- Healthcare Services

- Elastography Imaging Market

Elastography Imaging Market Size, Share, and Growth Forecast, 2025 - 2032

Elastography Imaging Market Modality (Ultrasound, Magnetic Resonance), Application (General Imaging, Hepatology, Breast, Cardiology, Nephrology), End-user (Hospitals, Imaging Centers), and Regional Analysis for 2025 - 2032

Elastography Imaging Market Size and Trends Analysis

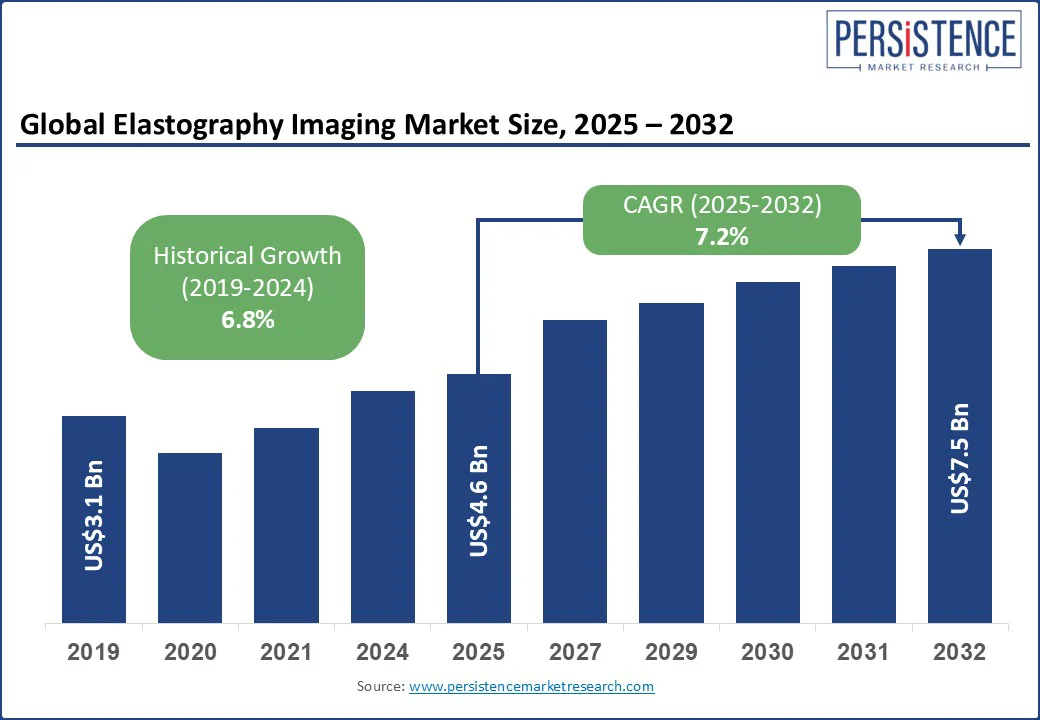

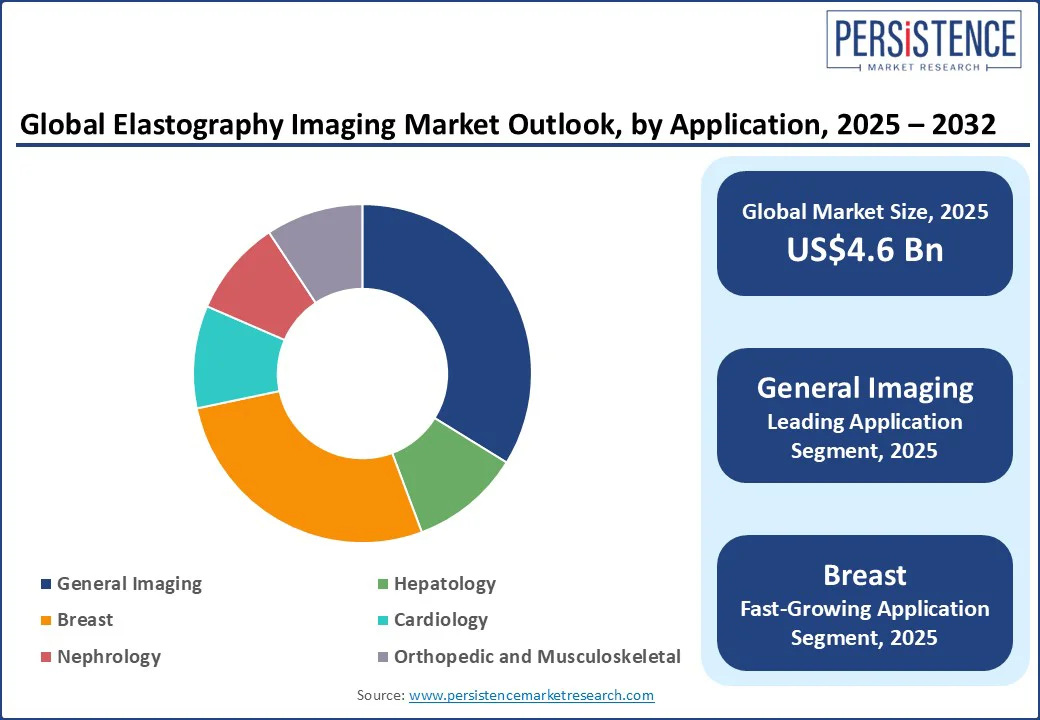

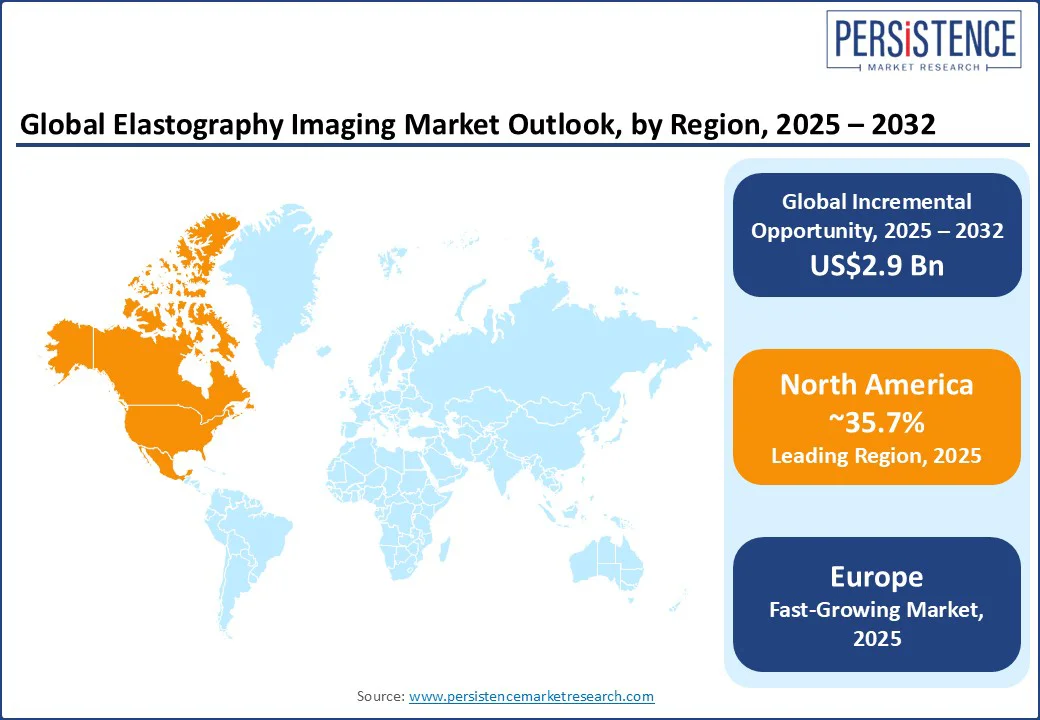

The global elastography imaging market size is likely to increase from US$4.6 Bn in 2025 to US$7.5 Bn by 2032. It is anticipated to witness a CAGR of 7.2% during the forecast period from 2025 to 2032.

The growth of the elastography imaging industry is driven by high demand for a non-invasive and affordable alternative to tissue biopsies among clinicians for assessing organ stiffness and disease progression. The technology has gained traction in mainstream healthcare, specifically in the evaluation of chronic liver disease, breast cancer, and musculoskeletal medicine disorders.

Key Industry Highlights:

- Leading Region: North America, with around 35.7% share in 2025, augmented by favorable reimbursement policies and surging adoption of advanced imaging technologies.

- Fastest-growing Region: Europe is expected to witness the fastest growth, due to expanding cancer screening programs and supportive government initiatives for early disease detection.

- Research Study: A 2025 study published in the Egyptian Journal of Radiology and Nuclear Medicine evaluated the clinical utility of shear-wave elastography in monitoring liver iron overload in children diagnosed with β-thalassemia major. It was found that non-invasive ultrasound elastography is expected to help clinicians track liver iron levels and guide chelation therapy when MRI is not readily available.

- Dominant Modality: Ultrasound is projected to account for 70.1% of the market share in 2025, fueled by its portability, low cost, and ability to deliver real-time results.

- Leading Application: General imaging is anticipated to register nearly 33.8% of the market share in 2025, owing to broad usage of liver, thyroid, and musculoskeletal assessments.

|

Global Market Attribute |

Key Insights |

|

Elastography Imaging Market Size (2025E) |

US$4.6 Bn |

|

Market Value Forecast (2032F) |

US$7.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Dynamics

Driver - Rising Burden of Chronic Liver Disease and Breast Cancer Spurs Demand

The rising prevalence of chronic liver disease is the most important factor boosting demand for elastography imaging. Clinicians today mainly favor non-invasive methods over traditional biopsies. Conditions such as hepatitis B, hepatitis C, and Non-Alcoholic Fatty Liver Disease (NAFLD) are rising sharply, creating a high demand for tools that can stage fibrosis accurately without repeated invasive sampling. Hospitals in Germany and France are now using elastography as a part of routine monitoring, lowering biopsy rates by nearly 40%.

The increasing prevalence of breast cancer is further driving market growth. According to the World Health Organization (WHO), in 2022 alone, breast cancer caused an estimated 670,000 deaths worldwide. Hence, clinicians require tools that can differentiate benign from malignant lesions efficiently. Elastography’s ability to provide stiffness mapping makes it valuable in dense breast tissue, where mammography is less effective.

Restraint - Technical Challenges in Obese Patients Limit Reliability

One of the key hindrances to the adoption of elastography imaging is the technical difficulty it faces in patients with large body habitus or atypical anatomy. Excess adipose tissue can weaken ultrasound signals and reduce penetration depth, making it difficult to generate reliable stiffness maps in obese patients. Accurate fibrosis measurement in liver elastography requires clear signal transmission, making this a significant challenge.

A 2023 multicenter study published in Hepatology Communications highlighted that liver stiffness measurements failed in nearly 15% of obese patients, often requiring repeat examinations or a fallback on biopsy. Technical challenges also extend to breast elastography, where dense tissue or large breast size can cause uneven stress distribution during compression-based techniques. Manufacturers are responding with new probes and AI-based correction algorithms, but adoption has been uneven.

Opportunity - Multi-modality Platforms Strengthen Oncology Diagnostics

The emergence of multi-modality elastography is opening new avenues by overcoming the limitations of single-technique approaches. Traditional shear-wave or strain elastography alone often struggles with image quality variations, primarily in patients with obesity or high breast density. By combining ultrasound elastography with Magnetic Resonance Elastography (MRE), clinicians can cross-validate stiffness measurements. This can lead to more reliable diagnostic outcomes.

Multi-modality elastography is also gaining momentum in oncology, where differentiating benign from malignant lesions remains challenging. Ultrasound elastography provides quick bedside imaging, while MRE provides whole-organ coverage with high reproducibility. Another opportunity is the surging trend of personalized medicine. By capturing complementary stiffness data across multiple modalities, physicians can track disease progression more dynamically.

Category-wise Analysis

Modality Insights

In terms of modality, the market is bifurcated into ultrasound and magnetic resonance. Among these, the ultrasound segment is predicted to account for nearly 70.1% of the elastography imaging market share in 2025, due to its ability to provide a balance of accessibility, cost, and adaptability across clinical settings. Ultrasound-based elastography can be added as a software upgrade to machines commonly used in hospitals and clinics. This plug-in model drastically reduces capital investment and fuels adoption.

Magnetic Resonance Elastography (MRE) is gaining impetus as it delivers higher reproducibility and whole-organ coverage compared with ultrasound-based methods. It provides consistent stiffness measurements across the entire liver, unlike shear-wave elastography, which is usually limited by obesity, ascites, or operator skill. This reliability is particularly important in MASLD and MASH clinical trials, where regulators and sponsors require standardized and repeatable endpoints.

Application Insights

By application, the segmentation comprises general imaging, hepatology, breast, cardiology, nephrology, orthopedics, and musculoskeletal. Out of these, the general imaging segment is poised to hold around 33.8% of the market share in 2025, as elastography allows hospitals to utilize the technology across multiple organ systems rather than restricting it to niche use.

Ultrasound systems with built-in elastography can be used for breast, thyroid, prostate, and musculoskeletal exams alongside standard abdominal scans. This multipurpose feature makes it convenient for radiology departments to justify the investment.

Breast imaging has emerged as a key application area due to the rising emphasis on early cancer detection in young populations. In Europe and the Asia Pacific, where mammography screening is less effective in dense breast tissue, elastography is being positioned as a complementary tool.

For example, hospitals in Japan and India reported integrating elastography into screening protocols for women under 40, where standard mammograms often miss tumors. This adaptation is important as breast cancer incidence in young women has been steadily increasing in the Asia Pacific, making elastography a practical solution.

Regional Insights

North America Elastography Imaging Market Trends - Medicare Coverage and Valuation Scrutiny Secure Stable Reimbursement Environment

In 2025, North America is expected to account for approximately 35.7% of the market share as the region is in an expansion phase, with growth secured in liver disease pathways and fast-tracked by clear coding. In the U.S. elastography imaging market, distinct Current Procedural Terminology (CPT) codes separate shear-wave liver tests from general ultrasound elastography. The Centers for Medicare & Medicaid Services (CMS) kept this code family under active review in the CY-2025 Physician Fee Schedule, signaling stable national coverage with valuation scrutiny rather than retreat.

MR elastography is billed under CPT code 76391 and is listed on Medicare’s procedure lookup, which has enabled large systems to fold MRE into fatty-liver clinics alongside ultrasound-based options. These coding frameworks have positioned elastography as a front-line diagnostic tool in hepatology, radiology, and GI services. Clinical adoption is also broadening beyond viral hepatitis into MASLD/MASH and alcohol-related disease. In this field, societies now position shear-wave methods as core tools.

Europe Elastography Imaging Market Trends - France Positions Transient Elastography as Standard in Chronic Liver Disease Monitoring

In Europe, elastography imaging is gaining clinical traction but adoption patterns are influenced by national health systems, reimbursement frameworks, and guideline endorsements. The region operates through country-specific approvals, which lead to varied levels of integration. France, for instance, has seen increased use of transient elastography, with FibroScan devices often positioned as a standard tool for chronic liver disease monitoring.

Germany and the U.K. have, however, leaned on shear-wave elastography integrated into multipurpose ultrasound systems. This is owing to the cost efficiency of equipping existing hospital fleets instead of relying on standalone devices. Recent regulatory developments are further accelerating adoption. The European Association for the Study of the Liver (EASL) issued updated guidance in 2024 recommending elastography as a front-line test for assessing fibrosis in MASLD and MASH patients. This has propelled hospitals across Spain and Italy to expand ultrasound-based elastography programs in hepatology departments.

Asia Pacific Elastography Imaging Market Trends - China Leads with Domestic Platforms Boosting Price Compression

Asia Pacific represents a high-growth market, augmented by rising MASLD/NASH cases, persistent viral hepatitis in some areas, and expanding device availability. China is currently at the forefront of growth as clinical requirements from HBV and metabolic liver disease have pushed the adoption of both transient and shear-wave systems.

Domestic platforms such as the FT9000 have been compared head-to-head with FibroScan in real-world cohorts. These have exhibited uniformity on key metrics and compelled price compression, broadening access beyond Tier-1 hospitals.

In Japan, tertiary centers are widely adopting ultrasound and MR elastography for research and complex care. Hospitals are also investing in MRI software upgrades and reproducibility workflows. Per-capita spend on elastography in Japan is far above regional averages, as certain zones support drug trials and high-resolution stiffness mapping.

Leading liver clinics and private hospitals across India have integrated transient and shear-wave elastography into routine practice. Even though private-pay dynamics and uneven distribution result in lagged rural access, guideline updates are improving mainstream adoption in metro cities.

Competitive Landscape

The global elastography imaging market is characterized by various established imaging giants and emerging players, each striving to differentiate their offerings in the market. Leading companies dominate the high-end hospital segment, where elastography is integrated into premium ultrasound and MRI systems.

Their edge comes from pairing hardware with AI-backed software that improves workflow. Small-scale but specialized firms maintain competitiveness by focusing on single-disease applications, specifically liver health. Various players are also focusing on mergers, acquisitions, and partnerships to compete with their rivals. The handheld and portable ultrasound space is an emerging area.

Key Industry Developments

- In August 2025, Sonic Incytes Medical Corp declared that the U.S. FDA granted 510(k) clearance for Velacur ONE, its point-of-care ultrasound elastography device. The device provides an improved interface as well as features for refined portability and user experience.

- In April 2025, Royal Philips introduced the Elevate Platform upgrade for its EPIQ Elite ultrasound system. The platform utilizes proactive system monitoring so that care teams can consult remotely, support diagnosis from a distance, and troubleshoot systems without on-site intervention.

Companies Covered in Elastography Imaging Market

- Canon Medical Systems Corporation

- FUJIFILM Corporation

- Esaote SpA

- Mindray Bio-Medical Electronics Co., Ltd. Koninklijke Philips N.V.

- Hitachi, Ltd.

- GE Healthcare

- Toshiba America Medical Systems, Inc.

- Siemens AG

- Samsung Medison Co., Ltd.

Frequently Asked Questions

The elastography imaging market is projected to reach US$ 4.6 Bn in 2025.

The rising prevalence of breast cancer and the increasing shift toward non-invasive diagnostics are the key market drivers.

The elastography imaging market is poised to witness a CAGR of 7.2% from 2025 to 2032.

Surging demand for point-of-care ultrasound systems and rising investments in oncology-focused imaging research are the key market opportunities.

Canon Medical Systems Corporation, FUJIFILM Corporation, and Esaote SpA are a few key market players.