- Medical Devices

- Endoscope Repair Market

Endoscope Repair Market Size, Trends, Share, Growth, and Regional Forecast, 2025 - 2033

Endoscope Repair Market by Product Type (Laparoscope, Arthroscope, Colonoscope, Gastroscope, Bronchoscope, Hysteroscope, Esophagoscope, Duodonoscope), Modality Type (Rigid, Flexible), Service Provider (Original Equipment Manufacturers (OEM), Third Party Vendors), Regional Analysis, from 2026 - 2033

Endoscope Repair Market Share and Trends Analysis

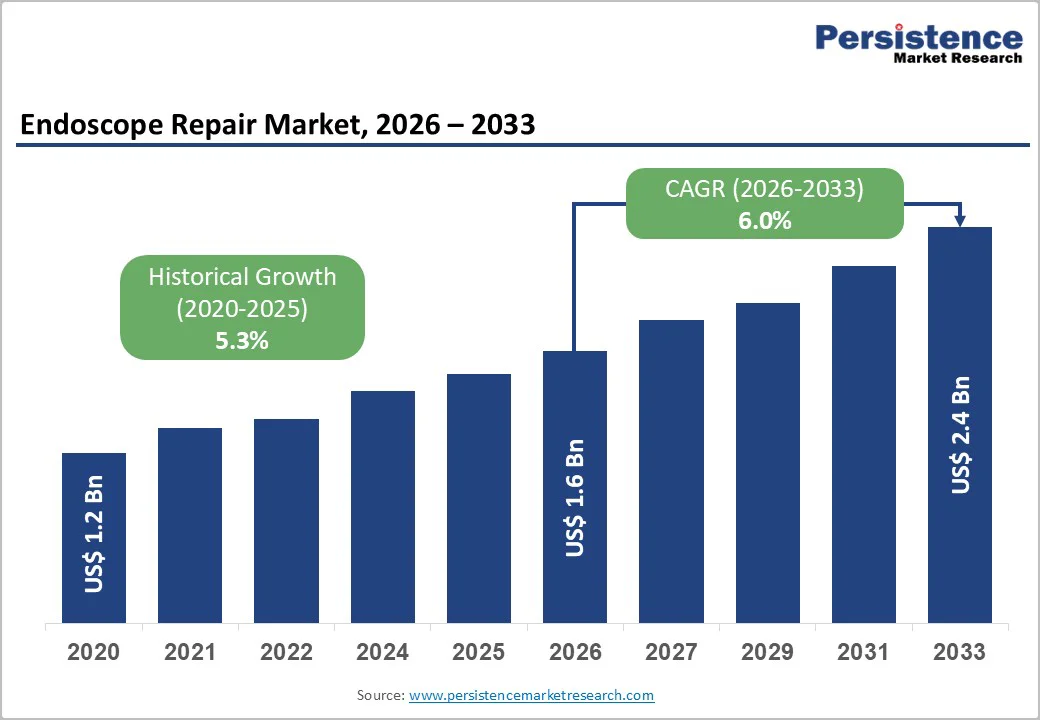

The global endoscope repair market size is estimated to grow from US$ 1.6 billion in 2026 to US$ 2.4 billion by 2033, at a CAGR of 6.0% from 2026 to 2033. Market growth is heavily dependent on hospitals adopting endoscopic procedures that require consistent equipment performance.

Frequent device wear, rise in procedure volumes, and high replacement costs make repair services a practical choice for healthcare facilities. A key trend is the shift toward outsourced maintenance with providers seeking faster turnaround times and standardized service quality. Demand for refurbished components, multi-brand repair capabilities, and preventive maintenance programs is rising. Manufacturers and independent service companies are also expanding regional service centers to support reliability, cost efficiency, and extended device lifecycles.

Key Industry Highlights:

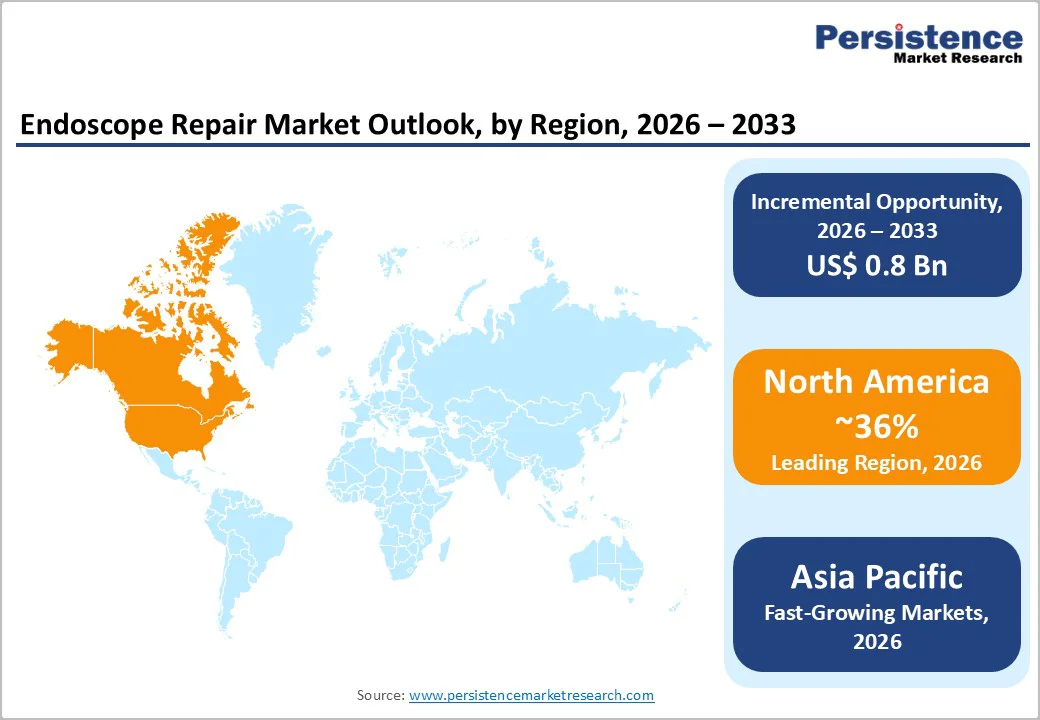

- Leading Region: North America holds the largest share of the global market in 2025, at approximately 36%, supported by high procedure volumes, mature healthcare infrastructure, and strict regulatory standards for device maintenance and infection control.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by expanding hospital networks, rising endoscopy procedures, growing awareness of minimally invasive diagnostics, and increasing adoption of third-party repair services.

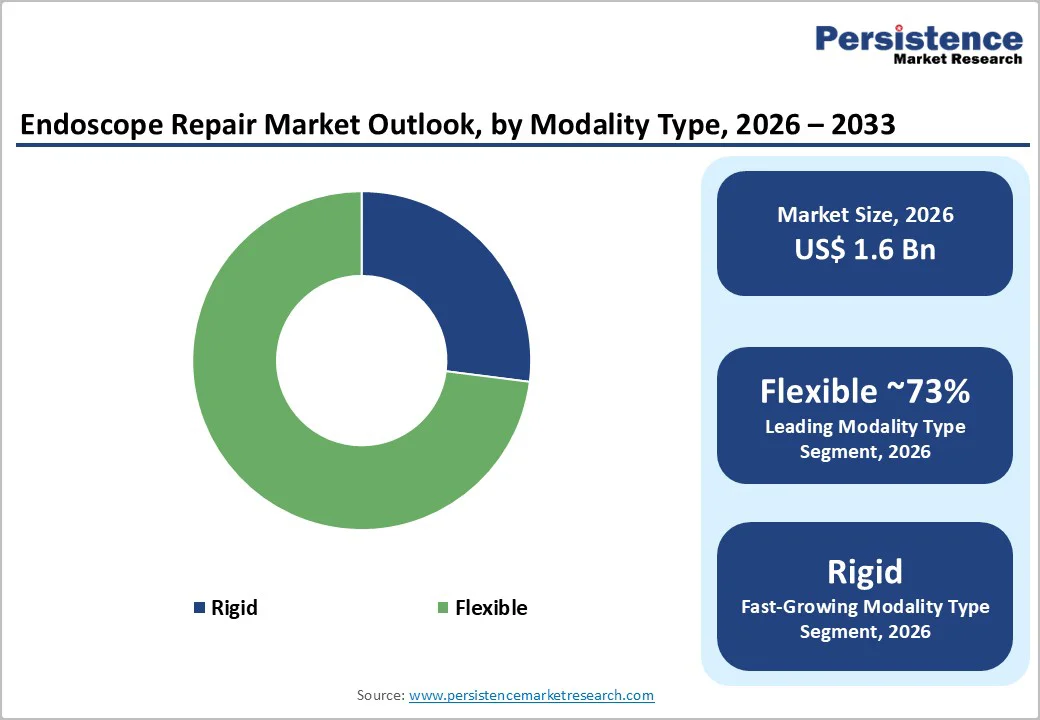

- Dominant Segment: Flexible endoscopes remain the dominant segment due to their widespread use in gastrointestinal, pulmonary, and surgical procedures, requiring frequent maintenance and specialized repair services.

- Fastest Growing Segment: Rigid endoscopes and advanced high-definition scopes represent the fastest-growing segment, driven by increasing adoption in surgical and specialty procedures and the need for precise refurbishment and preventive maintenance programs.

| Key Insights | Details |

|---|---|

|

Endoscope Repair Market Size (2026E) |

US$ 1.6 Bn |

|

Market Value Forecast (2033F) |

US$ 2.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.0% |

|

Historical Market Growth (CAGR 2020 to 2024) |

5.3% |

Market Dynamics

Driver - Rising Endoscopy Procedure Volumes and Aging Installed Base

The rapid increase in global endoscopy procedures is a major driver of the endoscope repair market, as higher patient volumes directly translate into greater wear on both flexible and rigid scopes. With more than 190 million endoscopic procedures performed each year worldwide, hospitals face growing pressure to maintain equipment uptime and ensure consistent image quality. Upper gastrointestinal endoscopy alone accounts for roughly 9.3 procedures per 1,000 inhabitants, increasing by nearly 2.6% annually, reflecting the shift toward minimally invasive diagnostics and treatments. This rising demand places continuous strain on optical fibers, angulation systems, insertion tubes, and electronic components. Since high-definition endoscopes and specialty models often cost tens of thousands of dollars, replacing them frequently is not financially viable. As a result, hospitals prioritize structured repair cycles and preventive maintenance programs to extend device life. Both OEM and third-party service providers benefit from this trend, offering refurbishment, calibration, parts replacement, and performance testing. The growing installed base of aging endoscopes, coupled with the need to maintain clinical efficiency, reinforces long-term, recurring demand for dependable repair services.

Restraints - OEM Control Over Parts and Service Information

A significant restraint in the endoscope repair market stems from OEM control over proprietary components, software access, and technical service documentation. Many leading manufacturers restrict the availability of specialized parts, diagnostic tools, and calibration systems needed for high-quality repairs. Such limitations create dependency on OEM service centers, concentrating revenue among a handful of large players and limiting competitive options for healthcare facilities. Restricted access can also result in higher service costs, longer repair timelines, and limited ability for hospitals to negotiate flexible contracts. Independent repair providers often struggle to expand their offerings because they cannot source certified components or obtain the engineering data required to meet OEM-level specifications. Although right-to-repair discussions are gaining attention in regions such as North America and Europe, regulatory progress remains slow and fragmented. This uncertainty discourages long-term investments in broader third-party service capabilities, limiting overall market development and keeping many hospitals tied to OEM-dominated repair models.

Opportunity - Growth of Third-Party and Hybrid Service Models

The rise of third-party repair organizations and hybrid service models presents one of the strongest opportunities in the endoscope repair market. Hospitals increasingly seek cost-effective, flexible, and faster repair options, areas where independent service providers often outperform OEMs. Analysts estimate that third-party firms already service nearly one-third of endoscopes in several regions, capturing about 20% of service revenue due to competitive pricing and quicker turnaround times. These companies offer tailored service contracts, extended warranties, and on-site repair capabilities, helping healthcare facilities reduce downtime and optimize equipment utilization.

Hybrid models are emerging in which OEMs and independent providers collaborate through co-branded service centers, shared diagnostic platforms, or authorized partner programs. Such arrangements allow hospitals to access OEM-level quality with the agility and affordability of third-party services. Advancements in digital platforms such as cloud-based service tracking, automated scheduling, and predictive maintenance analytics further enhance transparency and efficiency. As healthcare systems focus on lifecycle management and cost containment, the expansion of third-party and hybrid service models is poised to create new revenue streams and reshape the competitive landscape.

Category-wise Analysis

By Product Type Insights

Across product types, gastrointestinal endoscopes, such as Colonoscopes and Gastroscope, account for a substantial share of repair volumes due to their very high utilization in colorectal cancer screening and upper GI diagnostics. Studies show that diagnostic and operative esophagogastroduodenoscopy procedures are performed at rates exceeding 9 per 1,000 inhabitants annually, and colonoscopy volumes are similarly high in organized screening programs, leading to frequent mechanical, optical, and channel-related failures that require repair. In many hospitals, colonoscopes alone can represent more than one-third of the endoscope fleet, and their intensive use during screening campaigns accelerates wear on insertion tubes, distal tips, and biopsy channels. With the expansion in cancer screening programs and lowering age thresholds in the U.S., the need for colonoscopies and gastroscopes is likely to remain robust and on account of less-used scopes such as esophagoscopes or duodunoscopes.

By Modality Type Insights

By modality, flexible endoscopes dominate the endoscope repair market with an estimated 73% share in 2025, reflecting their central role in modern minimally invasive diagnostics and therapy. Flexible instruments are widely used in gastroenterology, pulmonology, urology, and gynecology, and their intricate design, including fiber bundles, distal bending sections, and multiple internal channels, makes them more susceptible to damage than rigid scopes. Research has documented frequent reprocessing-related wear, with flexible ureteroscopes in some centers requiring repair every 9–10 cases, illustrating the intensive service needs typical for this modality. Continuous innovations in imaging quality, wider working channels, and integrated accessories further increase the value and complexity of flexible scopes, reinforcing their share of repair revenues compared with more durable rigid devices used in laparoscopy or arthroscopy.

Region-wise Insights

North America Endoscope Repair Market Trends

North America is expected to dominate the global endoscope repair market, holding approximately 36% market share in 2025. The region’s leadership is driven by a high volume of endoscopic procedures, a well-developed healthcare infrastructure, and stringent regulatory standards for device maintenance and infection control. Hospitals, ambulatory surgery centers, and specialized clinics depend heavily on both OEM and third-party repair and reprocessing services to ensure the uninterrupted operation of flexible and rigid endoscopes used across gastrointestinal, bronchoscopy, and surgical applications.

The widespread use of automated reprocessors and leak-testing systems, and adherence to regulatory compliance guidelines, further reinforce demand for certified repair services. With high-definition and specialty endoscopes often costing tens of thousands of dollars per unit, institutions prefer repair and refurbishment over replacement, generating recurring service revenue for providers. The combination of increasing procedure volumes, an aging installed base, and a focus on reducing operational costs contributes to steady growth in North America. Additionally, healthcare providers’ preference for preventive maintenance and rapid turnaround repair services strengthens the adoption of both OEM-led and third-party endoscope repair solutions.

Asia and Pacific Endoscope Repair Market Trends

The Asia-Pacific region is emerging as the fastest-growing market for endoscope repair services, fueled by the rapid expansion of healthcare infrastructure, rising procedural volumes, and growing adoption of minimally invasive diagnostics and surgical interventions.

Countries such as China, India, Japan, and South Korea are significantly expanding hospital networks and endoscopy centers, creating sustained demand for maintenance, repair, and reprocessing services, particularly for flexible endoscopes used in gastrointestinal, pulmonary, and surgical procedures. Cost considerations in many APAC markets drive hospitals and clinics to prefer repair over replacement, increasing reliance on third-party and independent service providers capable of offering affordable and timely solutions. Growing awareness of infection control, sterilization standards, and regulatory compliance further emphasizes the importance of certified repair services.

Additionally, increasing installation of advanced endoscopic equipment, such as high-definition and specialty scopes, requires specialized servicing and refurbishment programs. Investments in regional service centers, on-site maintenance capabilities, and preventive maintenance contracts are becoming more common, enabling hospitals to reduce downtime and extend the lifespan of endoscopic devices. These trends collectively support robust growth of the Asia-Pacific endoscope repair market over the coming years.

Competitive Landscape

The global endoscope repair market is characterized by a mix of OEM service divisions and independent third-party repair providers competing on cost, turnaround time, and service quality. Major manufacturers such as Olympus, Stryker, Fujifilm, and Karl Storz offer authorized repair programs, while specialized firms provide multi-brand repair solutions that appeal to facilities seeking budget-friendly options. Competition is strengthened by hospitals increasingly outsourcing maintenance to reduce downtime and improve device performance. Vendors differentiate through technical expertise, availability of certified parts, preventive maintenance programs, and regional service networks that ensure reliable, timely support.

Key Industry Developments:

- In September 2023, IRCAD proudly announced a strategic partnership with Pentax Medical. This collaboration aims to enhance healthcare training and improve patient outcomes by leveraging advanced flexible endoscopy technology.

Companies Covered in Endoscope Repair Market

- Stryker Corporation

- Medivators Inc.

- Olympus Corporation

- Pentax Medical Company (Hoya Corporation)

- Smith & Nephew PLC.

- Fujifilm Holdings Corp.

- Karl Storz GmbH & Co. KG

- Medserv International, Inc.

- Endoscopy Repair Specialist Inc.

- Fibertech Incorporation

- Associated Endoscopy, Inc.

- EndocorpUSA

- Others

Frequently Asked Questions

The global endoscope repair market is projected to be valued at US$ 1.6 Bn in 2026.

Growing endoscopy procedures, rising equipment wear-and-tear, high replacement costs, and demand for faster turnaround drive endoscope repair growth.

The global endoscope repair market is poised to witness a CAGR of 6.0% between 2026 and 2033.

Opportunities include outsourced repair models, service contracts, refurbished scope demand, emerging-market expansion, and AI-based predictive maintenance solutions.

Key companies include Stryker Corporation, Medivators Inc., Olympus Corporation, Pentax Medical Company (Hoya Corporation), and Smith & Nephew PLC.