- Plastics, Polymers & Resins

- Dichloroethane Market

Dichloroethane Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Dichloroethane Market by Grade Type (Technical grade, reagent grade, pharmaceutical grade), Application Type (Vinyl Chloride Monomer, Ethylene Amines), End-use (Construction, Automotive, Packaging, Furniture, Medical), and Regional Analysis for 2025 - 2032

Dichloroethane Market Size and Forecast Analysis

Market Overview

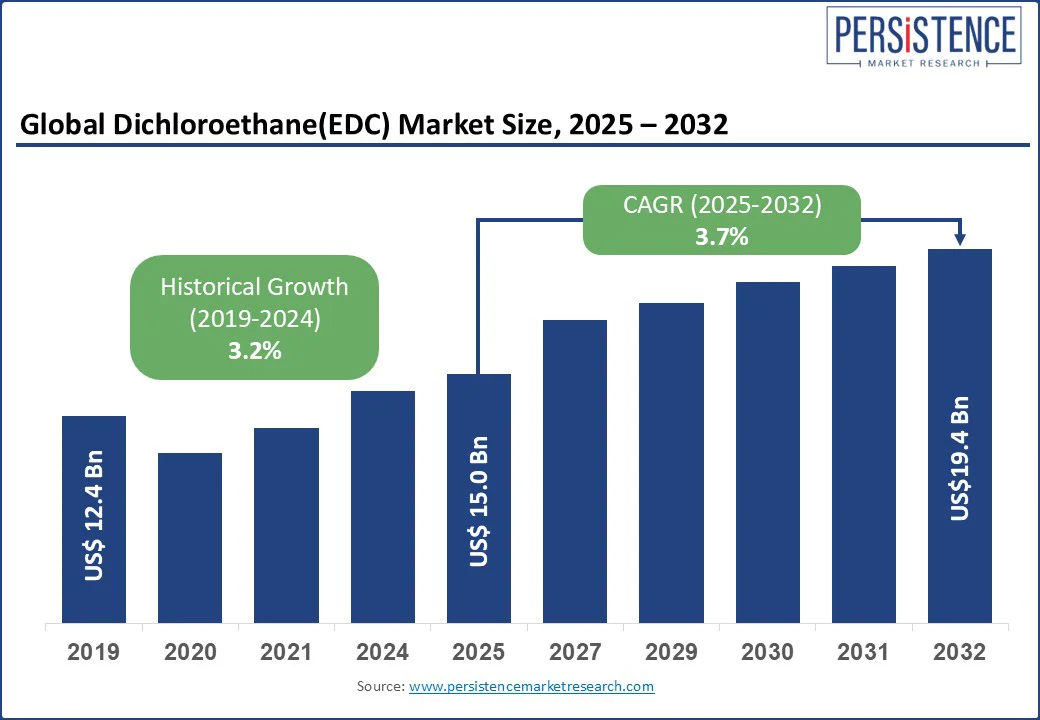

The global dichloroethane market size is likely to be valued at US$ 15.0 Bn in 2025 and is expected to reach US$ 19.4 Bn by 2032, growing at a CAGR of 3.7% from 2025 to 2032. Rising PVC demand in construction and automotive, fueled by urbanization, drives dichloroethane market growth. Technological advancements and pharmaceutical applications further boost expansion.

The global dichloroethane market is driven by increasing demand for vinyl chloride monomer (VCM) used in polyvinyl chloride (PVC) production, which is extensively utilized in construction, packaging, and automotive industries. Energy-efficient production technologies and the growing use of dichloroethane in ethylene amine manufacturing support market growth, especially in Asia-Pacific (China, India), North America, and Europe.

Market Dynamics

Drivers

Rising Demand for Vinyl Chloride Monomer (VCM) and PVC

The demand for dichloroethane is strongly driven by its role in producing vinyl chloride monomer (VCM), which is almost entirely used to manufacture polyvinyl chloride (PVC). PVC's versatility and low cost make it essential in the construction sector for applications such as piping, siding, and window frames. According to the U.S. Environmental Protection Agency (EPA), nearly all vinyl chloride produced in the U.S. is used in PVC manufacturing, underscoring its importance in this value chain. Government infrastructure initiatives further illustrate this trend. For instance, the U.S. Census Bureau reported that total construction spending surpassed $2.1 trillion in May 2025, indicating a continued rise in PVC use-and thus in dichloroethane demand-as construction activity intensifies.

Advancements in Production Technologies

Technological advancements in dichloroethane production are significantly boosting market growth. Innovations such as improved chlorination techniques and energy-efficient reactors have enhanced operational efficiency while reducing environmental impact. Major industry players have adopted catalytic systems that cut energy consumption in vinyl chloride monomer (VCM) production, helping to lower overall manufacturing costs and carbon emissions. These improvements are especially vital in meeting evolving environmental regulations. For instance, under the European Union’s Industrial Emissions Directive, facilities are required to adopt best available techniques (BAT) to limit pollution. The European Commission identified optimized thermal chlorination and by-product recycling as part of BAT conclusions for large chemical plants, reinforcing the industry's shift toward cleaner and more sustainable production.

Restraints

Health and Safety Concerns

Dichloroethane safety concerns are rising due to its classification as a Group 2B carcinogen by the IARC, indicating possible cancer risks. Manufacturers must comply with strict occupational exposure limits, such as OSHA’s 10 ppm and NIOSH’s 1 ppm guidelines, increasing operational costs. Compliance requires advanced ventilation, monitoring, and personal protective equipment. In regions with strict chemical safety laws, such as the EU (under REACH), usage is increasingly limited. These health risks and regulatory pressures reduce its adoption in sensitive applications and encourage investment in safer alternatives. As environmental and worker safety regulations tighten globally, managing dichloroethane exposure remains a critical challenge for manufacturers.

Opportunities

Expansion in Emerging Markets

Rapid industrialization in the Asia-Pacific and Latin America offers strong growth opportunities for the dichloroethane market. India’s construction sector, valued at US$ 650 billion in 2024, is growing at 6% annually, fueling demand for PVC and dichloroethane-based materials. In Latin America, Brazil’s packaging industry, worth US$30 billion, is driving market expansion. These high-growth regions present untapped potential for manufacturers to scale production, optimize distribution networks, and strengthen their presence in key downstream sectors such as infrastructure and consumer packaging.(Source: (IBEF))

Growth in Medical Applications

The pharmaceutical-grade dichloroethane market is expanding due to its critical role in drug synthesis and medical device manufacturing. The global pharmaceutical industry, valued at US$ 1.5 trillion in 2023, continues to grow steadily, increasing the need for high-purity solvents such as dichloroethane. This trend creates opportunities for companies such as Meru Chem Pvt. Ltd., which specializes in producing pharmaceutical-grade dichloroethane that complies with stringent quality and regulatory standards required by the healthcare and life sciences sectors.(Source: IQVIA).

Category-wise Analysis

Grade Type Insights

- Technical-grade dichloroethane leads the 2024 market due to its vital role in VCM manufacturing, driven by its extensive use in VCM production for PVC. Its cost-effectiveness and compatibility with industrial processes make it the preferred choice in construction and packaging.

- Pharmaceutical grade is projected to grow rapidly from 2025 to 2032, driven by increasing demand in medical applications, such as drug synthesis and sterilization processes. Its high purity and compliance with stringent regulatory standards fuel adoption in the healthcare sector.

Application Type Insights

- Vinyl chloride monomer (VCM) production dominates the market in 2024, driven by its essential role in PVC manufacturing, driven by the global demand for PVC in construction, packaging, and automotive sectors. The scalability of VCM production processes ensures its dominance.

- Ethylene amines are expected to grow significantly, supported by their use in adhesives, coatings, and agricultural chemicals. The adhesives market’s growth, particularly in the Asia-Pacific region, drives this segment’s expansion.

End-Use Insights

- Construction remains the leading sector in 2024, driven by robust demand across global infrastructure projects, fueled by global infrastructure development and PVC’s widespread use in pipes, fittings, and profiles. Urbanization in emerging markets such as India and China supports this segment.

- The medical sector is projected to grow rapidly, driven by the increasing use of pharmaceutical-grade dichloroethane in drug manufacturing and medical device production, supported by the global pharmaceutical market’s expansion.

Regional Insights

North America Dichloroethane Market Trends

- United States: The U.S. dominates the North American dichloroethane market, accounting for 25% of global demand in 2024. This leadership is fueled by a strong construction sector valued at US$ 1.8 trillion in 2023 that heavily utilizes PVC for infrastructure development. The packaging industry, estimated at US$ 190 billion, also contributes significantly, according to the Packaging Machinery Manufacturers Institute. Additionally, the U.S. Environmental Protection Agency’s (EPA) emphasis on low-emission manufacturing has led to a 12% annual rise in sustainable production practices, with companies such as Westlake Chemical investing in energy-efficient technologies.

- Canada: Market growth in Canada is supported by a steadily expanding construction industry, which is growing at an annual rate of 4%, creating consistent demand for dichloroethane-based products.

Europe Dichloroethane Market Trends

- Germany: Germany leads the European dichloroethane market, accounting for 30% of the regional share in 2024. The construction sector, valued at US$ 500 billion, drives significant PVC demand, thereby boosting dichloroethane consumption. The European Union’s Green Deal, which aims to cut chemical emissions by 50% by 2030, has propelled a 10% annual increase in sustainable production methods across the country.

- France: Market growth in France is supported by a US$ 50 billion packaging industry, which relies on PVC applications. Key players such as Vynova Group are advancing the dichloroethane market through investments in low-emission technologies aligned with EU environmental directives.

- United Kingdom: The U.K. contributes steadily to regional demand, with its construction industry expanding at an annual rate of 3.5%, creating a sustained need for dichloroethane-based materials.

Asia-Pacific Dichloroethane Market Trends

- China: China anchors Asia-Pacific’s dominance in the dichloroethane market, driven by a US$ 1.2 trillion construction industry and a US$ 150 billion packaging sector. The government’s “Made in China 2025” initiative continues to fuel industrial output, with adhesive consumption-closely tied to dichloroethane. This industrial momentum sustains high demand for PVC and related chemicals.

- India: India’s market growth is propelled by its US$ 650 billion construction sector and government-led “Make in India” initiative, which encourages domestic manufacturing. Dichloroethane usage in India is increasing at a rate of 9% per year, supported by rising infrastructure and packaging needs.

- Asia-Pacific Overall: The region maintains a strong focus on sustainable production practices, in line with global environmental standards, further shaping market dynamics in 2024.

Competitive Landscape

Key players in the global dichloroethane market are focusing on sustainability and efficiency to stay competitive. Investments in low-emission and bio-based production help meet strict environmental regulations, while partnerships with construction and packaging sectors expand market reach. Companies such as Vynova Group prioritize cost-effective manufacturing to manage raw material volatility, and Formosa Plastics is expanding capacity in the Asia-Pacific region to meet growing demand.

Key Developments

- 2024: Hanwha Solutions launched a low-emission dichloroethane production process, reducing carbon emissions by 20%.

- 2023: Occidental Petroleum invested US$ 400 million in energy-efficient VCM production, enhancing sustainability.

- 2024: SABIC introduced a bio-based dichloroethane variant for pharmaceutical applications, targeting the medical sector.

Companies Covered in Dichloroethane Market

- Formosa Plastics Corporation

- Occidental Petroleum Corporation

- Vynova Group

- Arihant Solvents and Chemicals

- Hwatsi Chemical Pvt. Ltd.

- Hanwha Solutions

- Westlake Chemical

- Valco Group

- SABIC

- Meru Chem Pvt. Ltd.

- Asahimas Chemical Company

- Others

Frequently Asked Questions

Rising demand for VCM and PVC in construction, advancements in production technologies, and growth in ethylene amine applications.

Technical grade is a dominant type known for its widespread use in VCM production.

Ethylene amines, driven by demand in adhesives and coatings.

Asia-Pacific, holding the largest share in 2024, is led by strong growth in China and India.

They drive the adoption of low-emission and bio-based production methods.

Formosa Plastics, Occidental Petroleum, and SABIC lead through innovation and strategic expansions.