production models. Local manufacturers in China and Southeast Asia have expanded converting capacity to serve large e-commerce platforms and international brands, while global suppliers have increased their presence through joint ventures and regional plants. Companies such as Oji Holdings, Nippon Paper Industries, and regional kraft processors are advancing recycled paper usage and improving envelope durability to meet export and domestic standards. At the same time, multinational packaging firms are leveraging Asia Pacific as a manufacturing hub to supply global fulfillment networks. These developments reinforce the region’s role as both a high-growth consumption market and a critical production center for the global envelope industry.

Competitive Landscape

The global envelope market is moderately fragmented, comprising global integrated paper producers and a large number of regional and local converters. Large players benefit from raw material control and distribution scale, while smaller firms compete through specialization, customization, and regional proximity. Competitive intensity remains high, particularly in commoditized segments.

Recent developments include the commercialization of paper-based protective mailers, increased investment in automation and sustainable converting lines, and expanded focus on e-commerce-oriented envelope formats. These initiatives aim to replace plastic packaging, improve fulfillment efficiency, and support long-term margin stability.

Leading strategies include product differentiation through sustainability and security, cost optimization via regional manufacturing, and vertical collaboration with logistics and e-commerce platforms. Automation and recycled material integration are central to competitive positioning.

Key Industry Developments

- In November 2025, Antalis unveiled its new eco-friendly expandable mailer featuring Hexpand flex-to-fit technology and 100% recycled materials, designed to reduce e-commerce shipping waste and improve fulfillment efficiency.

- In November 2025, Mondi introduced a fully recyclable protective mailer developed in collaboration with major online marketplaces, replacing plastic bubble wrap with open-flute paper for sustainable and protective e-commerce shipping solutions.

Companies Covered in Envelope Market

- Mondi Group

- International Paper

- Amcor plc

- Taylor Corporation

- WestRock

- Neenah Inc.

- Mohawk Fine Papers

- Cenveo

- Supremex

- Bong AB

- Tension Envelope Corporation

- Paoli/Paoli Envelope

- Smurfit Kappa Group

- DS Smith

- Stora Enso

- Sappi Limited

- Oji Holdings Corporation

- Nippon Paper Industries

Frequently Asked Questions

The global envelope market size is US$2.7 billion in 2026.

By 2033, the global envelope market is expected to reach US$3.6 billion.

Key trends shaping the envelope market include rising demand for cushioned envelopes driven by e-commerce growth, increasing adoption of recycled and sustainable paper materials, wider use of self-seal closures for operational efficiency, and continued demand from commercial and institutional users despite digital communication alternatives.

The cushioned envelope segment is the leading product type, accounting for 53.7% market share, supported by its extensive use in e-commerce, logistics, and document protection applications.

The envelope market is projected to grow at a CAGR of 4.1% between 2026 and 2033.

Major players include Mondi Group, International Paper, Smurfit Kappa Group, DS Smith, and WestRock.