- Non-food Packaging

- Dropper System Market

Dropper System Market Size, Share, and Growth Forecast, 2026 - 2033

Dropper System Market By Material (Glass, Polypropylene, Others), Dropper Size (15-18 mm, 18-21 mm, Others, Capacity, End-user, and Regional Analysis for 2026 - 2033

Dropper System Market Size and Trends Analysis

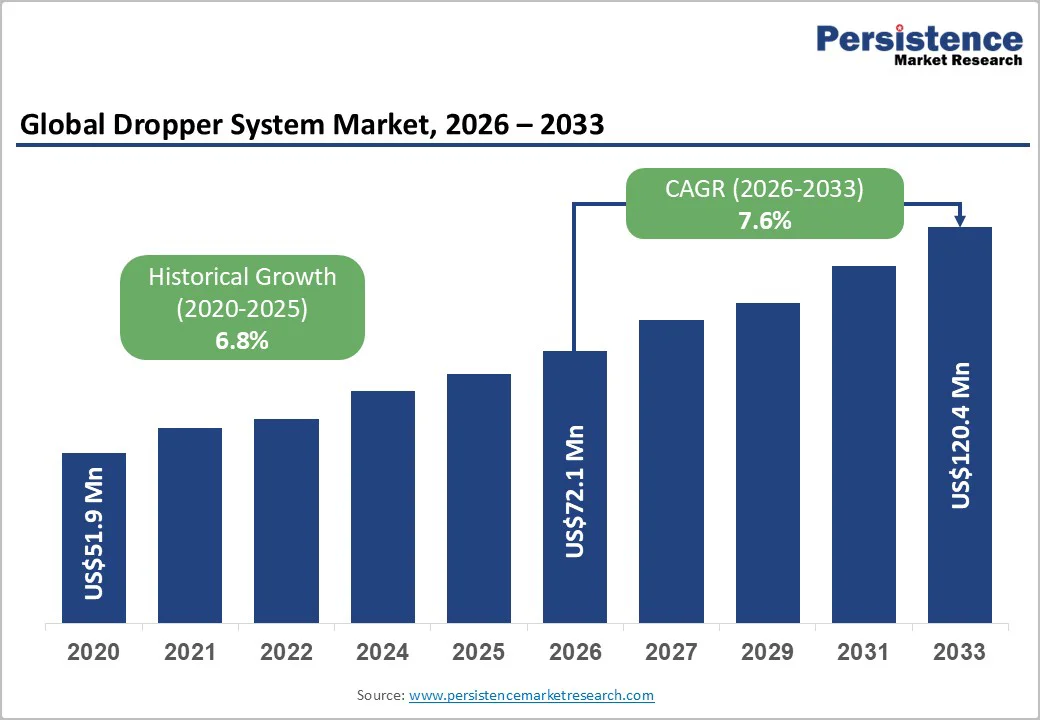

The global dropper system market size is likely to be valued at US$72.1 million in 2026 and is expected to reach US$120.4 million by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033, driven by rising pharmaceutical and ophthalmic therapy volumes, sustained expansion of premium cosmetics, and stronger regulatory emphasis on container-closure integrity.

Precision dosing demand expands across consumer healthcare and beauty, while sustainability drives upgrades to recycled glass and mono-material plastics. Asia-Pacific manufacturing growth ensures supply stability and accelerates innovation.

Key Industry Highlights

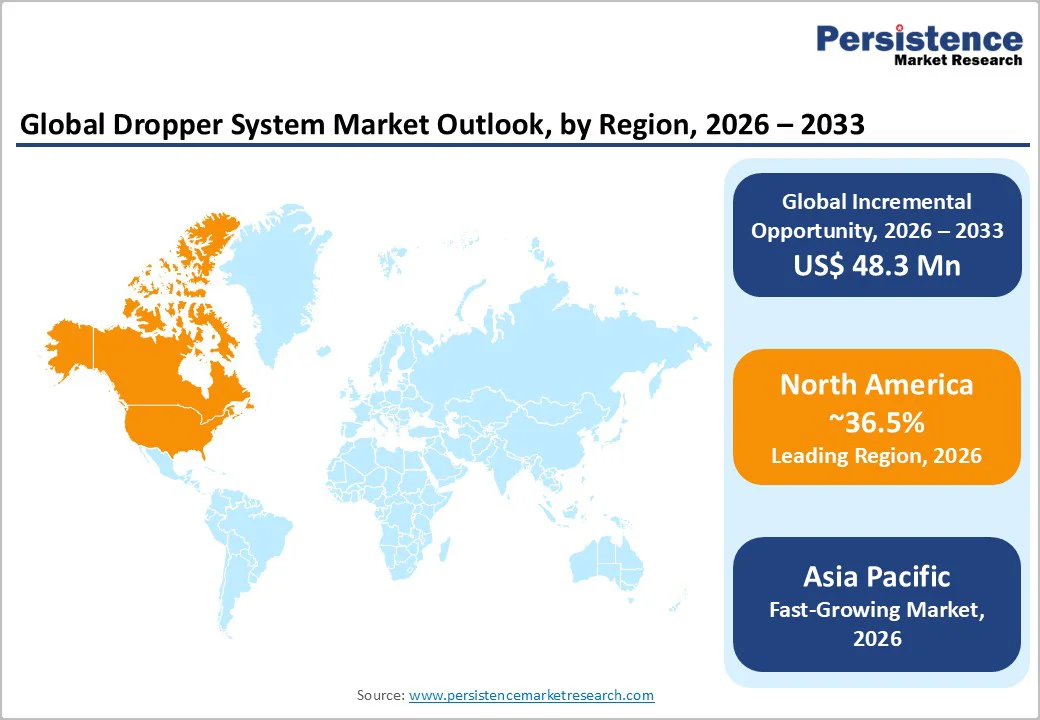

- Leading Region: North America is estimated to be the largest regional market, holding an estimated 36.5% share in 2026, supported by strong pharmaceutical production, advanced ophthalmic care, and stringent U.S. FDA CCI and material-compliance expectations.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by expanding pharmaceutical manufacturing, rising cosmetic consumption, and regulatory upgrades across China (NMPA), Japan (PMDA), India (Schedule M), and ASEAN markets.

- Investment Plans: Industry investment is focused on automation of dropper assembly, expansion of low-particle glass and elastomer lines, sustainable materials (PCR glass, mono-material PP), and regional capacity expansion in North America, Europe, China, India, and Vietnam to support clinical trials, premium cosmetics, and high-purity ophthalmic products.

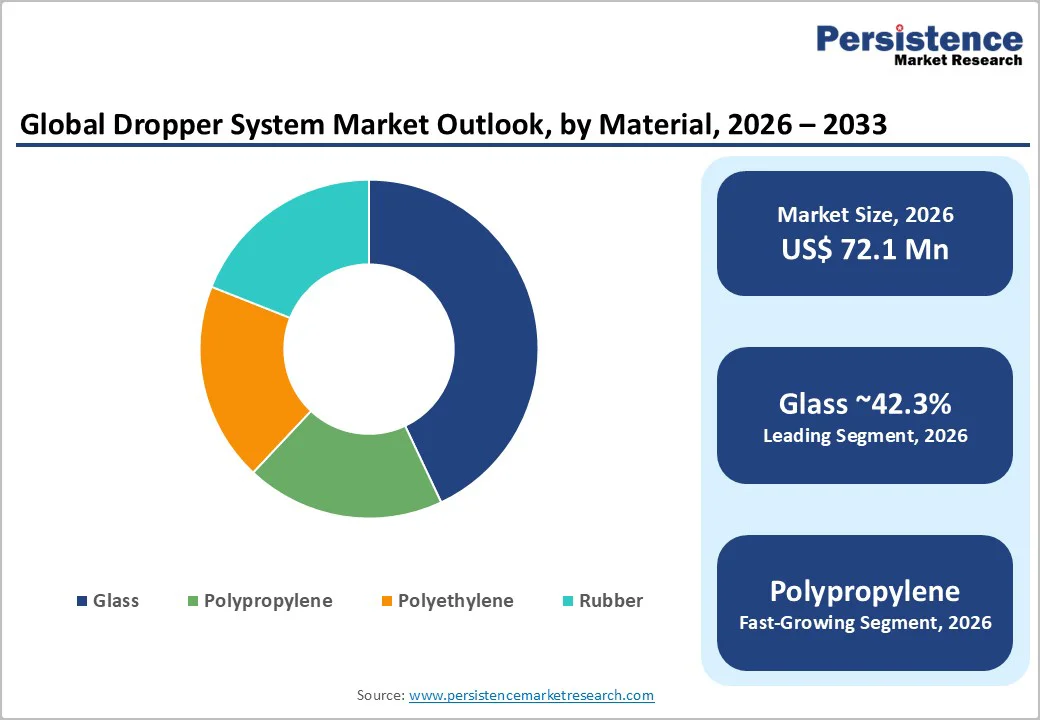

- Dominant Material: Glass is estimated to lead the material segment with 42.3% market share in 2026, driven by its superior chemical stability, barrier performance, and regulatory acceptance in pharmaceuticals, ophthalmic, and premium skincare applications.

- Leading Dropper Size: The 15-18 mm segment is expected to hold the highest share at 36.3% in 2026, supported by compatibility with standardized filling lines, broad design flexibility, and widespread use across prescription liquids, ophthalmic products, and serums.

| Key Insights | Details |

|---|---|

| Dropper System Market Size (2026E) | US$72.1 Mn |

| Market Value Forecast (2033F) | US$120.4 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Pharmaceutical and Ophthalmic Products

Pharmaceutical packaging demand continues to accelerate as biopharmaceutical pipelines expand and outpatient therapies grow. Ophthalmic treatments for chronic conditions such as dry eye, glaucoma, and postsurgical care have increased the use of both single-dose and multi-dose droppers. The rise in prescription liquid formulations places pressure on suppliers to deliver sterile, low-particle systems with validated light protection and extractables performance.

These requirements favor amber glass containers, pharmaceutical-grade plastics, and premium closure components designed for accurate dosing. Vendors with strong compliance documentation and proven container-closure integrity capabilities gain share and command higher margins, particularly within regulated prescription channels.

Regulatory and Quality Emphasis on Container-Closure Systems

Regulatory authorities emphasize material compatibility, sterility assurance, leachable control, and barrier performance for liquid dosage packaging. The technical expectations for droppers used in pharmaceuticals and ophthalmics continue to rise as guidance expands on validation, integrity testing, and quality system reliability. T

his environment raises the qualification burden for lower-cost suppliers and increases demand for materials such as Type I and Type III glass, low-shedding elastomers, and reliably molded plastic components. Vendors able to support audits, provide extractables datasets, and demonstrate compliance with recognized standards secure a competitive advantage.

The market thereby experiences consolidation among suppliers with the capital and expertise required to maintain stringent documentation and quality control.

Sustainability and Material Substitution

Brands across pharmaceuticals, cosmetics, and consumer healthcare increasingly prioritize sustainability metrics such as recycled content, mono-material recyclability, and carbon-efficient production. Glass maintains a strong position due to its inertness and chemical stability. Yet, lighter plastic alternatives, such as polypropylene, gain traction when product sensitivity is lower.

This shift enables two growth tracks: high-value inert packaging for sensitive drugs and cost-efficient recyclable plastics for cosmetics and OTC categories. Suppliers that scale post-consumer recycled glass or validated mono-material plastic droppers quickly attract interest in Europe and the Asia Pacific, where environmental regulations and corporate stewardship commitments strongly influence purchasing decisions.

Barrier Analysis - High Qualification and Cost Burdens

Validating container-closure systems requires extensive testing, documentation, and material qualification. Pharmaceutical-grade glass, low-particulate elastomers, and certified closures increase per-unit production costs.

Smaller drug developers, niche brands, and price-sensitive OTC categories may delay adoption of premium droppers as qualification cycles add months to regulatory filings and early-stage project budgets. This constraint reduces near-term conversion toward advanced droppers in lower-margin product lines, slowing premiumization within certain market segments.

Supply Chain Concentration and Raw Material Volatility

Production of pharmaceutical-grade glass and specialized elastomers is concentrated among a limited number of global manufacturers. Periodic disruptions in material availability, fluctuations in energy costs, and resin volatility create extended lead times and pricing uncertainty.

Events from 2022 to 2024 demonstrated how quickly supply constraints can shift inventory strategies for packaging buyers. Manufacturers often need to qualify secondary suppliers or increase safety stocks, raising operational complexity and procurement costs.

Precision Dosing and Differentiated Dispensing Technology

The shift toward metered-dosing droppers and low-shear valves creates significant opportunities, especially in biologics, ophthalmology, and high-value skincare. Precision formats address consistent dosing needs, reduce patient application errors, and differentiate premium products.

If precision systems capture 8 to 12% of global market adoption by 2030, the incremental addressable market would meaningfully exceed baseline growth suggested by the core market CAGR. Partnerships between packaging suppliers and pharmaceutical developers can accelerate technology validation and secure multi-year contracts tied to drug lifecycle timelines.

Opportunity Analysis - Asia Pacific Manufacturing Scale and Localization

Asia Pacific’s rapid growth in pharmaceuticals, cosmetics, generics manufacturing, and contract packaging offers substantial expansion potential for dropper suppliers. A 40-60% uplift in regional capacity would reduce global costs, improve lead times, and increase participation in international tenders.

Localized production supports regulatory filings in domestic markets and enhances supply chain resilience. Joint ventures, regional tooling centers, and plant expansions enable suppliers to meet both cost-sensitive consumer needs and quality-driven pharmaceutical requirements under a unified footprint.

Category-wise Analysis

Material Insights

Glass is projected to lead with 42.3% market share in 2026, valued for chemical inertness, superior gas barriers, and compatibility with active ingredients. Amber glass excels in UV/light protection for ophthalmic drugs such as timolol, latanoprost, and moxifloxacin, preventing degradation.

Premium cosmetics favor glass droppers for retinol serums, vitamin C, and bioactives, ensuring stability against oxidation. Suppliers meet USP <660>/<1660> via enhanced particulate control, annealing, and delamination resistance for injectables/topicals. Expanded Type II/III options, plus validated extractables/leachables reports for FDA/EMA compliance, solidify glass dominance in regulated healthcare categories.

Polypropylene (PP) is poised to be the fastest-growing material in 2026, driven by its light weight, low cost, and enhanced grades meeting ISO 10993 biocompatibility standards. Adoption is rising in pharmaceutical and personal care applications such as eye lubricants, saline formulations, essential oils, and ayurvedic drops.

Its break resistance and ease of handling offer strong advantages over glass. PP’s recyclability and suitability for mono-material packaging align with global sustainability goals, prompting major beauty brands to adopt PP droppers for skincare serums and oils. Converters are expanding validated PP assemblies ensuring suction control, dosing precision, and consistent viscosity performance.

Dropper Size Insights

The 15-18 mm neck finish is projected to dominate with a 36.3% share in 2026, due to its compatibility across ophthalmic, therapeutic, and cosmetic liquids. Its standardized geometry supports consistent dosing for eye drops, antihistamines, and pediatric vitamins, while being easily integrated into automated filling lines.

Widely accepted by pharmaceutical and cosmetic manufacturers, it enables use with tamper-evident closures, CRC systems, and inserts compliant with FDA 21 CFR 820 and EU MDR standards. Contract packers prefer this globally tooled format for efficiency. In cosmetics, it remains the go-to for precise, aesthetic droppers in serums, facial oils, and concentrates.

The 18-21 mm neck finish segment is projected to grow the fastest as brands adopt larger openings for advanced dispensing technologies. It supports metered pipettes, airless hybrids, viscous droppers, and enhanced child-resistant systems without affecting ergonomics. Premium skincare brands favor this format for thicker formulations such as peptide and retinoid serums, while pharmaceutical applications expand into elderly-care nutrition and therapeutic oils.

The wider finish improves line alignment, throughput, and reject rates in high-speed filling operations. With rising demand for precision, ease of use, and product differentiation, the 18-21 mm segment is becoming central to next-generation regulated and premium dropper designs.

Regional Insights

North America Dropper System Market Trends - Advanced Regulations and Biologics Accelerate High-Purity Dropper Demand

North America leads with a 36.5% market share in 2026, driven by U.S. pharmaceutical output, advanced ophthalmic therapies, and specialty liquid formulations needing validated droppers.

Novel biologics and ophthalmic drugs boost demand for extractables-compliant glass, high-precision pipettes, and low-particle elastomers. U.S. beauty and OTC sectors expand usage in active serums, children’s medicines, and wellness products, fueled by a robust innovation pipeline.

The FDA’s 2024 CCI testing guidance for sterile drugs mandates robust validation, sterile barriers, and documentation, heightening need for extractables/leachables data, USP-compliant glass droppers, and traceable components. Nitrosamine contamination focus (2023 - 2025) prompts validation of packaging interactions, favoring high-purity glass and polymer droppers.

Canada advances via specialty pharma and Health Canada’s 2024 sterile ophthalmic generics approvals, spurring preservative-free dropper demand. Regional drivers include biologics manufacturing growth, therapies for glaucoma/dry eye, and tamper-evident usability.

The U.S. Plastics Pact 2025 targets drive recyclable mono-material PP/HDPE droppers. Investments target clinical trial packaging, low-particle closures, and sustainability. Vendors launch ISO 8317 child-resistant droppers, ophthalmic metered pipettes, and recyclable cosmetic options.

Europe Dropper System Market Trends - Stringent Compliance Drives Premium, Recyclable Dropper Innovation

Europe is a regulation-driven market with advanced pharmaceutical hubs in Germany, France, the U.K., and Spain, plus a premium cosmetics sector. Demand stems from strict material safety, lifecycle, and recyclability standards. Germany drives growth via its pharma and medtech ecosystems; BfArM’s 2024 extractables/leachables rules for ophthalmic packaging spur compliant glass/polymer solutions.

The U.K. biotech and clinical trials advance with MHRA’s 2023 international GMP recognition, easing multinational manufacturing and boosting validated dropper needs. Cosmetics Europe’s 2024 Sustainable Packaging Guidelines push recyclable glass, PCR content, and mono-material droppers for serums, brighteners, and dermocosmetics.

EMA harmonization ensures uniform packaging specs across borders. Suppliers emphasize recyclability, validation, and documentation. EU PPWR 2024 mandates recycling rates, material restrictions, and design-for-recycling.

Investments target automation, energy-efficient glass furnaces, and recycler partnerships; 2023-2024 saw expansions in high-recycled-content production for reliability. Rising active-ingredient concentrations in cosmetics heighten demand for precision-dosing, aesthetic, compatible droppers.

Asia Pacific Dropper System Market Trends - Regulatory Upgrades and Cosmetics Expansion Fuel Rapid Growth

The Asia Pacific region is poised to be the fastest-growing market for droppers, driven by expanding pharmaceutical manufacturing, strong cosmetics consumption, and deeper integration into global supply chains.

China leads with manufacturing scale, robust domestic brand growth, and strengthened regulations from the National Medical Products Administration (NMPA) in 2023 - 2024, including updated GMP requirements emphasizing traceable primary packaging. This shift benefits suppliers of compliant droppers, particularly for ophthalmics and traditional Chinese medicine (TCM) liquid formulations.

China’s booming beauty sector, fueled by active-ingredient serums, further boosts glass and PP dropper demand. Japan maintains the region’s highest technical standards, with the Pharmaceutical and Medical Device Agency (PMDA) 2024 guidance on container-closure integrity driving demand for high-purity glass and premium polymer droppers for sterile ophthalmic products.

India remains a key player in generics and low-cost packaging, with Schedule M revisions in 2023 enhancing GMP compliance and promoting standardized, validated droppers for exports. The country’s Ayurvedic and herbal medicine sectors also rely on customizable liquid droppers.

ASEAN markets are expanding due to rising health awareness and beauty consumption, with regulations such as Indonesia’s 2024 Halal Product Assurance Regulation influencing packaging transparency. Investment opportunities include capacity expansion, localized tooling, and sustainability initiatives such as PCR-content glass, lightweight PP, and recyclable mono-material droppers, aligning with both regulatory compliance and brand-driven eco-friendly objectives.

Competitive Landscape

The global dropper system market is moderately concentrated, with global suppliers holding substantial share in regulated pharmaceutical applications and regional converters serving cosmetics and consumer healthcare. Leading companies dominate segments requiring sterile manufacturing, validated materials, and detailed regulatory documentation.

Smaller converters succeed in less regulated categories where customization, short lead times, and cost control matter most. Market conditions favor suppliers capable of providing integrated systems that include glass, closures, pipettes, and inserts alongside strong quality systems. Sustainability attributes and rapid-qualification services are emerging as key differentiators.

Key strategic themes include innovation in precision dosing, regional capacity expansion to lower costs, and adoption of sustainable materials such as PCR glass and mono-material plastics. Suppliers combine regulatory support, rapid qualification, and integrated component offerings to secure long-term partnerships, especially in pharmaceutical and ophthalmic segments.

Key Industry Developments

- In May 2024, AptarGroup launched its “NeoDropper”, a next-generation dropper designed for high-precision skincare and cosmetic formulations. The dropper improves formula protection and dosing control and is compatible with existing glass bottles

- In January 2025, after completing the acquisition of Bormioli Pharma, Gerresheimer presented an expanded portfolio of containment and delivery solutions, including vial, cartridge, ampoule, and dropper systems for sensitive biologics, at the 2025 edition of Pharmapack. The move is anticipated to broaden its reach in pharmaceutical packaging beyond droppers alone.

Companies Covered in Dropper System Market

- Adelphi Group

- SGD Pharma

- VWR International

- DWK Life Sciences

- Gerresheimer AG

- Stevanato Group

- Bormioli Pharma

- Pacific Vial Manufacturing

- The Plasticoid Company

- Qosina Corporation

- Thermo Fisher Scientific

- Wheaton Industries

- Comar LLC

- O.Berk Company

- Acme Vial and Glass

- Nipro Pharma Packaging

- Alpha Packaging

- Vidraria Anchieta

- Roetell Glass

- Jayhawk Plastics

Frequently Asked Questions

The dropper system market is estimated to reach US$72.1 million in 2026.

By 2033, the market value is projected to reach US$120.4 million.

Key trends include an accelerating shift toward sustainable materials, especially mono-material PP droppers and higher recycled-content glass, and stricter regulatory expectations for container-closure integrity, extractables, and leachables (FDA, EMA, NMPA, PMDA).

Glass is the leading material, holding 42.3% of the market share due to its chemical stability, regulatory acceptance, and suitability for pharmaceuticals and premium skincare.

By dropper size, the 15-18 mm segment leads with 36.3% share, supported by standardized tooling, compatibility with automated filling lines, and versatile use across pharma, ophthalmic, and cosmetic products.

The dropper system market is expected to grow at a CAGR of 7.6% from 2026 to 2033.

Major companies include Berry Global, Gerresheimer AG, AptarGroup Inc., DWK Life Sciences, and Nipro Corporation.