- Bulk Chemicals

- Sulfuric Acid Market

Sulfuric Acid Market Size, Share, and Growth Forecast 2026 - 2033

Sulfuric Acid Market by Raw Material Source (Elemental Sulfur, Base Metal Smelters, Pyrite Ore, Others), by Manufacturing Process (Contact Process, Wet Sulfuric Acid (WSA) Process, Lead Chamber Process, Others), by Grade (Technical Grade, Battery Grade, Chemically Pure/Reagent Grade, Pharmaceutical Grade, Electronic/Ultra-Pure Grade), by End-Use, by Regional Analysis, 2026 - 2033

Sulfuric Acid Market Size and Trend Analysis

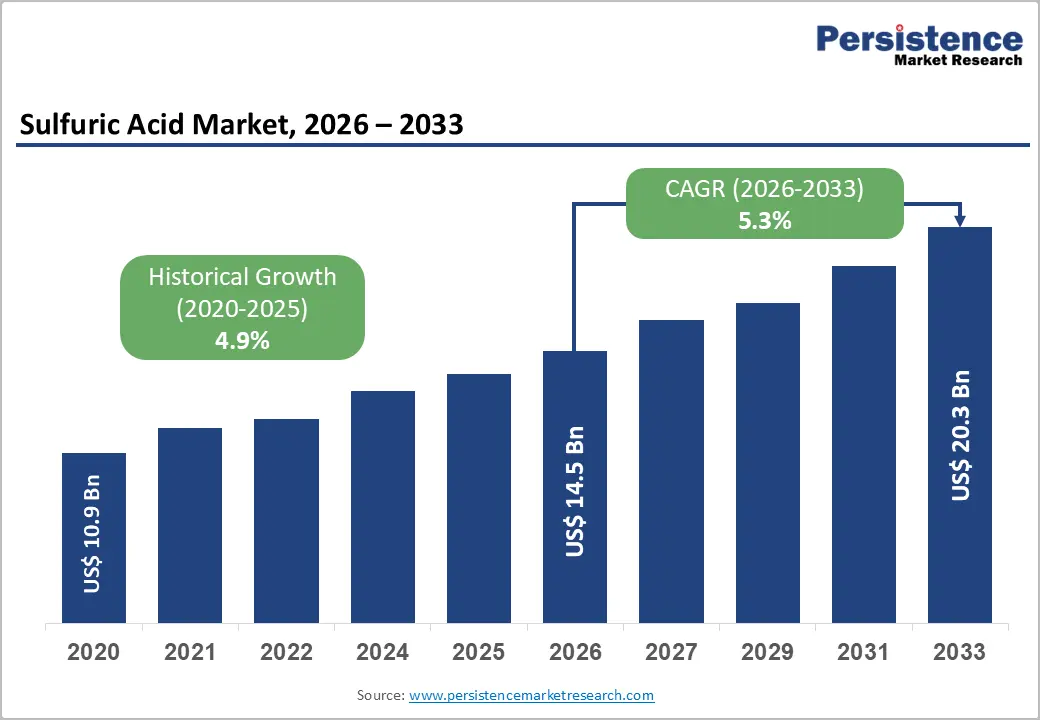

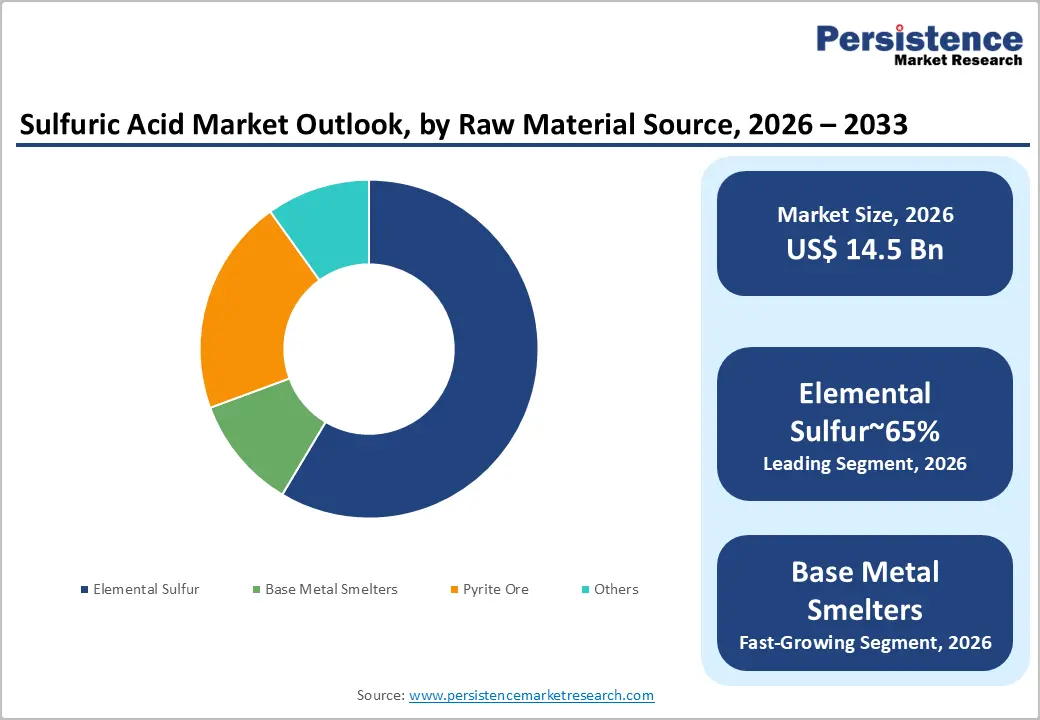

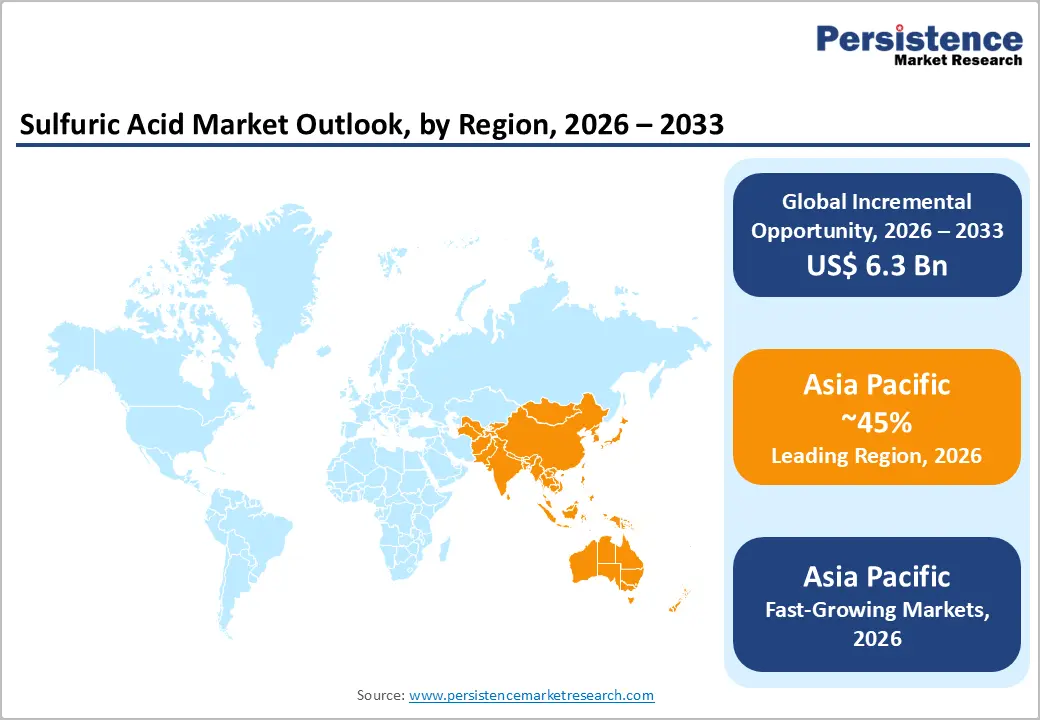

The global sulfuric acid market size is likely to be valued at US$ 14.5 billion in 2026 and is expected to reach US$ 20.8 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033. The sulfuric acid market is experiencing consistent growth underpinned by its indispensable role across agriculture, mining, chemical manufacturing, and the rapidly expanding battery and electronics industries.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the global sulfuric acid market holding 45% share, with China dominating production and consumption through its world's largest fertilizer industry, supported by Japan's smelter by-product acid output and India's rapidly growing fertilizer and chemicals sectors.

- Fastest Growing Region: Asia Pacific also registers the fastest growth, driven by India's expanding DAP and complex fertilizer consumption per the Fertiliser Association of India, South Korea's semiconductor ultra-pure acid demand, and ASEAN's expanding mining and chemicals manufacturing base.

- Dominant Segment: Elemental Sulfur dominates by raw material source with approximately 65% share, reflecting its large-scale recovery from petroleum refining and natural gas desulfurization operations in the Middle East, North America, and Russia.

- Fastest Growing Segment: Battery Grade and Electronic/Ultra-Pure Grade are the fastest growing grade segments, propelled by EV lithium processing demand following IEA's 14 million EV sales in 2023 and semiconductor fab investment under the U.S. CHIPS Act.

- Key Market Opportunity: Ultra-pure sulfuric acid for semiconductor wafer cleaning represents a high-margin growth opportunity, with the U.S. CHIPS Act committing US$ 52 billion to domestic chip manufacturing and over 40 new semiconductor projects announced by the U.S. Department of Commerce.

Market Dynamics

Drivers - Surging Global Fertilizer Demand Driving Phosphoric Acid and Sulfuric Acid Consumption

Agriculture is the single largest end-use sector for sulfuric acid globally, consuming the majority of output through the production of phosphoric acid - an essential intermediate in phosphate fertilizer manufacturing. The Food and Agriculture Organization (FAO) of the United Nations projects that global food production must increase by approximately 50% by 2050 to feed an estimated 9.7 billion people, placing sustained pressure on fertilizer producers to scale output.

The International Fertilizer Association (IFA) reports that global phosphate fertilizer consumption has grown year over year. Key fertilizer producers, including The Mosaic Company, Nutrien Ltd., OCP Group, and PhosAgro, are major sulfuric acid consumers, integrating large-scale sulfuric acid plants directly into their phosphate fertilizer complexes to ensure a reliable acid supply.

Growing Demand from the Metals and Mining Sector for Hydrometallurgical Processing

The global mining industry's expanding use of hydrometallurgical processes - particularly heap leaching and solvent extraction-electrowinning (SX-EW) for copper, nickel, cobalt, and lithium recovery - is generating substantial incremental demand for sulfuric acid. The International Copper Study Group (ICSG) reports that global refined copper production exceeded 26 million tonnes in 2023, with the SX-EW route accounting for a significant and growing share of primary copper output.

The green energy transition's surging demand for battery metals - particularly lithium, cobalt, and nickel - is driving new mine development and expansions of hydrometallurgical processing facilities that consume sulfuric acid at scale. Companies, including Aurubis AG and Boliden Group produce sulfuric acid as a by-product of base metal smelting while simultaneously being significant consumers in refining operations.

Restraints - Stringent Environmental and Safety Regulations Governing Sulfuric Acid Production and Transport

Sulfuric acid is classified as a highly corrosive and hazardous substance subject to stringent regulatory oversight across production, storage, and transportation. The U.S. Environmental Protection Agency (EPA) classifies sulfuric acid as a listed hazardous air pollutant under the Clean Air Act, imposing extensive emission controls and reporting requirements on production facilities.

In the European Union, sulfuric acid is regulated under the REACH regulation and the Seveso III Directive for major accident hazard control. Compliance with these evolving regulatory frameworks increases capital expenditure on emission abatement systems, spill containment infrastructure, and safety management programs, particularly impacting smaller producers with limited balance sheet flexibility.

Price Volatility of Raw Sulfur and Dependence on By-Product Supply from Smelters

Global sulfuric acid production is heavily dependent on elemental sulfur - primarily recovered from oil and natural gas desulfurization - and by-product gas from base metal smelters, both of which are subject to supply and price volatility.

Sulfur prices fluctuated significantly in 2021-2022, with spot prices in some markets swinging by over 150% within a 12-month period, according to S&P Global Commodity Insights. As oil refinery throughputs fluctuate with energy markets and smelter output adjusts to metal prices, sulfuric acid producers face an inherently variable feedstock environment that complicates long-term pricing contracts and margin planning.

Opportunities - Battery-Grade Sulfuric Acid Demand Surge from EV Battery Manufacturing

The lithium-ion battery supply chain is generating a powerful new demand stream for high-purity battery-grade sulfuric acid, used in electrolyte preparation, lithium chemical processing, and nickel-cobalt-manganese (NCM) cathode material production. The International Energy Agency (IEA) reported that global EV sales exceeded 14 million units in 2023, with battery demand growing commensurately.

Lithium refining via the sulfate process - which converts lithium ore into battery-grade lithium hydroxide or carbonate - consumes substantial quantities of sulfuric acid. Governments including the U.S. (via the Inflation Reduction Act) and the European Union (via the Critical Raw Materials Act) are incentivizing domestic battery material processing that will require significant sulfuric acid supply. Companies such as BASF SE and Solvay S.A. are investing in high-purity acid production capabilities to serve this fast-growing premium demand segment.

Expanding Semiconductor and Electronics Fabrication Driving Ultra-Pure Sulfuric Acid Demand

The global semiconductor industry's unprecedented capacity expansion - catalyzed by the U.S. CHIPS and Science Act (committing US$ 52 billion to domestic chip manufacturing) and the EU Chips Act - is creating substantial demand for electronic/ultra-pure grade sulfuric acid used in wafer cleaning (piranha etch solutions), oxidation processes, and photoresist stripping. The Semiconductor Industry Association (SIA) reported global semiconductor sales of over US$ 520 billion in 2023.

Ultra-pure sulfuric acid (with metallic impurities at parts-per-trillion levels) commands significant price premiums over technical grade material, representing a high-margin growth avenue for specialty chemical manufacturers, including PVS Chemicals, Inc. and Nouryon, that invest in advanced purification and quality management capabilities to serve leading chip fabricators.

Category-wise Analysis

By Raw Material Source Insights

Elemental sulfur is the dominant raw material source for sulfuric acid production globally, accounting for an estimated 65% of total sulfuric acid production. Elemental sulfur is primarily recovered as a by-product of petroleum refining and natural gas processing - industries that remove sulfur compounds to comply with low-sulfur fuel standards.

The U.S. Energy Information Administration (EIA) confirms that recovered sulfur from petroleum refining represents the largest single source of global sulfur supply. The dominance of elemental sulfur reflects the geographic distribution of major oil refining and gas processing hubs in the Middle East, North America, and Russia, which export large volumes of sulfur to global acid producers. Key sulfur-to-acid producers include BASF SE and Chemtrade Logistics Inc.

By Manufacturing Process Insights

The contact process dominates the sulfuric acid manufacturing landscape, accounting for an estimated 88% or more of global production. Developed in the early 20th century and continuously refined, the double absorption contact process achieves sulfur trioxide conversion efficiencies exceeding 99.7%, meeting both economic performance requirements and environmental SO2 emission standards set by regulators including the U.S. EPA and European Commission.

Its scalability to very large production capacities (single-train plants producing over 1 million tonnes per year) makes it the preferred process for both stand-alone acid plants and integrated fertilizer complexes. The Wet Sulfuric Acid (WSA) Process is gaining traction for treating dilute sulfur dioxide off-gases from smelters, representing the most significant emerging process alternative.

By Grade Insights

Technical grade sulfuric acid leads the grade segment with an estimated market share of approximately 55%. Technical grade acid - typically 93-98% H2SO4 purity - is the workhorse product used across the highest-volume applications, including phosphate fertilizer production, metal ore leaching, petroleum refining (alkylation), and general chemical manufacturing. Its dominant share reflects the overwhelming scale of agricultural and chemical sector consumption.

The IFA notes that phosphate fertilizer production alone accounts for more than half of global sulfuric acid demand. While Battery Grade and Electronic/Ultra-Pure Grade segments are the fastest growing due to EV and semiconductor expansion, their current absolute volumes remain significantly smaller than the technical grade commodity segment led by producers such as OCP Group and Yunnan Yuntianhua Co., Ltd.

By End-user Insights

Agriculture is the dominant end-use segment for the sulfuric acid market, commanding an estimated share of approximately 54% of global consumption. This dominant position is structural and long-standing - sulfuric acid is a mandatory intermediate in the production of phosphoric acid, which in turn is reacted with ammonia to produce diammonium phosphate (DAP) and monoammonium phosphate (MAP) fertilizers.

The FAO projects global food demand to grow by 50% by 2050, sustaining fertilizer production growth. The Chemicals & Petrochemicals segment is the second largest end-use, covering applications in organic chemical synthesis, petroleum refining alkylation, and dye manufacturing. The Electronics & Semiconductors end-use is the fastest growing, driven by global fab construction investments under the CHIPS Act and EU Chips Act.

Regional Insights

North America Sulfuric Acid Market Trends & Analysis

North America represents a mature yet strategically expanding sulfuric acid market, supported by strong refining integration and regulatory-driven efficiency upgrades. The U.S. dominates regional demand, accounting for ~78% share, with growth driven by semiconductor fabs, battery supply chains, and fertilizer demand. Regional CAGR is estimated at ~4.9% through 2033.

- U.S. Sulfuric Acid Market Size

The U.S. sulfuric acid market was valued at approximately USD 8.5 billion in 2026 and is projected to reach around USD 12.5 billion by 2033, growing at ~5.0% CAGR. Growth is driven by electronic-grade acid demand from semiconductor fabs, battery manufacturing expansion, and sustained fertilizer consumption.

Europe Sulfuric Acid Market Trends, Drivers & Insights

Europe’s sulfuric acid market is technologically advanced and compliance-driven, with strong emphasis on emission control and circular production via smelting. The region accounts for ~22% of global demand, with moderate growth supported by battery materials, specialty chemicals, and regulatory mandates such as REACH and IED.

- Germany Sulfuric Acid Market Size

Germany’s sulfuric acid market is valued at approximately USD 2.2 billion in 2026, projected to reach USD 3.2 billion by 2033 at ~4.5% CAGR. Demand is driven by integrated chemical production, battery materials, and strong industrial consumption across automotive and specialty chemicals sectors.

- U.K. Sulfuric Acid Market Size

The U.K. market is estimated at USD 0.9 billion in 2026, expected to reach USD 1.5 billion by 2033, growing at ~4.0% CAGR. Growth is supported by fertilizer demand, chemical manufacturing, and increasing focus on sustainable industrial practices and emission control technologies.

- France Sulfuric Acid Market Size

France’s sulfuric acid market is valued at around USD 1.1 billion in 2026 and is projected to reach USD 1.6 billion by 2033, growing at ~4.3% CAGR. Key demand drivers include fertilizers, nuclear fuel processing, and growing investments in battery and energy transition industries.

Asia Pacific Sulfuric Acid Market Drivers & Analysis

Asia Pacific dominates the global sulfuric acid market with over 45% share, driven by large-scale fertilizer production, mining, and chemical industries. The region is expected to grow at ~5.5% CAGR, supported by China’s industrial expansion, India’s fertilizer demand, and semiconductor growth in advanced economies.

- China Sulfuric Acid Market Size

China’s sulfuric acid market was valued at approximately USD 7.0 billion in 2026 and is projected to reach USD 11.5 billion by 2033, growing at ~5.8% CAGR. Growth is fueled by phosphate fertilizers, metal processing, and battery materials aligned with industrial policy initiatives.

- India Sulfuric Acid Market Size

India’s market is estimated at USD 1.8 billion in 2026 and is expected to reach USD 3.2billion by 2033, growing at ~6.5% CAGR. Strong demand from fertilizers, chemicals, and refining industries, along with agricultural expansion, drives rapid market growth.

- Japan Sulfuric Acid Market Size

Japan’s sulfuric acid market stands at approximately USD 1.2 billion in 2026 and is projected to reach USD 1.6 billion by 2033, growing at ~4.0% CAGR. Growth is supported by stable demand from electronics, chemicals, and by-product acid generation from smelting operations.

Competitive Landscape

The sulfuric acid market exhibits a moderately fragmented structure at the global level, with no single company dominating worldwide production, given the regional nature of acid distribution (high freight costs limit long-distance trade). Key players, including BASF SE, The Mosaic Company, Nutrien Ltd., and OCP Group, maintain large integrated production positions in their respective regions.

Competitive differentiation is achieved through feedstock integration, production scale, logistics infrastructure, and grade-specific quality capabilities (particularly battery-grade and electronic-grade). R&D focus areas include WSA process optimization for dilute gas streams, advanced purification for high-purity grades, and SO2 emission minimization. By-product acid producers such as Aurubis AG and Boliden Group compete on cost advantage from captive feedstock.

Key Developments:

- March, 2025: Nouryon announced capacity expansion of its high-purity sulfuric acid production in Europe to serve growing demand from semiconductor wafer cleaning applications linked to new EU Chips Act-funded fab construction projects in Germany and the Netherlands.

- October, 2024: Aurubis AG commissioned a new Wet Sulfuric Acid (WSA) plant at its Hamburg smelter complex, upgrading SO2 off-gas recovery to produce commercial-grade sulfuric acid while significantly reducing atmospheric emissions in compliance with EU Industrial Emissions Directive requirements.

- June, 2024: OCP Group announced the commissioning of a new large-scale sulfuric acid production unit at its Jorf Lasfar complex in Morocco, expanding integrated phosphate fertilizer production capacity to meet growing African and global agricultural demand.

Global Sulfuric Acid Market - Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 10.9 Bn |

|

Current Market Value (2026) |

US$ 14.5 Bn |

|

Projected Market Value (2033) |

US$ 20.8 Bn |

|

CAGR (2026-2033) |

5.3% |

|

Leading Region |

Asia Pacific, 45% share |

|

Dominant Raw Material Source |

Elemental Sulfur, 65% share |

|

Top-ranking End Use |

Agriculture, 54% |

|

Incremental Opportunity |

US$ 6.3 Bn |

Companies Covered in Sulfuric Acid Market

- BASF SE

- The Mosaic Company

- AkzoNobel N.V.

- Solvay S.A.

- INEOS Group Holdings S.A.

- Nutrien Ltd.

- PVS Chemicals, Inc.

- Nouryon

- Aurubis AG

- OCP Group

- Chemtrade Logistics Inc.

- Boliden Group

- PhosAgro

- Yunnan Yuntianhua Co., Ltd.

- Groupe Chimique Tunisien

- Coromandel International Ltd.

- Tronox Holdings plc

- Gulf Sulfur Services

Frequently Asked Questions

The global sulfuric acid market is estimated to be valued at US$ 14.5 billion in 2026 and is projected to reach US$20.8 billion by 2033, expanding at a CAGR of 5.3% during the forecast period.

The primary driver is sustained global fertilizer demand - with the FAO projecting food production must grow 50% by 2050 - requiring sulfuric acid as an essential intermediate in phosphoric acid production. The accelerating green energy transition is a second major driver, with EV battery lithium processing and semiconductor fab investments under the U.S. CHIPS Act creating growing demand for battery-grade and electronic ultra-pure sulfuric acid grades.

Agriculture leads the sulfuric acid market by end-use with approximately 54% share, driven by the irreplaceable role of sulfuric acid in phosphoric acid and phosphate fertilizer production. The IFA reports that global phosphate fertilizer consumption continues to grow annually, reflecting rising food production requirements across Asia, Africa, and Latin America that sustain persistent high-volume sulfuric acid demand from integrated fertilizer producers.

Asia Pacific leads the global sulfuric acid market, with China alone accounting for the majority of global production and consumption through its world's largest fertilizer manufacturing base. The region's leadership is further reinforced by Japan's smelter by-product acid industry, India's growing fertilizer and chemicals sectors, and South Korea's semiconductor industry consuming ultra-pure grade sulfuric acid.

Battery-grade and electronic ultra-pure sulfuric acid represent the highest-growth opportunities, aligned with the EV battery manufacturing boom (IEA reporting 14 million EV sales in 2023) requiring acid for lithium chemical processing, and semiconductor fab construction under the U.S. CHIPS Act (US$ 52 billion committed) driving demand for parts-per-trillion purity acid in wafer cleaning and piranha etch applications.