- Beverages

- Elderflower Drink Market

Elderflower Drink Market Size, Share, and Growth Forecast, 2026 - 2033

Elderflower Drink Market by Product Type (Alcoholic, Non-Alcoholic), Application (Food & Beverages, HoReCa, Household), Nature (Organic, Conventional), and Regional Analysis for 2026 - 2033

Elderflower Drink Market Share and Trends Analysis

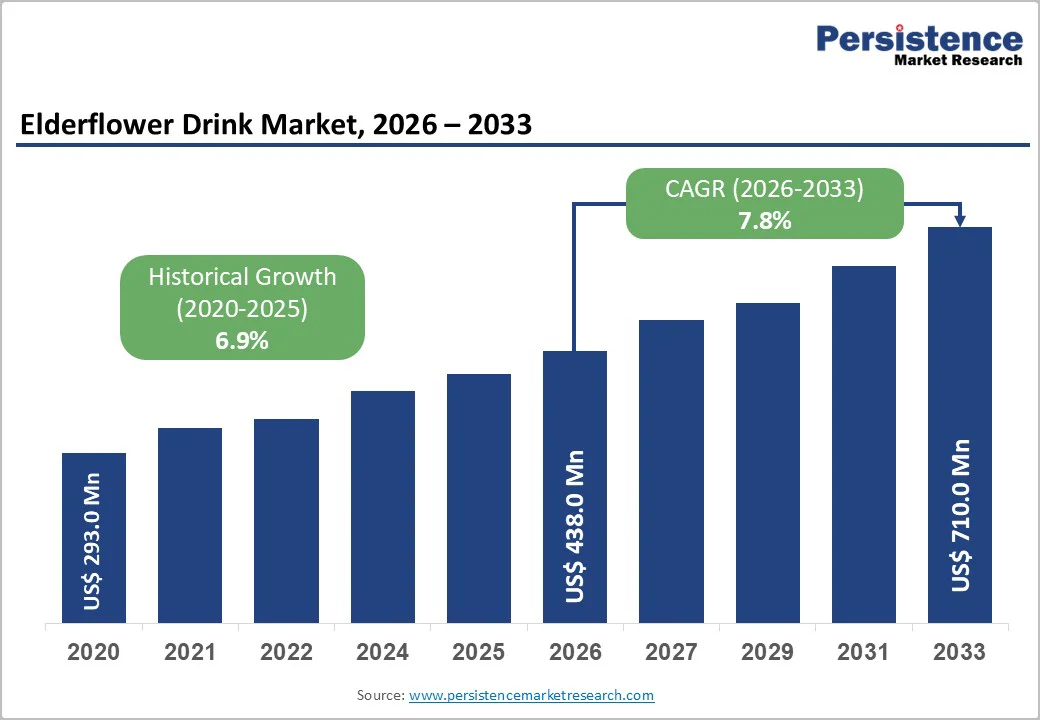

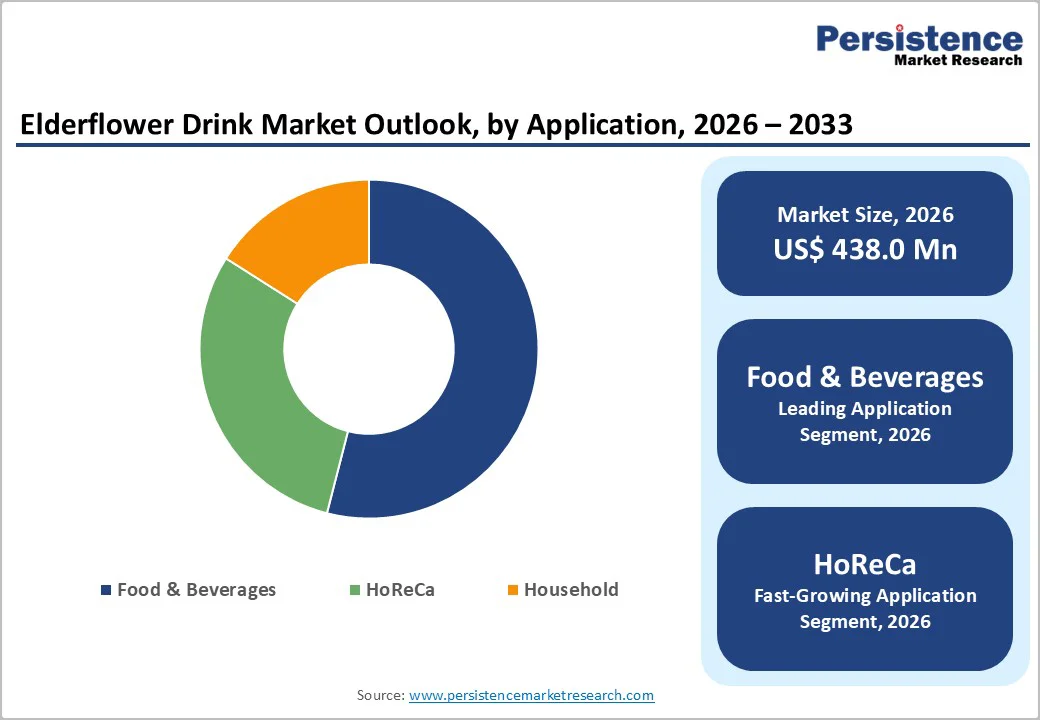

The global elderflower drink market size is likely to be valued at US$ 438.0 million in 2026, and is projected to reach US$ 710.0 million by 2033, growing at a CAGR of 7.8% during the forecast period 2026−2033. This strong expansion is driven by rising consumer preference for natural, botanical beverages, supported by growing health awareness and a shift toward premium, better-for-you drinks.

Elderflower drinks, made from Sambucus nigra blossoms, have evolved from traditional European cordials into modern functional beverages that appeal to younger consumers seeking authentic, clean-label flavor experiences. For brands, this signals an opportunity to innovate across formats such as sparkling drinks, cordials, syrups, and ready-to-drink options that align with wellness and indulgence trends. The market’s success hinges on balancing heritage with contemporary positioning, using storytelling around botanical purity, floral notes, and natural ingredients to stand out in crowded beverage aisles. Companies that invest in clear value propositions, premium packaging, and targeted marketing to millennials and Gen Z will be best placed to capture share in both mature and developing markets.

Key Industry Highlights

- Dominant Region: Europe is expected to command about 40% market share in 2026, owing to its long-standing cultural traditions around elderflower cordials and seasonal beverages.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing market through 2033, due to westernization of beverage preferences.

- Leading & Fastest-growing Product Types: Non-alcoholic is likely to be the leading segment with an approximate 72% revenue share in 2026, with the alcoholic segment growing the fastest during the 2026-2033 forecast period.

- Competitive Trends: The market exhibits moderate fragmentation, dominated by leading players such as Belvoir Fruit Farms, Bottlegreen Drinks Co., Teisseire, FRÏSA Beverages, and St-Germain.

- June 2025: Lincolnshire farm won a national award for its elderflower cordial, recognizing the quality of its handmade, small-batch product.

| Key Insights | Details |

|---|---|

|

Elderflower Drink Market Size (2026E) |

US$ 438.0 Mn |

|

Market Value Forecast (2033F) |

US$ 710.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

7.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Consumer Preference for Natural and Functional Beverages

The elderflower drink market growth is being pulled forward by the global shift toward natural ingredients and functional nutrition. Consumer interest in organic and natural beverages has risen sharply, with botanical drinks emerging as a particularly dynamic and visible subcategory. Elderflower-based products align closely with this movement, as they are perceived as authentic, plant-based alternatives to conventional soft drinks and artificially flavored beverages. This alignment with broader lifestyle and wellness trends enables brands to position elderflower drinks as part of a holistic approach to healthier, more mindful consumption rather than merely an indulgent refreshment.

Regulatory and scientific developments further enhance the appeal of elderflower beverages. Scientific assessments indicate that elderflower contains beneficial bioactive compounds, supporting its positioning as a functional ingredient with advantages that extend beyond basic hydration. The government dietary guidelines in several leading markets increasingly encourage lower intake of refined sugars and promote choices that favor natural, minimally processed ingredients. These evolving guidelines create a supportive policy and communication environment for elderflower drinks formulated as low-sugar, plant-based options. Together, these factors reinforce the strategic opportunity for manufacturers to develop, differentiate, and market elderflower beverages as both enjoyable and aligned with contemporary nutrition and wellness priorities.

Limited Consumer Awareness in Emerging Markets

Despite growing popularity in established markets, elderflower remains a relatively unfamiliar flavor profile in many regions, particularly outside Europe. In several parts of Asia Pacific, Latin America, and North America, consumers have limited exposure to elderflower in everyday cuisine or traditional beverages, which constrains initial interest and trial. This lack of cultural reference points makes it more difficult for brands to communicate the appeal of elderflower through simple product descriptions or packaging cues. As a result, early-stage market development often relies on in-store sampling, influencer collaborations, and carefully curated brand storytelling to introduce the flavor in a relatable way.

Consumer awareness requirements also translate into higher marketing expenditures and longer lead times before meaningful brand traction is achieved. Companies must invest in campaigns that not only explain the flavor profile but also position elderflower as relevant to local beverage occasions and preferences. At the same time, elderflower drinks face direct competition from other botanical beverages that already have stronger recognition, such as hibiscus, chamomile, and jasmine-based formulations. These alternatives often benefit from established associations with relaxation, wellness, or traditional remedies, making them easier for consumers to adopt. Consequently, elderflower brands tend to encounter longer conversion cycles and higher customer acquisition costs compared with more familiar botanical beverage categories.

Innovation in Functional and Hybrid Beverage Formats

The convergence of elderflower beverages with functional nutrition trends is unlocking substantial opportunities for product innovation. As consumers increasingly look for drinks that provide both sensory enjoyment and wellness benefits, interest in adaptogens, probiotics, and botanical ingredients continues to rise. Elderflower offers an appealing base for such formulations because of its premium, plant-based positioning and its association with a light, refreshing flavor profile. When combined thoughtfully with other functional ingredients, elderflower drinks can be positioned as part of a broader lifestyle focused on balance, vitality, and mindful consumption rather than simple indulgence.

Substantial scope also exists for innovation through hybrid product formats and sustainable packaging solutions. Elderflower can be incorporated into emerging beverage categories, including alcohol-adjacent offerings, modern soft drinks, and wellness-focused refreshers, allowing brands to stand out on increasingly crowded shelves. At the same time, the development of environmentally responsible formats such as recyclable containers, biodegradable materials, and concentrated refills supports alignment with circular economy principles and strengthens brand credibility among sustainability-focused consumers. Together, these innovation pathways create a foundation for elderflower beverages to move beyond niche positioning and become a core component of the evolving functional and premium beverage landscape.

Category-wise Analysis

Product Type Insights

Non-alcoholic is expected to be the leading segment in 2026, holding approximately 72% of the elderflower drink market revenue share. This leadership position reflects the segment’s broad consumer appeal, higher consumption frequency, and wide distribution across family-oriented retail channels and diverse demographic groups. Non-alcoholic elderflower products include cordials, syrups, sparkling waters, tonics, pressés, and ready-to-drink beverages that have successfully positioned themselves as premium alternatives to traditional soft drinks while still maintaining mass-market accessibility. The segment's dominance stems from several competitive advantages, including unrestricted retail distribution channels, appeal across all age demographics, and suitability for diverse consumption occasions from family gatherings to workplace refreshment.

The alcoholic segment is likely to register the highest CAGR during the 2026-2033 forecast period. This strong growth trajectory reflects the premiumization of alcoholic beverages, the continued expansion of the craft cocktail movement, and elderflower’s distinctive positioning as a sophisticated botanical ingredient in spirits, liqueurs, and wine-based drinks. Elderflower liqueurs, particularly St-Germain, have become reference brands in contemporary mixology, with several bar owners actively incorporating elderflower-based spirits into signature serves and modern interpretations of classic cocktails. For instance, 89 Charles, Boston's new Beacon Hill cocktail lounge, blends 1920s speakeasy aesthetics with modern mixology in its 12-seat bar and 30-seat space, featuring drinks such as the Melon Baller, a light and refreshing tequila drink with midori, lime, elderflower, togarashi and soda.

Application Insights

Food & beverages is slated to be dominant in 2026 with an approximate 48% of the revenue share. The segment dominates market utilization, covering both retail beverage products and business-to-business sales where manufacturers incorporate elderflower into a wide range of food and drink formulations. This segment includes consumer-packaged cordials, syrups, and concentrates for home preparation, as well as finished beverages across multiple subcategories. Its strength stems from elderflower’s versatility as a flavor enhancer and natural-style sweetening component in products such as sparkling waters, flavored teas, desserts, and confectionery. Manufacturers also favor elderflower for its clean-label positioning and suitability for more health-conscious, at-home consumption occasions.

HoReCa is anticipated to be the fastest-growing segment during the 2026-2033 forecast period. The rapid expansion as elderflower drinks gain prominence in professional foodservice environments, where elevated beverage programs support differentiation and premium pricing. Upscale restaurants, cocktail bars, and boutique hotels increasingly use elderflower as a signature menu element, leveraging its elegant flavor profile and versatility in both alcoholic and non-alcoholic formats. Growth is driven by the craft cocktail movement and the rise of sophisticated zero-proof options, with bartenders incorporating elderflower liqueurs, cordials, and syrups into cocktails and mocktails alike. Hotels and catering operators also feature elderflower-based welcome drinks and specialty refreshments that align with wellness-oriented positioning and premium guest experience expectations.

Nature Insights

Conventional form of elderflower extracts are slated lead with an estimated revenue share of 65% in 2026. This dominance reflects price accessibility, broader distribution networks, and established consumer acceptance across mass-market retail channels. Conventional products typically utilize commercially cultivated elderflowers with standard agricultural practices, enabling consistent supply, predictable quality, and competitive pricing strategies. The segment serves price-conscious consumers and maintains strong presence in mainstream supermarkets, hypermarkets, and convenience stores where value positioning drives purchase decisions. Conventional elderflower drinks have positively democratized access to this traditionally premium ingredient, introducing elderflower flavors to broader consumer demographics beyond specialty food enthusiasts.

The organic segment is expected to be the fastest-growing between 2026 and 2033. This exceptional growth trajectory aligns with global organic food and beverage market expansion driven by health consciousness, environmental sustainability concerns, and clean-label preferences. Organic certification provides quality assurance and environmental credentials that resonate strongly with premium consumer segments willing to pay price premiums for certified products. Growth drivers include increasing organic retail infrastructure, mainstream supermarket expansion of organic sections, and regulatory support for organic agriculture in multiple regions.

Regional Insights

Europe Elderflower Drink Market Trends

Europe is set to command a significant portion of the elderflower drink market share at roughly 40% in 2026. Europe is the core demand center for elderflower drinks, supported by long-standing cultural traditions around elderflower cordials and seasonal beverages, particularly in Central and Northern European countries. The United Kingdom, Germany, France, Spain, and Austria make up the largest national markets and collectively shape regional consumption patterns across both retail and foodservice channels. The U.K. exhibits a mature yet innovation-driven market profile, Germany is notable for strong organic and clean-label adoption, France and Spain are expanding rapidly through craft cocktail culture and premium hospitality, and Austria and neighboring countries maintain robust traditional usage.

Regional market growth is further reinforced by a supportive regulatory and competitive environment. Regulatory harmonization across the European Union (EU) simplifies cross-border trade, while organic certification and sustainability policies, including Green Deal and Farm to Fork initiatives, support local sourcing and environmentally responsible production. The market structure includes established brands such as Belvoir Fruit Farms, Bottlegreen, and Fever-Tree alongside a broad base of artisanal producers and expanding private-label ranges in major supermarkets, which increased price competition in mainstream segments. Investment activity increasingly focuses on sustainability, functional formulations, sugar reduction, and innovative flavor combinations that align with evolving consumer preferences and premium positioning.

North America Elderflower Drink Market Trends

North America is an important region for elderflower drinks, with the United States driving most of the demand and Canada and Mexico contributing smaller but steadily expanding shares. Regional growth is supported by rising consumer awareness of botanical beverages, strong premiumization trends, and the continued influence of the craft cocktail movement on beverage preferences. Major metropolitan areas such as New York, Los Angeles, San Francisco, Chicago, and Toronto show particularly strong adoption among younger, urban, health-conscious consumers who actively seek differentiated flavor profiles and elevated drinking experiences in both alcoholic and non-alcoholic formats.

Growth of the market in this region is further supported by increasing health consciousness and a shift toward functional, clean-label beverages as alternatives to conventional sugary sodas and artificial drinks. Elderflower benefits from favorable regulatory treatment, including safety recognition and alignment with transparency and clean-label expectations, as well as from sugar-reduction initiatives that support naturally lighter, botanically driven formulations. The competitive environment remains relatively fragmented, with international brands expanding from established European bases and domestic craft producers emphasizing artisanal production, sustainable sourcing, and distinctive flavor profiles. Investment activity focuses on functional innovation, brand building, and omnichannel distribution, with a strong emphasis on e-commerce and direct-to-consumer models that enable niche elderflower brands to reach dispersed but highly engaged consumer segments across the region.

Asia Pacific Elderflower Drink Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing elderflower drink market globally through 2033. Australia and Japan are currently leading consumption, and major urban centers in China and India are emerging as high-potential markets. The region’s positive outlook is driven by rising disposable incomes, rapid urbanization, the westernization of beverage preferences, and growing health consciousness among middle-class consumers. Megacities such as Tokyo, Seoul, Shanghai, Beijing, Mumbai, and Sydney show particularly strong momentum as cosmopolitan consumers seek premium, natural beverage alternatives that align with global lifestyle trends.

Key growth determinants for the Asia Pacific market include expanding middle-class populations in China and India that are increasingly willing to experiment with premium imported beverages, alongside a broader premiumization trend across regional beverage markets that supports elderflower’s positioning as a sophisticated, European-inspired product. Health and wellness trends, particularly strong in Japan and South Korea, align with elderflower’s natural and functional image, while exposure to Western food and beverage culture through international hotel chains, restaurants, and expatriate communities helps build awareness and encourage initial trial. Although regulatory frameworks vary widely and require careful navigation of food safety, import, and labeling rules, modernization efforts and the expansion of organized retail create more favorable conditions for premium product distribution.

Competitive Landscape

The global elderflower drink market landscape exhibits moderate fragmentation, dominated by leading players such as Belvoir Fruit Farms, Bottlegreen Drinks Co., Teisseire, FRÏSA Beverages and St-Germain. These players collectively capture 45-50% of the market share. The competitive landscape is increasingly innovation-driven, as players experiment with novel formulations, distinctive packaging, and evolving marketing approaches to stand out. Established brands are capitalizing on their longstanding heritage and deep expertise in elderflower beverages, while newer entrants differentiate through sustainability-led positioning, organic certifications, and small-batch, artisanal production. At the same time, rivalry is intensifying in digital channels, with companies ramping up investment in online marketing and e-commerce capabilities to expand their reach and engage a broader consumer base.

Key Industry Developments

- In December 2025, Penrhos Spirits, a Herefordshire family fruit-farm distiller known for its craft gins made with “wonky” fruit, including a Rhubarb, Apple & Elderflower variant, partnered with Fortitude Drinks UK to scale its presence across premium retail, hospitality, and on-trade channels nationwide.

- In June 2025, SWISS launched its first signature cocktail, 'SWISS Alpine Essence', a light floral White Negroni variant with dry white vermouth, elderflower syrup, crème de menthe, white crème de cacao, and citrus-herbal notes, developed with bartender Sarah Madritsch.

- In March 2025, Starbucks Reserve introduced a new spring menu that highlights botanical flavors, featuring beverages infused with ingredients such as elderflower, lavender, and other floral notes to offer a refined, seasonal experience.

Companies Covered in Elderflower Drink Market

- Fever-Tree Holdings plc

- Sicilia Bevande

- Bottlegreen Drinks Ltd.

- East Imperial

- Q Drinks

- Remedy Drinks

- Belvoir Fruit Farms

- Lakeland Cordials

- Roses Cordials

- Cottontail Beverages

- Boteco Botanical Beverages

- Heritage Botanical Company

- Pacific Edge Organic

- Noble Endeavors

- Elderflora Naturals

Frequently Asked Questions

The global elderflower drink market is projected to reach US$ 438.0 million in 2026.

Rising demand for natural, botanical, and premium beverages aligned with health, wellness, and low-/no-alcohol consumption trends are driving the market.

The market is poised to witness a CAGR of 7.8% from 2026 to 2033.

Key market opportunities include functional and hybrid product innovation and growth of e-commerce and premium HoReCa channels for elderflower-based beverages.

Belvoir Fruit Farms, Bottlegreen Drinks Co., Teisseire, FRÏSA Beverages and St-Germain are some of the key players in the market.