- Automotive

- Dirt Bike Market

Dirt Bike Market Size, Share, and Growth Forecast, 2026 - 2033

Dirt Bike Market by Powertrain (ICE 2-Stroke, ICE 4-Stroke, ICE Fuel-Injected, Electric, Hybrid), Product Type (Motocross, Enduro, Trail/Recreation, Dual-Sport/Street-Legal, Adventure/Long-Distance, Mini/Kids, Others), Business Model (New Sales, Used Sales/Certified Pre-Owned, Rental, Subscription/Motorcycle-as-a-Service (MaaS), Aftermarket Parts & Accessories, Service & Maintenance Contracts, Telematics/Connected Services, Battery-as-a-Service (BaaS)), and Regional Analysis for 2026 - 2033

Dirt Bike Market Share and Trends Analysis

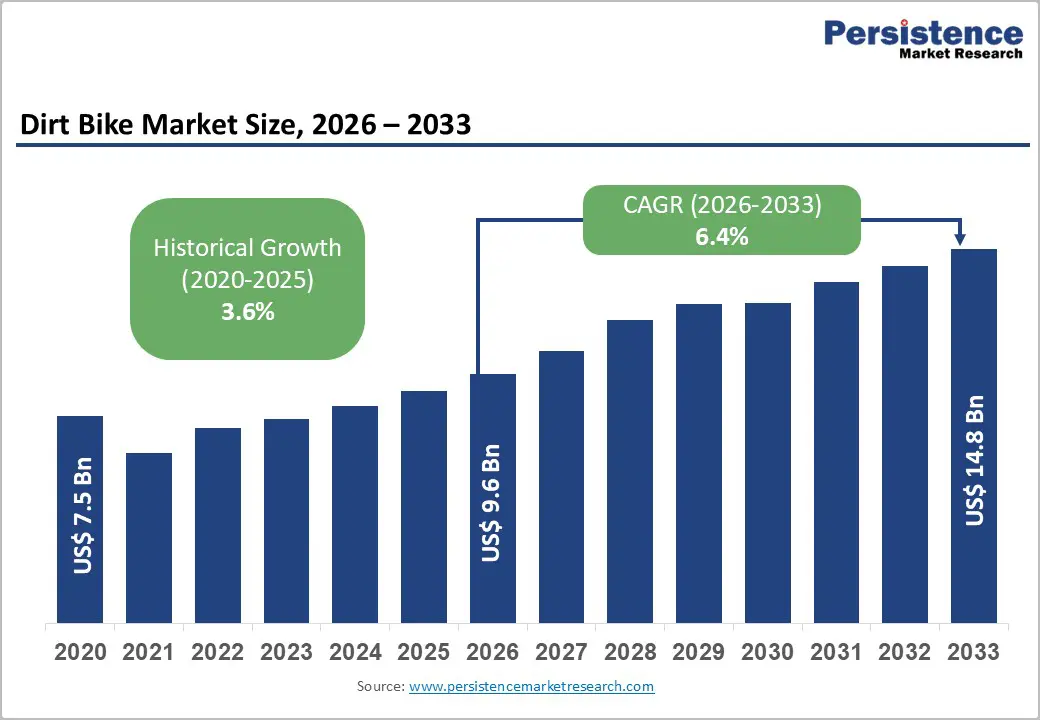

The global dirt bike market size is likely to be valued at US$ 9.6 billion in 2026, and is projected to reach US$ 14.8 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026 - 2033. The demand graph is moving in the upward direction as recreational off-road participation is increasing across North America and Europe, while electrification is accelerating in Asia Pacific.

Youth entry platforms are expanding as original equipment manufacturers (OEMs) are strengthening financing schemes and digital retail channels. Buyers are gradually shifting toward mid-displacement performance motorcycles and electric variants as governments are tightening emission and noise regulations. Manufacturers are aligning product portfolios with these regulatory trends and are prioritizing compliant four-stroke and battery-electric platforms to secure long-term volume stability.

Production and registration data from the European Association of Motorcycle Manufacturers (ACEM), the Motorcycle Industry Council (MIC), and the Society of Indian Automobile Manufacturers (SIAM) are indicating that off-road categories are recovering steadily following supply chain disruptions after 2020. Electric off-road registrations are increasing in semi-urban areas where internal combustion engine (ICE) noise limits are becoming stricter. OEMs are focusing on premium motocross platforms to improve margins while expanding recurring revenue streams through aftermarket components, telematics solutions, and battery subscription programs.

The industry is transitioning from a hardware-focused sales model toward a broader ecosystem strategy that integrates vehicle sales, performance upgrades, digital connectivity, and service contracts. Capital investment is increasingly flowing into electrified architectures, dealer credit expansion, and emerging Asia Pacific tourism corridors, and these decisions are shaping competitive positioning through 2033.

Key Industry Highlights

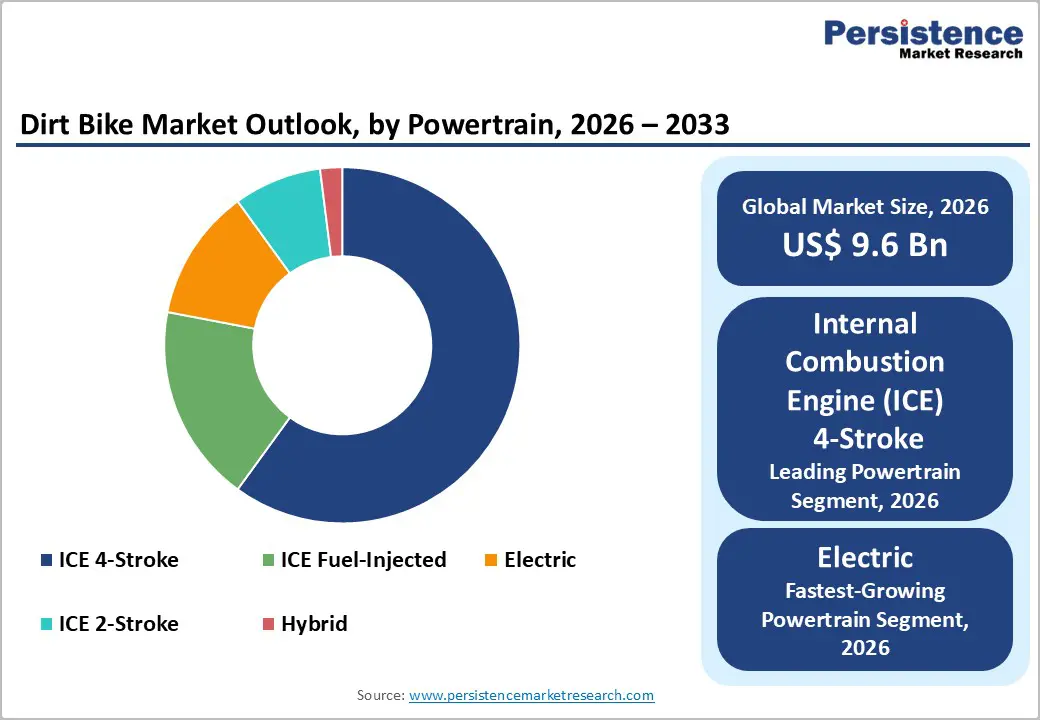

- Powertrain Dominance: 4-stroke ICE models are projected to account for approximately 60% of global revenues in 2026, owing to regulatory compliance advantages and broader torque delivery.

- Fastest-growing Powertrain: Electric dirt bikes are anticipated to expand the fastest at roughly 15% CAGR through 2033, driven by tightening emissions standards and declining battery costs.

- Product Leadership: Motocross models are estimated to hold around 32% market share in 2026, reflecting strong participation in organized racing circuits and premium upgrade cycles.

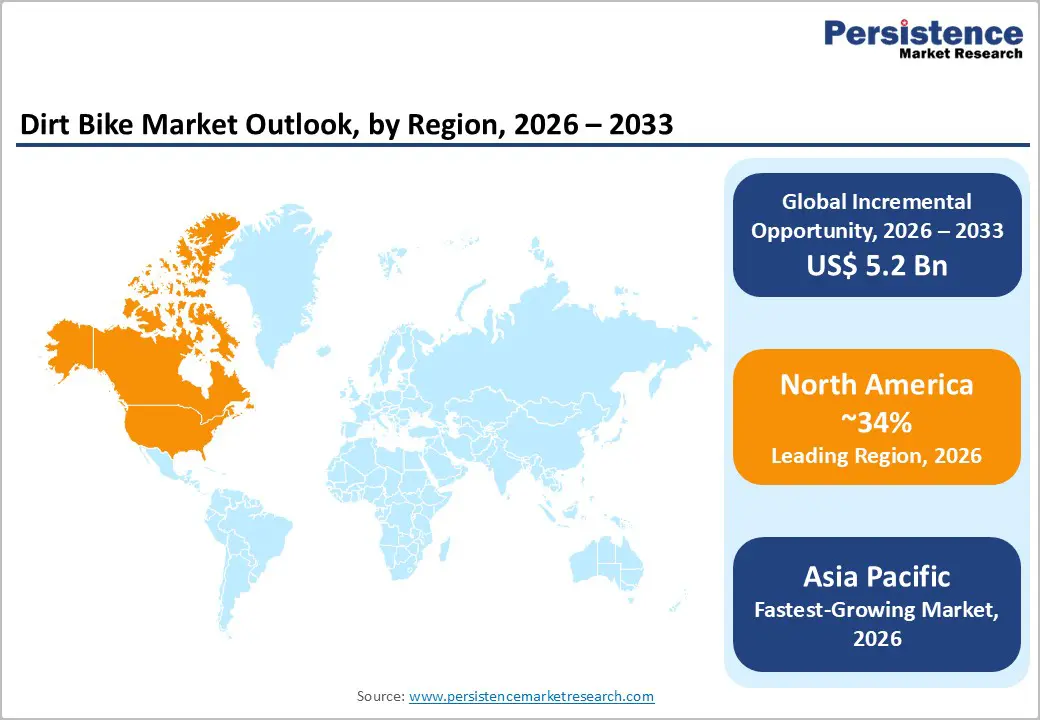

- Regional Performance: North America is expected to lead with an estimated 34% share in 2026, underpinned by established motocross infrastructure, whereas Asia Pacific is projected to be the fastest-growing market at roughly 8% CAGR, driven by electric manufacturing scale.

- December 2025: Talaria unveiled the Komodo, a high-performance electric off-road dirt bike featuring a 32 kW motor, up to 754 Nm of torque, a lithium battery with about 115 km range, and a rugged forged alloy chassis aimed at delivering powerful acceleration and agility on trails.

| Key Insights | Details |

|---|---|

| Dirt Bike Market Size (2026E) | US$ 9.6 Bn |

| Market Value Forecast (2033F) | US$ 14.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Factors - Growth, Barriers, Opportunity

Electrification of Off-Road Mobility under Noise and Emissions Regulations

Regulatory authorities are tightening emission and noise standards for off-road vehicles, and this shift is accelerating electric dirt bike adoption. The European Union (EU), for example, is enforcing Stage V emission standards for non-road mobile machinery, and these rules are limiting allowable exhaust output from ICE platforms. In the United States, states such as California are strengthening off-road vehicle noise thresholds under the supervision of the California Air Resources Board (CARB). At the global level, the International Energy Agency (IEA) is reporting sustained double-digit annual growth in global electric two-wheeler sales. These regulatory and market signals are encouraging manufacturers to accelerate electrification strategies in the off-road segment.

Electric dirt bikes are eliminating tailpipe emissions and are reducing acoustic output by approximately 70 to 80 percent compared with conventional ICE models. This reduction is enabling broader access to semi-urban and peri-urban recreational areas where riding restrictions are becoming stricter. Municipal authorities are limiting ICE riding hours, and this trend is indirectly favoring electric platforms. OEMs are reallocating capital expenditure toward modular battery systems and advanced motor controller software. Electric models are commanding premium price points due to instant torque delivery and reduced maintenance intervals. Battery costs per kilowatt-hour are declining over the past decade according to IEA data, and this trend is improving total cost of ownership. Electric penetration in dirt bikes is projected to increase from approximately 8-10% in 2025 to nearly 22-25% by 2033, and companies investing early in scalable battery architecture and dealer charging infrastructure are strengthening long-term compliance positioning and margin stability.

Cost Inflation in Performance Components and Lithium Supply Volatility

High-performance dirt bikes rely on lightweight aluminum frames, advanced suspension assemblies, and increasingly lithium-ion battery systems. Lithium carbonate prices are experiencing sharp volatility between 2022 and 2024 according to data from the IEA and global commodity exchanges, and this fluctuation is directly affecting electric motorcycle input costs. Although prices are stabilizing partially, battery pack cost variability is continuing to represent a structural exposure for manufacturers. Premium suspension systems are being sourced from a limited group of specialized suppliers, and this concentration is increasing procurement risk. Retail pricing for high-performance motocross models ranges between US$ 9,000 and US$ 12,000 in developed markets, and higher benchmark interest rates are raising financing costs for consumers following global monetary tightening cycles.

Regulatory compliance is adding additional certification expenses, particularly across European markets where emission and noise validation procedures are becoming more stringent. Manufacturers are spending more time and capital on homologation testing, which is extending product development cycles. A 10% increase in battery costs raises electric dirt bike production expenses by approximately 4-6%, compressing gross margins in price-sensitive segments. Elevated borrowing costs are reducing discretionary spending on recreational vehicles in certain developed economies. Companies that are lacking vertical integration in battery sourcing or diversified supplier networks are facing higher margin pressure through 2026. Firms that are strengthening supply contracts, localizing component production, and improving cost forecasting capabilities are positioning themselves to manage volatility more effectively.

Digital Performance Ecosystems and Data-Driven Rider Monetization

Digital integration is emerging as a high-value opportunity within the dirt bike market landscape. Riders are increasingly demanding performance analytics, route mapping, maintenance alerts, and ride telemetry that are comparable to connected automotive platforms. Telematics hardware, cloud-based diagnostics, and mobile applications are becoming commercially viable as sensor costs are declining and wireless connectivity is expanding across recreational corridors. Organized motocross leagues and amateur racing communities are adopting data-driven coaching tools to optimize lap times, suspension calibration, and throttle response. This shift is creating a scalable software layer that extends revenue beyond initial vehicle sales.

The opportunity is particularly significant in premium motocross and electric segments where buyers are willing to pay for performance optimization and predictive maintenance services. Connected modules are enabling real-time battery health monitoring, over-the-air firmware updates, and remote diagnostics. Subscription-based analytics platforms are generating recurring monthly revenue streams, and integrated rider communities are strengthening brand loyalty. OEMs that are embedding factory-installed connectivity modules and partnering with software developers are positioning themselves to capture higher lifetime customer value. Companies that are standardizing data architecture and integrating dealer service networks with digital dashboards are strengthening retention rates while reducing warranty costs through predictive maintenance intelligence.

Category-wise Analysis

Powertrain Insights

ICE 4-stroke platforms are set to lead in 2026, accounting for approximately 60% of the dirt bike market revenue share. These engines are delivering smoother torque curves and are meeting tightening emission standards across North America and Europe. Riders are selecting four-stroke variants across trail and enduro categories because they are offering better throttle control and longer service intervals. Annual disclosures from Honda Motor and KTM AG are indicating stronger sales volumes in the 250 cubic centimeter to 450 cubic centimeter range. Dealers are prioritizing these configurations because they are generating higher average selling prices and consistent aftermarket service income. Manufacturers are continuing to refine fuel injection systems and combustion efficiency to preserve regulatory compliance while sustaining performance benchmarks.

Electric dirt bikes are slated to be the fastest-growing powertrain segment between 2026 and 2033, predicted to showcase a CAGR of about 15%. Segmental growth is accelerating as governments are tightening emission and noise regulations and as battery pack costs are stabilizing following earlier volatility. Improvements in power-to-weight ratios are enhancing ride quality and competitive performance. Recreational riders near urban centers are increasingly selecting low-noise electric platforms to comply with local restrictions. OEMs are investing in modular battery architecture and advanced motor control software, and these investments are enabling scalable product portfolios. As battery energy density is improving and charging infrastructure is expanding, electric adoption is strengthening in both youth and performance segments.

Product Type Insights

Motocross motorcycles are anticipated to dominate with an estimated 32% of the dirt bike market share in 2026. Organized racing circuits across North America and Europe are sustaining consistent demand from both professional and amateur participants. Structured league calendars are encouraging recurring equipment upgrades, and riders are replacing or modifying motorcycles at regular intervals to maintain competitive performance. Mid- to high-displacement race-specification models are commanding premium pricing due to advanced suspension systems, lightweight chassis engineering, and high-output engines. Sponsorship ecosystems are reinforcing brand visibility and are influencing purchasing decisions at the enthusiast level. OEMs are continuing to launch limited-edition variants and factory racing replicas, and these strategies are supporting higher average selling prices, while dealers are benefiting from strong parts replacement cycles, particularly for tires, braking systems, and suspension components.

Dual-sport motorcycles are poised to become the fastest-growing product segment during the 2026-2033 forecast period, expanding at about 9% CAGR. These platforms are combining off-road capability with limited on-road legality, and this flexibility is attracting a broader consumer base. Regulatory adjustments in several regions are permitting controlled road access for compliant models, and this shift is supporting incremental demand. Urban riders are increasingly seeking mobility solutions that can navigate traffic congestion while also enabling weekend trail exploration. Rising fuel costs and parking constraints in metropolitan areas are reinforcing interest in versatile motorcycles that serve multiple use cases. Manufacturers are introducing lightweight dual-purpose platforms with improved fuel efficiency and enhanced comfort features, further augmenting market prospects.

Business Model Insights

New vehicle sales are likely to command approximately 72% of the dirt bike market revenues in 2026. Authorized dealership networks are continuing to anchor distribution, and physical retail presence is reinforcing brand credibility and after-sales support. Original equipment manufacturers are expanding structured financing programs, and these initiatives are sustaining transaction volumes despite elevated interest rates in certain markets. Premium model launches in motocross and enduro categories are supporting higher average selling prices and are strengthening gross margins. Dealers are generating additional income through extended warranties, accessories, and maintenance packages bundled at the point of sale. Inventory management systems are improving stock rotation and reducing holding costs. Companies that are optimizing dealer incentive structures and aligning product launches with seasonal demand cycles are protecting revenue consistency within this dominant channel.

Rental and subscription models are expected to register the highest CAGR for the 2026-2033 forecast period. Fleet-based recreational tourism operators across Asia Pacific and selected European corridors are increasing procurement of mid-displacement motorcycles to serve guided trail experiences. Subscription-based access programs are lowering entry barriers by eliminating large upfront payments and bundling maintenance into predictable monthly fees. Telematics systems are enabling real-time fleet monitoring, usage analytics, and preventive maintenance scheduling, and these tools are improving return on investment calculations for operators. Electric variants are gaining share within rental fleets because lower operating noise and simplified servicing are reducing downtime. Manufacturers that are designing fleet-optimized platforms with reinforced components and centralized diagnostics are strengthening recurring revenue streams while diversifying beyond single-unit retail transactions.

Regional Insights

North America Dirt Bike Market Trends

North America is forecast to hold an estimated market share of 34% in 2026, fostering its place as the largest regional market for dirt bikes. Well-established motocross leagues, structured amateur racing programs, and extensive off-road trail infrastructure across public and private land are factors favoring the market here. The United States dominates regional demand due to high discretionary spending and a strong culture of recreational motorsports participation. Canada is expanding organized adventure tourism networks, particularly in western provinces where trail access and outdoor recreation are increasing. Industry data indicate that steady off-road motorcycle registrations, which is supporting stable baseline demand. Dealership networks across the United States and Canada are mature, and they are generating significant aftermarket revenue through parts, service contracts, and accessories.

Regulatory developments are influencing purchasing behavior, particularly in states such as California where the CARB is tightening emission and noise standards. These measures are accelerating interest in electric dirt bikes, especially in peri-urban recreational zones. Urban expansion near traditional riding areas is increasing scrutiny on noise compliance, and electric models are gaining consideration as a practical solution. Growth is remaining moderate compared to emerging economies, but revenue per unit remains high due to premium motocross and performance-oriented platforms. Manufacturers that are investing in electrified variants, dealer financing programs, and performance-focused product upgrades are positioning themselves to sustain competitive advantage in North America through 2033.

Europe Dirt Bike Market Trends

Europe is expected to secure around 27% of dirt bike market revenues in 2026, and is set to remain a high-value market for premium off-road motorcycles. Germany, France, Italy, and Austria are contributing the majority of regional demand due to established racing traditions and strong dealer ecosystems. The EU is enforcing Stage V emission standards for non-road mobile machinery, and these regulations are influencing product development priorities across the region. Manufacturers are continuing to upgrade engine management systems and exhaust configurations to maintain compliance while preserving performance benchmarks. Companies that are aligning homologation strategy with regulatory timelines are strengthening market continuity and reducing certification delays.

Electric adoption is expanding more rapidly in urban-fringe areas where municipalities are tightening noise controls and environmental oversight. Electric dirt bikes are providing lower acoustic output and zero tailpipe emissions, and this advantage is enabling broader access to regulated recreational zones. Europe is benefiting from the presence of major original equipment manufacturers such as KTM AG and Husqvarna Motorcycles GmbH, which are headquartered within the region and are investing in electrified platforms. This local manufacturing base is strengthening innovation capacity and supply chain integration. Manufacturers that are accelerating electric portfolio expansion, reinforcing dealer training, and optimizing cross-border distribution within the EU are positioning themselves for sustained growth through the forecast horizon.

Asia Pacific Dirt Bike Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market for dirt bikes, projected to post a CAGR of nearly 8.2% between 2026 and 2033. India, China, and Australia are serving as primary growth corridors due to expanding middle-income populations and rising participation in recreational motorsports. Disposable household income is increasing across urban centers, and younger demographics are seeking experiential outdoor activities. Organized adventure tourism operators are scaling guided trail programs, which is stimulating fleet procurement of mid-displacement motorcycles. Government initiatives supporting tourism infrastructure are improving rural connectivity and access to off-road destinations. Manufacturers that are tailoring product specifications to regional terrain conditions and price sensitivity are strengthening competitive positioning across this diverse market landscape.

China is playing a strategic role in shaping regional supply chains due to its established electric two-wheeler manufacturing ecosystem. Battery production capacity, motor assembly expertise, and component localization are supporting cost efficiencies for electric dirt bike platforms. Regulatory authorities across several Asia Pacific countries are prioritizing low-emission mobility policies, and this focus is encouraging gradual electrification within recreational segments. Urban expansion is increasing scrutiny on noise and environmental impact, and electric variants are gaining acceptance in regulated zones. Domestic producers and global OEMs are investing in localized assembly and distribution networks to reduce import dependence and currency exposure. Companies that are leveraging China’s battery value chain while adapting marketing strategies to India’s and Australia’s recreational culture are positioning themselves to capture long-term growth.

Competitive Landscape

The global dirt bike market structure exhibits moderate concentration, with Honda, Yamaha, Kawasaki, KTM, and Suzuki accounting for approximately 45-50% of total revenues. Japanese and European OEMs are sustaining dominance in premium performance categories due to established engineering expertise and global brand recognition. Companies headquartered in Japan are leveraging extensive distribution networks and proven reliability standards to maintain strong positions across North America, Europe, and parts of Asia Pacific. European manufacturers are capitalizing on racing heritage and factory-backed competition programs to reinforce premium positioning. Chinese producers are simultaneously expanding electric portfolios by utilizing domestic battery supply chains and cost-efficient manufacturing structures, and this strategy is increasing competitive intensity in entry-level and mid-range electric segments.

Competitive differentiation is increasingly depending on channel control and recurring revenue capabilities. Japanese manufacturers are scaling global dealership footprints and strengthening supply chain coordination to ensure consistent parts availability. European firms are aligning product development with professional racing feedback to sustain technological credibility. Emerging electric startups are competing through rapid innovation cycles, integrated software platforms, and over-the-air update functionality. Dealer network strength is remaining a decisive advantage because after-sales service, financing support, and spare parts distribution are directly influencing customer retention.

Key Industry Developments

- In January 2026, at CES 2026 in Las Vegas, Segway introduced the Xaber 300 electric dirt bike, marking a strategic push into performance-oriented off-road electric vehicles and commuter solutions. The new products showcase enhanced connectivity, adaptive shifting, traction control, and integrated ride systems.

- In December 2025, Vida, the electric vehicle division of Hero MotoCorp, launched the Dirt.E K3 electric dirt bike in India, targeting children aged 4 to 10 years and serving as an accessible entry point into off-road motorcycling. The bike features an adjustable chassis that lets the wheelbase, handlebar height, and ride height grow with the rider, and is powered by a 500 W motor with a removable 360 Wh battery.

- In August 2025, Stark Future upgraded its VARG MX electric dirt bike with improved suspension, enhanced rider ergonomics, and refined power delivery aimed at broadening appeal beyond competitive motocross riders. The updates are designed to boost overall ride quality and functionality as Stark continues to position the VARG series within the premium electric off-road segment.

Companies Covered in Dirt Bike Market

- Honda Motor Co., Ltd.

- Yamaha Motor Co., Ltd.

- Kawasaki Motors, Ltd.

- KTM AG

- Suzuki Motor Corporation

- Husqvarna Motorcycles GmbH

- GasGas Motorcycles

- Beta Motor S.p.A.

- Sherco Motorcycles

- Zero Motorcycles, Inc.

- Stark Future S.L.

- Apollo Motors Inc.

- SSR Motorsports

- Kuberg s.r.o.

Frequently Asked Questions

The global dirt bike market is projected to reach US$ 9.6 billion in 2026.

Increasing interest in recreational off-road participation across North America and Europe, expansion of youth entry platforms through the strengthening of financing schemes by OEMs, and proliferation of digital retail channels are driving the market.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Gradual consumer shift toward mid-displacement performance motorcycles and electric variants in response to tightening emission and noise regulations, development of compliant four-stroke and battery-electric platforms by manufacturers, and redirection of capital toward electrified architectures, dealer credit expansion, and emerging Asia Pacific tourism corridors are key market opportunities.

Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., Kawasaki Motors, Ltd., and KTM AG are some of the key players in the market.