- Medical Devices

- Global Endoscopes Market

Global Endoscopes Market Size, Share, and Growth Forecast 2026 - 2033

The global endoscopes market by product type (rigid endoscopes, flexible endoscopes, capsule endoscopes, disposable (single-use) endoscopes), by application (gastroenterology, pulmonology, urology, gynecology, orthopedics, others), by end user (hospitals, specialty clinics, ambulatory surgical centers (ASCs), diagnostic centers), and by regional analysis, 2026-2033

Endoscopes Market Size and Trends Analysis

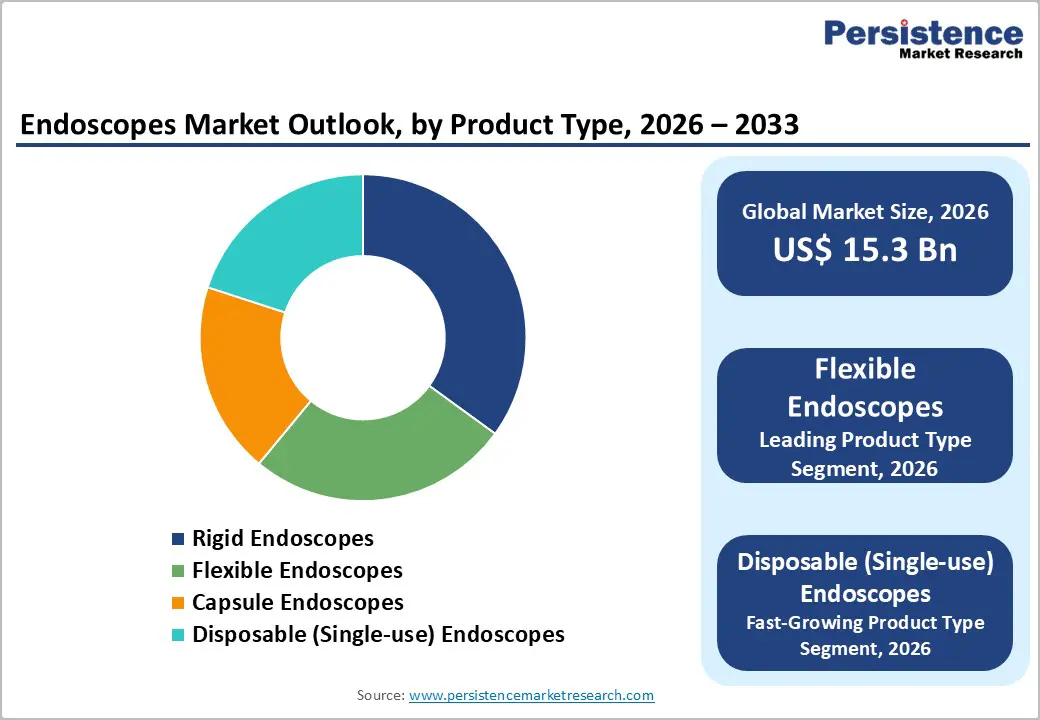

The global endoscopes market size is expected to be valued at US$ 15.3 billion in 2026 and projected to reach US$ 23.4 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Strong demand for minimally invasive procedures, coupled with rising prevalence of gastrointestinal, respiratory, and urological diseases, is accelerating adoption of advanced endoscopic systems across hospital and ambulatory settings. This growth is further supported by continuous product innovation, including high definition imaging, robotics, and single use endoscopes that address infection control concerns and improve procedural efficiency. Favorable reimbursement in major markets and expanding procedure volumes in Asia Pacific underpin a stable, long term growth outlook for both reusable and disposable endoscopes.

Key Market Highlights

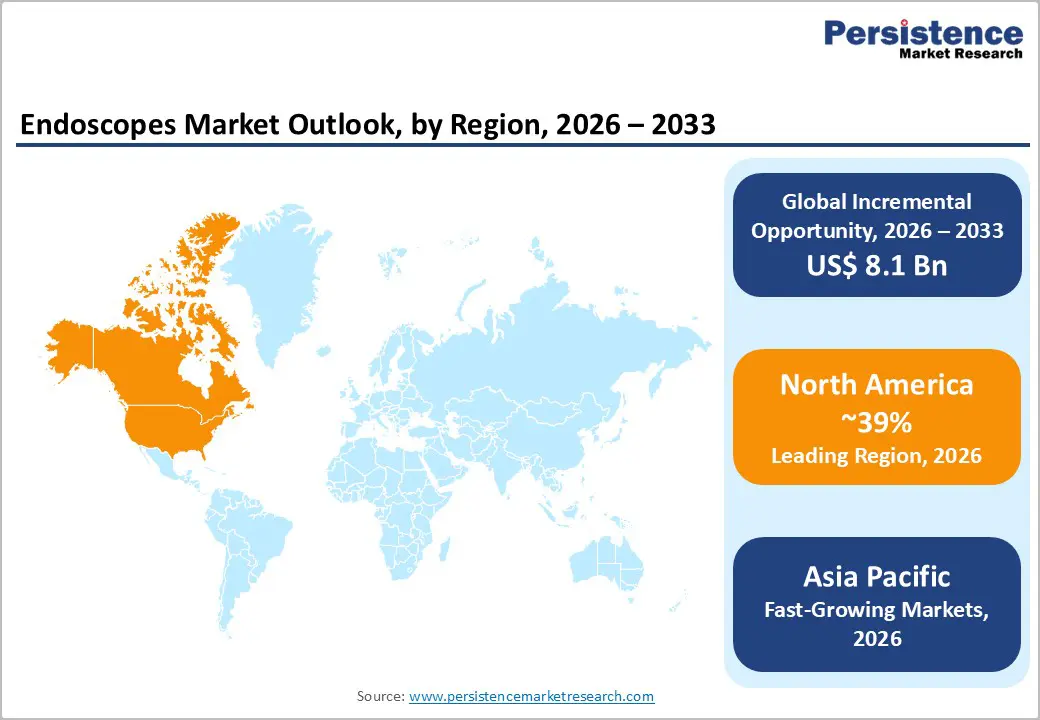

- North America leads the endoscopes market, supported by high procedure volumes, strong reimbursement, and robust adoption of advanced imaging and infection control technologies across hospitals and ambulatory centers.

- Asia Pacific is the fastest growing region, driven by large patient pools, rapid healthcare expansion in China, India, and ASEAN, and rising uptake of minimally invasive procedures in both public and private sectors.

- Flexible endoscopes dominate product demand, with the largest market share due to their critical role in GI, pulmonary, urological, and gynecological procedures and continuous advances in visualization quality.

- Disposable (single-use) endoscopes form the fastest growing segment as hospitals seek to reduce infection risk, reprocessing burden, and cross-contamination, supported by clinical evidence of lower complication rates.

- A key opportunity lies in AI-enabled, robot-assisted, and smart endoscopy platforms that improve diagnostic accuracy, procedural efficiency, and safety, creating new revenue streams for technology-focused manufacturers.

| Global Market Attributes | Key Insights |

|---|---|

| Endoscopes Market Size (2026E) | US$ 15.3 billion |

| Market Value Forecast (2033F) | US$ 23.4 billion |

| Projected Growth CAGR (2026-2033) | 6.2% |

| Historical Market Growth (2020-2025) | 5.8% |

Market Dynamics

Market Growth Drivers

Rising burden of gastrointestinal and chronic diseases

The growing incidence of gastrointestinal disorders, colorectal cancer, obesity, and liver diseases is a primary driver of endoscope demand. The World Health Organization (WHO) reports that colorectal cancer is among the top three most common cancers worldwide, with millions of new cases annually, driving large volumes of colonoscopy and GI endoscopy procedures for screening and diagnosis. Gastrointestinal endoscopy already accounts for around 32.3% of the procedure share in the endoscopes market, underlining its central role in clinical practice. In addition, an aging population with higher prevalence of chronic conditions such as COPD and urological disorders increases the need for bronchoscopy, cystoscopy, and related endoscopic interventions, reinforcing sustained procedure growth across care settings.

Shift toward minimally invasive and day care procedures

Patient and provider preference for minimally invasive procedures is strongly boosting the endoscopes market. Endoscopic interventions reduce hospital stay, lower complication risks, and enable faster recovery compared to open surgery, aligning with value-based care and cost containment objectives. Global endoscopy procedure volumes have expanded significantly, with Asia Pacific accounting for over 43% of all endoscopy procedures in 2021, reflecting both rising access and demand. The proliferation of ambulatory surgical centers and outpatient endoscopy units, combined with advances in high definition visualization and therapeutic tools, is enabling more complex procedures to be performed in day care settings, thereby increasing utilization of endoscopes across specialties from gastroenterology to orthopedics and gynecology.

Market Restraints

Infection control challenges with reusable endoscopes

Despite robust growth, infection control concerns remain a significant restraint for reusable endoscopes. Clinical literature shows that flexible endoscopes are among the medical devices most frequently linked to healthcare-associated infections due to complex designs that hinder effective cleaning. Studies indicate that even when reprocessing follows guidelines, residual microbial contamination and biofilm formation can persist in channels and ports, contributing to outbreaks of Pseudomonas aeruginosa and other pathogens. These safety concerns have prompted regulatory scrutiny, hospital audits, and, in some cases, temporary procedure disruptions, increasing operational burden and dampening adoption of older reusable systems.

High capital costs and reimbursement pressure

High upfront capital expenditure for endoscopy towers, video processors, and premium scopes, along with recurring maintenance and reprocessing costs, can constrain adoption, particularly in resource-constrained settings. Hospitals and smaller facilities must balance investments in rigid, flexible, and capsule endoscopes with competing budget priorities such as imaging and robotic surgery platforms. In parallel, reimbursement pressure in many health systems forces providers to seek cost efficiencies, sometimes delaying upgrades or limiting access to cutting edge platforms. This cost barrier is particularly relevant for emerging markets and smaller ambulatory centers, moderating the pace of penetration despite clear clinical benefits.

Market Opportunities

Rapid adoption of disposable (single-use) endoscopes

Disposable or single-use endoscopes represent one of the most compelling opportunities in the endoscopes market, especially in high-income countries. Evidence comparing reusable and single-use flexible endoscopes shows substantial infection control advantages, with reusable scopes associated with higher contamination and complication risks even under rigorous reprocessing. A recent meta-analysis indicated that reusable endoscopes can have up to 25% higher complication risk, while single-use devices significantly reduce post procedural fever and infection. These findings, coupled with the resource burden of cleaning, traceability, and repairs, are encouraging hospitals and ambulatory centers to pilot and gradually scale single-use bronchoscopes, cystoscopes, and GI scopes.

Category-wise Insights

Product Type Analysis

Flexible endoscopes as the leading product segment

Flexible endoscopes are the leading product segment in the global endoscope market due to their versatility, wide clinical application, and minimally invasive nature. Unlike rigid endoscopes, flexible endoscopes can navigate complex anatomical pathways, making them essential for gastroenterology, pulmonology, urology, and ENT procedures. Their ability to provide real-time imaging, coupled with advanced features like high-definition visualization and video integration, enhances diagnostic accuracy and procedural efficiency. Additionally, the growing preference for outpatient and minimally invasive surgeries has significantly boosted their adoption in hospitals, specialty clinics, and ambulatory surgical centers. The rising prevalence of chronic diseases such as gastrointestinal disorders, respiratory ailments, and urinary tract complications further drives demand, positioning flexible endoscopes as the largest and most critical segment in the endoscope market globally.

Application Analysis

Gastroenterology accounts for the highest share in the global endoscopes market

Gastroenterology dominates the endoscope market because it encompasses the most frequently performed diagnostic and therapeutic procedures. Conditions such as colorectal cancer, gastric ulcers, inflammatory bowel disease, and gastrointestinal bleeding are highly prevalent worldwide, driving routine use of endoscopic interventions. Colonoscopy and gastroscopy, key procedures in this field, are critical for early detection, prevention, and treatment, which increases procedure volumes significantly compared to other specialties. The adoption of advanced flexible and high-definition endoscopes further enhances the accuracy and efficiency of gastrointestinal examinations, encouraging their widespread use in hospitals, specialty clinics, and ambulatory surgical centers. Government-led screening programs for colorectal and gastric cancers also contribute to higher procedural demand. Combined with the rising incidence of GI disorders due to lifestyle and dietary changes, these factors make gastroenterology the largest and most impactful application segment in the global endoscope market.

End User Analysis

Hospitals are the dominant end-user segment

Hospitals constitute the dominant end-user segment for the endoscopes market, capturing the largest share of procedure volumes globally. Large tertiary and secondary hospitals house multidisciplinary endoscopy suites that support gastroenterology, pulmonology, urology, gynecology, and orthopedic procedures under one roof. They are also the primary sites for complex therapeutic interventions such as ERCP, ESD, and advanced bronchoscopic procedures, which require high-end imaging systems and specialized staff. In addition, hospitals have greater capacity to invest in premium systems and centralized reprocessing units, making them the key customers for leading manufacturers and the focal point for new product launches and clinical trials.

Regional Insights

North America Endoscopes Market Trends and Insights

North America is the leading regional market for endoscopes, accounting for an estimated 39% share in 2025, underpinned by the United States as the primary demand center. High procedure volumes, early adoption of innovative technologies, and favorable reimbursement for minimally invasive procedures support robust utilization across hospitals and ambulatory centers. The U.S. Food and Drug Administration (FDA) has issued detailed guidance on endoscope reprocessing and post market surveillance, pushing manufacturers toward safer designs and driving interest in single use devices, particularly for bronchoscopy and urology.

The region also benefits from a strong innovation ecosystem, with leading companies investing in AI enabled imaging, robotic assisted endoscopy, and smart processing systems. Major academic medical centers in the U.S. and Canada frequently participate in clinical trials evaluating new endoscopic platforms and techniques, accelerating time to market for breakthrough technologies. Together, this ecosystem of stringent regulatory oversight, high healthcare spending, and technology leadership cements North America’s position as the benchmark market for advanced endoscopy solutions.

Asia Pacific Endoscopes Market Trends and Insights

In the Asia Pacific region, the endoscopes market is emerging as one of the fastest growing global hubs due to multiple structural and demand side trends. Rapid investments in healthcare infrastructure across countries like China, India, Japan, and South Korea are expanding access to quality diagnostic services, leading to higher adoption of endoscopic procedures. Rising prevalence of chronic diseases such as gastrointestinal and respiratory disorders, along with an aging population, further amplifies the need for minimally invasive diagnostics. Technological advancements, including high definition imaging, AI integration, and portable endoscopic systems, are improving procedural outcomes and attracting both public and private healthcare providers. Government initiatives to modernize healthcare and increase preventive care awareness are also boosting endoscopy adoption. Additionally, medical tourism and expanding healthcare access in tier 2 and tier 3 cities contribute to sustained demand growth in the region.

Competitive Landscape

Market Structure Analysis

The global endoscopes market is moderately consolidated, with a handful of multinational corporations accounting for a significant share alongside specialized regional players. Leading companies compete on imaging performance, ergonomic design, breadth of procedural instruments, and after sales service, while increasingly differentiating through AI enabled software, integrated platforms, and infection control features. R&D pipelines are focused on disposable endoscopes, robotic and navigational systems, and enhanced imaging modalities, often developed through strategic partnerships and acquisitions. Emerging business models include equipment as a service, managed endoscopy suites, and bundled device plus software offerings, aligning vendor incentives with procedural volumes and outcomes.

Key Market Developments

- In July 2025, FUJIFILM (Thailand) Ltd. advanced healthcare diagnostics and patient treatment with comprehensive health innovations by unveiling the ELUXEO® 8000 Endoscopy System and the 800 Series ELUXEO® Endoscopes for the first time in Thailand. The launch occurred at the 50th Annual Scientific Congress of the Royal College of Surgeons of Thailand (RCST 2025) from July 10-12, 2025, which was organized in collaboration with the Ministry of Public Health and the National Health Security Office under the theme "RCST Half Century: The Changing Landscape of Surgery."

- In November 2025, Olympus Canada Inc. (OCI), a leader in medical technology for gastrointestinal endoscopy, launched the EZ1500 series endoscopes featuring Extended Depth of Field (EDOF™) technology.

Companies Covered in Global Endoscopes Market

- Medtronic Plc.

- Olympus Corporation

- KARL STORZ SE & Co. KG

- Johnson & Johnson

- Fujifilm Holdings Corporation

- Richard Wolf GmbH

- Braun Melsungen Ag

- Stryker Corporation

- PENTAX Medical

- CONMED Corporation

- Boston Scientific Corporation

- Smith & Nephew PLC

- GS Yuasa International Ltd.

- NEXcell Battery Company

- BYD Company Limited

Frequently Asked Questions

The global endoscopes market size is expected to reach about US$ 15.3 billion in 2026, driven by rising minimally invasive procedures and growing chronic disease burden worldwide.

A key demand driver is the increasing prevalence of gastrointestinal, respiratory, and urological diseases, which boosts procedure volumes for diagnostic and therapeutic endoscopy across hospitals and ambulatory centers.

North America is expected to lead the market with an estimated 39% share in 2025, driven by high procedure volumes, strong reimbursement, and the rapid adoption of advanced endoscopic technologies.

A major opportunity is the rapid expansion of disposable (single‑use) endoscopes and AI‑enabled platforms that reduce infection risk, streamline workflows, and enhance diagnostic accuracy, especially in high‑income countries.

Key players include Medtronic Plc., Olympus Corporation, KARL STORZ SE & Co. KG, Johnson & Johnson, Fujifilm Holdings Corporation, Richard Wolf GmbH, B. Braun Melsungen AG, Stryker Corporation, PENTAX Medical, CONMED Corporation, Boston Scientific Corporation, Smith & Nephew plc, Ambu A/S, and Cook Medical, among others.