- Home Care & Utilities

- Cloth Drying Racks Market

Cloth Drying Racks Market Size, Share, and Growth Forecast 2026 - 2033

Cloth Drying Racks Market by Material Type (Bamboo/ Wood, Fabric, Metal, Plastic, Other), Applications (Residential, Commercial), Mounting Type (Freestanding, Ceiling-mounted, Wall-mounted), Distribution Channel (Online, Hypermarkets & Supermarkets, Specialty Home Stores, Department Stores, Other), and Regional Analysis for 2026 - 2033

Cloth Drying Racks Market Size and Trend Analysis

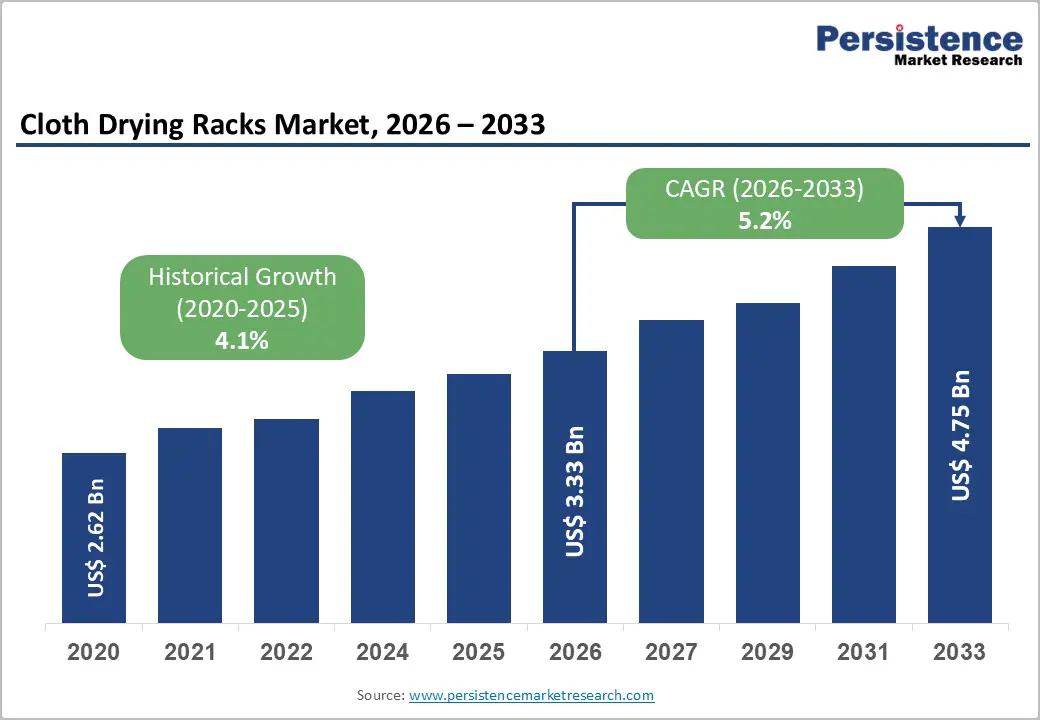

The global cloth drying racks market size is supposed to be valued at US$ 3.33 billion in 2026 and is projected to reach US$ 4.75 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. Rising demand for cloth drying racks is driven by rapid urbanization and increasing household space constraints, which encourage the adoption of compact and efficient drying solutions.

United Nations data indicates that 56% of the global population lived in urban areas in 2024, intensifying pressure on limited indoor spaces. Energy efficiency regulations, including the EU’s Ecodesign Directive, further promote low-energy alternatives to electric dryers. Consumer preference is also shifting toward sustainable and cost-effective laundry practices, supported by findings that dryers account for approximately 15% of household energy use in the United States. As urbanization is projected to reach 68% globally by 2050, particularly across densely populated regions in the Asia Pacific, Europe, and North America, awareness of energy conservation continues to accelerate demand for environmentally friendly air-drying solutions.

Key Industry Highlights:

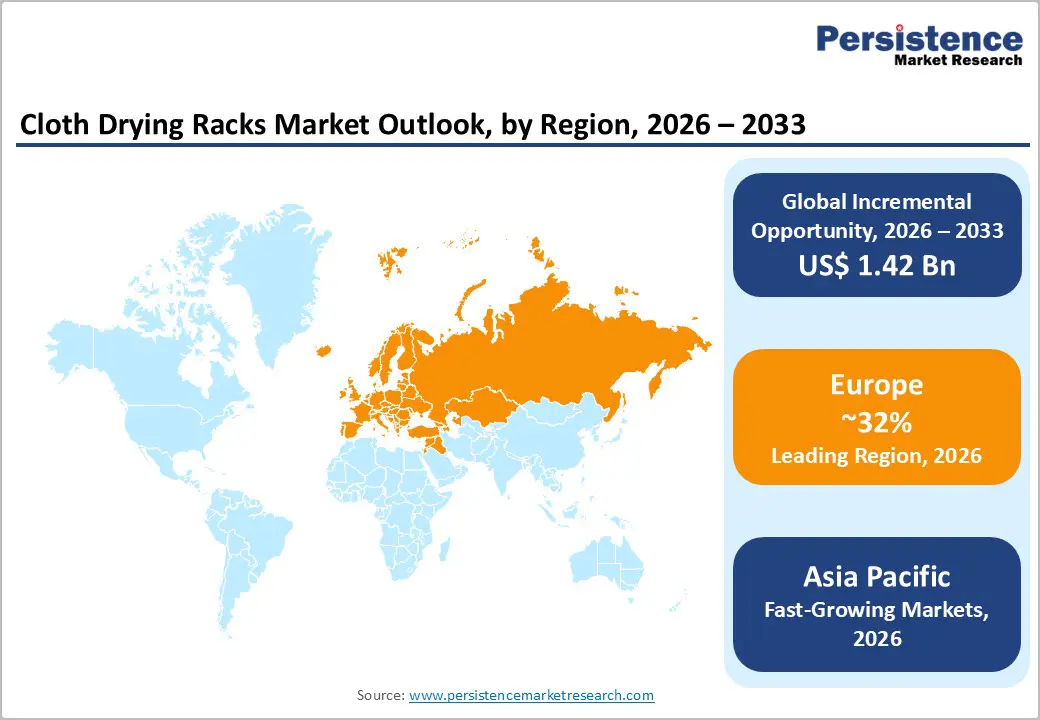

- Regional Leader: Europe maintains market leadership with 32% share, combining cultural air-drying traditions, stringent energy efficiency directives under European Union frameworks, and premium product innovation.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing regional market, driven by explosive urbanization projected to reach 70% in China by 2030 and 50% in India by 2051, rapidly expanding middle-class populations with rising disposable incomes, and manufacturing cost advantages.

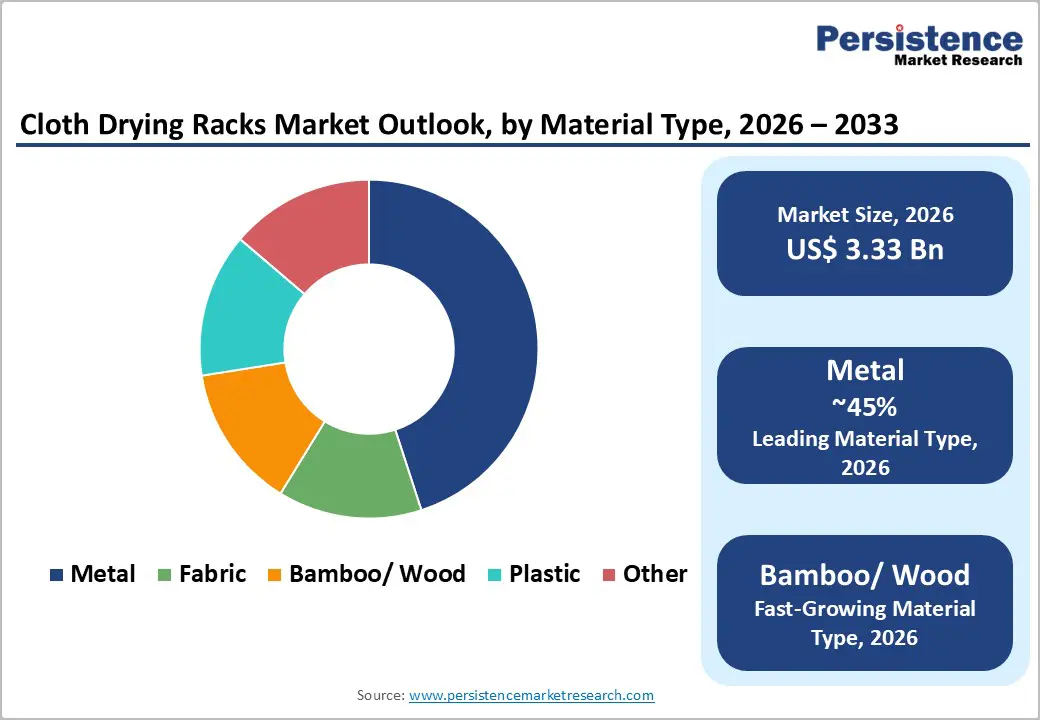

- Leading Material Segment: Metal type dominates with approximately 45% market share, driven by superior durability enabling higher weight-bearing capacities, structural strength essential for supporting wet textiles and heavy garments, competitive pricing through manufacturing economies of scale, and aesthetic versatility with finishes ranging from industrial steel to polished aluminum, suitable for diverse interior design preferences.

- Fastest Growing Mounting Type: Wall-mounted drying racks represent the fastest-growing mounting segment, propelled by accelerating urbanization, creating acute space constraints in metropolitan apartments and condominiums, necessitating permanent vertical space solutions with fold-down retractable designs preserving floor area.

- Key Opportunity: Smart and IoT-enabled drying rack integration presents a transformative market opportunity as manufacturers incorporate automated rain-sensing retraction systems, integrated heating elements with mobile app temperature controls, voice command compatibility with platforms like Amazon Alexa and Google Assistant, and antimicrobial coatings meeting contemporary consumer expectations for convenience, hygiene standards, and smart home ecosystem integration.

| Key Insights | Details |

|---|---|

| Cloth Drying Racks Size (2026E) | US$ 3.33 Bn |

| Market Value Forecast (2033F) | US$ 4.75 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Urbanization and Space Optimization Needs

The rapid pace of global urbanization is significantly transforming residential infrastructure and housing patterns, driving strong demand for space-efficient household solutions, such as cloth-drying racks. According to the United Nations World Urbanization Prospects 2025, urban areas are expected to accommodate 68% of the global population by 2050. In India, urbanization, currently estimated at 31% to 33%, is projected to reach 50% by 2051, supported by substantial migration flows. This demographic shift has intensified housing shortages and spatial constraints, with over 85% of urban dwellings comprising single rooms or similarly constrained layouts. The India Economic Survey 2026 highlights 526 emerging urban settlements, reflecting expansion that surpasses infrastructure development. Rising property prices are further compelling developers to reduce unit sizes, thereby increasing the need for wall-mounted and foldable drying solutions that optimize limited living spaces.

Environmental Consciousness and Energy Efficiency Preferences

Escalating energy prices and rising environmental awareness are accelerating the shift toward cloth drying racks as low-cost, zero-energy alternatives to electric dryers. The International Energy Agency reports a 12% increase in global household electricity prices between 2023 and 2024, raising dryer operating costs to US$0.10-0.20/kWh. Air-drying reduces energy consumption by approximately 75%, according to the U.S. Department of Energy.

Increasing consumer preference for sustainable products, reflected in surveys showing that 78% favor eco-friendly options and 40% plan to adopt greener laundry practices, is further boosting adoption. Additionally, 80% of consumers express concern about the environmental impact of their purchases, underscoring a broad shift toward sustainable household behavior. Supported by stringent energy-efficiency regulations, particularly in North America and Europe, cloth drying racks offer both cost savings and reduced environmental impact.

Restraints - Competition from Electric Dryers and Alternative Drying Methods

The widespread availability and convenience of electric clothes dryers create substantial competitive pressure on the clothes drying racks market, particularly in developed economies with high penetration of automated laundry appliances. Electric dryers provide significant time savings and weather-independent drying, offering strong value for households with high laundry volumes or limited indoor space. With an average lifespan of about 13 years, these appliances represent durable, long-term investments that reduce repeat purchases of drying racks.

Improved heat-pump technologies have also enhanced dryer energy efficiency, partly addressing prior environmental concerns. In humid or low-sunlight regions, electric dryers outperform passive drying methods, further limiting the adoption of racks. Seasonal conditions exacerbate this trend; prolonged cold winters in the U.S. Northeast and frequent rainy days in Northern Europe significantly slow air-drying, reducing drying rack usage across major temperate markets.

Fluctuating Raw Material Prices and Manufacturing Cost Pressures

Volatility in raw material prices, particularly for steel, aluminum, bamboo, and plastic resins, continues to create cost uncertainty and margin pressure for cloth drying rack manufacturers. Metal racks, which form a major market segment due to their durability and affordability, remain vulnerable to commodity price fluctuations driven by supply chain disruptions, mining output variability, and global trade policy shifts. Bamboo and wood-based products also face supply challenges linked to sustainable forestry practices, harvest cycles, and transportation constraints, further contributing to pricing instability.

Plastic components derived from petroleum-based feedstocks are subject to volatility aligned with crude oil markets, while tightening environmental regulations require costly material reformulation. Collectively, these pressures restrict manufacturers’ ability to maintain competitive pricing without compromising quality or innovation, particularly in price-sensitive markets and emerging economies.

Opportunity - Smart and IoT-Enabled Drying Rack Innovation

The integration of smart home technology and IoT capabilities into cloth drying racks presents a substantial opportunity for product differentiation and premium market growth. Modern smart racks now feature rain-sensing automatic retraction, integrated heating with temperature control, and mobile app connectivity for remote operation. As smart home ecosystems expand, consumers increasingly prefer connected, energy-efficient appliances that enhance convenience and energy management.

Manufacturers are therefore investing in advanced features such as retractable arms, multi-tier configurations, automated folding mechanisms, and compatibility with voice assistants like Amazon Alexa and Google Assistant. Additionally, the use of corrosion-resistant materials, antibacterial coatings, and lightweight yet durable alloys such as aluminum and stainless steel improves product longevity and user experience, enabling premium pricing while meeting evolving expectations for convenience, hygiene, and contemporary interior integration.

Commercial and Hospitality Sector Expansion

The commercial laundry and hospitality sectors offer strong growth opportunities as organizations seek to improve operational efficiency and reduce energy use in large-scale laundry processes. Growth in coin-operated and self-service laundries is driven by rising urbanization, higher population density, and limited in-unit laundry facilities in rental housing. Hotels, hostels, serviced apartments, and resorts are increasingly installing wall-mounted and freestanding drying racks to enhance guest convenience while lowering reliance on energy-intensive commercial dryers.

Laundromats, fitness centers, hospitals, and healthcare facilities are also adopting these solutions to streamline operations and support sustainability goals. Customization options, such as branding, tailored configurations, and antimicrobial coatings, enable alignment with specific hygiene and operational needs. This focus on efficiency and environmental responsibility is driving demand for durable, high-capacity, commercial-grade drying racks suited for intensive institutional use.

Category-wise Analysis

Material Type Insights

Metal drying racks hold roughly 45% of the material-type market due to their durability, structural strength, and competitive pricing, making them suitable for both residential and commercial use. Steel and aluminum are the primary substrates, with stainless steel offering strong rust resistance for humid or outdoor conditions. Their sturdy construction supports heavier textiles, while economies of scale help maintain affordability compared with premium bamboo options.

Metal racks also offer aesthetic flexibility through powder-coated, chrome, and matte-black finishes, enabling compatibility with diverse interior styles. Aluminum variants provide lightweight portability and corrosion resistance, enhancing longevity. Their full recyclability further aligns with growing sustainability preferences. Although metal dominates, bamboo and wood alternatives are gaining momentum as consumers increasingly prefer eco-friendly materials and natural aesthetics.

Application Insights

The residential application segment accounts for about 68% of market share, driven by consistent household demand for daily drying solutions across bathrooms, laundry rooms, closets, and indoor living areas. Laundry rooms and indoor drying spaces make up the largest sub-segment, as dedicated laundry areas increasingly feature in modern housing developments and apartment renovations. Bathroom-mounted racks offer convenient access for towel and delicate-garment drying, while closet-mounted options maximize vertical space and support garment organization.

The residential segment benefits from universal household penetration, as drying racks are essential rather than discretionary items. However, the commercial segment is expanding more rapidly, supported by the laundromat industry’s 6%-10% CAGR from 2025 to 2030, along with rising adoption by hotels, resorts, hospitals, clinics, and modern office environments that require durable, hygienic, and space-efficient drying solutions.

Mounting Type Insights

Freestanding drying racks hold about 52% of the mounting-type market, driven by strong consumer preference for portable, non-permanent solutions that require no installation or wall modifications. Their flexibility allows users to reposition them to optimize sunlight exposure, airflow, or temporary household space needs, making them especially suitable for renters, military families, and other mobile populations.

Brabantia’s HangOn Tower Drying Rack, introduced in September 2025, illustrates innovation in this segment with 23- and 30-meter configurations that occupy minimal floor space (79 × 59 cm) while accommodating multiple laundry loads. However, wall-mounted racks represent the fastest-growing segment, expected to rise at a 7.1% CAGR. Their fold-down, retractable designs maximize vertical space and integrate multi-tier structures and automated mechanisms ideal for compact urban living spaces.

Distribution Channel Insights

Online distribution channels hold about 38% of the market and are the fastest-growing category, supported by expanding e-commerce platforms, transparent pricing, broad product variety, and doorstep delivery convenience, which particularly appeal to urban consumers with limited time and transportation options. Digital marketplaces such as Amazon, Alibaba, Walmart.com, and specialized home goods retailers enable informed purchasing through product comparisons, customer reviews, and detailed specifications.

The online channel also offers access to international brands and niche variants unavailable in traditional stores, while bulk-priced options attract B2B buyers, including property developers, hospitality operators, and laundromat franchises. Hypermarkets and supermarkets maintain a 28% share through high foot traffic and immediate availability, complemented by specialty stores and department stores offering curated and mid-tier assortments.

Regional Insights

North America Cloth Drying Racks Market Trends

North America represents a mature market characterized by steady demand driven by environmental consciousness, energy-cost sensitivity, and premium product adoption among affluent consumers. The United States leads regional consumption, supported by approximately 144 million housing units across diverse climates that favor indoor drying during winter and humid summer months. Consumer trends show that 65% prefer fragrance-free laundry products, while 40% plan to transition to eco-friendly alternatives, reinforcing a shift toward sustainable air-drying practices.

Typical replacement cycles for washing machines and dryers, averaging 10 to 13 years, align with laundry-room renovation projects that increasingly integrate modern drying racks. In Canada, strong e-commerce growth and energy-efficiency regulations are driving increased adoption. North American brands further strengthen market momentum through smart-home integration, premium materials, and extended warranties, appealing to consumers seeking durability and aesthetic appeal.

Europe Cloth Drying Racks Market Trends

Europe demonstrates strong market fundamentals, supported by cultural preferences for air-drying, stringent energy-efficiency regulations, and advanced sustainability awareness across Northern and Western regions. Germany represents the largest market, driven by 42 million households and policy frameworks such as the EU Energy Efficiency Directive that encourage reduced electricity use through behavioral and appliance-level changes. The United Kingdom shows high adoption due to shrinking urban living spaces, particularly in London, while France and Spain benefit from Mediterranean climates that enable outdoor drying during warm seasons and require indoor options in winter.

European manufacturers lead premium product innovation, exemplified by Brabantia’s Refresh and Steam Collection (2024) and HangOn Tower Drying Rack (2025), both of which incorporate recycled materials and Cradle to Cradle Certified components. Affluent regions such as Scandinavia, the Netherlands, and Switzerland further drive premium demand.

Asia Pacific Cloth Drying Racks Market Trends

Asia Pacific is the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and manufacturing cost advantages that support competitive pricing and widespread market penetration. China dominates regional production and consumption, with major manufacturing clusters in Guangdong, Zhejiang, and Jiangsu offering integrated supply chains spanning raw materials to finished goods assembly. As China’s urbanization advances toward 70% by 2030, demand for space-efficient household solutions continues to rise.

India follows a similar trajectory, with urbanization expected to reach 50% by 2051, bringing nearly 600 million urban residents into the fold, requiring affordable household infrastructure. Japan’s market is shaped by limited residential space and an aging population that favors lightweight, easy-to-operate drying solutions. Southeast Asian countries, including Indonesia, Thailand, Vietnam, and the Philippines, benefit from rising incomes, growing homeownership, and tropical climates that necessitate indoor drying during monsoon seasons.

Competitive Landscape

The cloth drying racks market is highly fragmented, with numerous regional manufacturers, private-label suppliers, and established home goods brands competing across varied price tiers and distribution channels. Market concentration remains low, fostering competition based on product differentiation, pricing strategies, and channel partnerships. Leading companies focus on expanding into emerging markets, diversifying product portfolios across mounting types and materials, and strengthening alliances with retail chains and e-commerce platforms to enhance accessibility. R&D priorities include smart-home integration, sustainable material sourcing such as recycled metals and certified bamboo, and ergonomic design improvements. Emerging business models feature direct-to-consumer e-commerce, subscription services for commercial laundry operators, and customizable solutions for hospitality clients.

Key Developments:

- Aug 2025: Brabantia launched the HangOn Tower Drying Rack featuring 23-meter and 30-meter configurations constructed with 38% recycled material, achieving 96% recyclability and Cradle-to-Cradle Certification at Silver level while occupying minimal floor space of only 79 x 59 cm to accommodate two to three machine loads of laundry.

- February 2024: Brabantia introduced the Refresh and Steam Collection at The Inspired Home Show, offering flexible steaming solutions with suggested retail prices ranging from US$ 16.50 to US$ 98, featuring designs matching the iconic Linn Clothing Rack and incorporating Cradle-to-Cradle Certified steel components with 2 to 5-year guarantees.

Top Companies in Cloth Drying Racks Market

- Brabantia (Netherlands) is a market leader in premium cloth-drying rack solutions, distinguished by exceptional design aesthetics, sustainable manufacturing practices, and comprehensive product guarantees. The company's commitment to environmental sustainability manifests through Cradle to Grave Certification, substantial recycled material content reaching 38% in recent product lines, and strategic partnerships with WeForest, resulting in over 3 million trees planted. Brabantia's product portfolio spans freestanding tower racks, wall-mounted systems, and specialty garment care solutions with pricing positioning in the mid-to-premium segment, supported by extensive European distribution networks and expanding global presence through online retail channels.

- Leifheit AG (Germany) maintains a strong market presence across European markets, leveraging German engineering heritage, product reliability, and extensive retail partnerships with hypermarkets, supermarkets, and specialty home stores. The company's drying rack portfolio emphasizes functional innovation, including quick-fold mechanisms, height-adjustable configurations, and corrosion-resistant finishes suitable for both indoor and outdoor applications. Leifheit targets value-conscious consumers seeking a balance between quality construction and competitive pricing, supported by efficient manufacturing operations and established supply chain infrastructure enabling consistent product availability across diverse retail formats.

- Honey-Can-Do International LLC (United States) represents a significant North American player specializing in home organization and storage solutions including comprehensive cloth drying rack offerings spanning freestanding, wall-mounted, and accordion-style configurations. The company's competitive advantage derives from extensive distribution reach through major retail partnerships including Walmart, Target, Amazon, and regional home goods chains, combined with competitive pricing strategies targeting budget-conscious consumers.

Companies Covered in Cloth Drying Racks Market

- Leifheit AG

- Honey-Can Do International LLC

- Whitmor, Inc.

- Minky Homecare Ltd.

- Brabantia

- Gimi S.p.A.

- JOMOO

- Pennsylvania Woodworks

- Cobbe

- Lehman Hardware and Appliances

- L-Best

- Xcentrik

- Ballard Designs

- IKEA

- Mainstays

Frequently Asked Questions

The global Cloth Drying Racks Market is projected to reach US$ 4.75 Bn by 2033, growing from US$ 3.33 Bn in 2026 at a compound annual growth rate of 5.2% during the forecast period.

Market demand is primarily driven by accelerating global urbanization with 68% of the world's population projected to reside in urban areas by 2050 according to the United Nations, creating acute housing space constraints that necessitate compact laundry solutions, combined with environmental consciousness as approximately 40% of consumers intend switching to eco-friendly laundry products and sustainable air-drying alternatives over energy-intensive electric dryers.

Metal drying racks command approximately 45% market share, dominating through superior durability enabling higher weight-bearing capacities essential for supporting wet garments, competitive pricing facilitated by manufacturing economies of scale, rust-resistant stainless steel options suitable for humid environments, and aesthetic versatility with diverse finishes compatible with contemporary and industrial interior design styles.

Asia Pacific constitutes the fastest-growing regional market driven by explosive urbanization rates with China projected to reach 70% urbanization by 2030 and India expected to achieve 50% by 2051, rapidly expanding middle-class populations with rising disposable incomes, and manufacturing cost advantages positioning the region as the global production hub serving both domestic consumption and international export markets.

Significant opportunities include smart and IoT-enabled drying rack development incorporating automated rain-sensing retraction, mobile app-controlled heating elements, and voice command compatibility with platforms like Amazon Alexa and Google Assistant, alongside commercial sector expansion targeting the laundromat industry projected to grow at 6% to 10% CAGR through 2030, hospitality establishments integrating guest room amenities, and healthcare facilities requiring antimicrobial-coated solutions meeting stringent hygiene standards.

Leading market participants include Brabantia, Leifheit AG, Honey-Can-Do International LLC, along with Whitmor Inc., Minky Homecare Ltd., Gimi S.p.A., JOMOO, and Ikea, among other established home goods manufacturers.