- Bulk Chemicals

- Defoamers Market

Defoamers Market Size, Share, and Growth Forecast 2026 - 2033

Defoamers Market by Product Type (Water-based, Oil-based, Silicone-based, Others), Form (Liquid, Powder, Emulsion/Dispersion), Application (Pulp & Paper, Paints, Coatings & Inks, Water & Wastewater Treatment, Oil & Gas, Detergents & Cleaning Products, Food & Beverage Processing, Textiles, Adhesives & Sealants, Agrochemicals, Others), and Regional Analysis, 2026 - 2033

Defoamers Market Size and Trend Analysis

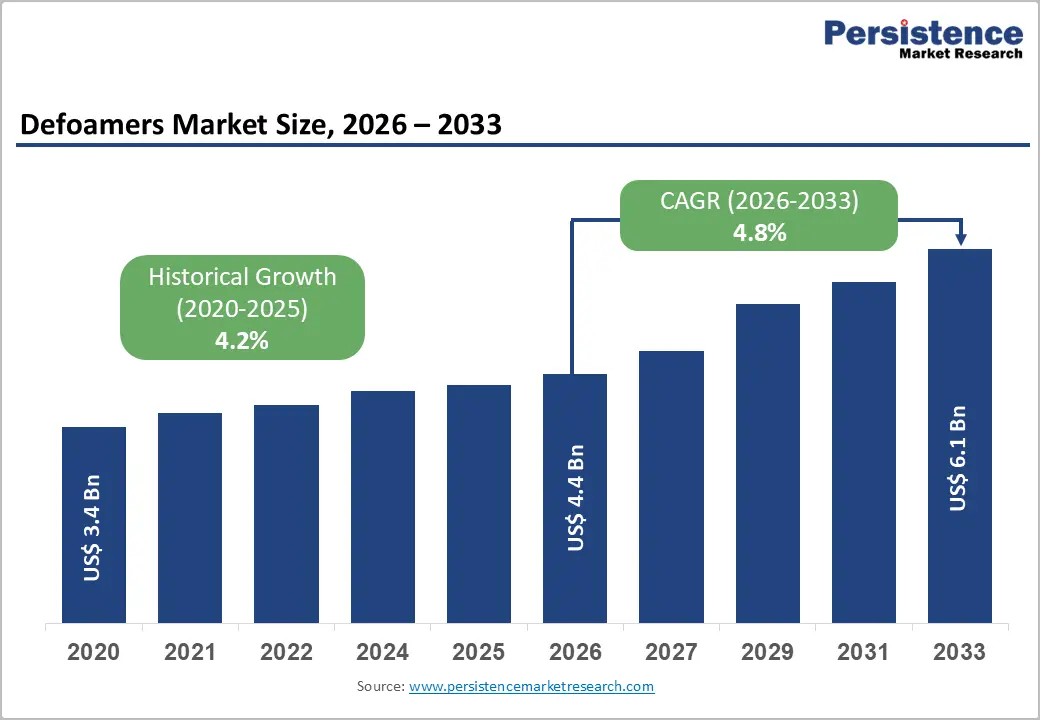

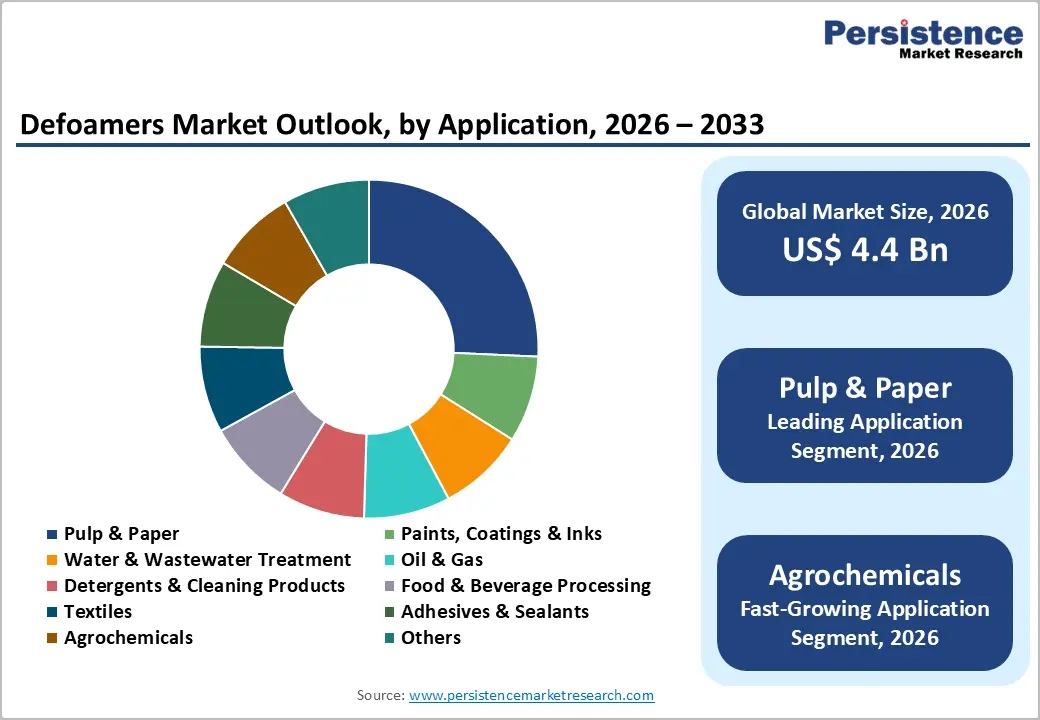

The global defoamers market size is expected to be valued at US$ 4.4 billion in 2026 and projected to reach US$ 6.1 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033. Rising industrial output across pulp and paper, water treatment, and paints and coatings is the central driver of defoamers market expansion.

Growing environmental mandates are accelerating demand for low-VOC, bio-based, and silicone-free formulations, while rapid industrialization across the Asia Pacific is broadening the consumer base. Increasing investments in municipal wastewater infrastructure and expanding agrochemical production in emerging economies further reinforce the structural growth trajectory of the global defoamers industry in the forecast period.

Key Industry Highlights:

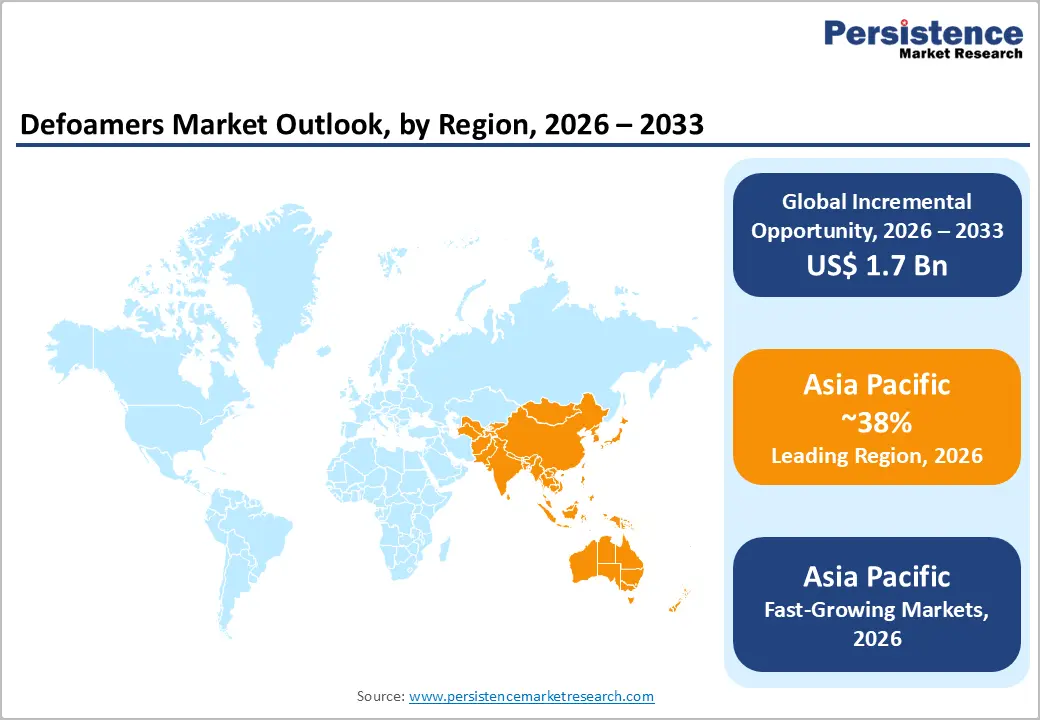

- Leading Region: Asia Pacific leads the global defoamers market with approximately 37% to 39% revenue share in 2025, anchored by China's dominant manufacturing base and India's expanding agrochemical, food processing, and water treatment sectors.

- Fastest Growing Region: Asia Pacific is also the fastest growing defoamers region through 2033, fueled by industrial expansion, rising agricultural chemical demand, infrastructure investment in water treatment, and growing eco-friendly formulation adoption across ASEAN nations.

- Dominant Segment: Silicone-based defoamers dominate by product type with approximately 37% market share in 2025, owing to superior foam control at low dosages, thermal and pH stability, and wide-ranging compatibility across pulp and paper, water treatment, and coatings.

- Fastest Growing Segment: The agrochemicals application segment is the fastest growing from 2026 to 2033, driven by rising global food demand, intensifying crop protection chemical use across Asia Pacific and Latin America, and bio-degradable defoamer innovation.

- Key Market Opportunity: Development of bio-based and low-VOC defoamer formulations presents the most significant opportunity, as regulatory mandates under EU REACH and U.S. EPA VOC standards and sustainability commitments from key end-users accelerate demand for green chemistry alternatives.

| Key Insights | Details |

|---|---|

| Defoamers Market Size (2026E) | US$ 4.4 Billion |

| Market Value Forecast (2033F) | US$ 6.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 4.8% |

| Historical Market Growth (2020 - 2025) | 4.2% CAGR |

Market Dynamics

Drivers - Expanding Pulp & Paper Industry Driving Consistent Defoamer Demand

The global pulp and paper industry remains one of the most significant end-use drivers of defoamer consumption. Defoamers are indispensable during the pulping, washing, coating, and recycling stages of paper manufacturing, where uncontrolled foam formation can disrupt machinery operation, impair product quality, and reduce production efficiency. Asia contributed approximately 39.8% of global pulp consumption out of the total 182.9 million tonnes produced globally in 2021, as reported by CEPI Key Statistics, with this share continuing to rise on the back of growing packaging, hygiene, and tissue paper demand. The surge in e-commerce-driven packaging demand and the global expansion of recycled fiber processing, where foam generation is particularly challenging, are creating sustained, incremental demand for advanced defoaming solutions. Companies such as Kemira Oyj, which specializes in pulp and paper defoamer applications, are directly benefiting from this structural demand trend.

Rising Global Investment in Water and Wastewater Treatment Infrastructure

Accelerating investment in municipal and industrial water treatment represents a second major demand catalyst for the defoamers market. Defoamers play a critical operational role in wastewater treatment facilities, controlling foam formation during aeration, biological treatment, and sludge processing stages. Stringent government regulations on water quality and industrial effluent discharge, such as those enforced by the U.S. Environmental Protection Agency (EPA) under the Clean Water Act and by the European Environment Agency under the Urban Wastewater Treatment Directive, are compelling utilities and industries to invest in compliant, high-efficiency treatment chemicals including defoamers. The United Nations Environment Programme (UNEP) estimates that over 80% of global wastewater is discharged without adequate treatment, underscoring the vast untapped opportunity for water treatment chemical adoption, including defoamers, across developing regions.

Restraints - Volatility in Raw Material Prices and Supply Chain Disruptions

The defoamers market is susceptible to raw material price volatility, particularly for silicone oils, mineral oils, fatty acids, and polyglycols that form the base of most commercial defoamer formulations. Silicone-based defoamers, which dominate the product landscape, rely on polydimethylsiloxane (PDMS) derivatives, whose production is dependent on silicon metal and methanol pricing, both of which experienced significant supply disruptions during 2021 and 2022. Fluctuations in crude oil prices directly impact the cost of mineral oil-based defoamers and intermediates. These cost pressures compress manufacturer margins, particularly for smaller regional formulators who lack the scale to absorb input cost volatility, creating a restraint on competitive pricing and product accessibility in cost-sensitive markets.

Stringent Environmental Regulations Restricting Conventional Formulations

Tightening environmental legislation governing volatile organic compound (VOC) emissions, chemical toxicity, and aquatic biodegradability is placing increasing pressure on manufacturers of conventional oil-based and solvent-containing defoamer formulations. Regulatory frameworks such as the EU REACH Regulation, the U.S. EPA's VOC emission standards, and food-contact substance regulations enforced by the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) impose strict usage and composition limits for defoamers in food processing, pharmaceutical, and consumer goods applications. Reformulating existing products to comply with these evolving standards requires substantial R&D investment and can entail lengthy regulatory approval processes that constrain product innovation cycles.

Opportunities - Growth in Agrochemical Formulations Creating Premium Defoamer Demand

The rapid global expansion of the agrochemical industry, driven by rising food demand from a growing global population projected to reach 9.7 billion by 2050 per the United Nations, is creating a high-value opportunity for defoamer manufacturers. Defoamers are essential additives in the formulation of pesticides, herbicides, and fertilizers, preventing foam formation during manufacturing, mixing, and spray application processes that can compromise dosage accuracy and application efficiency. The agrochemical sector is one of the fastest-growing application segments for defoamers, with Asia Pacific and Latin America representing the highest-growth demand regions due to intensifying agricultural activity. Manufacturers capable of developing food-safe, biodegradable defoamers compliant with regulatory frameworks such as those of the EPA and EFSA are well-positioned to capture premium pricing in this expanding market segment.

Bio-Based and Sustainable Defoamer Innovation Unlocking New Market Segments

The industry-wide shift toward green chemistry and sustainable specialty chemicals is creating a transformative opportunity for defoamer manufacturers that invest in bio-based and low-environmental-impact formulations. In June 2023, Elementis launched DAPRO BIO 9910, a defoamer made from 96% bio-based carbon content certified to C14 standards, specifically designed for paint applications. In April 2024, Evonik Industries AG introduced TEGO Foamex 16, containing 25% bio-based material, and TEGO Foamex 11 at the American Coatings Show, setting a new sustainability benchmark for waterborne architectural coating defoamers with near-zero VOC and SVOC content. These innovations reflect a broader market movement that rewards first movers with premium pricing and regulatory compliance advantage, particularly in food processing, personal care, and architectural coatings applications.

Category-wise Analysis

Product Type Insights

Silicone-based defoamers represent the leading segment by product type, accounting for approximately 37% of global defoamers revenue in 2025. The dominance of this segment stems from the exceptional performance characteristics of silicone, particularly polydimethylsiloxane (PDMS), based formulations, which deliver superior foam control at low dosage rates, maintain stability across extreme temperatures and pH levels, and are compatible with a broad range of industrial process fluids. These properties make silicone-based defoamers indispensable in high-demand applications including pulp and paper processing, paints and coatings, water treatment, and food and beverage processing. Leading companies including Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Dow Inc., and Bluestar Silicones International are investing in next-generation silicone defoamer formulations. Among the fastest-growing product types, water-based defoamers are projected to register the highest CAGR from 2026 to 2033, driven by mounting preference for eco-friendly, low-toxicity formulations across food processing, pharmaceuticals, and wastewater treatment.

Form Insights

The liquid form segment leads the defoamers market by form, accounting for approximately 55% of total revenue in 2025. Liquid defoamers, whether in neat oil, emulsion, or solution form, offer key operational advantages: ease of accurate dosing, rapid dispersibility in process streams, compatibility with automated chemical dosing systems, and broad substrate compatibility. In high-volume industrial applications, including pulp mills, wastewater treatment plants, paints manufacturing, and food processing facilities, liquid defoamers are the preferred format due to seamless integration with existing process infrastructure. The emulsion and dispersion sub-segment held the highest individual revenue contribution of approximately 41% in 2025 within the broader liquid category. Powder-form defoamers are gaining traction in solid formulation applications such as detergent powders, construction chemicals, and specific agrochemical preparations where shelf stability and ease of transport are priorities.

Application Insights

The pulp and paper segment leads the defoamers market by application, accounting for approximately 27% of global revenue in 2025. This dominance reflects the critical, non-substitutable role of defoamers across multiple stages of paper manufacturing, including kraft pulping, chemical recovery, bleaching, coating, and recycled fiber processing. Foam generation in these processes can cause machine breaks, reduce drainage efficiency, impair product sheet quality, and increase operational downtime, making effective defoaming a production-critical requirement. The expanding global demand for sustainable packaging materials, hygiene products, and tissue paper, driven by e-commerce growth and post-pandemic hygiene awareness, is sustaining incremental defoamer consumption in this sector. Among the fastest growing application segments, agrochemicals are expected to register the highest CAGR from 2026 to 2033, fueled by rising agricultural intensification, expanding crop protection chemical use in Asia and Latin America, and innovation in biodegradable defoamer formulations suited to agrochemical manufacturing requirements.

Regional Insights

North America Defoamers Market Trends and Insights

North America is a leading regional market for defoamers, commanding approximately 28% of global revenue in 2025. The United States is the dominant national market, driven by a mature industrial base with robust demand across pulp and paper, paints and coatings, water treatment, and oil and gas sectors. The U.S. EPA's stringent VOC emission standards and Clean Water Act regulations are compelling industrial operators to transition to low-VOC, water-based, and silicone-based defoamer formulations, directly supporting market growth in compliant product categories. The American Coatings Association plays an important advocacy role in shaping product standards and sustainability practices.

North America is a hub for defoamer innovation, with companies including Dow Inc., Evonik Industries AG, BASF SE, Ashland Inc., and Air Products and Chemicals, Inc. maintaining significant R&D and manufacturing infrastructure in the region. The U.S. oil and gas sector, particularly unconventional shale operations, generates substantial demand for specialized defoamers in drilling muds, produced water treatment, and refinery operations. Ongoing infrastructure renewal and municipal water treatment expansion further sustain defoamer demand, while bio-based and sustainable formulations are being accelerated by corporate sustainability commitments.

Europe Defoamers Market Trends and Insights

Europe holds a well-established and innovation-driven position in the global defoamers market. The region's regulatory environment, governed by the EU REACH Regulation, EU VOC Directive, and EFSA food contact substance standards, is one of the world's most comprehensive, continuously pushing manufacturers toward sustainable, compliant formulations. Germany, France, the United Kingdom, and Spain represent the largest national markets, with Germany serving as a key hub for specialty chemical manufacturing. Major companies including BASF SE, Evonik Industries AG, Wacker Chemie AG, and Clariant AG are headquartered in Europe and lead global product innovation.

In November 2023, BASF expanded its Foamaster and Foamstar defoamer production capacity with a new line at its Dilovasi plant in Turkey, specifically to address growing demand from South-East Europe, the Middle East, and Africa. The pulp and paper sector in Nordic countries and the UK is a significant end-use driver. Europe's expanding water treatment infrastructure investments, supported by the EU Urban Wastewater Treatment Directive revision, are also sustaining defoamer demand. The region is expected to grow at the highest CAGR among developed markets from 2026 to 2033, driven by the accelerating transition to bio-based and low-VOC product formulations.

Asia Pacific Defoamers Market Trends and Insights

Asia Pacific is the largest regional market for defoamers, commanding approximately 38% of global revenue in 2025, and is projected to sustain the highest CAGR among all regions through 2033. The region's market leadership is underpinned by its dominant position in global pulp consumption, approximately 39.8% of the world total, its rapidly expanding paints, coatings, and agrochemical industries, and massive government-led investments in water and wastewater treatment infrastructure. China is the world's largest consumer of defoamers, driven by its dominant manufacturing base across coatings, paper, textiles, and chemical processing. India is an emerging high-growth market, supported by expanding food processing, agrochemical production, and construction activity.

Japan and South Korea maintain mature defoamer markets with strong demand for high-performance silicone and specialty formulations in electronics, food processing, and automotive coatings. ASEAN nations, including Vietnam, Indonesia, and Thailand are experiencing accelerating defoamer demand from industrial expansion and agricultural modernization. Leading multinationals such as Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, and Dow Inc. are expanding their regional production and technical service capabilities to capitalize on Asia Pacific's sustained growth momentum through 2033.

Competitive Landscape

The global defoamers market is characterized by a fragmented competitive structure, with numerous multinational and regional specialty chemical manufacturers operating across diverse product types and application segments. The top players collectively account for a limited share, indicating the absence of strong market concentration and the presence of intense competition across regional and niche markets.

Competition is primarily driven by product performance, regulatory compliance capabilities, and the ability to deliver application-specific formulations supported by strong technical service. Companies are increasingly focusing on expanding their portfolios through innovation and customization to cater to varied industrial requirements. Key business strategies include heightened investment in research and development, particularly in bio-based and low-VOC defoamer technologies, alongside capacity expansions in high-growth regions. Strategic collaborations with end-use industries are also gaining importance, enabling manufacturers to align with evolving regulatory standards and sustainability goals while strengthening long-term customer relationships.

Key Developments:

- June 2025: Evonik Industries launched TEGO® Foamex 8051, a high-performance siloxane-based defoamer for waterborne decorative coatings, offering strong defoaming efficiency, low VOC content, and compliance with global environmental regulations.

- April 2025: Silibase Silicone introduced SilibaseDFX-054N, a high-activity silicone defoamer with performance comparable to FOAM BAN® 1880, designed for water-based systems including industrial cleaning, sewage treatment, and adhesives, offering strong foam suppression and cost efficiency.

Companies Covered in Defoamers Market

- Kemira Oyj

- Air Products and Chemicals, Inc.

- Ashland Inc.

- Bluestar Silicones International

- Dow Inc.

- Evonik Industries AG

- Wacker Chemie AG

- Shin-Etsu Chemical Co., Ltd.

- BASF SE

- Syensqo

- Clariant AG

- KCC Basildon

- Eastman Chemical Company

- Synalloy Chemicals

- Tiny Chempro

- Elementis Plc

- BYK-Chemie GmbH (ALTANA Group)

- Munzing Chemie GmbH

- Nouryon

- Silibase

- Momentive Performance Materials Inc.

Frequently Asked Questions

The global defoamers market is estimated to reach US$ 4.4 billion in 2026, driven by demand from pulp and paper, water treatment, and coatings industries.

Key drivers include growth in pulp and paper, rising wastewater treatment investments, regulatory compliance, and increasing adoption of bio-based defoamers.

Asia Pacific leads due to strong industrial growth, high pulp consumption, and expanding demand across coatings, agrochemicals, and water treatment sectors.

The development of bio-based and low-VOC defoamers presents a major opportunity driven by environmental regulations and sustainability trends.

Key players include BASF SE, Evonik Industries AG, Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical, Kemira Oyj, Clariant AG, Elementis Plc, and BYK-Chemie.