- Medical Devices

- Endocavity Transducer Market

Endocavity Transducer Market Size, Share, and Growth Forecast, 2026 – 2033

Endocavity Transducer Market by Product Type (Curvilinear, Phased array, Endocavity, Linear), Technology (2D, 3D/4D, Doppler, Color Doppler, Power Doppler), and Regional Analysis for 2026 – 2033

Endocavity Transducer Market Size and Trends Analysis

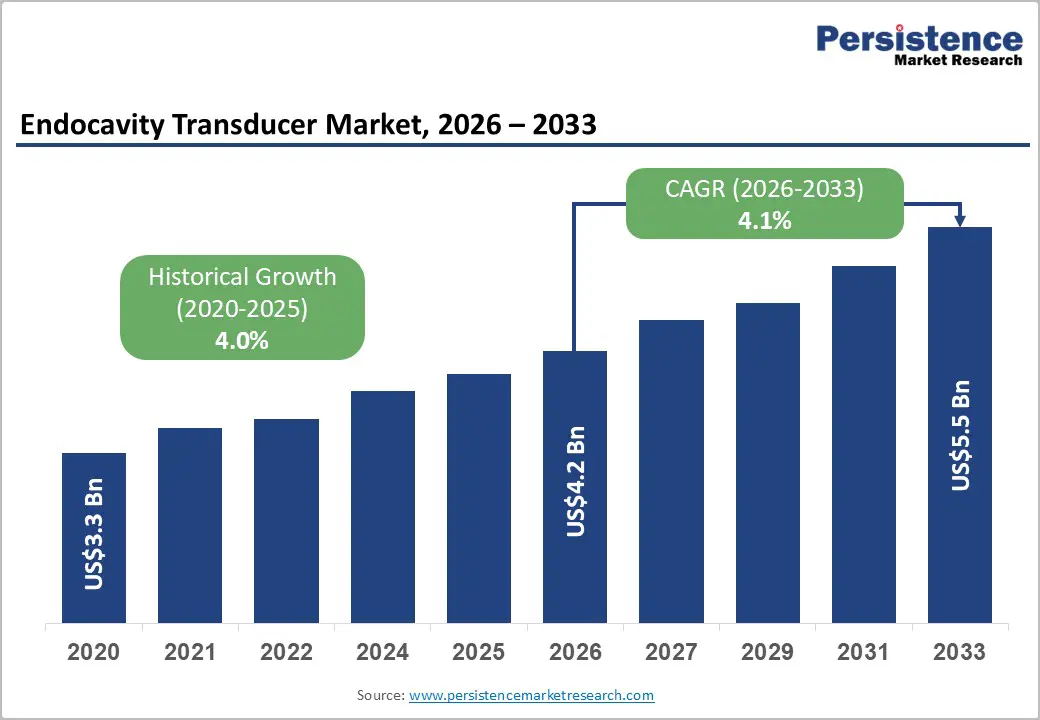

The global endocavity transducer market size is likely to be valued at US$4.2 billion in 2026 and is expected to reach US$5.5 billion by 2033, growing at a CAGR of 4.1% during the forecast period from 2026 to 2033, driven by the increasing demand for high-resolution internal ultrasound imaging across several clinical specialties.

These transducers are widely used in diagnostic procedures that require close-range imaging within body cavities, particularly in gynecology, obstetrics, and urology. Growing emphasis on early disease detection and preventive healthcare has significantly increased the use of ultrasound-based examinations, especially for pelvic assessments, prostate evaluations, and prenatal monitoring. According to the World Health Organization, global cancer incidence continues to rise, with approximately 20 million new cancer cases reported worldwide in 2022, highlighting the increasing need for advanced diagnostic imaging technologies. Improvements in probe design, including enhanced ergonomics, higher frequency capabilities, and better imaging sensitivity, have strengthened diagnostic efficiency and clinician adoption in hospitals and diagnostic facilities.

Key Industry Highlights:

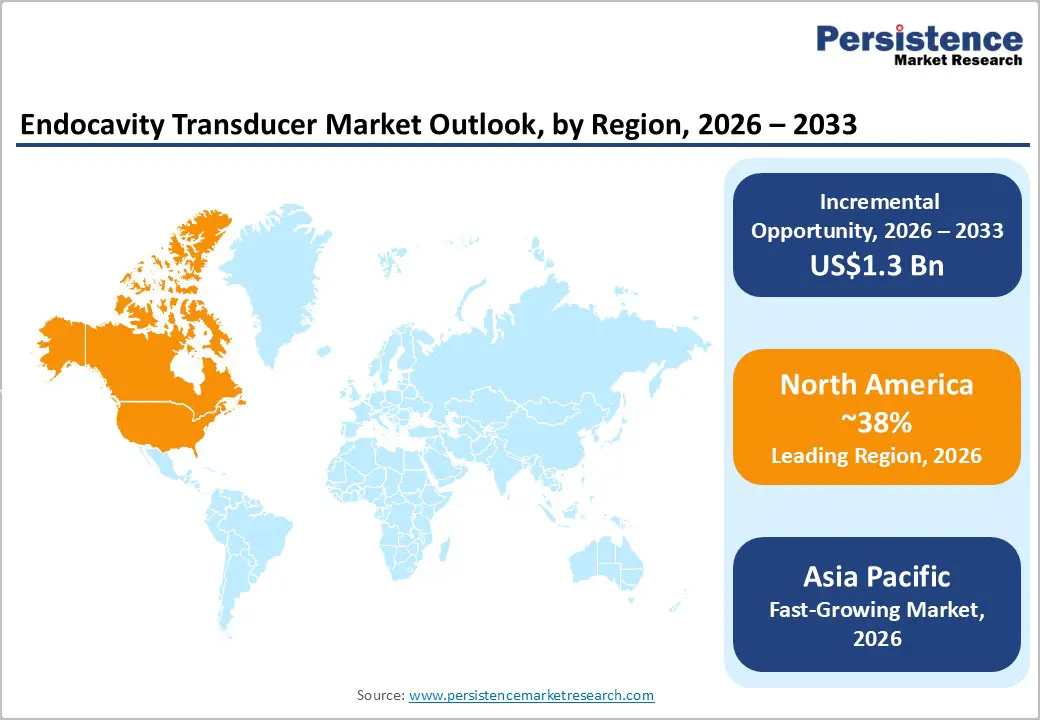

- Leading Region: North America, accounting for a market share of 38% in 2026, driven by advanced healthcare infrastructure, high adoption of ultrasound diagnostics, and strong demand for gynecological and urological imaging procedures.

- Fastest-growing Region: Asia Pacific, supported by expanding healthcare infrastructure, rising diagnostic demand, and increasing adoption of ultrasound technologies across major economies in the region.

- Leading Product Type: Endocavities, accounting for 41% of the revenue share, driven by their extensive use in transvaginal and transrectal imaging for gynecology and urology diagnostics.

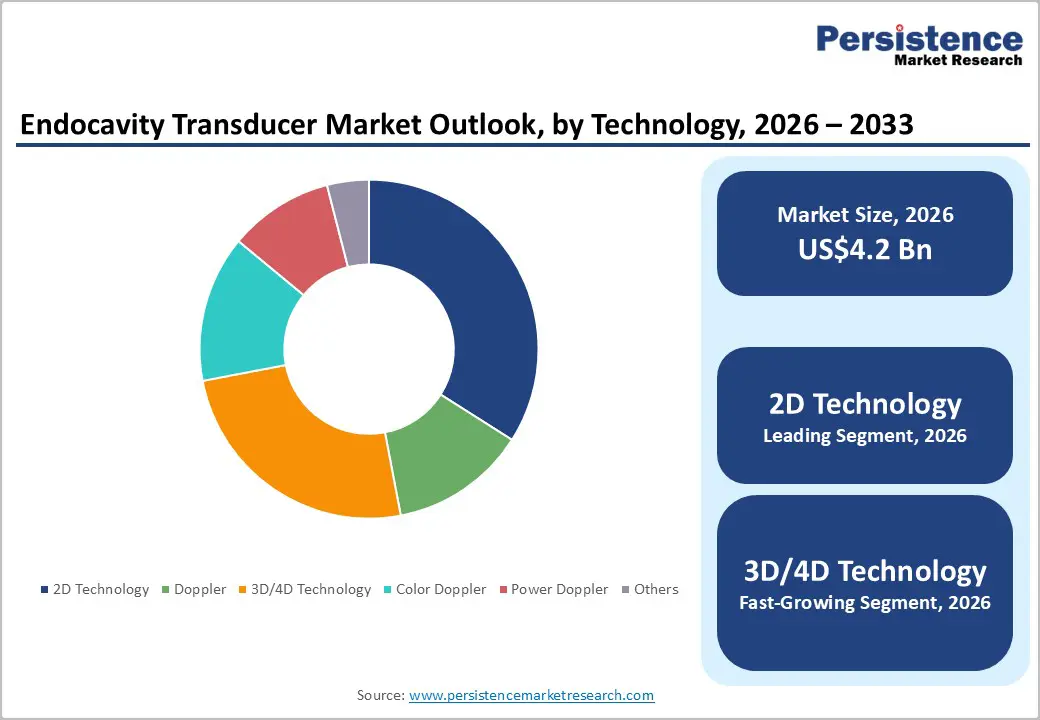

- Leading Technology: 2D technology, accounting for over 46% of the revenue share in 2026, supported by its widespread clinical adoption, cost-effectiveness, and extensive use in routine diagnostic ultrasound procedures across hospitals and diagnostic centers.

| Key Insights | Details |

|---|---|

| Endocavity Transducer Market Size (2026E) | US$4.2 Bn |

| Market Value Forecast (2033F) | US$5.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Rising Prevalence of Target Diseases and Minimally Invasive Diagnostics

The increasing prevalence of gynecological disorders, prostate diseases, and reproductive health conditions is a major driver of demand for endocavity transducers. These devices are widely used in transvaginal and transrectal ultrasound procedures to detect abnormalities in pelvic organs, monitor pregnancies, and evaluate prostate conditions. Rising awareness of early disease detection and preventive screening programs is encouraging more patients to undergo ultrasound examinations. Hospitals and diagnostic centers increasingly rely on endocavity probes because they provide high-resolution imaging of internal structures, enabling accurate diagnosis without invasive surgical procedures.

Healthcare systems are emphasizing minimally invasive diagnostic techniques that reduce patient discomfort and hospital stay. Endocavity ultrasound procedures are considered safe, efficient, and cost-effective for evaluating pelvic and reproductive organs. Growing patient preference for outpatient diagnostic procedures has expanded the use of these probes in clinics and ambulatory centers. The aging population and increasing incidence of chronic conditions such as prostate enlargement and gynecological cancers are strengthening long-term demand.

Technological Advancements in Imaging Modalities

Continuous advancements in ultrasound imaging technologies are significantly driving the adoption of endocavity transducers in modern diagnostic systems. Improvements in probe design, higher frequency capabilities, and enhanced signal processing have enabled clearer visualization of internal organs and tissues. Modern endocavity probes now support advanced imaging modes that provide more detailed and accurate diagnostic information. Healthcare providers increasingly prefer technologically advanced ultrasound systems that deliver improved resolution and faster imaging, which enhances clinical decision-making in gynecology, obstetrics, and urology procedures.

Innovations such as three-dimensional and four-dimensional imaging, Doppler imaging modes, and compact portable ultrasound platforms are expanding the clinical capabilities of endocavity transducers. These technological developments allow physicians to detect subtle abnormalities and evaluate blood flow or tissue structures more effectively. Manufacturers are also focusing on ergonomic probe designs and improved durability to enhance usability and patient comfort during examinations. Integration of advanced imaging technologies into diagnostic workflows is encouraging healthcare providers to upgrade existing ultrasound equipment, thereby supporting steady demand for next-generation endocavity transducers in hospitals and specialized diagnostic facilities.

Barrier Analysis - Infection Control and Reprocessing Challenges

Infection control remains a significant challenge in the use of endocavity transducers because these probes come into direct contact with internal body cavities during diagnostic procedures. Proper cleaning, high-level disinfection, and sterilization are essential after each use to prevent cross-contamination between patients. Maintaining strict reprocessing protocols can be time-consuming and requires specialized equipment and trained personnel. Healthcare facilities must follow stringent hygiene standards to ensure patient safety, which can increase operational complexity and limit workflow efficiency in busy diagnostic environments.

Regulatory guidelines and infection control standards are becoming increasingly strict, requiring healthcare providers to invest in advanced disinfection technologies and monitoring systems. Improper reprocessing may lead to healthcare-associated infections, which can damage institutional reputation and result in regulatory penalties. These concerns sometimes discourage smaller clinics from adopting advanced endocavity probes due to the added responsibility of maintaining strict sterilization protocols. Infection control challenges remain a key restraint affecting widespread adoption, particularly in resource-limited healthcare settings and emerging markets.

Competitive Pressures from Alternative Imaging Modalities

The endocavity transducer market also faces competition from other advanced imaging technologies, such as magnetic resonance imaging and computed tomography. These modalities provide comprehensive diagnostic information and are sometimes preferred for complex disease evaluation. In certain cases, physicians choose alternative imaging techniques when broader anatomical visualization or greater diagnostic detail is required. This competitive pressure can reduce the reliance on ultrasound-based imaging in specific clinical scenarios, particularly in well-equipped healthcare facilities.

Some healthcare providers consider alternative imaging technologies for oncology and advanced diagnostic assessments due to their ability to capture multi-dimensional data and detailed tissue characterization. Although ultrasound remains widely used due to its affordability and accessibility, the presence of advanced imaging systems such as MRI and CT in developed healthcare facilities reduces the reliance on endocavity transducers in certain complex diagnostic procedures, as physicians prefer these modalities for broader anatomical visualization and detailed tissue evaluation. The increasing integration of hybrid imaging approaches also creates competition within diagnostic workflows, making it necessary for ultrasound manufacturers to continuously innovate to maintain clinical relevance.

Opportunity Analysis - Upselling to 3D/4D and Doppler-Enabled Probes

A major opportunity in the endocavity transducer market lies in the growing demand for advanced imaging technologies such as three-dimensional, four-dimensional, and Doppler-enabled probes. Healthcare providers increasingly seek enhanced imaging capabilities that allow better visualization of internal organs, vascular structures, and fetal development. These advanced probes provide more detailed diagnostic information compared with traditional two-dimensional imaging. Hospitals and diagnostic centers are upgrading their ultrasound equipment to incorporate more advanced imaging modes that improve diagnostic confidence and clinical outcomes.

The shift toward technologically advanced ultrasound systems also enables manufacturers to promote premium endocavity probes with enhanced imaging performance. Upgrading existing diagnostic equipment with advanced probes can significantly improve examination quality while maintaining the cost advantages of ultrasound technology. Improved visualization in obstetric and gynecological applications is encouraging clinicians to adopt advanced imaging tools for detailed fetal and pelvic assessments. This ongoing transition toward advanced ultrasound modalities is creating opportunities for manufacturers to expand their product portfolios and strengthen their presence by offering technologically enhanced probes with improved imaging capabilities and diagnostic efficiency.

Integration into Image-Guided and Fusion Biopsy Workflows

Another promising opportunity for the endocavity transducer market is the growing integration of ultrasound technology into image-guided diagnostic and interventional procedures. Endocavity probes are increasingly used in procedures such as prostate biopsies, fertility treatments, and minimally invasive therapeutic interventions. Their ability to provide real-time imaging guidance helps physicians perform procedures with higher precision and reduced risk. This expanding role in image-guided procedures is strengthening the importance of endocavity transducers in modern clinical practice.

The development of fusion imaging technologies, which combine ultrasound images with other imaging modalities, is creating new clinical applications for endocavity probes. Fusion biopsy systems enable more accurate targeting of suspicious lesions by integrating ultrasound with other diagnostic imaging data. This advancement improves diagnostic accuracy and enhances patient outcomes in procedures such as prostate cancer detection. As healthcare providers use image-guided interventions, specialized endocavity transducers support precise visualization and guidance in diagnostic and minimally invasive procedures.

Category-wise Analysis

Product Type Insights

The endocavity segment is expected to lead, accounting for approximately 41% of revenue in 2026, driven by its specialized role in internal ultrasound imaging procedures. These probes are primarily used for transvaginal and transrectal examinations, enabling clinicians to obtain high-resolution images of pelvic organs, reproductive structures, and the prostate. Their widespread adoption in gynecology, obstetrics, and urology diagnostics significantly contributes to their leading position.

For example, GE HealthCare Technologies Inc. offers advanced endocavity ultrasound probes designed for high-precision pelvic imaging, which are widely used in hospitals and fertility clinics to support accurate diagnosis and patient monitoring.

Linear probes are likely to represent the fastest-growing segment, supported by healthcare providers increasingly adopting high-frequency imaging technologies for detailed diagnostic applications. Linear probes provide excellent image clarity for superficial structures and are being increasingly integrated into broader ultrasound systems used in combination with endocavity imaging workflows. Their rising adoption is linked to the growing demand for versatile ultrasound devices that can perform multiple diagnostic procedures within a single system.

For example, Canon Medical Systems Corporation has developed advanced ultrasound systems equipped with high-frequency linear probes that support improved visualization and are increasingly utilized in modern diagnostic imaging environments.

Technology Insights

The 2D technology is projected to lead the market, capturing around 46% of the revenue share in 2026, supported by its widespread availability and extensive use in routine diagnostic imaging procedures. Two-dimensional ultrasound imaging has long been the standard technology used in hospitals and diagnostic centers because it provides reliable real-time visualization of internal organs while remaining cost-effective and easy to operate. For example, Mindray Medical International Limited offers ultrasound platforms with advanced 2D imaging capabilities that are widely used in hospitals and diagnostic facilities for routine endocavity examinations.

3D/4D technology is likely to be the fastest-growing technology, driven by increasing demand for advanced visualization in obstetric and pelvic diagnostic procedures. These technologies provide detailed volumetric images that allow physicians to observe anatomical structures more clearly compared to traditional imaging methods. In obstetric care, 3D and 4D imaging help clinicians monitor fetal development with improved accuracy and detect potential abnormalities at earlier stages.

The ability to visualize tissues and organs from multiple angles also enhances diagnostic confidence in complex gynecological assessments. For example, Samsung Medison Co., Ltd. offers ultrasound solutions equipped with advanced 3D and 4D imaging technologies that enable detailed visualization during obstetric and gynecological examinations, supporting improved diagnostic accuracy.

Regional Insights

North America Endocavity Transducer Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by strong technological adoption and well-established diagnostic infrastructure, particularly in the U.S. and Canada. Hospitals and specialized diagnostic centers widely use endocavity ultrasound probes for gynecology, obstetrics, and urology procedures due to their ability to provide accurate real-time imaging of pelvic organs and prostate structures. Increasing awareness of early disease detection and preventive healthcare screening programs has expanded the number of ultrasound examinations performed across healthcare systems.

The region benefits from advanced healthcare spending, strong reimbursement policies, and a high concentration of specialized imaging centers.

The increasing focus on advanced ultrasound technologies, including high-resolution imaging, ergonomic probe design, and AI-supported diagnostic capabilities. Healthcare providers are adopting modern ultrasound systems that improve imaging clarity and procedural efficiency for applications such as fertility assessments, prostate evaluations, and minimally invasive biopsy guidance. The presence of major medical imaging manufacturers supports innovation and market expansion across North America.

For example, Philips Healthcare offers advanced ultrasound platforms equipped with specialized endocavity probes designed to enhance visualization during obstetric and gynecological examinations.

Europe Endocavity Transducer Market Trends

Europe is likely to be a significant market for endocavity transducers, due to strong clinical adoption and well-established healthcare systems across countries such as Germany, France, the U.K., and the Nordic region. Hospitals and fertility clinics in these countries widely use endocavity ultrasound probes for gynecology, obstetrics, and prostate imaging procedures. The region places strong emphasis on preventive healthcare, early cancer detection, and reproductive health services, which contribute to steady demand for high-precision ultrasound diagnostics.

European healthcare providers also prioritize patient safety, ergonomic probe design, and strict infection-control protocols during diagnostic procedures.

Healthcare providers are adopting modern ultrasound systems that offer improved image resolution, advanced visualization features, and better integration with digital healthcare platforms. Regulatory frameworks such as the European medical device standards encourage manufacturers to develop safe, efficient, and high-quality diagnostic equipment. The presence of established imaging technology companies contributes to continuous product development and market competitiveness.

For example, Esaote S.p.A., an Italy-based medical imaging manufacturer, provides advanced ultrasound systems and endocavity probes widely used across European hospitals for gynecological and urological imaging procedures.

Asia Pacific Endocavity Transducer Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by strong development due to expanding healthcare infrastructure, increasing investments in diagnostic imaging technologies, and rising awareness of early disease detection across countries such as China and India. Hospitals and diagnostic centers across the region are increasingly adopting ultrasound-based diagnostic tools for gynecological, obstetric, and urological examinations. The growing prevalence of chronic diseases and reproductive health conditions is encouraging healthcare providers to rely on non-invasive imaging technologies that provide real-time clinical insights.

The strong presence of regional ultrasound manufacturers that focus on cost-effective and technologically advanced imaging solutions. Healthcare providers increasingly prefer modern ultrasound systems that support high-resolution imaging, improved probe ergonomics, and enhanced workflow efficiency for routine diagnostic procedures. Regional manufacturers are also introducing specialized ultrasound platforms designed for obstetrics and gynecology applications, supporting the use of endocavity probes in clinical practice.

For example, Shenzhen Mindray Bio?Medical Electronics Co., Ltd. expanded its ultrasound portfolio with dedicated obstetrics and gynecology systems designed to support pelvic and reproductive health examinations with improved usability and ergonomic design.

Competitive Landscape

The global endocavity transducer market exhibits a moderately fragmented structure, driven by the growing demand for minimally invasive diagnostic imaging, continuous advancements in ultrasound technology, and increasing clinical applications in gynecology, obstetrics, and urology. Healthcare providers increasingly require high-resolution imaging solutions that provide accurate visualization of pelvic organs and internal tissues.

With key leaders including GE HealthCare Technologies Inc., Koninklijke Philips N.V., Canon Medical Systems Corporation, FUJIFILM Holdings Corporation, and Mindray Medical International Limited, the market is characterized by strong competition among medical imaging manufacturers and emerging regional companies. These players compete through technological innovation, expansion of advanced ultrasound product portfolios, strategic partnerships, and continuous research and development activities aimed at improving imaging precision and clinical usability.

Key Industry Developments:

- In March 2026, Nanosonics Limited received a national group purchasing agreement with Premier Inc. for its trophon®3 automated high-level ultrasound probe disinfection system, enabling healthcare providers in Premier’s network to access advanced infection-control technology designed for safe reprocessing of ultrasound probes used in procedures such as transvaginal and transrectal imaging.

- In March 2025, Mindray Medical International Limited showcased its Resona A20 ultrasound system at the European Congress of Radiology (ECR) 2025, featuring the acoustic intelligence technology platform designed to enhance imaging performance, automation, and diagnostic confidence in ultrasound examinations used in clinical imaging applications.

- In November 2025, Canon Medical Systems Corporation received FDA 510(k) clearance for its Aplio i-series ultrasound systems (Aplio i900, Aplio i800, and Aplio i700) with Software Version 9.0, introducing advanced imaging technologies such as 3rd Harmonic Imaging, SMI Angio, and Auto Tune Shear Wave to improve image clarity, workflow efficiency, and diagnostic performance in ultrasound examinations.

Companies Covered in Endocavity Transducer Market

- ALPINION MEDICAL SYSTEMS Co., Ltd.

- Analogic Corporation

- BK Medical ApS

- Broadsound Corporation

- Butterfly Network Inc.

- Canon Medical Systems Corporation

- Carestream Health

- CIVCO Medical Solutions

- EDAN Instruments Inc.

- Esaote S.p.A.

- eZono AG

- FUJIFILM Holdings Corporation

- GE HealthCare Technologies Inc.

- Hitachi Ltd.

- Hologic Inc.

Frequently Asked Questions

The global endocavity transducer market is projected to reach US$4.2 billion in 2026.

Rising demand for minimally invasive diagnostic imaging in gynecology, obstetrics, and urology drives the endocavity transducer market.

The endocavity transducer market is expected to grow at a CAGR of 4.1% from 2026 to 2033.

Growing adoption of advanced ultrasound technologies, such as 3D/4D and Doppler imaging in diagnostic procedures, creates key opportunities in the endocavity transducer market.

ALPINION MEDICAL SYSTEMS Co. Ltd., Analogic Corporation, BK Medical ApS, and Broadsound Corporation are the leading players.